MARKET INSIGHTS

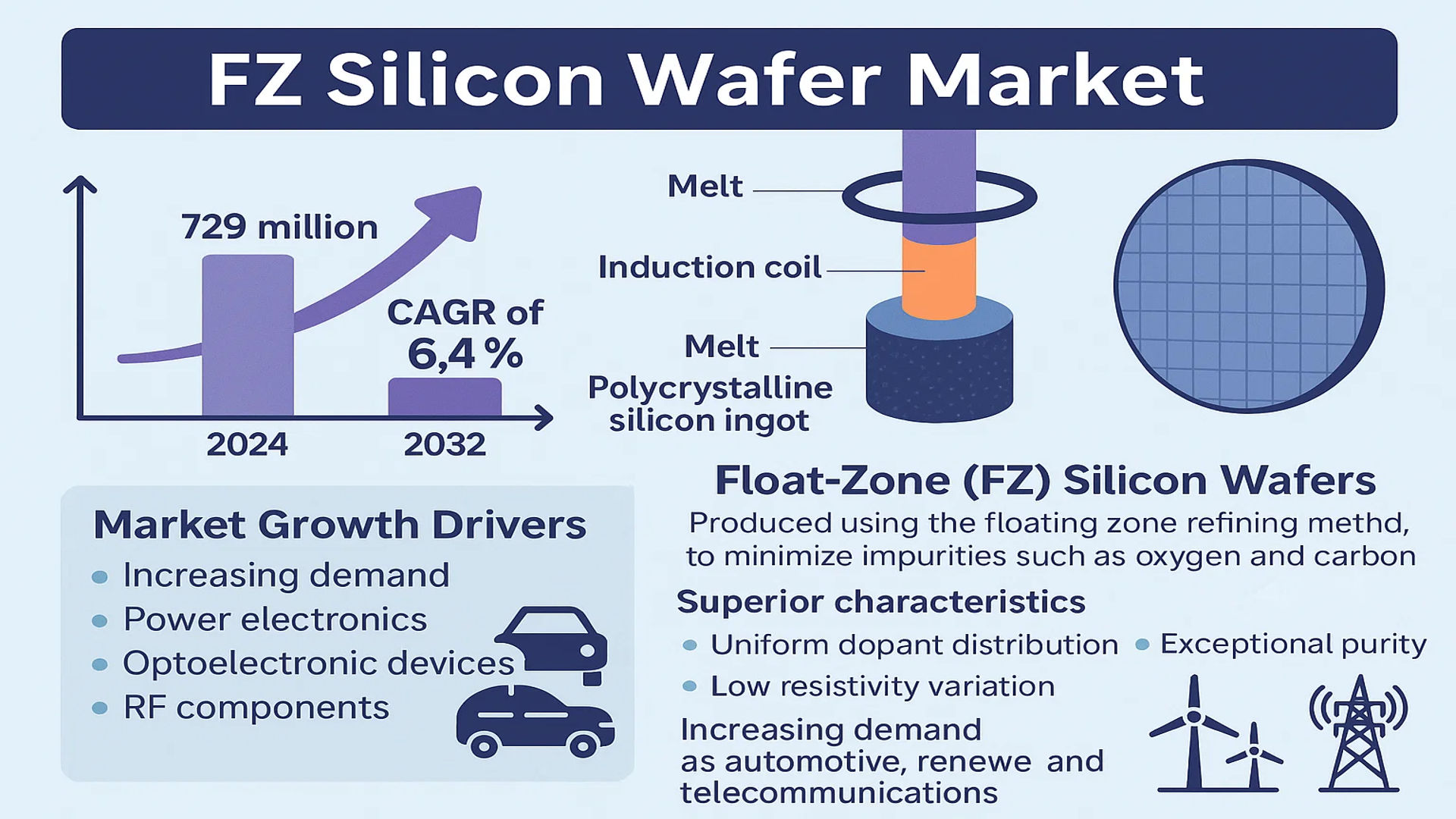

The global FZ Silicon Wafer Market was valued at 729 million in 2024 and is projected to reach US$ 1180 million by 2032, at a CAGR of 6.4% during the forecast period.

Float-Zone (FZ) Silicon Wafers are ultra-pure silicon substrates produced using the floating zone refining method, which minimizes oxygen and carbon impurities. This technique involves melting a polycrystalline silicon ingot with an RF induction coil, allowing a single crystal to solidify atop a seed crystal. The resulting wafers exhibit superior characteristics such as uniform dopant distribution, low resistivity variation, high carrier lifetime, and exceptional purity—making them ideal for high-performance applications.

The market growth is driven by increasing demand for power electronics, optoelectronic devices, and RF components in industries such as automotive, renewable energy, and telecommunications. Additionally, advancements in semiconductor manufacturing and the rise of IoT applications are accelerating adoption. Key players like Shin-Etsu Chemical, SUMCO, and GlobalWafers dominate the market, with 8-inch wafers being the most sought-after segment due to their versatility in power device fabrication.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Efficiency Power Electronics Driving FZ Silicon Wafer Adoption

The global shift toward energy-efficient power devices is significantly boosting demand for float-zone silicon wafers. FZ wafers offer superior performance in power electronic components like IGBTs and MOSFETs due to their exceptionally low impurity levels and high resistivity. The power electronics market is projected to grow at over 10% annually through 2030, with FZ wafers becoming the substrate of choice for applications requiring minimal energy losses and maximum thermal stability. Semiconductor manufacturers are increasingly adopting FZ technology as vehicle electrification and renewable energy systems demand more robust power management solutions.

Proliferation of 5G and RF Devices Accelerating Market Growth

The rapid expansion of 5G networks globally is creating substantial demand for high-frequency RF components manufactured using FZ silicon wafers. Compared to CZ wafers, FZ wafers demonstrate superior signal integrity at high frequencies, making them ideal for 5G base stations and satellite communication equipment. With over five million 5G base stations expected to be deployed by 2025, semiconductor foundries are scaling up production of FZ-based RF devices. The unique dielectric properties of FZ silicon enable lower signal loss, which is critical for maintaining network performance in next-generation wireless infrastructure.

Growing Demand for High-Performance Sensors in Automotive and Industrial Applications

Automotive electrification and industrial automation trends are driving adoption of high-precision sensors that rely on FZ silicon wafers. The exceptional purity and uniformity of FZ wafers make them ideal for manufacturing sensitive MEMS sensors used in advanced driver assistance systems (ADAS), industrial robotics, and medical diagnostic equipment. As vehicles incorporate more autonomous functions and factories implement Industry 4.0 technologies, demand for these high-performance sensors is expected to grow at over 15% annually. FZ wafers’ ability to maintain consistent electrical properties under extreme conditions gives them a competitive advantage in these mission-critical applications.

➤ The automotive semiconductor market, where FZ wafers are increasingly utilized, is projected to reach $90 billion by 2030, demonstrating the significant growth potential for high-quality silicon substrates.

MARKET RESTRAINTS

High Production Costs and Limited Manufacturing Capacity Creating Supply Constraints

The specialized nature of FZ silicon wafer production presents significant barriers to market expansion. FZ crystal growth requires expensive vacuum equipment and consumes significantly more energy than conventional CZ methods, with production costs approximately 30-40% higher. This cost premium limits adoption in price-sensitive applications despite the performance advantages. Currently, only a handful of manufacturers possess the technical expertise to produce large-diameter FZ wafers at commercial scale, creating bottlenecks in the supply chain. The capital-intensive nature of expanding FZ production lines has constrained capacity growth despite increasing demand.

Technical Challenges in Larger Wafer Diameter Production

While the industry is transitioning toward larger wafer diameters for improved economies of scale, FZ technology faces unique challenges in scaling beyond 200mm. The physics of the float-zone process become increasingly complex at larger diameters, with higher risks of crystal defects and lower yields. Currently, only about 15% of FZ wafer production utilizes 300mm technology, compared to over 80% for CZ wafers. This limitation restricts FZ wafer adoption in advanced logic and memory applications where large wafer sizes are essential for cost efficiency. Manufacturers are investing in new zone refining techniques to overcome these technical hurdles, but progress remains incremental.

Competition from Alternative Semiconductor Materials

Emerging wide-bandgap semiconductor materials like silicon carbide and gallium nitride are gaining traction in power electronics applications traditionally dominated by FZ silicon. These materials offer superior performance in high-voltage, high-temperature applications, with adoption growing at over 25% annually in automotive and energy sectors. While FZ silicon maintains advantages in cost and manufacturing maturity for many applications, material science advancements are gradually eroding its market share in premium power device segments. Manufacturers must continue improving FZ wafer quality and lowering costs to remain competitive against these alternative substrates.

MARKET OPPORTUNITIES

Expansion in Renewable Energy Infrastructure Creating New Demand

The global transition to renewable energy is generating significant opportunities for FZ silicon wafer manufacturers. Solar inverters, wind turbine converters, and grid-scale energy storage systems increasingly require the high-power handling capabilities offered by FZ-based power devices. With worldwide renewable energy capacity expected to double by 2030, the addressable market for these applications could expand by over $500 million for FZ wafer suppliers. Manufacturers are developing specialized wafer specifications optimized for power conversion efficiency in renewable energy systems.

Emerging Applications in Quantum Computing and Photonics

Cutting-edge technologies like quantum computing and integrated photonics are creating new high-value applications for ultra-pure FZ silicon wafers. The exceptional material properties of FZ silicon make it an ideal substrate for qubit implementations and silicon photonics components. Research institutions and technology companies are increasingly specifying FZ wafers for prototype quantum devices and optical interconnects. While these applications currently represent a small portion of the market, commercialization breakthroughs could drive exponential demand growth in the latter half of the decade.

Regional Capacity Expansion Initiatives Reducing Supply Chain Risks

Recent geopolitical developments have accelerated investments in regional semiconductor supply chains, including specialty wafer production. Governments across North America, Europe, and Asia are providing substantial incentives for domestic FZ wafer manufacturing capabilities. These initiatives are enabling market expansion through new production facilities and technology transfer programs. Leading manufacturers are establishing strategic partnerships with research institutions to develop next-generation FZ crystal growth techniques while addressing the industry’s skilled labor shortage through targeted training programs.

FZ SILICON WAFER MARKET TRENDS

Expansion of Power Electronics Market Driving FZ Silicon Wafer Demand

The increasing adoption of power discrete devices, including IGBTs and power MOSFETs, is accelerating demand for high-purity Float-Zone (FZ) silicon wafers. These wafers offer superior resistivity control and lower defect density compared to traditional Czochralski (CZ) wafers, making them essential for energy-efficient power modules. The automotive industry’s transition to electric vehicles has increased requirements for reliable semiconductor components, with FZ wafer shipments for power electronics growing at approximately 8.3% CAGR between 2022-2024. Furthermore, advancements in 5G infrastructure are expanding applications in RF devices that require low-loss silicon substrates.

Other Trends

Renewable Energy Adoption

The global shift toward solar energy continues to create opportunities for FZ silicon wafers in photovoltaic applications where high carrier lifetime reduces recombination losses in solar cells. While traditional solar panels predominantly use CZ wafers, premium efficiency modules increasingly incorporate FZ silicon, particularly in concentrated photovoltaic (CPV) systems. Recent R&D efforts have demonstrated FZ-based solar cells achieving over 26% conversion efficiency in laboratory settings, suggesting potential for broader adoption as manufacturing costs decline.

Manufacturing Consolidation and Technological Innovation

The FZ silicon wafer industry remains highly concentrated among a few specialty manufacturers due to significant technical barriers in crystal growth processes. Leading producers are investing in diameter scaling from traditional 8-inch wafers toward 12-inch formats to meet semiconductor industry demands for larger substrates. However, yield challenges at larger diameters maintain price premiums of 30-45% over equivalent CZ wafers. Concurrently, novel doping techniques are enhancing wafer uniformity, with some manufacturers achieving resistivity variations below ±5% across 300mm wafers – a critical specification for power IC applications.

Regional Supply Chain Dynamics

Geopolitical factors are reshaping FZ wafer supply chains, with Japan maintaining its dominant position as both producer and consumer, accounting for nearly 40% of global capacity. Meanwhile, North American and European markets show accelerated growth in wafer sourcing as part of semiconductor sovereignty initiatives, with fab projects driving projected demand increases of 12-15% annually through 2027. The Asia-Pacific region, particularly China, demonstrates the fastest expansion in FZ wafer consumption at 7.63% CAGR, though domestic production still lags behind technological leaders in Japan and Germany.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Expand Production Capacity to Meet Rising Demand for High-Purity Wafers

The global FZ silicon wafer market features a concentrated competitive landscape dominated by a few major manufacturers that control significant production capacities. Shin-Etsu Chemical commands a leading position, owing to its technological expertise in high-purity silicon production and extensive global distribution network across semiconductor hubs in Asia, North America and Europe. The company accounted for over 35% of global FZ wafer production capacity in 2024.

SUMCO Corporation and Siltronic AG maintain strong market positions through specialized FZ wafer manufacturing facilities and long-term supply agreements with major power semiconductor manufacturers. These companies benefit from vertically integrated production processes that ensure strict quality control from polysilicon refining to final wafer polishing.

Several Chinese manufacturers including Zhonghuan Advanced Semiconductor Materials and GRINM Semiconductor Materials are rapidly expanding their market presence. These firms are investing heavily in production capacity while leveraging government support for domestic semiconductor material supply chains. Their growth reflects the strategic importance of FZ wafers in power electronics and new energy applications.

List of Major FZ Silicon Wafer Manufacturers

- Shin-Etsu Chemical (Japan)

- SUMCO Corporation (Japan)

- Siltronic AG (Germany)

- GlobalWafers (Taiwan)

- Zhonghuan Advanced Semiconductor Materials (China)

- GRINM Semiconductor Materials (China)

- Beijing Jingyuntong Technology (China)

- Luoyang Hongtai Semiconductor (China)

- Chengdu Qingyang Electronic (China)

Segment Analysis:

By Type

8-Inch FZ Silicon Wafers Dominate the Market Due to High Demand in Power Electronics and MEMS Applications

The market is segmented based on wafer size into:

- Less than 6-inch

- 8-inch

By Application

Power Discrete Devices Segment Leads Due to Increased Adoption in Electric Vehicles and Renewable Energy Systems

The market is segmented based on application into:

- Power Discrete Devices

- Diodes

- Thyristors

- IGBTs

- Power MOSFETs

- Optoelectronic Devices

- RF Devices

- Other Applications

By End-User Industry

Semiconductor Manufacturing Segment Holds Major Share Due to Growing Chip Demand Across Sectors

The market is segmented based on end-user industries into:

- Semiconductor Manufacturing

- Electronics

- Solar Energy

- Research & Development

By Purity Level

Ultra-High Purity Segment Prevails Due to Critical Requirements in High-Performance Electronics

The market is segmented based on purity levels into:

- Standard Purity

- High Purity

- Ultra-High Purity

Regional Analysis: FZ Silicon Wafer Market

Asia-Pacific

As the leading global region for FZ silicon wafer production and consumption, Asia-Pacific commands the largest market share, driven by Japan’s dominance with over 40% of global wafer production. The region is projected to sustain high growth, supported by China’s rapid semiconductor expansion and Japan’s technological leadership in high-purity wafer manufacturing. China’s market alone is forecast to grow at 7.63% CAGR through 2029, fueled by government semiconductor self-sufficiency initiatives and thriving power electronics sectors. While Japan’s Shin-Etsu and SUMCO lead in FZ wafer technology, Chinese players like Zhonghuan Advanced Semiconductor Materials are rapidly scaling production to meet domestic demand for power devices and solar applications. The concentration of major electronics manufacturers and strong R&D ecosystems position APAC as both the innovation hub and volume driver for FZ wafers.

North America

The North American market prioritizes high-performance FZ wafers for specialized applications in aerospace, defense, and next-generation power electronics. With growing emphasis on domestic semiconductor production through initiatives like the CHIPS Act, localized FZ wafer capacity is receiving increased investment. The market demonstrates steady 6.08% CAGR projections through 2029, led by demand for ultra-pure wafers in RF devices and MEMS sensors. Key technological drivers include 5G infrastructure rollout and electric vehicle adoption, both requiring FZ wafers’ superior electronic properties. Major North American semiconductor fabs collaborate closely with wafer suppliers to develop application-specific solutions, though production remains dependent on imports from Japanese and German manufacturers for the most advanced specifications.

Europe

Europe maintains a strong position in the FZ wafer value chain through technologically advanced producers like Siltronic AG, specializing in high-resistivity wafers for automotive and industrial applications. The region benefits from established R&D pipelines between wafer manufacturers and academic institutions, driving innovations in wafer purification and doping processes. Growing demand stems from automotive electrification and renewable energy sectors, where FZ wafers enable more efficient power conversion systems. European wafer producers emphasize sustainability in manufacturing processes, aligning with stringent EU environmental regulations. While facing cost pressures from Asian competitors, European manufacturers retain leadership in customized wafer solutions for mission-critical applications in medical equipment and scientific instrumentation.

South America

The South American FZ wafer market remains in nascent stages, primarily serving industrial electronics maintenance requirements rather than high-volume semiconductor production. Limited local manufacturing capabilities create dependency on imports, with Brazil constituting the largest regional market. Emerging opportunities exist in renewable energy applications, particularly for solar power infrastructure utilizing high-efficiency FZ-based cells. However, economic instability and lack of specialized semiconductor ecosystems restrain market expansion. Some transnational wafer producers maintain distribution networks in major industrial centers, but the region lacks the scale to justify localized FZ wafer production facilities. Long-term growth potential hinges on integration into global semiconductor supply chains and technology transfer agreements.

Middle East & Africa

This developing market shows selective demand for FZ wafers primarily in oil/gas sensing applications and telecommunications infrastructure projects. Countries like Israel demonstrate advanced capabilities in wafer-based sensor development, while Gulf nations invest in downstream electronics manufacturing. The absence of domestic wafer production facilities creates total import dependency, with Japanese and European suppliers dominating high-end applications. Strategic investments in technology hubs, particularly in UAE and Saudi Arabia, may stimulate future demand for specialized wafers. Growth remains constrained by limited semiconductor manufacturing bases, though increasing focus on smart city initiatives and renewable energy projects could drive adoption of FZ wafers in power management systems over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the global FZ Silicon Wafer market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global FZ Silicon Wafer market was valued at USD 729 million in 2024 and is projected to reach USD 1180 million by 2032, growing at a CAGR of 6.4%.

- Segmentation Analysis: Detailed breakdown by product type (Less than 6 inch, 8 inch), application (Power Discrete Devices, Optoelectronic Devices, RF Device, Others), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis. Asia-Pacific dominates with Japan accounting for over 40% of global silicon wafer production.

- Competitive Landscape: Profiles of leading players including Shin-Etsu Chemical, SUMCO, GlobalWafers, Siltronic AG, and Zhonghuan Advanced Semiconductor Materials, who collectively hold significant market share.

- Technology Trends & Innovation: Assessment of float-zone refining technology advancements, ultra-pure wafer fabrication techniques, and integration in power electronics and photovoltaic applications.

- Market Drivers & Restraints: Evaluation of IoT proliferation, renewable energy demand, and microelectronics innovation as growth drivers, along with supply chain constraints and high production costs as challenges.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, equipment suppliers, investors, and policymakers regarding market opportunities and technological evolution.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global FZ Silicon Wafer Market?

-> FZ Silicon Wafer Market was valued at 729 million in 2024 and is projected to reach US$ 1180 million by 2032, at a CAGR of 6.4% during the forecast period.

Which key companies operate in Global FZ Silicon Wafer Market?

-> Key players include Shin-Etsu Chemical, SUMCO, GlobalWafers, Siltronic AG, Zhonghuan Advanced Semiconductor Materials, and GRINM Semiconductor Materials.

What are the key growth drivers?

-> Key growth drivers include rising demand for power electronics, IoT proliferation, renewable energy adoption, and advancements in semiconductor fabrication technologies.

Which region dominates the market?

-> Asia-Pacific is the dominant region, with Japan being the largest producer accounting for over 40% of global silicon wafer production.

What are the emerging trends?

-> Emerging trends include development of larger diameter wafers, ultra-high purity fabrication techniques, and increasing adoption in photovoltaic applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...