MARKET INSIGHTS

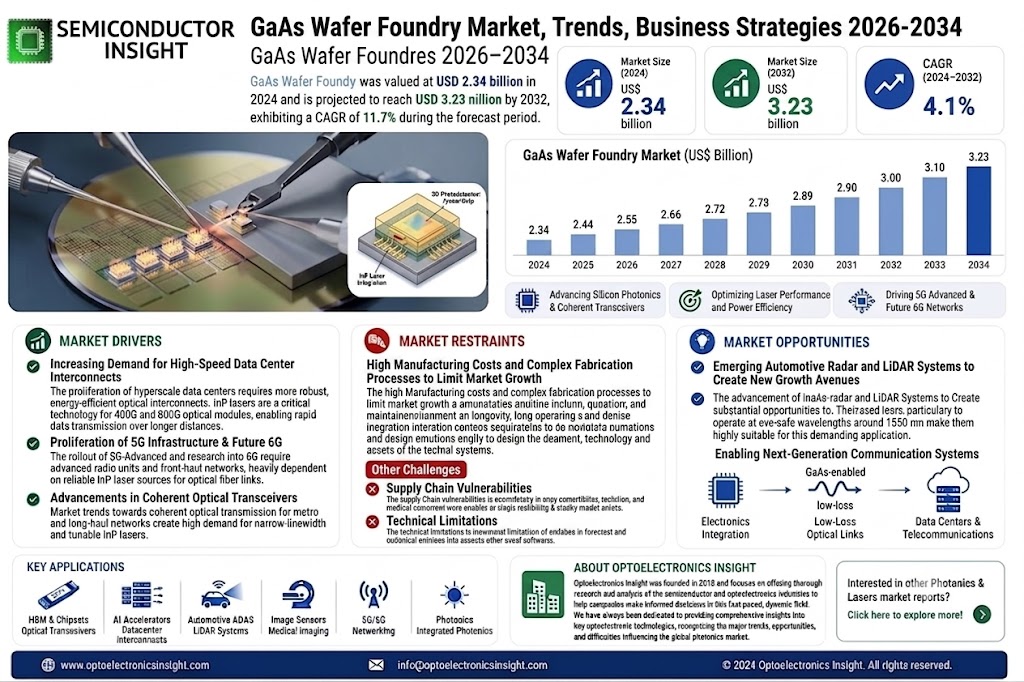

The global GaAs Wafer Foundry Market size was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 3.23 billion by 2032, at a CAGR of 4.1% during the forecast period 2025-2032.

GaAs (Gallium Arsenide) wafers are semiconductor substrates essential for high-frequency, high-power, and optoelectronic applications. These wafers offer superior electron mobility compared to silicon, making them ideal for radio frequency (RF) devices, LEDs, laser diodes, and solar cells. The market comprises two primary foundry models: pure-play foundries that focus solely on manufacturing and IDM (Integrated Device Manufacturer) foundries that handle both design and production.

The market growth is driven by accelerating 5G network deployments, which increased 38% year-over-year in 2023 according to industry reports. While demand remains strong for smartphone and WiFi applications, emerging sectors like automotive radar systems (projected to grow at 12.3% CAGR) and satellite communications are creating new opportunities. However, supply chain constraints and the high cost of GaAs substrates compared to silicon pose challenges. Key players like WIN Semiconductor and Advanced Wireless Semiconductor Company dominate the market, collectively holding over 45% share in 2024 through advanced epitaxial growth technologies.

MARKET DYNAMICS

MARKET DRIVERS

Expanding 5G and Satellite Communication Networks to Drive Demand for GaAs Wafers

The rapid global rollout of 5G infrastructure is significantly boosting the GaAs wafer foundry market. GaAs wafers are increasingly preferred for their superior high-frequency performance and low noise characteristics in RF applications, which are critical for 5G base stations and smartphones. With over 260 commercial 5G networks deployed worldwide and 5G smartphone shipments projected to exceed 1.2 billion units annually, the demand for GaAs-based power amplifiers and RF components continues to grow substantially. This trend is further amplified by the escalating need for high-speed data transmission in both consumer and enterprise applications.

Growing Adoption in Aerospace and Defense Applications to Fuel Market Growth

Defense and aerospace sectors are increasingly adopting GaAs technology for radar systems, electronic warfare, and satellite communication applications. GaAs wafers offer distinct advantages in these applications due to their radiation hardness and reliability in extreme environments. The global defense satellite communication market, valued at over $12 billion, is creating substantial demand for GaAs-based components. Furthermore, modern military systems increasingly require high-performance RF components that can operate across multiple frequency bands, positioning GaAs as the material of choice for these critical applications.

In addition to defense applications, the commercial satellite sector is experiencing significant growth with the rising demand for high-throughput satellites and low-Earth orbit constellations. Major satellite operators are deploying hundreds of new satellites annually, each requiring multiple GaAs-based power amplifiers and RF components, further driving the foundry market.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Fabrication Processes to Limit Market Growth

While GaAs wafers offer superior performance characteristics, their adoption is restrained by significantly higher production costs compared to silicon alternatives. The epitaxial growth process for GaAs requires specialized equipment and strict environmental controls, resulting in production costs up to five times higher than silicon-based solutions. These cost challenges are particularly problematic for price-sensitive consumer applications, where silicon-based technologies continue to dominate market share despite inferior performance characteristics.

Other Challenges

Supply Chain Vulnerabilities

The GaAs foundry market faces persistent supply chain challenges, particularly concerning gallium raw material availability. Over 90% of the world’s gallium supply originates from China, creating potential geopolitical risks and price volatility. Recent export control measures have demonstrated the fragility of this supply chain, compelling manufacturers to seek alternative sources and diversify their supply networks.

Technical Limitations

Though advantageous for RF applications, GaAs technology shows limitations in scaling to smaller process nodes compared to silicon. This constraint makes it less competitive for integrated solutions where size reduction and higher integration density are priorities. Additionally, the material’s thermal conductivity properties present challenges for high-power applications requiring efficient heat dissipation.

MARKET OPPORTUNITIES

Emerging Automotive Radar and LiDAR Systems to Create New Growth Avenues

The rapid evolution of advanced driver assistance systems (ADAS) and autonomous vehicle technologies is creating substantial opportunities for GaAs foundries. Modern automotive radar systems operating at 77-79 GHz frequencies increasingly utilize GaAs-based components for their superior performance in object detection and collision avoidance. With projections indicating over 60 million automotive radar units will ship annually by 2027, this application presents a significant growth opportunity for the GaAs foundry market.

Additionally, the development of next-generation LiDAR systems for autonomous vehicles is creating demand for high-performance optoelectronic components where GaAs technology offers distinct advantages. These emerging applications are expected to complement traditional cellular and satellite communication markets, providing diversified revenue streams for GaAs foundry providers.

➤ Industry analysts project the automotive GaAs component market to grow at a compound annual growth rate exceeding 15% through 2030, driven by increasing ADAS penetration rates across all vehicle segments.

The integration of GaAs technology with other compound semiconductors like gallium nitride (GaN) is creating new opportunities for hybrid solutions that leverage the strengths of both materials. Foundries developing these integrated processes are well-positioned to capitalize on emerging applications in 6G communications, quantum computing, and advanced sensing technologies.

GaAs WAFER FOUNDRY MARKET TRENDS

5G Network Expansion Drives Demand for GaAs Wafer Foundries

The global rollout of 5G infrastructure remains a primary growth driver for the GaAs wafer foundry market, as gallium arsenide (GaAs) wafers enable high-frequency, low-noise performance critical for 5G RF components. With over 1.4 billion 5G connections expected worldwide by 2025, foundries specializing in GaAs-based power amplifiers and RF front-end modules are experiencing increased demand. The inherent physical properties of GaAs – including higher electron mobility and thermal stability compared to silicon – make it indispensable for millimeter-wave applications above 24GHz. Leading foundries are expanding production capacities by 15-20% annually to accommodate orders from major telecom equipment providers, particularly for massive MIMO antenna systems requiring dozens of GaAs chips per unit.

Other Trends

Automotive Radar Adoption

Advanced driver assistance systems (ADAS) and autonomous vehicle development are creating new opportunities for GaAs foundries, as 77GHz automotive radar systems increasingly utilize GaAs-based monolithic microwave integrated circuits (MMICs). The automotive radar segment is projected to grow at a CAGR exceeding 12% through 2030, with each Level 4 autonomous vehicle requiring 8-12 radar units. Foundries with specialized GaAs processes for high-power radar chips are forming strategic partnerships with Tier 1 automotive suppliers, particularly for applications requiring operation in extreme temperature ranges from -40°C to 125°C.

Consolidation and Technology Transitions Reshape Competitive Landscape

The GaAs foundry market is undergoing significant restructuring as IDMs transition toward fab-lite models and pure-play foundries invest in 6-inch wafer migration to improve cost efficiency. While 4-inchGaAs wafers still account for approximately 35% of production capacity, leading foundries are rapidly converting to 6-inch processes that deliver 2.4x more die per wafer. This transition coincides with growing adoption of pHEMT (pseudomorphic high electron mobility transistor) and HBT (heterojunction bipolar transistor) technologies for differentiated performance characteristics. The market has seen multiple strategic acquisitions, with established semiconductor companies acquiring specialized GaAs foundries to secure supply chains for defense, aerospace, and premium consumer applications.

Supply Chain Localization Gains Momentum

Geopolitical factors are accelerating regional GaAs foundry development, particularly in North America and Europe, where governments are implementing semiconductor sovereignty initiatives. The U.S. CHIPS Act has allocated substantial funding for compound semiconductor manufacturing, including GaAs technologies vital for defense applications. European foundries are similarly expanding GaAs capabilities to reduce reliance on Asian supply chains, with several new 6-inch production lines scheduled for 2025-2026. This localization trend is creating opportunities for second-tier foundries to specialize in niche applications like satellite communications and industrial sensors, where GaAs offers distinct performance advantages over silicon-based solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Foundries Invest in GaAs Technology to Capture Growing RF and Optoelectronic Demand

The global GaAs wafer foundry market features a mix of specialized pure-play foundries and integrated device manufacturers (IDMs). WIN Semiconductor dominates the market with approximately 32% revenue share in 2024, driven by its advanced 6-inch wafer production capabilities and strong relationships with RF component manufacturers. The company’s leadership position stems from decades of focused GaAs technology development and strategic partnerships with major wireless IC designers.

Advanced Wireless Semiconductor Company (AWSC) maintains strong market presence through its cost-effective production of GaAs wafers for power amplifiers, holding about 18% market share. Meanwhile, Visual Photonics Epitaxy (VPEC) has emerged as a key player in optoelectronic applications, particularly for VCSELs used in 3D sensing and LiDAR systems.

The competitive landscape is evolving as Chinese players like SANAN Optoelectronics aggressively expand their GaAs production capacity. SANAN’s vertical integration from epitaxy to device manufacturing allows competitive pricing, though quality challenges remain for high-frequency applications. Established Western players face pricing pressure but maintain technological advantages in RF performance and yield rates.

Recent strategic moves include GCS Holdings partnering with major smartphone OEMs to develop customized GaAs processes, while UMC leverages its silicon foundry expertise to offer hybrid silicon/GaAs solutions for 5G mmWave applications.

List of Key GaAs Wafer Foundry Companies Profiled

- WIN Semiconductor (Taiwan)

- Advanced Wireless Semiconductor Company (Taiwan)

- Visual Photonics Epitaxy (Taiwan)

- SANAN Optoelectronics (China)

- TriQuint Semiconductor (U.S.)

- GCS Holdings (U.S.)

- United Microelectronics Corporation (Taiwan)

Market competition intensifies as 5G infrastructure deployment accelerates and automotive radar adoption grows. While pure-play foundries focus on specialty processes, IDMs leverage their system-level expertise to offer complete RF solutions. The industry sees gradual consolidation as smaller players struggle with the capital intensity of advanced GaAs manufacturing.

Segment Analysis:

By Type

Pure-play Foundry Segment Leads Owing to Specialized Manufacturing Capabilities for GaAs Wafers

The market is segmented based on type into:

- Pure-play Foundry

- Subtypes: 4-inch wafers, 6-inch wafers, and others

- IDM Foundry

By Application

Cell Phone Segment Dominates Market Share Due to Rising Demand for 5G-enabled Smartphones

The market is segmented based on application into:

- Cell Phone

- WiFi

- Satellite

- Automotive Radar System

- Others

By End User

Telecom Sector Holds Largest Share with Increasing Deployment of 5G Infrastructure

The market is segmented based on end user into:

- Telecom

- Automotive

- Aerospace & Defense

- Consumer Electronics

- Others

By Wafer Size

6-inch Wafers Gain Preference for Cost-efficiency in RF Applications

The market is segmented based on wafer size into:

- 4-inch wafers

- 6-inch wafers

- Others

Regional Analysis: GaAs Wafer Foundry Market

North America

The North American GaAs wafer foundry market benefits from robust demand in defense, aerospace, and 5G infrastructure sectors, fueled by substantial R&D investments. As of 2022, the semiconductor market in the Americas grew by 17% YoY, reaching $142.1 billion. Key players like TriQuint and WIN Semiconductor support the production of GaAs wafers for high-frequency applications, particularly in automotive radar systems and satellite communications. However, stringent export controls and trade policies regarding advanced semiconductor technologies create operational complexities for market participants. The US CHIPS Act, allocating $52 billion for domestic semiconductor production, could further boost local GaAs manufacturing capabilities, though implementation challenges remain.

Europe

Europe’s GaAs wafer foundry market exhibits steady growth, driven by increasing adoption in automotive electronics and IoT devices. The region’s 12.6% semiconductor market growth in 2022 highlights consistent demand. Companies like UMC leverage Europe’s strong fabless ecosystem, collaborating with RF and photonics designers. Unlike other regions, Europe emphasizes R&D partnerships between universities and corporations, particularly in GaAs-based power amplifiers for 5G applications. However, higher operational costs and reliance on Asian raw material suppliers limit production scalability. The EU Chips Act aims to strengthen semiconductor sovereignty, potentially benefiting GaAs foundries through targeted investments in compound semiconductors.

Asia-Pacific

Asia-Pacific dominates global GaAs wafer production, accounting for over 60% of market share. While the broader semiconductor market declined by 2% in 2022, GaAs foundries in Taiwan (WIN Semiconductors), China (SANAN), and South Korea maintained stable output. China’s focus on semiconductor self-sufficiency through initiatives like ‘Made in China 2025’ has significantly expanded domestic GaAs capacity. The region benefits from mature supply chains and cost-efficient manufacturing, though export restrictions on gallium (critical GaAs raw material) create supply chain uncertainties. Growing 5G deployment across India and Southeast Asia further drives demand for GaAs-based RF components, with foundries adapting to accommodate higher-volume, lower-margin production models.

South America

South America represents a nascent but strategically emerging market for GaAs wafers, primarily serving local telecom infrastructure needs. Brazil leads regional adoption through partnerships with global IDMs for automotive radar and satellite communication systems. However, limited local expertise in compound semiconductor fabrication results in heavy reliance on imports. Economic instability and underdeveloped semiconductor policies hinder large-scale investments in GaAs foundries. Recent free trade agreements with Asian manufacturers could facilitate technology transfer, but progress remains slow compared to more mature markets. The region shows potential for growth in test and assembly operations rather than front-end manufacturing.

Middle East & Africa

This region demonstrates incremental growth in GaAs wafer applications, primarily in defense and oil/gas sensor markets. While lacking significant local foundry capabilities, countries like Israel and UAE import GaAs components for specialized military and aerospace applications. The absence of comprehensive semiconductor ecosystems and limited technical workforce pose barriers to establishing local GaAs production facilities. However, sovereign wealth funds in Gulf nations have shown interest in investing in semiconductor technologies as part of broader economic diversification plans. Partnerships with established foundries for knowledge transfer could create niche opportunities, particularly for high-reliability GaAs devices used in extreme environments.

Report Scope

This market research report provides a comprehensive analysis of the global and regional GaAs Wafer Foundry markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global GaAs Wafer Foundry market was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 3.23 billion by 2032, growing at a CAGR of 4.1% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Pure-play Foundry, IDM Foundry), application (Cell Phone, WiFi, Satellite, Automotive Radar System, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market, driven by semiconductor manufacturing hubs in China, Japan, and South Korea.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include WIN Semiconductor, Advanced Wireless Semiconductor Company, and Visual Photonics Epitaxy.

- Technology Trends & Innovation: Assessment of emerging semiconductor fabrication technologies, integration of AI in wafer production, and evolving industry standards for GaAs wafer manufacturing.

- Market Drivers & Restraints: Evaluation of factors driving market growth (5G deployment, automotive radar demand) along with challenges (supply chain constraints, high production costs).

- Stakeholder Analysis: Insights for semiconductor manufacturers, foundry operators, equipment suppliers, and investors regarding strategic opportunities in the GaAs wafer ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global GaAs Wafer Foundry Market?

-> GaAs Wafer Foundry Market size was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 3.23 billion by 2032, at a CAGR of 4.1% during the forecast period 2025-2032.

Which key companies operate in Global GaAs Wafer Foundry Market?

-> Key players include WIN Semiconductor, Advanced Wireless Semiconductor Company, Visual Photonics Epitaxy, SANAN, TriQuint, GCS, and UMC, among others.

What are the key growth drivers?

-> Key growth drivers include 5G infrastructure deployment, increasing demand for automotive radar systems, and growing WiFi applications.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for the largest share of global GaAs wafer production and consumption.

What are the emerging trends?

-> Emerging trends include advancements in 6-inch and 8-inch wafer production, integration of AI in fabrication processes, and development of high-performance GaAs solutions for 5G applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...