MARKET INSIGHTS

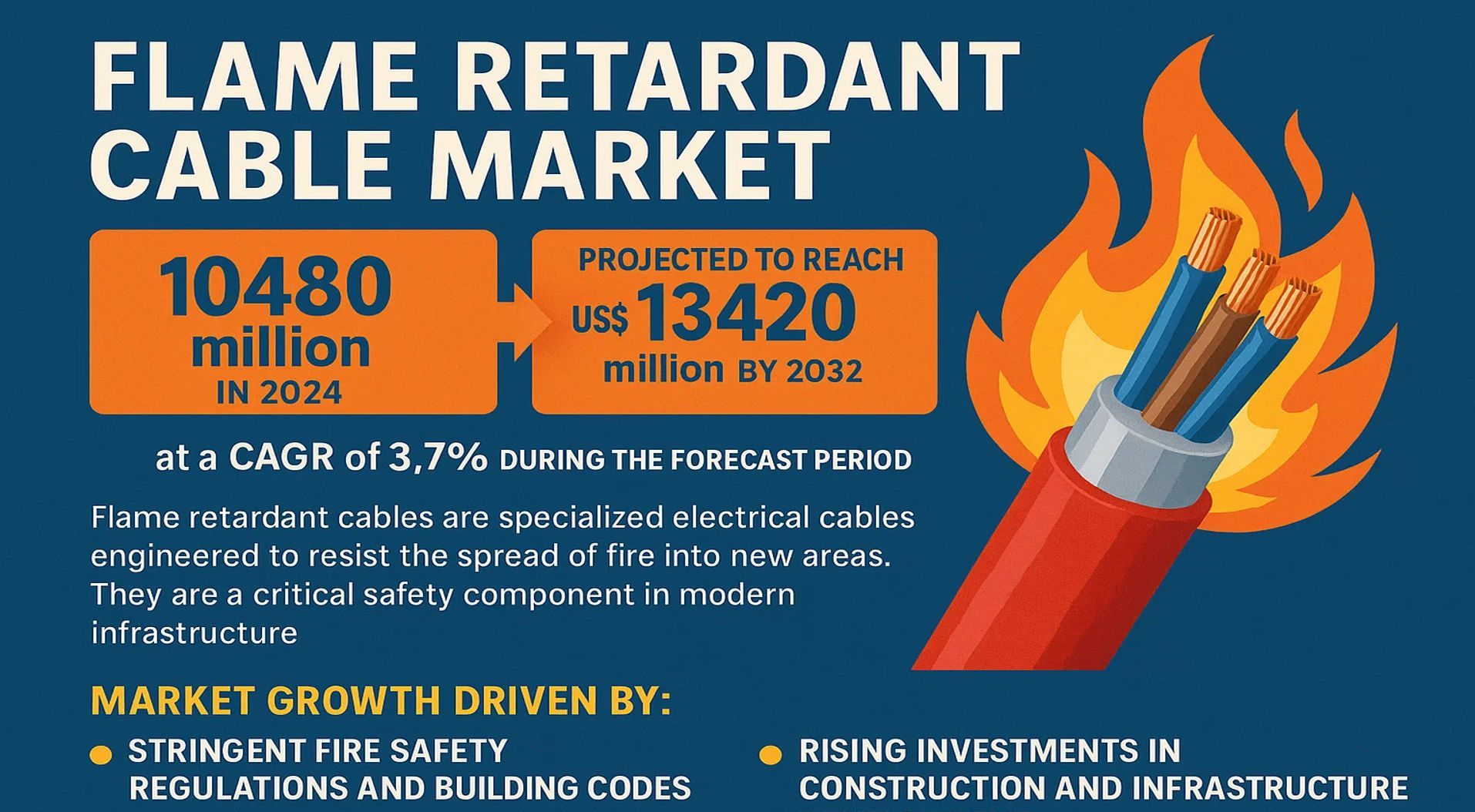

The global Flame Retardant Cable Market was valued at 10480 million in 2024 and is projected to reach US$ 13420 million by 2032, at a CAGR of 3.7% during the forecast period.

Flame retardant cables are specialized electrical cables engineered to resist the spread of fire into new areas. While fire-rated cables maintain circuit integrity and continue to operate for a specified time under fire conditions, flame retardant cables are designed to contain combustion to a local scope, preventing the fire from spreading and thereby protecting other equipment to avoid greater losses. These cables are a critical safety component in modern infrastructure.

The market growth is primarily driven by stringent fire safety regulations and building codes across the globe, alongside rising investments in construction and infrastructure development. The low-smoke halogen-free segment dominates the market, holding over 70% share, due to its superior safety profile as it emits minimal smoke and toxic halogens when exposed to fire. Geographically, Europe is the largest market with over a 25% share, followed closely by North America and the Asia-Pacific region, which together account for over 40% of the global market. Key players such as Nexans, Prysmian, and Leoni AG operate with extensive portfolios, driving innovation and market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Fire Safety Regulations and Standards to Propel Market Growth

The global flame retardant cable market is significantly driven by stringent fire safety regulations and standards imposed by governments and international bodies. These regulations mandate the use of flame retardant cables in critical applications such as residential buildings, commercial complexes, industrial facilities, and public infrastructure to minimize fire hazards and ensure safety. For instance, regulations like the International Electrotechnical Commission (IEC) standards, National Electrical Code (NEC) in the United States, and Construction Products Regulation (CPR) in Europe enforce specific performance criteria for cables regarding fire resistance, smoke emission, and halogen content. The increasing number of fire incidents worldwide has further intensified regulatory scrutiny, with over 3.5 million fire incidents reported annually globally, leading to substantial economic losses and safety concerns. This regulatory environment compels infrastructure developers and industries to adopt flame retardant cables, thereby boosting market demand.

Rapid Urbanization and Infrastructure Development to Fuel Demand

Rapid urbanization and massive infrastructure development projects across emerging and developed economies are key drivers for the flame retardant cable market. The global urban population is projected to reach 68% by 2050, necessitating the construction of smart cities, transportation networks, energy systems, and residential complexes that require advanced fire safety solutions. Investments in infrastructure are soaring, with the global construction market valued at over $12 trillion annually, and a significant portion allocated to safety-compliant materials. Flame retardant cables are essential in these projects to prevent fire propagation, ensure operational continuity, and protect lives and assets. Major projects, such as the development of high-speed rail networks, renewable energy plants, and data centers, particularly emphasize the integration of high-performance flame retardant cables to meet safety and reliability standards.

Growing Awareness and Adoption in Industrial and Energy Sectors to Accelerate Market Expansion

The industrial and energy sectors are increasingly adopting flame retardant cables due to growing awareness of operational safety and the need to prevent catastrophic failures. Industries such as oil and gas, manufacturing, power generation, and chemicals are highly susceptible to fire risks, making flame retardant cables a critical component in their operations. The global energy sector, for example, invests substantially in upgrading infrastructure to enhance safety, with flame retardant cables being integral to power distribution, control systems, and emergency circuits. Additionally, the rise of renewable energy projects, such as solar and wind farms, which require durable and safe cabling solutions, further drives demand. The industrial sector’s emphasis on minimizing downtime and protecting expensive machinery from fire-related damages reinforces the adoption of these cables, supporting steady market growth.

MARKET CHALLENGES

High Production Costs and Raw Material Price Volatility to Challenge Market Growth

The flame retardant cable market faces challenges related to high production costs and volatility in raw material prices. Flame retardant cables require specialized materials such as low-smoke halogen-free (LSHF) compounds, which are more expensive than conventional PVC or polyethylene used in standard cables. The cost of raw materials like aluminum, copper, and flame retardant additives can fluctuate significantly due to geopolitical tensions, supply chain disruptions, and changing demand patterns. For instance, copper prices have experienced variations of over 25% annually in recent years, impacting overall production costs. These high costs are often passed on to end-users, making flame retardant cables less attractive in price-sensitive markets, particularly in developing regions where budget constraints limit large-scale adoption.

Other Challenges

Technical Complexity in Manufacturing

Manufacturing flame retardant cables involves complex processes to ensure consistent quality, performance, and compliance with international standards. Achieving the right balance between flame retardancy, mechanical strength, and electrical properties requires advanced technology and expertise. Small and medium-sized manufacturers may struggle with these technical complexities, leading to inconsistencies in product quality and reliability. This can result in increased rejection rates, higher R&D expenditures, and longer time-to-market, posing challenges for market players aiming to scale production and meet growing demand efficiently.

Limited Awareness in Developing Regions

In many developing regions, awareness about the benefits of flame retardant cables and adherence to safety standards remain limited. While regulations are becoming stricter, enforcement is often lax, and cost considerations prioritize conventional cables over safer alternatives. This lack of awareness and regulatory enforcement hinders market penetration in these regions, despite their rapidly growing infrastructure needs. Educating stakeholders and promoting the long-term cost benefits of flame retardant cables in preventing fire-related losses is essential to overcome this challenge.

MARKET RESTRAINTS

Availability of Substitutes and Competitive Pricing to Restrain Market Growth

The availability of alternative fire safety solutions and the competitive pricing of conventional cables act as significant restraints on the flame retardant cable market. While flame retardant cables offer enhanced safety, alternatives such as fire-resistant cables, ceramic-based coatings, and compartmentalization techniques are also used to achieve similar safety objectives. In cost-sensitive applications, end-users may opt for these alternatives or combine them with standard cables to reduce expenses. Additionally, the price difference between flame retardant cables and regular cables can be substantial, sometimes exceeding 30-40%, which deters price-conscious consumers, especially in regions with less stringent enforcement of safety norms. This competitive landscape pressures manufacturers to innovate cost-effectively without compromising quality.

Supply Chain Disruptions and Geopolitical Factors to Impede Market Stability

Supply chain disruptions and geopolitical factors present considerable restraints to the flame retardant cable market. The industry relies on a global supply chain for raw materials, including copper, aluminum, and specialty polymers, which are susceptible to disruptions caused by trade policies, natural disasters, or political instability. For example, trade tensions between major economies have led to tariffs and supply bottlenecks, increasing costs and delaying projects. Moreover, logistical challenges and fluctuating freight costs add to the complexity, affecting the timely delivery of products. These factors create uncertainty in the market, prompting end-users to seek local alternatives or delay projects, thereby restraining growth.

Slow Adoption in Retrofit and Upgrade Projects to Limit Market Penetration

The slow adoption of flame retardant cables in retrofit and upgrade projects is another restraint for the market. While new construction projects readily incorporate these cables due to regulatory compliance, existing infrastructure often undergoes gradual upgrades, where replacement with flame retardant variants may not be prioritized. Retrofitting involves additional costs, logistical challenges, and downtime, which many operators seek to avoid. In sectors like telecommunications and older industrial facilities, the urgency to upgrade cabling systems is low unless mandated by regulations or after a safety incident. This slow adoption pace limits the market’s growth potential in the retrofit segment, despite its significant size.

MARKET OPPORTUNITIES

Technological Advancements and Product Innovations to Unlock New Opportunities

Technological advancements and continuous product innovations present substantial opportunities for the flame retardant cable market. Manufacturers are investing in R&D to develop cables with improved properties such as higher fire resistance, reduced smoke emission, enhanced durability, and better environmental performance. For instance, the development of bio-based flame retardant materials and nanotechnology-integrated cables offers eco-friendly and high-performance solutions. These innovations cater to the evolving demands of sectors like data centers, electric vehicles, and renewable energy, where safety and efficiency are paramount. Companies that leverage these technologies can differentiate their products, capture niche markets, and command premium prices, driving overall market growth.

Expansion in Emerging Economies and Infrastructure Investments to Offer Growth Avenues

The expansion of the flame retardant cable market in emerging economies offers lucrative opportunities, driven by massive infrastructure investments and increasing regulatory focus on safety. Countries in Asia, Latin America, and the Middle East are witnessing rapid urbanization, industrial growth, and government initiatives to modernize infrastructure. For example, national smart city projects and investments in power transmission networks require advanced cabling solutions. As these regions strengthen their fire safety regulations and awareness grows, the demand for flame retardant cables is expected to surge. Market players can tap into these opportunities by establishing local presence, forming partnerships, and offering cost-effective solutions tailored to regional needs.

Increasing Focus on Sustainable and Eco-friendly Solutions to Drive Future Demand

The increasing global focus on sustainability and eco-friendly products creates significant opportunities for the flame retardant cable market. There is a growing preference for low-smoke halogen-free (LSHF) cables, which minimize toxic emissions and environmental impact during fires. Regulations and corporate policies emphasizing green building standards, such as LEED and BREEAM, encourage the use of sustainable cables. Additionally, the circular economy trend promotes recyclable and energy-efficient products. Manufacturers that develop and promote environmentally compliant flame retardant cables can gain a competitive edge, attract environmentally conscious customers, and align with global sustainability goals, thereby expanding their market share.

FLAME RETARDANT CABLE MARKET TRENDS

Stringent Fire Safety Regulations Driving Global Market Adoption

The global flame retardant cable market is experiencing significant growth, primarily driven by increasingly stringent fire safety regulations and building codes worldwide. Regulatory bodies, including the National Fire Protection Association (NFPA) in the United States and various European Union directives, mandate the use of flame retardant materials in construction and industrial applications to enhance public safety. These regulations are particularly rigorous in commercial buildings, public infrastructure, and transportation sectors, where the risk of fire must be minimized. The International Electrotechnical Commission (IEC) standards, such as IEC 60332, which specifies tests for vertical flame propagation for single vertical insulated wires or cables, have become a global benchmark, compelling manufacturers to produce compliant products. This regulatory pressure is not just a compliance issue but a fundamental driver of product specification and procurement decisions across the value chain. The market has responded with a compound annual growth rate (CAGR) of 3.7%, reflecting the steady and mandated adoption of these safety-critical components. While the initial cost of flame retardant cables is higher than standard alternatives, the long-term risk mitigation and potential for reduced insurance premiums are powerful economic incentives for their widespread use.

Other Trends

Rising Demand for Low-Smoke Halogen-Free (LSHF) Variants

A prominent trend within the flame retardant cable market is the accelerating shift towards Low-Smoke Halogen-Free (LSHF) cables, which now command over 70% of the global market share by product type. This preference is driven by a heightened awareness of the toxic hazards associated with traditional halogenated compounds, which, while effective at suppressing flames, can emit dense, corrosive, and toxic smoke when burned. LSHF cables, typically using materials like magnesium hydroxide or aluminium hydroxide as flame retardants, significantly reduce these secondary hazards, making them indispensable in enclosed public spaces such as airports, hospitals, metro systems, and high-rise buildings. The superior safety profile of LSHF cables is becoming a default specification in new construction projects, especially in developed regions with advanced safety protocols. This trend is further supported by material science innovations that improve the mechanical and electrical properties of LSHF compounds, making them more versatile and reliable for a broader range of applications beyond their initial niche uses.

Infrastructure Modernization and Renewable Energy Integration

Global infrastructure modernization efforts, coupled with the rapid expansion of renewable energy sources, are creating substantial new demand for flame retardant cables. The Buildings segment remains the largest application area, but significant growth is emerging from power plants, particularly those integrating solar and wind energy. These installations require cabling that can withstand harsh environmental conditions while providing absolute fire safety to protect high-value assets. The manufacturing factory sector also relies heavily on these cables to safeguard automated processes and sensitive machinery. Furthermore, massive government-led investments in smart city projects, which involve dense networks of sensors and communication lines, necessitate the use of fire-safe cabling infrastructure. The Asia-Pacific region, led by China, is a focal point for this trend due to its unprecedented pace of urbanization and industrial expansion, accounting for a substantial portion of the global demand. This broad-based infrastructural demand ensures a resilient and growing market, as these cables are integral to both new builds and the retrofitting of existing structures to meet modern safety standards.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Geographic Expansion to Secure Position

The global flame retardant cable market exhibits a semi-consolidated structure, characterized by the presence of several multinational corporations alongside numerous regional and specialized manufacturers. The market’s competitive intensity is high, driven by stringent safety regulations across the construction, industrial, and energy sectors worldwide. Nexans S.A. and Prysmian Group are unequivocally the dominant forces, collectively holding a significant portion of the global market share. Their leadership is anchored in extensive product portfolios, cutting-edge R&D capabilities, and a truly global distribution network that allows them to serve major projects in Europe, North America, and Asia-Pacific.

Leoni AG and Belden Inc. also command considerable market influence, particularly within specialized industrial and instrumentation applications. Their growth is largely attributed to a deep focus on high-performance, low-smoke halogen-free (LSHF) cables, which represent over 70% of the market by product type. These companies have built a strong reputation for reliability, which is paramount for critical infrastructure like power plants and manufacturing facilities.

Furthermore, strategic initiatives are a primary growth lever. Key players are actively engaging in mergers and acquisitions to bolster their technological expertise and expand their geographic footprint. Simultaneously, continuous investment in research and development is crucial for creating next-generation materials that offer enhanced fire safety and environmental compliance. This focus on innovation is expected to be a key differentiator and a major driver for market share growth throughout the forecast period.

Meanwhile, other significant players like Axon’ Cable and Keystone Cable are strengthening their positions by carving out niches in specific end-markets, such as aerospace, automotive, and transportation. Their strategy often involves forming strategic partnerships with OEMs and investing in custom solution development, ensuring their sustained relevance in a competitive landscape.

List of Key Flame Retardant Cable Companies Profiled

- Nexans S.A. (France)

- Prysmian Group (Italy)

- Keystone Cable (China)

- Axon’ Cable (France)

- Leoni AG (Germany)

- Belden Inc. (U.S.)

- Coleman Cable (U.S.)

- Shanghai Delixi (China)

- Tsubaki Kabelschlepp (Germany)

- Changzhou Bayi Cable (China)

Segment Analysis:

By Type

Low-smoke Halogen-free Flame-retardant Cable Segment Dominates the Market Due to Superior Safety and Environmental Standards

The market is segmented based on type into:

- Low-smoke Halogen-free

- Low-smoke Low-Halogen

- Low-smoke Halogen

By Application

Buildings Segment Leads Due to Stringent Fire Safety Regulations and Urbanization Trends

The market is segmented based on application into:

- Buildings

- Power Plant and Manufacturing Factory

- Others

By Insulation Material

Polymer-based Insulation Holds Major Share Owing to its Excellent Flame Retardant Properties

The market is segmented based on insulation material into:

- Polymer-based

- Mineral-based

- Others

By Voltage Rating

Low Voltage Cables Command Significant Market Share Due to Widespread Use in Building Infrastructure

The market is segmented based on voltage rating into:

- Low Voltage

- Medium Voltage

- High Voltage

Regional Analysis: Flame Retardant Cable Market

Europe

Europe is the largest market for flame retardant cables globally, holding over 25% market share. This dominance is driven by some of the world’s most stringent fire safety and environmental regulations, including the EU Construction Products Regulation (CPR) which mandates the use of cables with specific fire performance classifications in buildings. The widespread adoption of Low-Smoke Halogen-Free (LSHF) cables, which account for the vast majority of product sales, is a direct result of these mandates aimed at minimizing toxic smoke and corrosive gas emissions during a fire. Major infrastructure modernization projects, investments in renewable energy, and a strong focus on upgrading aging building stock further propel demand. Leading global manufacturers like Nexans (France) and Prysmian (Italy) have a significant presence here, driving innovation in high-performance, sustainable cable solutions.

Asia-Pacific

The Asia-Pacific region, led by China, represents the fastest-growing and highest volume market, collectively accounting for over 40% of global consumption. This explosive growth is fueled by massive urbanization, unprecedented investments in infrastructure development, and the rapid expansion of the construction and industrial sectors. China’s Belt and Road Initiative and its focus on building smart, safe cities have created immense demand. While cost sensitivity can sometimes lead to the use of less advanced halogenated cables in certain applications, there is a pronounced and accelerating shift toward LSHF variants, driven by growing environmental awareness and the adoption of stricter national safety standards. Domestic players like Shanghai Delixi and Changzhou Bayi Cable compete vigorously with international giants to serve this vast market.

North America

North America is a mature and highly regulated market, characterized by strict enforcement of fire codes such as the National Electrical Code (NEC) and standards from Underwriters Laboratories (UL). These regulations necessitate the use of flame retardant cables across commercial, residential, and industrial construction. The market is driven by a continuous cycle of building renovations, technological infrastructure upgrades in data centers, and investments in energy transmission. While the market growth is steady, it is highly innovation-focused, with a strong preference for cables that offer enhanced fire performance, reduced environmental impact, and long-term reliability. Key players like Belden and Coleman Cable are significant contributors to the regional supply.

South America

The flame retardant cable market in South America is developing, with growth primarily concentrated in larger economies like Brazil and Argentina. Demand is fueled by ongoing industrial development, mining activities, and gradual upgrades to urban infrastructure. However, market expansion faces headwinds from economic volatility, which impacts large-scale investment, and inconsistent enforcement of building safety codes outside major metropolitan areas. While there is a recognized need for improved fire safety, price often remains a primary purchasing criterion, which can slow the adoption of premium LSHF cables. The market presents a long-term opportunity as regulations evolve and economic conditions stabilize, but progress is expected to be measured.

Middle East & Africa

This region presents an emerging market with significant potential, though development is uneven. Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, are leading drivers due to ambitious megaprojects, smart city initiatives, and high-value construction that mandates advanced fire safety solutions. In these nations, the adoption of international standards and the use of high-quality LSHF cables are common. In contrast, other parts of Africa face challenges, including limited infrastructure investment, less stringent regulatory frameworks, and a greater focus on cost-effective solutions. Nonetheless, overall regional demand is on a gradual upward trajectory, supported by urbanization and economic diversification efforts in key countries.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Flame Retardant Cable markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Flame Retardant Cable Market?

-> Flame Retardant Cable Market was valued at 10480 million in 2024 and is projected to reach US$ 13420 million by 2032, at a CAGR of 3.7% during the forecast period.

Which key companies operate in Global Flame Retardant Cable Market?

-> Key players include Nexans, Prysmian, Keystone Cable, Axon’ Cable, Leoni AG, Belden Electronics, Coleman Cable, Shanghai Delixi, Tsubaki Kabelschlepp, and Changzhou Bayi Cable, among others.

What are the key growth drivers?

-> Key growth drivers include stringent fire safety regulations, increasing infrastructure development, growing demand from construction and power generation sectors, and rising investments in smart building technologies.

Which region dominates the market?

-> Europe is the largest market with over 25% share, while Asia-Pacific (particularly China) shows significant growth potential.

What are the emerging trends?

-> Emerging trends include development of eco-friendly halogen-free cables, integration of smart monitoring technologies, increased adoption in renewable energy projects, and advancements in material science for enhanced fire resistance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...