MARKET INSIGHTS

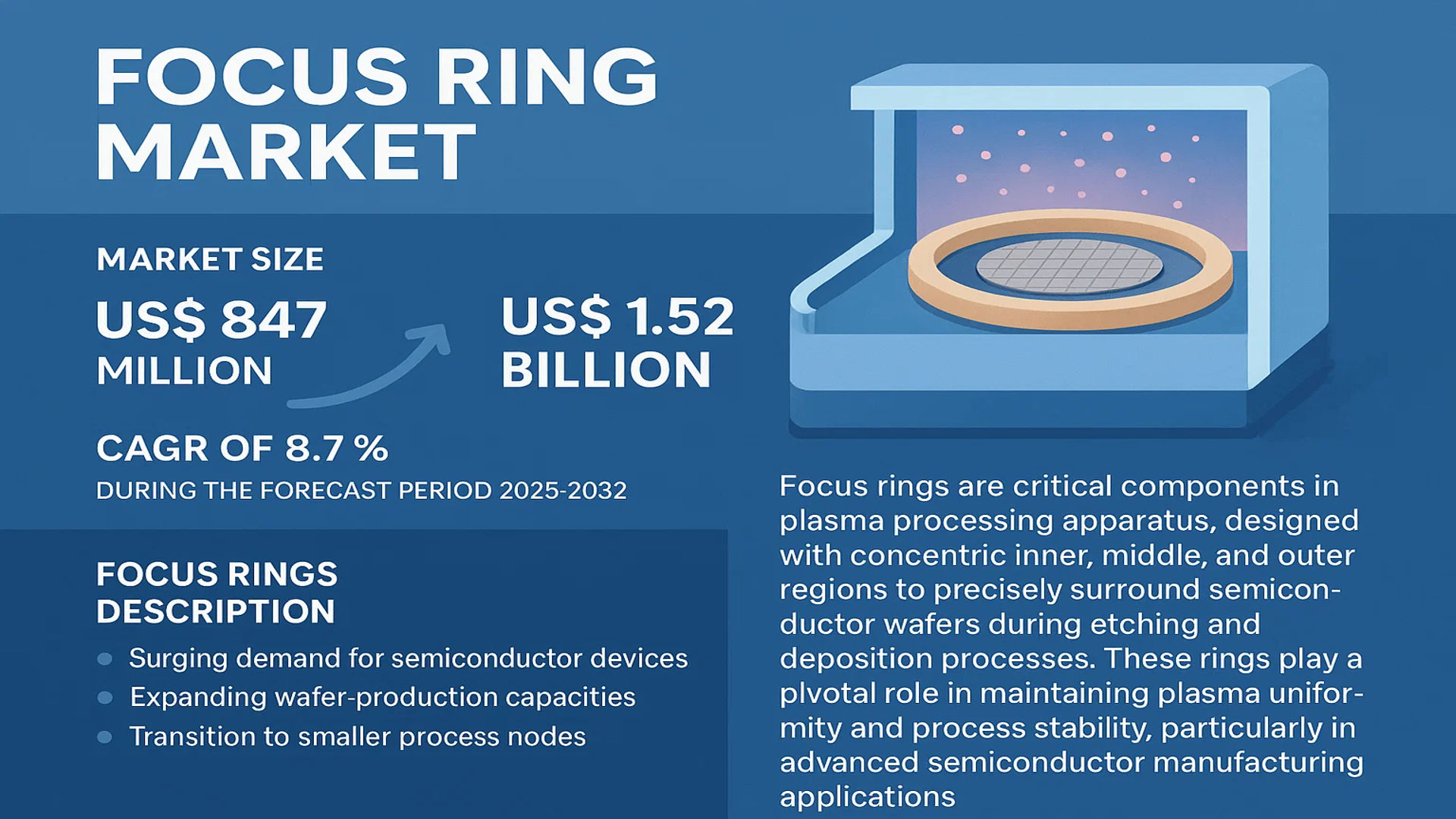

The global Focus Ring Market size was valued at US$ 847 million in 2024 and is projected to reach US$ 1.52 billion by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Focus rings are critical components in plasma processing apparatus, designed with concentric inner, middle, and outer regions to precisely surround semiconductor wafers during etching and deposition processes. These rings play a pivotal role in maintaining plasma uniformity and process stability, particularly in advanced semiconductor manufacturing applications.

Market growth is driven by surging demand for semiconductor devices, expanding wafer production capacities, and the transition to smaller process nodes. While quartz remains the dominant material segment, silicon carbide variants are gaining traction due to superior durability in high-temperature environments. The U.S. and China collectively account for over 55% of global demand, reflecting concentrated semiconductor manufacturing activity in these regions. Key players like CoorsTek and Kallex continue to innovate, with recent developments including ceramic-composite focus rings for 5nm node compatibility.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Semiconductor Industry to Fuel Demand for Focus Rings

The global semiconductor industry is experiencing robust growth, driving substantial demand for focus rings used in wafer fabrication processes. As chip manufacturers scale production to meet increasing demand for consumer electronics, automotive semiconductors, and IoT devices, the need for precision plasma etching components grows accordingly. Focus rings play a critical role in maintaining plasma density uniformity during etching processes, directly impacting yield rates. With semiconductor foundries investing heavily in new fabrication facilities – over 200 new fabs are expected to be operational by 2025 – the market for high-quality focus rings is poised for significant expansion.

Material Innovation in Focus Ring Design Accelerates Market Adoption

Recent advancements in focus ring materials are creating new opportunities in semiconductor manufacturing. Traditional quartz rings are being increasingly replaced by silicon carbide variants offering superior plasma resistance and extended service life. These innovations directly translate to reduced downtime for chamber maintenance and improved process consistency. Leading manufacturers have developed rings with advanced coatings that demonstrate 40-60% longer operational lifespans compared to conventional designs. As fabrication processes become more demanding with smaller node sizes, the industry’s transition to advanced materials will continue driving market growth for performance-enhanced focus rings.

➤ For instance, recent industry benchmarks demonstrate that silicon carbide focus rings can withstand over 1,500 wafer processing cycles before requiring replacement, compared to just 800-900 cycles for standard quartz versions.

Growing Investment in 300mm Wafer Capacity Creates New Market Potential

The semiconductor industry’s ongoing transition to larger wafer sizes presents significant growth opportunities for focus ring manufacturers. With 300mm wafer fabs accounting for nearly 80% of global silicon wafer area production, equipment components must scale accordingly. Leading manufacturers are responding with optimized product lines specifically designed for 300mm process chambers. The increasing complexity of 3D NAND and advanced logic devices at these dimensions further drives the need for precision-engineered focus rings that can maintain process stability across larger surface areas.

MARKET RESTRAINTS

High Material and Manufacturing Costs Limit Market Penetration

The focus ring market faces significant challenges related to production costs. Advanced materials like high-purity silicon carbide require specialized manufacturing processes and stringent quality control measures, resulting in substantially higher unit costs compared to conventional components. For cost-sensitive semiconductor manufacturers, particularly in developing regions, these price premiums can delay adoption of next-generation products. While the total cost of ownership justifies premium pricing through extended service life, the initial capital expenditure remains a barrier for many fabrication facilities operating on tight budgets.

Technical Complexity in Advanced Node Processing Creates Integration Challenges

As semiconductor nodes advance below 5nm, focus ring manufacturers face increasing technical hurdles. The extreme precision required for sub-5nm etching processes demands rings with near-perfect geometric tolerances and material uniformity. Even minor variations in thermal expansion coefficients or plasma resistance can significantly impact device yields. This complexity creates substantial R&D costs for manufacturers developing solutions for cutting-edge applications. Additionally, the validation process for new focus ring designs has lengthened considerably, as chipmakers rigorously test components before qualifying them for high-volume production.

MARKET CHALLENGES

Rapid Technological Evolution Creates Product Obsolescence Risks

The focus ring market must contend with the semiconductor industry’s exceptionally fast pace of technological change. As etching processes evolve to accommodate new device architectures and materials, existing ring designs may become obsolete within relatively short timeframes. Manufacturers face the dual challenge of maintaining current product lines while investing in next-generation solutions. This constant innovation cycle requires substantial R&D expenditures and creates inventory management complexities, particularly for products with long lead times like customized silicon carbide rings.

Other Challenges

Supply Chain Vulnerabilities

Global supply chain disruptions continue to impact the availability of critical raw materials for focus ring production. Specialty ceramics and high-purity silicon carbide face periodic shortages, creating production bottlenecks. These challenges are compounded by the concentrated nature of supplier networks, with few qualified sources for semiconductor-grade materials.

Skilled Labor Shortages

The precision manufacturing required for focus rings demands highly trained technicians and engineers. As competition for semiconductor talent intensifies globally, manufacturers face difficulties in recruiting and retaining personnel with the specialized skills needed for product development and quality control.

MARKET OPPORTUNITIES

Emerging Markets Present Significant Growth Potential

Rapid expansion of semiconductor manufacturing capacity in Southeast Asia and other developing regions creates substantial opportunities for focus ring suppliers. With governments offering incentives for local chip production and multinational corporations diversifying their geographic footprint, new fabrication clusters are emerging outside traditional manufacturing centers. These greenfield facilities represent prime opportunities for suppliers to establish long-term partnerships with growing manufacturers. Early engagement in these developing markets can provide first-mover advantages as local ecosystems mature.

Aftermarket Services Offer Revenue Diversification

The focus ring aftermarket presents significant opportunities for value-added services. With thousands of installed etch tools worldwide requiring regular component replacement, manufacturers can develop service offerings that complement their core products. Predictive maintenance programs leveraging IoT sensors to monitor ring degradation, along with refurbishment services for high-value components, can create recurring revenue streams. These services not only improve customer retention but also provide valuable usage data to inform future product development.

Collaboration with Equipment OEMs Drives Innovation

Strategic partnerships with semiconductor equipment manufacturers represent a key growth avenue. As etch tool designs evolve to accommodate new process requirements, close collaboration enables focus ring suppliers to develop optimized, system-level solutions. Joint development programs can accelerate the introduction of advanced materials and geometries while ensuring seamless integration with next-generation processing platforms. These partnerships often lead to preferred supplier status and long-term supply agreements, providing market stability amid industry fluctuations.

FOCUS RING MARKET TRENDS

Semiconductor Industry Expansion Driving Focus Ring Demand

The global focus ring market, valued at $XX million in 2024, is experiencing robust growth driven by rapid advancements in semiconductor manufacturing. Focus rings play a critical role in plasma processing apparatus, ensuring uniform etching and deposition processes for wafer fabrication. With semiconductor manufacturing projected to grow at a CAGR of 7.2% through 2032, demand for high-performance focus rings is rising concurrently. Key semiconductor hubs such as Taiwan, South Korea, and the United States are leading this expansion, with foundries investing heavily in next-generation fabrication facilities. The U.S. market alone accounts for nearly 22% of global semiconductor production, positioning it as a major consumer of focus rings.

Other Trends

Material Innovation Enhancing Performance

Manufacturers are increasingly shifting from traditional quartz-based focus rings to advanced silicon carbide (SiC) variants, which offer superior plasma resistance and extended operational lifespans. SiC focus rings exhibit up to 40% longer durability compared to quartz alternatives, significantly reducing tool downtime in high-volume fabrication environments. This material transition is particularly pronounced in leading-edge nodes below 10nm, where process stability is paramount. While quartz remains dominant with a 48% market share in 2024, silicon carbide is projected to grow at 11.3% CAGR through 2032 as 5nm and 3nm production scales globally.

Geopolitical Factors Reshaping Supply Chains

Recent trade policies and semiconductor self-sufficiency initiatives are dramatically altering focus ring supply networks. China’s $140 billion semiconductor investment plan has created a parallel demand stream, with domestic manufacturers like Max Luck Technology expanding production capacity by 35% in 2023. Meanwhile, U.S. CHIPS Act funding is driving localization efforts, with CoorsTek and Greene Tweed establishing new manufacturing facilities in Arizona and Texas. This geographic diversification is causing suppliers to develop regional-specific product lines, with some variants showing 15-20% performance optimization for local fab conditions. However, export controls on advanced manufacturing equipment are creating supply bottlenecks for cutting-edge focus ring production.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Advanced Materials and Semiconductor Applications

The global focus ring market features a competitive landscape with both established players and emerging companies vying for market share. Kallex currently leads the market, holding approximately 18% revenue share in 2024, due to its patented quartz-based focus ring technology and strong supplier relationships with leading semiconductor manufacturers.

CoorsTek and Daewon follow closely, collectively accounting for nearly 25% of the market. These companies have strengthened their positions through continuous R&D investment in silicon carbide focus rings, which are increasingly preferred for high-temperature plasma processing applications.

The market demonstrates dynamic competition as manufacturers expand their geographic footprint and product portfolios. While leading players dominate through technological expertise, mid-sized companies are gaining traction by offering cost-effective solutions to smaller semiconductor fabs.

Recent acquisitions and partnerships have reshaped the competitive dynamics. FerroTec’s 2023 acquisition of a specialty ceramics manufacturer and Worldex’s strategic partnership with a Japanese tech firm illustrate how companies are broadening their capabilities to meet growing demand from the semiconductor sector.

Looking ahead, competition is expected to intensify as quartz-based products face challenges from emerging silicon carbide alternatives, forcing manufacturers to accelerate innovation cycles while maintaining production efficiency.

List of Key Focus Ring Manufacturers Profiled

- Kallex (South Korea)

- CoorsTek (U.S.)

- Daewon (South Korea)

- Greene Tweed (U.S.)

- Worldex (China)

- Max Luck Technology (Taiwan)

- Coma Technology (Japan)

- FerroTec (U.S.)

Segment Analysis:

By Type

Quartz Segment Leads the Market Due to High Thermal Resistance and Durability in Plasma Processing

The market is segmented based on type into:

- Quartz

- Silicon

- Silicon Carbide

- Others

By Application

Wafer Etching Dominates Due to Rising Semiconductor Manufacturing Demand

The market is segmented based on application into:

- Wafer Etching

- Others

By End User

Semiconductor Fabrication Facilities Hold Major Share Due to High-Volume Production Requirements

The market is segmented based on end user into:

- Semiconductor Fabrication Facilities

- Research Institutes

- Equipment Manufacturers

Regional Analysis: Focus Ring Market

Asia-Pacific

The Asia-Pacific region dominates the global Focus Ring market, driven by robust semiconductor manufacturing activity in countries like China, South Korea, and Taiwan. The region accounts for over 65% of global semiconductor production capacity, creating substantial demand for plasma processing components including focus rings. While Japan remains a technological leader in advanced materials for semiconductor equipment, China’s aggressive fab expansion projects fuel volume demand for cost-effective solutions. Local suppliers are increasingly competing with established global players through vertically integrated manufacturing and government-supported R&D initiatives. However, supply chain vulnerabilities and geopolitical tensions present ongoing challenges to market stability.

North America

Home to leading semiconductor equipment manufacturers and R&D centers, the North American market prioritizes high-performance quartz and silicon carbide focus rings for cutting-edge wafer processing. The U.S. CHIPS Act’s $52 billion investment in domestic semiconductor manufacturing is driving facility expansions, subsequently increasing demand for precision components. Strict export controls on advanced technologies influence supply chain strategies, with manufacturers gradually reshoring production capabilities. The region maintains strong innovation in plasma-resistant materials, though higher costs compared to Asian alternatives limit price competitiveness in high-volume applications.

Europe

European demand stems primarily from specialty semiconductor applications and research institutions developing next-generation deposition and etching technologies. Germany and France host several leading equipment OEMs that specify premium-grade focus rings with extended operational lifetimes. The region’s materials science expertise fosters innovations in composite materials, though market growth remains constrained by limited local fab capacity compared to Asia. REACH regulations influence material selection, with manufacturers prioritizing environmentally sustainable production processes for focus ring components.

Middle East & Africa

This emerging market shows potential through strategic investments in technology hubs and specialized manufacturing zones. While current demand remains modest, planned semiconductor initiatives in countries like Saudi Arabia and the UAE could drive future growth. The lack of established supply chains and dependency on imports presently restricts market development. However, partnerships with global foundries and incentive programs may accelerate adoption of semiconductor manufacturing ecosystems in the long term.

South America

The region represents a niche market with limited semiconductor manufacturing presence. Most focus ring demand comes from maintenance and replacement cycles at existing fabrication facilities in Brazil. Economic volatility deters large-scale investments in semiconductor production infrastructure, keeping the market dependent on imported components. While some countries show interest in developing technology sectors, progress remains slow due to infrastructure gaps and limited technical expertise in advanced semiconductor manufacturing.

Report Scope

This market research report provides a comprehensive analysis of the Global Focus Ring market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Quartz, Silicon, Silicon Carbide, Others), application (Wafer Etching, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor fabrication techniques and material advancements in focus rings.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with supply chain constraints and regulatory considerations.

- Stakeholder Analysis: Insights for semiconductor equipment manufacturers, component suppliers, and investors regarding strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Focus Ring Market?

-> Focus Ring Market size was valued at US$ 847 million in 2024 and is projected to reach US$ 1.52 billion by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Which key companies operate in Global Focus Ring Market?

-> Key players include Kallex, Daewon, CoorsTek, Greene Tweed, Worldex, Max Luck Technology, Coma Technology, and FerroTec, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor manufacturing activities, demand for advanced wafer processing, and expansion of foundry capacity.

Which region dominates the market?

-> Asia-Pacific dominates the market, driven by semiconductor manufacturing hubs in China, South Korea, and Taiwan.

What are the emerging trends?

-> Emerging trends include development of high-performance silicon carbide focus rings and integration with advanced plasma etching systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...