MARKET INSIGHTS

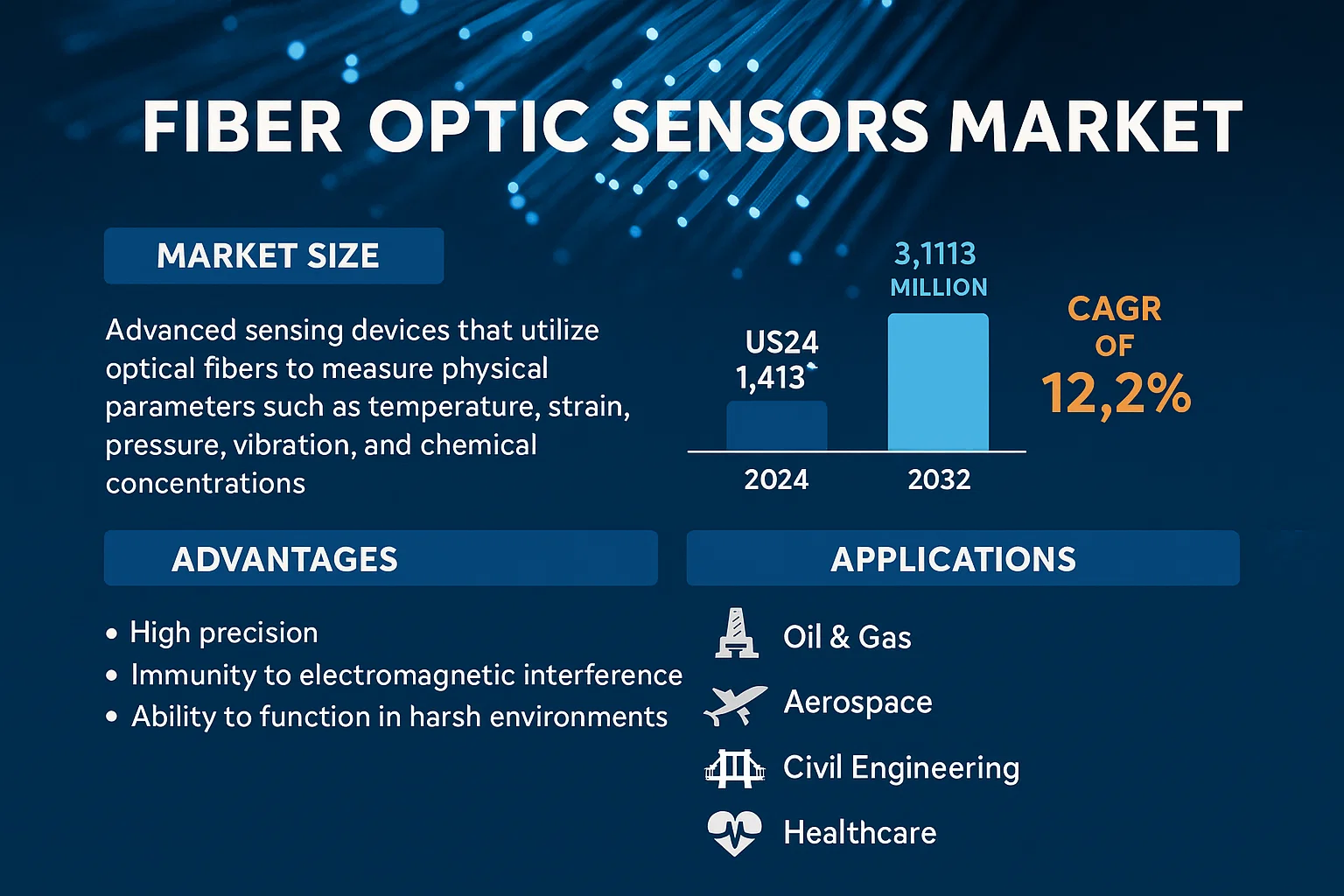

Global Fiber Optic Sensors Market size was valued at USD 1,413 million in 2024 to USD 3,111 million by 2032, exhibiting a CAGR of 12.2% during the forecast period.

Fiber optic sensors are advanced sensing devices that utilize optical fibers to measure physical parameters such as temperature, strain, pressure, vibration, and chemical concentrations. These sensors operate by transmitting light through an optical fiber and detecting changes in its properties, such as intensity, phase, or wavelength, caused by external stimuli. Their high precision, immunity to electromagnetic interference, and ability to function in harsh environments make them ideal for applications in industries like oil & gas, aerospace, civil engineering, and healthcare.

The market is witnessing robust growth due to increasing demand for real-time monitoring systems in critical infrastructure and industrial applications. The rising adoption of distributed sensing technology, particularly in smart cities and energy sectors, further drives market expansion. Key players such as Micron Optics, Honeywell, and Omron dominate the industry, collectively holding around 39% market share. Additionally, advancements in fiber Bragg grating (FBG) sensors and the expansion of 5G networks are expected to create new opportunities for market growth in the coming years.

MARKET DRIVERS

Increasing Demand from Oil & Gas and Infrastructure Sectors

The global push towards renewable energy and the need for efficient infrastructure monitoring are driving demand. Fiber optic sensors provide critical data for structural health monitoring in bridges, tunnels, and wind turbines, while the oil and gas industry uses them for pipeline monitoring and leak detection, reducing environmental risks.

Rising Adoption in Aerospace and Defense Applications

Advanced fiber optic sensors are increasingly used in aerospace for strain and temperature monitoring in aircraft structures, contributing to lighter and safer designs. Defense applications include perimeter security and underwater monitoring, where their immunity to electromagnetic interference is crucial.

➤ Enhanced capabilities in harsh environments drive adoption.

With the ability to operate in extreme temperatures, corrosive environments, and high radiation areas, fiber optic sensors are becoming the preferred choice for nuclear facilities and space applications where traditional sensors fail.

MARKET CHALLENGES

High Initial Investment and Installation Complexity

The sophisticated nature of fiber optic sensing systems requires significant upfront investment in both equipment and specialized personnel. Small and medium enterprises often find the initial costs prohibitive, especially when retrofitting existing infrastructure with these advanced monitoring systems.

Other Challenges

Technical Expertise Gap

The technology requires specialized knowledge for installation, calibration, and data interpretation. There’s a shortage of technicians and engineers with experience in both fiber optics and sensor technology, creating implementation bottlenecks even where budgets exist.

MARKET RESTRAINTS

High Cost of Advanced Sensing Solutions

While prices have decreased over the past decade, premium fiber optic sensing systems remain significantly more expensive than traditional electronic sensors. This cost barrier limits adoption in price-sensitive markets and applications where the superior performance is not absolutely necessary.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Vehicles and Smart Cities

Autonomous vehicles require highly reliable and precise sensing systems for navigation and obstacle detection. Fiber optic sensors offer advantages in size, weight, and electromagnetic immunity. Meanwhile, smart city initiatives are deploying these sensors for traffic monitoring, structural health monitoring of bridges, and utility monitoring, creating new revenue streams.

Fiber Optic Sensors Market Trends

Increased Demand for Distributed Sensing Solutions

Distributed fiber optic sensing (DFOS) technology continues to gain traction across various industries due to its ability to provide real-time monitoring over long distances. The market is seeing increased adoption in oil and gas pipeline monitoring, where these sensors detect leaks, third-party interference, and ground movement with high precision. Civil engineering applications, particularly in structural health monitoring of bridges, tunnels, and buildings, are driving demand as infrastructure aging becomes a global concern. The technology provides continuous monitoring without requiring extensive hardware along the entire length being monitored.

Other Trends

Advancements in Multiplexing Technologies

Wavelength division multiplexing (WDM) and time division multiplexing (TDM) technologies have significantly improved, allowing a single optical fiber to carry multiple sensor signals simultaneously. This reduces the cost per sensing point and enables more dense sensor networks. The development of fiber Bragg grating (FBG) based sensors has accelerated, offering high resolution and the ability to measure multiple parameters like strain and temperature simultaneously on the same fiber.

Integration with IoT and Industry 4.0

The integration of fiber optic sensors with the Internet of Things (IoT) platforms is a key trend, enabling real-time data collection and predictive maintenance in smart factories. Industry 4.0 initiatives are driving adoption as manufacturers seek to monitor equipment health and production processes with higher precision. These sensors provide data for predictive maintenance systems, reducing downtime in manufacturing, energy, and transportation sectors. The data from these sensors is increasingly being integrated with AI and machine learning algorithms to predict failures before they occur.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players and Market Structure

The global fiber optic sensors market is characterized by the presence of several established players and emerging specialists. The market is moderately fragmented with the top 5 manufacturers holding approximately 39% market share. These leading companies have extensive product portfolios, global distribution networks, and strong R&D capabilities focused on developing advanced sensing technologies for various industrial applications.

Beyond the market leaders, numerous other companies operate in specific niches or regional markets. These include specialized sensor manufacturers, fiber optic component suppliers, and system integrators who offer customized solutions for particular industries like oil and gas, infrastructure monitoring, or aerospace. These companies often focus on specific technology segments such as distributed sensing, point sensors, or multiplexed systems, catering to the diverse needs of end-users across different regions.

List of Key Fiber Optic Sensors Companies

- Micron Optics

- Honeywell

- FISO Technologies

- Omron

- FBGS TECHNOLOGIES GMBH

- Proximion

- Smart Fibres Limited

- Sensornet

- ITF Labs / 3SPGroup

- Keyence

- IFOS

- NORTHROP GRUMMAN

- O/E LAND, Inc

- KVH

- Photonics Laboratories

- Chiral Photonics

- FBG TECH

- OPTOcon GmbH

- Redondo Optics

- Wutos

- BEIYANG

- Bandweaver

- DSC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Distributed Sensors are gaining significant traction due to their ability to provide continuous monitoring along the entire length of the fiber, making them ideal for large-scale infrastructure monitoring where precise location detection is critical. |

| By Application |

|

Strain Sensing applications continue to dominate due to their critical role in structural health monitoring across civil engineering, aerospace, and energy infrastructure where precise deformation measurement is paramount. |

| By End User |

|

Aerospace & Defense sector demonstrates the highest growth momentum due to increasing investments in advanced surveillance systems, structural health monitoring of aircraft, and the development of next-generation military equipment requiring precise and immune sensing technologies. |

| By Technology |

|

Fiber Bragg Grating (FBG) technology maintains dominance due to its maturity, reliability, and cost-effectiveness for multipoint sensing applications, particularly in structural health monitoring and temperature monitoring across industries. |

| By Region |

|

Asia Pacific region shows the most dynamic growth driven by massive infrastructure development, increasing industrialization, and the rapid adoption of Industry 4.0 technologies across major economies like China, Japan, and South Korea. |

Regional Analysis: Fiber Optic Sensors Market

North American aerospace giants leverage fiber optic sensors for real-time structural health monitoring in next-generation aircraft, enabling predictive maintenance and reducing operational costs. The region’s dominance in defense spending ensures continued investment in advanced sensor technologies for military applications.

The extensive North American oil and gas industry utilizes distributed fiber optic sensing for pipeline integrity monitoring across thousands of miles, preventing environmental disasters and optimizing maintenance schedules. The transition to renewable energy sees increased deployment in wind turbine monitoring across the continent.

As the birthplace of Industry 4.0 concepts, North American manufacturers rapidly adopt smart sensor technologies for quality control and predictive maintenance. The region’s strong automotive sector utilizes fiber optic sensors in automated assembly lines and robotic welding systems.

North America remains the global center for photonics research with leading universities and corporate labs continuously pushing the boundaries of fiber optic sensing technology. This innovation ecosystem consistently delivers more sensitive, accurate, and cost-effective solutions that drive adoption across industries.

Europe

Europe represents the second largest market for fiber optic sensors, characterized by its strong industrial base and emphasis on quality assurance. The region’s leadership in automotive manufacturing (particularly German automakers) drives adoption in automated production lines and quality control systems. Strict European Union regulations regarding industrial safety and environmental protection mandate advanced monitoring systems in chemical plants and energy infrastructure. The region’s historical strength in optical engineering (particularly in Germany and the UK) supports continued innovation in sensor design and applications.

Asia-Pacific

The Asia-Pacific region demonstrates the fastest growth rate in fiber optic sensor adoption, though from a smaller base than North America. Japan and South Korea lead in industrial applications through partnerships with global manufacturing firms, while China’s massive infrastructure investment includes fiber optic monitoring in bridges, tunnels, and energy projects. The region’s rapid industrialization creates demand for predictive maintenance solutions, though the market remains more fragmented than in the West. Southeast Asian nations increasingly adopt these technologies in urban development and manufacturing hubs.

South America

South America represents an emerging market with specific regional strengths in mining and energy applications. Chilean and Brazilian mining operations utilize fiber optic sensing for structural monitoring in challenging terrain, while Brazil’s offshore oil industry adopts similar technologies for subsea pipeline monitoring. The region shows steady but slower adoption rates compared to global leaders, with growth concentrated in specific industrial sectors rather than widespread adoption.

Middle East & Africa

These regions show the lowest adoption rates globally but with significant growth potential in specific applications. Middle Eastern oil producers increasingly utilize fiber optic sensing in refineries and pipeline networks, while African nations show patchy adoption concentrated around South African industrial centers and Nigerian oil fields. The regions’ development priorities and infrastructure challenges create different adoption patterns than more mature markets.

Report Scope

This market research report provides a comprehensive analysis of the Fiber Optic Sensors Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Fiber Optic Sensors Market?

-> The global Fiber Optic Sensors market was valued at US$ 1413 million in 2024 and is projected to reach US$ 3111 million by 2032.

What is the growth rate of Fiber Optic Sensors Market?

-> The market is expected to grow at a CAGR of 12.2% from 2025 to 2032.

Which are the key companies in Fiber Optic Sensors Market?

-> Key players include Micron Optics, Honeywell, FISO Technologies, Omron, FBGS TECHNOLOGIES GMBH, Proximion, Smart Fibres Limited, Sensornet, ITF Labs / 3SPGroup, Keyence, IFOS, NORTHROP GRUMMAN, O/E LAND, Inc, KVH, Photonics Laboratories, Chiral Photonics, FBG TECH, OPTOcon GmbH, Redondo Optics, Broptics, Wutos, Pegasus (Qingdao) Optoelectronics, BEIYANG, Bandweaver, DSC, among others.

What are the key applications of Fiber Optic Sensors?

-> Key applications include Oil & Gas, Buildings and Bridges, Tunnels, Dams, Heritage Structures, Power Grid, Aerospace Applications.

Which regions are key for Fiber Optic Sensors Market?

-> The market is globally distributed with key regions including North America (US, Canada, Mexico), Europe (Germany, France, U.K., Italy, Russia, Nordic Countries, Benelux, Rest of Europe), Asia (China, Japan, South Korea, Southeast Asia, India, Rest of Asia), South America (Brazil, Argentina, Rest of South America), and Middle East & Africa (Turkey, Israel, Saudi Arabia, UAE, Rest of Middle East & Africa).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...