Market Insights

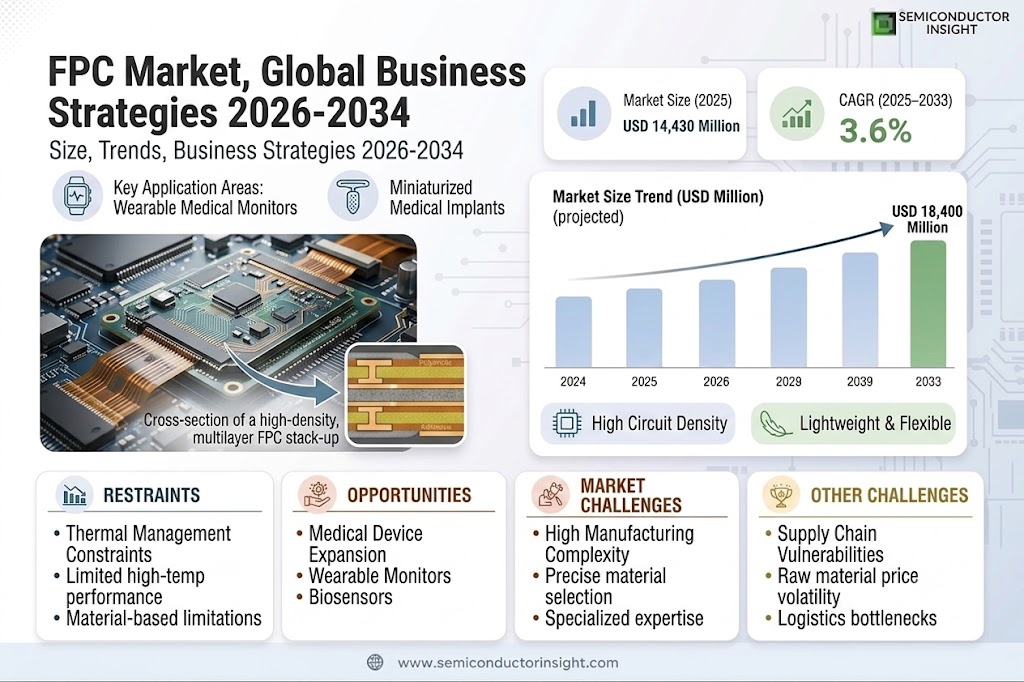

Global FPC Market was valued at USD 14,430 million in 2025 and is projected to reach USD 18,400 million by 2033, exhibiting a CAGR of 3.6% during the forecast period.

The top five players Nippon Mektron, Suzhou Dongshan Precision, SEI, ZDT, and Flexium collectively hold a dominant market share of over 51.02%.

Flexible Printed Circuits (FPCs) are lightweight, high-density interconnect solutions used across industries for their adaptability in compact electronic designs. These circuits consist of conductive traces laminated between flexible insulating materials, enabling bending and folding without compromising electrical performance. Key product segments include single-layer, double-layer, multi-layer, and rigid-flex circuits.

The market growth is driven by rising demand for miniaturized electronics in consumer devices like smartphones and wearables where multi-layer FPCs command a 55% market share. Consumer electronics alone account for approximately 19% of total FPC applications. Technological advancements in automotive electronics and medical devices further propel adoption, while Asia-Pacific leads production with major manufacturers expanding capacity to meet global demand.

MARKET DRIVERS

Growing Demand for Miniaturization in Electronics

FPC Market is experiencing significant growth due to the rising demand for flexible printed circuits in compact electronic devices. Industries such as consumer electronics, automotive, and medical devices increasingly require lightweight, thin, and flexible circuitry solutions. FPC Market benefits from innovations in wearable technology and foldable smartphones, where traditional rigid PCBs cannot meet design requirements.

Advancements in Automotive Electronics

Electric and autonomous vehicles are propelling the FPC Market forward, as flexible circuits enable seamless integration of advanced driver assistance systems (ADAS) and infotainment solutions. With automotive manufacturers prioritizing lightweight components, the adoption of FPCs in vehicle electronics is projected to grow by over 9% annually.

Additionally, the rapid rollout of 5G networks and IoT devices is accelerating FPC demand, as these applications require high-frequency signal transmission capabilities that flexible circuits provide.

MARKET CHALLENGES

High Manufacturing Complexity

Despite strong growth prospects, the FPC Market faces challenges related to the complex manufacturing processes involved in producing high-quality flex circuits. Precise material selection, etching techniques, and multilayer lamination require specialized expertise, leading to higher production costs compared to traditional PCBs.

Other Challenges

Supply Chain Vulnerabilities

FPC Market is susceptible to disruptions in raw material availability, particularly for polyimide films and conductive adhesives. Geopolitical tensions and logistics bottlenecks have caused price volatility in recent years.

MARKET RESTRAINTS

Thermal Management Constraints

Flexible printed circuits face limitations in high-temperature applications due to their material composition. While innovative substrates are being developed, current FPC solutions struggle to match the thermal performance of rigid PCBs in industrial and aerospace applications, restricting market penetration in these sectors.

MARKET OPPORTUNITIES

Emerging Applications in Medical Devices

FPC Market is poised for expansion in the healthcare sector, where flexible circuits enable breakthroughs in miniaturized medical implants and diagnostic equipment. With wearable health monitors and biosensors gaining traction, medical applications could account for 15% of FPC revenue by 2026.

FPC Market (Flexible Printed Circuit) Trends

Steady Growth Projected for Global FPC Market

Global FPC Market is projected to grow from USD 14.43 billion in 2025 to USD 18.4 billion by 2033, at a 3.6% CAGR. This growth is driven by increasing demand from consumer electronics and automotive sectors, where flexible circuits enable compact, lightweight designs. Asia dominates production, with key manufacturers concentrated in Japan, China, and South Korea.

Other Trends

Market Segmentation by Product Type

Multi-layer circuits dominate the FPC Market with 55% share, followed by double-layer (23%) and rigid-flex circuits (15%). The multi-layer segment’s growth reflects increasing complexity in electronic devices requiring higher circuit density. Single-layer circuits maintain relevance in cost-sensitive applications with 7% market share.

Application-Specific Growth Patterns

Consumer electronics leads FPC applications (19% share), with increasing adoption in smartphones and wearables. Automotive applications show the fastest growth (13% share) as vehicles incorporate more electronic systems. Medical applications are expanding due to diagnostic and monitoring device miniaturization, currently holding 9% market share.

The top five FPC manufacturers (Nippon Mektron, Suzhou Dongshan Precision, SEI, ZDT, Flexium) control 51% of the market. Competitive strategies include vertical integration and R&D investments in high-density interconnect technologies. Emerging players focus on niche applications like aerospace (7% market share) where reliability requirements create barriers to entry.

Regional Market Dynamics

Asia accounts for 78% of FPC production, led by China (42%), Japan (19%), and South Korea (11%). North America maintains 12% share, specialized in high-reliability applications. Europe’s 8% market share focuses on automotive and industrial uses. Regional growth correlates with electronics manufacturing clusters and supply chain advantages.

COMPETITIVE LANDSCAPE

Key Industry Players

Top 5 Players Dominate 51.02% of the Global FPC Market

Global Flexible Printed Circuit (FPC) Market is moderately consolidated, with Nippon Mektron, Suzhou Dongshan Precision, SEI, ZDT, and Flexium collectively controlling over half of the market share. Nippon Mektron leads with advanced multi-layer circuit technology, particularly serving high-end consumer electronics and automotive applications. Japanese and Chinese manufacturers dominate production, benefiting from established supply chains and significant R&D investments in flexible electronics.

Specialized players like Fujikura and Daeduck Electronics focus on niche segments including aerospace-grade FPCs and medical device applications. Emerging Asian manufacturers such as Kinwong Electronic and Hongxin are gaining traction through competitive pricing and rapid prototyping capabilities. The market sees increasing competition in the rigid-flex circuit segment, with ICHIA and Interflex introducing innovative solutions for compact wearable devices.

List of Key FPC Companies Profiled

- Nippon Mektron

- Suzhou Dongshan Precision

- SEI

- ZDT

- Flexium

- Fujikura

- CAREER

- SIFLEX

- Bhflex

- Interflex

- Hongxin

- Kinwong Electronic

- ICHIA

- AKM

- Daeduck Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi-Layer Circuit dominates due to:

|

| By Application |

|

Consumer Electronics leads with:

|

| By End User |

|

OEMs represent the key customer base because:

|

| By Material Type |

|

Polyimide maintains dominance due to:

|

| By Manufacturing Process |

|

Subtractive Process remains prevalent because:

|

Regional Analysis: Asia-Pacific FPC Market

East Asia Dominates FPC Adoption

China accounts for over 60% of global FPC production capacity, with clustered facilities in Guangdong and Jiangsu provinces. The country’s electronics manufacturing scale creates sustained demand for flexible circuits across consumer devices, automotive systems, and industrial applications.

Japanese suppliers lead in high-performance FPC solutions for automotive and medical applications, specializing in ultra-thin and heat-resistant flex circuits. Their precision manufacturing capabilities support advanced applications requiring reliability under extreme conditions.

South Korean FPC manufacturers excel in display-related flexible circuits, supplying major panel makers with high-precision interconnects for foldable devices. The country’s R&D investments in flexible electronics drive innovation in FPC materials and processes.

Southeast Asian nations are developing FPC manufacturing capabilities as companies diversify supply chains. Countries like Vietnam and Thailand attract investments for mid-range FPC production, complementing East Asia’s high-end capabilities.

North America

The North American FPC Market thrives on specialized, high-value applications in aerospace, defense, and medical devices. U.S.-based designers focus on custom solutions with stringent reliability requirements, leveraging local expertise in advanced materials and ruggedized designs. The region sees growing adoption of FPCs in next-gen automotive electronics and wearable technologies, supported by strong R&D ecosystems and collaborations between manufacturers and end-users.

Europe

European FPC demand centers on automotive and industrial applications, with German and French manufacturers leading in precision flex circuits for automotive sensors and control systems. Strict environmental regulations drive innovation in sustainable FPC materials and manufacturing processes. The medical device sector presents significant growth opportunities for biocompatible flexible circuit solutions.

South Asia

India emerges as a promising FPC Market with expanding electronics manufacturing and growing domestic demand for consumer electronics. Government initiatives to boost local production create opportunities for FPC suppliers, though the region currently depends on imports for advanced flex circuit technologies. Cost competitiveness makes India attractive for medium-complexity FPC production.

Middle East & Africa

The MEA region shows nascent but growing FPC adoption, primarily serving industrial equipment and telecommunications infrastructure. Local assembly of electronic components drives demand for basic flexible circuits, while high-value applications remain limited. Strategic logistics locations could position certain countries as distribution hubs for FPC products.

Report Scope

This market research report provides a comprehensive analysis of the FPC Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of FPC Market?

-> PC Market was valued at USD 14,430 million in 2025 and is projected to reach USD 18,400 million by 2033, exhibiting a CAGR of 3.6% during the forecast period.

Which key companies operate in FPC Market?

-> Key players include Nippon Mektron, Suzhou Dongshan Precision, SEI, ZDT, Flexium, among others. The top five players hold a share over 51.02%.

What are the key product segments?

-> Multi-layer circuit is the largest segment, occupying 55% market share, followed by single-layer circuit, double-layer circuit, and rigid-flex circuit.

Which application dominates the market?

-> Consumer electronics holds the largest application share at 19%, followed by automotive, aerospace & defense/military, and medical applications.

What are the major regional markets?

-> Asia leads the global FPC Market with major contributions from China, Japan, and South Korea, while North America and Europe also hold significant shares.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...