MARKET INSIGHTS

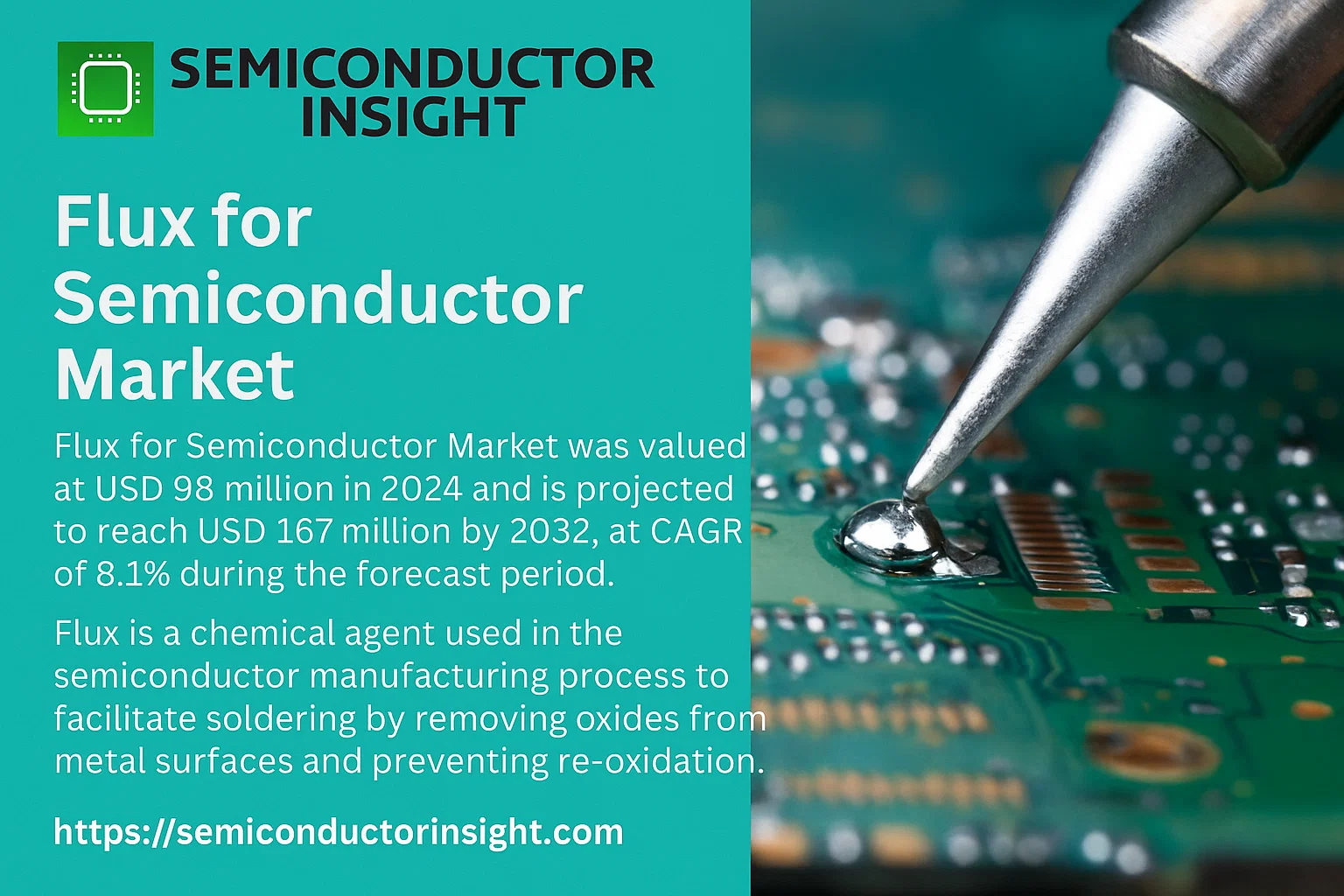

Global Flux for Semiconductor Market was valued at USD 98 million in 2024 and is projected to reach USD 167 million by 2032, at a CAGR of 8.1% during the forecast period.

Flux is a chemical agent used in the semiconductor manufacturing process to facilitate soldering by removing oxides from metal surfaces and preventing re-oxidation. This ensures strong, reliable electrical connections in components like integrated circuits (ICs) and printed circuit boards (PCBs). The market is driven by the expanding electronics industry, the proliferation of IoT devices, and the increasing complexity of semiconductor devices requiring precise soldering.

Key market segments include water-soluble fluxes, which are easy to clean and suitable for high-precision applications, and rosin-based fluxes, which offer excellent wetting properties. The Asia-Pacific region dominates the market due to its large electronics manufacturing base, particularly in countries like China, South Korea, and Taiwan. Leading players are focusing on developing halogen-free and low-VOC (volatile organic compound) flux formulations to meet environmental regulations and customer demands for greener products.

MARKET DRIVERS

Expansion of Advanced Packaging Technologies

The market for semiconductor flux is being strongly driven by the global expansion of advanced packaging solutions such as 2.5D/3D ICs, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP). These technologies demand highly reliable and efficient fluxes to ensure strong interconnections and miniaturized, high-performance devices, particularly in the consumer electronics and automotive sectors. The push for higher I/O density and better thermal performance necessitates fluxes with superior wetting characteristics and minimal residue.

Growth in Automotive Electronics and Electrification

The rapid electrification of vehicles, including the proliferation of electric vehicles (EVs), advanced driver-assistance systems (ADAS), and in-vehicle infotainment, requires robust and durable semiconductor packages. Fluxes used in the assembly of power management units, sensors, and control modules must exhibit high thermal stability and withstand harsh operating conditions. This trend is a significant driver for the development and adoption of no-clean and high-reliability fluxes.

➤ The global demand for miniaturized, high-performance electronics continues to be a primary catalyst for flux innovation.

Additionally, the increasing complexity of printed circuit board assemblies (PCBAs) with finer pitches and mixed-technology components requires fluxes that can prevent solder bridging and ensure high first-pass yields. The trend toward lead-free soldering, mandated by environmental regulations like RoHS, also compels the use of advanced flux formulations compatible with higher processing temperatures.

MARKET CHALLENGES

Stringent Environmental and Health Regulations

The formulation of semiconductor fluxes faces significant challenges due to stringent global regulations concerning volatile organic compound (VOC) emissions and hazardous substances. Compliance with standards such as REACH and RoHS requires manufacturers to invest heavily in research and development of environmentally friendly, halide-free, and low-VOC flux chemistries, which can increase production costs and complexity.

Other Challenges

Technical Demands for Miniaturization

As semiconductor packages and PCB features continue to shrink to micrometer scales, fluxes must provide extremely precise activity without causing corrosion or electromigration. Achieving this level of performance while maintaining high reliability and long-term stability under thermal cycling presents a major technical hurdle for flux manufacturers.

Supply Chain and Raw Material Volatility

The flux market is susceptible to fluctuations in the supply and price of key raw materials, such as rosin, activators, and solvents. Geopolitical tensions and trade policies can disrupt supply chains, leading to cost instability and potential delays in semiconductor manufacturing, which operates on tight production schedules.

MARKET RESTRAINTS

High Cost of Advanced Flux Formulations

The development of specialized fluxes for advanced semiconductor packaging, such as those required for ultra-fine-pitch applications or high-temperature lead-free processes, involves significant R&D investment. The resulting high cost of these premium products can act as a restraint, particularly for small and medium-sized electronics manufacturers operating with thin profit margins, potentially limiting market penetration.

Maturation of Certain End-Use Segments

While sectors like smartphones and personal computing continue to evolve, their growth rates have stabilized compared to previous decades. This maturation can temper the demand for new flux formulations in these high-volume but slower-growth segments, as manufacturers may prioritize cost reduction over the adoption of next-generation flux technologies.

MARKET OPPORTUNITIES

Rise of AI, HPC, and 5G Infrastructure

The deployment of 5G networks and the exponential growth in artificial intelligence (AI) and high-performance computing (HPC) are creating substantial opportunities. These applications require semiconductor packages with exceptional performance and thermal management, driving demand for fluxes that enable reliable soldering of complex substrates and heat-dissipating materials. This represents a high-value growth avenue for flux suppliers.

Development of Sustainable and High-Reliability Fluxes

There is a growing market opportunity for developing fluxes that meet both high-reliability standards for critical industries (aerospace, medical devices) and stringent sustainability criteria. Bio-based, low-residue, and no-clean fluxes that reduce environmental impact without compromising performance are poised for significant adoption, aligning with corporate sustainability goals and regulatory trends.

Global Flux for Semiconductor Market Trends

Strong Market Growth Driven by Semiconductor Industry Expansion

The global market for flux used in semiconductor manufacturing is experiencing robust growth, driven by the relentless expansion of the semiconductor industry. The market, valued at US$98 million in 2024, is projected to reach US$167 million by 2032, growing at a compound annual growth rate (CAGR) of 8.1%. This growth is intrinsically linked to the demand for increasingly complex and miniaturized electronic components, where flux is an indispensable chemical agent in the soldering process. Fluxes perform critical functions that ensure the integrity and reliability of solder joints, which are vital for the performance of everything from consumer electronics to advanced automotive and computing systems.

Other Trends

Dominance of Water Soluble and Low Residue Fluxes

A significant product trend is the pronounced demand for water soluble and low residue flux types. As semiconductor packaging becomes more intricate, particularly with the proliferation of flip-chip and ball grid array (BGA) technologies, the need for fluxes that leave minimal ionic contamination is paramount. These high-purity fluxes help prevent corrosion and electrical failures, directly supporting the production of more reliable and higher-performance semiconductor devices. Their ease of cleaning also aligns with stringent manufacturing requirements, making them a preferred choice for advanced applications.

Asia-Pacific as the Undisputed Market Leader

The geographical distribution of the flux market is heavily concentrated in the Asia-Pacific region, which commands approximately 56% of the global market share. This dominance is a direct consequence of the region’s status as the world’s semiconductor manufacturing hub. Countries like China, Japan, South Korea, and Taiwan are home to major semiconductor fabrication plants and electronics assembly operations, creating sustained, high-volume demand for flux. The continuous investment in new semiconductor capacity across Asia ensures that the region will remain the primary driver of market growth for the foreseeable future.

Consolidated Competitive Landscape

The competitive landscape of the flux for semiconductor market is characterized by a high degree of consolidation. The top three players, including MacDermid (encompassing Alpha and Kester), SENJU METAL INDUSTRY, and Henkel, collectively hold about 55% of the total market share. These established companies possess significant technological expertise, extensive product portfolios, and strong relationships with major semiconductor manufacturers. Competition is fierce, with a focus on developing innovative flux formulations that offer superior performance, higher reliability, and compliance with evolving environmental regulations.

COMPETITIVE LANDSCAPE

Key Industry Players

A Consolidated Market Driven by Technological Expertise and Regional Strength

The global Flux for Semiconductor market features a landscape that is dominated by a few major international players who collectively hold a significant market share. The market is considered fully developed, with the top three players—MacDermid (through its Alpha and Kester brands), SENJU METAL INDUSTRY, and Henkel—commanding approximately 55% of the global market. These leaders have established their positions through extensive product portfolios, deep technical expertise in formulations like water-soluble, rosin-soluble, and epoxy fluxes, and strong global supply chains that cater to major semiconductor manufacturing hubs. The Asia-Pacific region is the largest sales market, accounting for about 56% of global sales, and the presence and performance of these key players in this high-growth region is a critical factor in their overall market dominance.

Beyond the top tier, the market includes a number of other significant, often more specialized, companies that compete by focusing on niche applications, specific flux chemistries, or regional markets. Players such as Indium Corporation and AIM Solder are recognized for their high-performance products tailored for advanced packaging applications like flip-chip and BGA (Ball Grid Array) attach. Several Asia-based manufacturers, including Vital New Material, Shenmao Technology, and Tong fang Electronic New Material, have grown substantially by leveraging the region’s booming semiconductor industry. These companies compete on factors such as price, technical service, and the ability to meet the stringent purity and performance requirements of modern semiconductor fabrication and assembly processes.

List of Key Flux for Semiconductor Companies Profiled

- MacDermid (Alpha and Kester)

- SENJU METAL INDUSTRY

- Asahi Chemical & Solder Industries

- Henkel

- Indium Corporation

- Vital New Material

- Tong fang Electronic New Material

- Shenmao Technology

- AIM Solder

- Tamura

- ARAKAWA CHEMICAL INDUSTRIES

- Changxian New Material Technology

- Superior Flux & Mfg. Co

- Inventec Performance Chemicals

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Water Soluble and Low Residue fluxes are the leading segment, driven by the critical need for superior cleaning processes and minimal ionic contamination in high-reliability semiconductor manufacturing. This type addresses stringent industry standards for post-soldering cleanliness, which is paramount for the longevity and performance of advanced microelectronics. The move towards eco-friendly formulations that reduce environmental impact further solidifies the dominance of this segment. Rosin Soluble fluxes maintain a critical role in specific through-hole applications, while Epoxy Fluxes are gaining traction in underfill and encapsulation processes for their excellent mechanical stability and protective qualities. |

| By Application |

|

Ball Attach (BGA) represents the most significant application segment, fueled by the pervasive adoption of Ball Grid Array packaging across a wide spectrum of electronic devices from smartphones to high-performance computing systems. The demand for fluxes that ensure robust, reliable solder joints with high standoff heights and strong thermal and electrical performance is a primary driver. Chip Attach, particularly for flip-chip technology, is also a major and sophisticated application requiring fluxes with precise activity profiles to ensure successful interconnection on a microscopic scale. The “Others” category, encompassing various surface-mount technologies, remains a consistent and substantial contributor to overall market volume. |

| By End User |

|

Outsourced Semiconductor Assembly and Test (OSAT) providers constitute the leading end-user segment, as the industry trend towards specialization and cost-efficiency drives the outsourcing of packaging and testing operations. OSATs are high-volume consumers of flux, requiring consistent, high-performance materials to meet the diverse needs of their broad client base. Semiconductor Foundries are also major consumers, particularly those expanding into advanced packaging, while Integrated Device Manufacturers (IDMs) with in-house packaging operations demand specialized, high-reliability flux formulations for their proprietary and often leading-edge products. |

| By Material Composition |

|

Organic Acid-Based fluxes lead this segment due to their balanced performance profile, offering effective oxide removal with relatively easy cleaning and lower corrosivity compared to inorganic alternatives. They are highly suitable for a wide range of semiconductor assembly processes. Rosin-Based fluxes continue to be valued for their excellent reliability and protective properties in certain high-end applications, despite requiring more vigorous cleaning. Inorganic Acid-Based fluxes are reserved for specialized applications where maximum cleansing power is required, but their use is carefully managed due to potential corrosive effects. |

| By Activity Level |

|

Medium Activity (M) fluxes represent the most widely used category, striking an optimal balance between strong oxide-removal capability and manageable post-soldering residues. This makes them versatile for the vast majority of standard semiconductor assembly processes. Low Activity fluxes are preferred for applications involving highly sensitive components where any residue could be detrimental, while High Activity fluxes are essential for soldering challenging surfaces with tenacious oxides but necessitate thorough cleaning to prevent long-term reliability issues, limiting their use to specific, controlled scenarios. |

Regional Analysis: Flux for Semiconductor Market

The sheer volume of semiconductor and electronics production in countries like China and Taiwan creates the world’s largest consumption base for fluxes. The presence of major OSATs and IDMs necessitates a constant supply of various flux formulations for different assembly stages, from wafer-level packaging to final board assembly, ensuring market stability and growth.

A well-established and localized supply chain for flux raw materials and finished products allows for rapid response to manufacturer needs and cost-effective production. This proximity fosters close collaboration between flux suppliers and semiconductor companies, leading to the co-development of specialized fluxes for advanced applications like flip-chip and 3D packaging.

The region is at the forefront of adopting advanced semiconductor packaging, which requires fluxes with specific properties such as ultra-low residue, high thermal stability, and compatibility with fine-pitch components. This technological advancement pushes flux manufacturers to continually innovate, creating a dynamic and high-value market segment.

Increasingly stringent environmental regulations in key countries are accelerating the shift towards halogen-free and water-soluble flux formulations. Manufacturers in the region are actively adapting their product portfolios to meet these requirements, driving the development of more sustainable and compliant flux solutions for the global market.

North America

North America remains a critical and technologically advanced market for flux, characterized by a strong presence of leading semiconductor design companies and specialized manufacturers, particularly in the United States. The demand is driven by high-value, low-volume production of cutting-edge semiconductors for applications in aerospace, defense, automotive, and high-performance computing. This focus on specialized and reliable components necessitates the use of high-purity, high-performance fluxes that ensure impeccable solder joint integrity and long-term reliability. The market is strongly influenced by stringent quality standards and a robust culture of research and development, leading to early adoption of innovative flux chemistries designed for challenging applications. Collaboration between material science companies and semiconductor firms is a key characteristic, fostering the development of tailored solutions.

Europe

The European flux market is characterized by a strong emphasis on quality, precision engineering, and environmental sustainability. The region has a significant automotive industry, which is a major consumer of semiconductors requiring highly reliable fluxes for harsh operating environments. This drives demand for fluxes that offer exceptional performance under thermal cycling and mechanical stress. Furthermore, the presence of major industrial automation and medical device manufacturers creates a need for precise and consistent flux application. European regulations, particularly concerning chemical safety and environmental impact (like REACH), significantly shape the market, pushing for the development and adoption of green chemistry principles in flux formulations. The market is mature, with a focus on value-added, specialized products rather than high-volume consumption.

South America

The flux market in South America is emerging and is considerably smaller than other regions, primarily serving the local consumer electronics assembly and industrial electronics sectors. The market growth is closely tied to the region’s economic stability and industrial development. Demand is largely for standard, cost-effective flux formulations used in mainstream electronic manufacturing. While the adoption of advanced flux technologies is slower compared to leading regions, there is a growing awareness of quality and reliability requirements. The market is characterized by the presence of multinational flux suppliers catering to global OEMs with local manufacturing plants, alongside smaller local distributors. Future growth potential hinges on increased foreign investment in local electronics manufacturing capabilities.

Middle East & Africa

The flux market in the Middle East & Africa is the smallest and most nascent on a global scale. Demand is primarily generated by the maintenance, repair, and operations sector for existing electronic infrastructure, as well as some light assembly operations. The market is heavily reliant on imports, with limited local production of flux materials. Key demand drivers include the telecommunications sector and industrial projects. The market tends to favor standard, no-clean flux formulations for their convenience. While there is potential for growth, particularly in Gulf Cooperation Council countries investing in technological diversification, the market currently remains a minor segment of the global flux industry, with dynamics influenced more by trade and distribution logistics than by local technological innovation.

Report Scope

This market research report provides a comprehensive analysis of the Flux for Semiconductor Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of flux in semiconductor soldering processes for applications such as chip attach, ball attach, and other critical electronic assembly operations.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging flux formulations, integration of new materials, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Flux for Semiconductor Market?

-> Global Flux for Semiconductor Market was valued at USD 98 million in 2024 and is projected to reach USD 167 million by 2032, exhibiting a CAGR of 8.1% during the forecast period.

Which key companies operate in Flux for Semiconductor Market?

-> Key players include MacDermid (Alpha and Kester), SENJU METAL INDUSTRY, Asahi Chemical & Solder Industries, Henkel, Indium Corporation, Vital New Material, Tong fang Electronic New Material, Shenmao Technology, AIM Solder, and Tamura, among others. The top 3 players hold approximately 55% market share.

What are the key growth drivers?

-> Key growth drivers include the rapid development of the global semiconductor industry and the critical role of flux in soldering processes for removing oxides and reducing surface tension during welding.

Which region dominates the market?

-> Asia is the largest sales market, accounting for approximately 56% of the global share, driven by its rapidly expanding semiconductor industry.

What are the emerging trends?

-> Emerging trends include the development of advanced flux formulations such as Water Soluble and Low Residue, Rosin Soluble, and Epoxy Flux to meet evolving performance requirements in semiconductor manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...