MARKET INSIGHTS

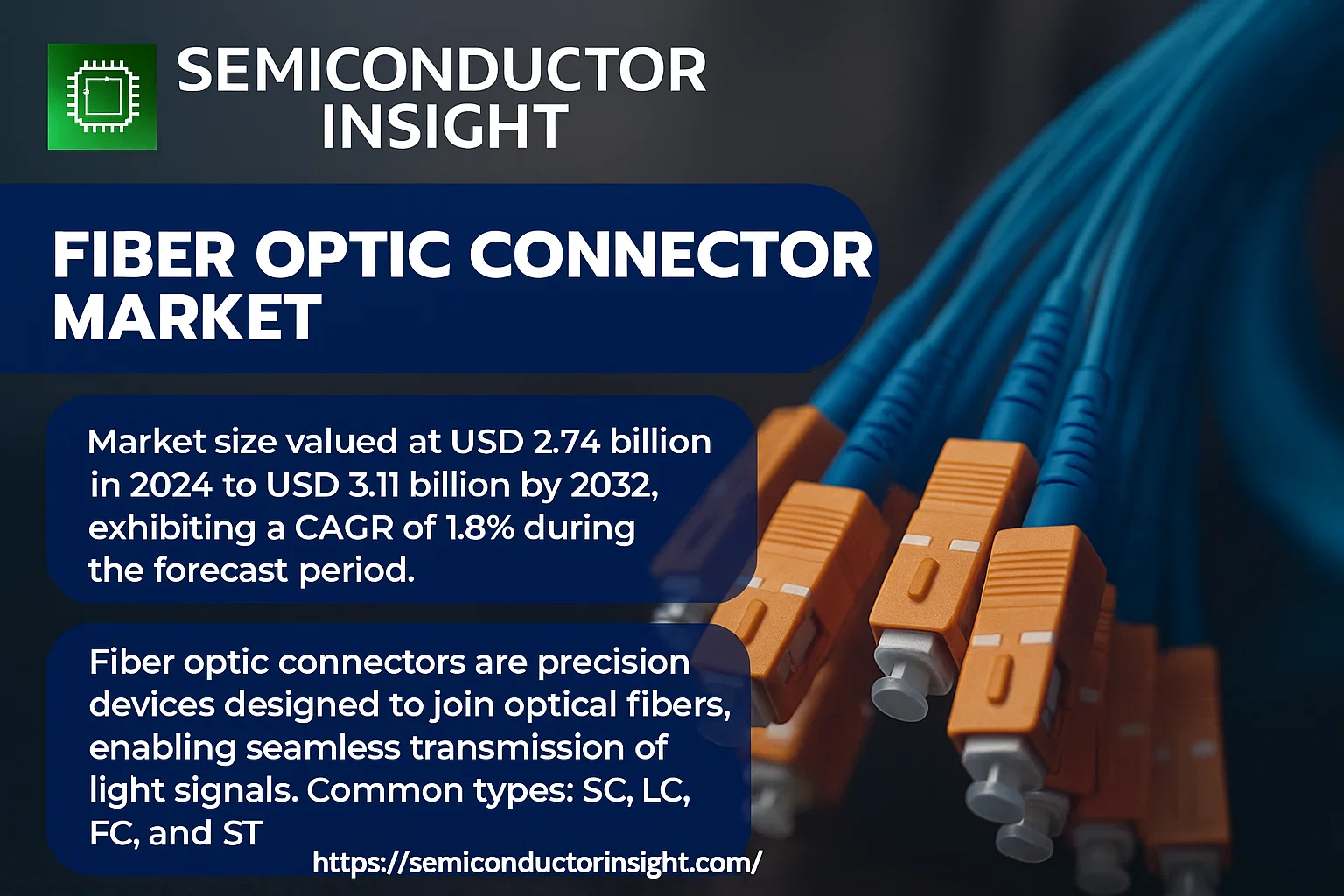

Global Fiber Optic Connector Market size was valued at USD 2.74 billion in 2024 to USD 3.11 billion by 2032, exhibiting a CAGR of 1.8% during the forecast period.

Fiber optic connectors are precision devices designed to join optical fibers, enabling seamless transmission of light signals between sections of fiber optic cables. These components are engineered at microscopic scales (0.1um precision) to minimize signal loss, ensuring high-speed data transfer in telecommunications and networking applications. Common connector types include SC, LC, FC, and ST variants, each offering specific advantages for different deployment scenarios.

Asia dominates the global market, accounting for 68% of production volume, with China and Taiwan collectively representing 44% of regional consumption. While the market remains fragmented (top 6 players hold 46% share), key manufacturers like CommScope, Amphenol, and Sumitomo Electric are driving innovation through advanced connector designs that support 5G infrastructure and hyperscale data centers. The commercial sector constitutes the largest application segment due to escalating bandwidth demands across enterprise networks.

MARKET DRIVERS

Exploding Global Data Consumption

The unprecedented surge in global data traffic, fueled by 5G deployment, rising streaming services, and cloud computing, is the primary driver for the fiber optic connector market. The demand for higher bandwidth and faster transmission speeds necessitates robust fiber optic infrastructure, where connectors are critical components for ensuring low-loss, reliable signal connections. This is particularly evident in data centers, which are expanding rapidly to support modern digital economies.

Expansion of FTTx Networks

Worldwide initiatives to deploy Fiber-to-the-x (FTTx) networks, including FTTH (Fiber-to-the-Home), are a major growth driver. Governments and telecommunication providers are heavily investing in upgrading last-mile connectivity to deliver high-speed internet directly to residences and businesses. This large-scale infrastructure rollout directly translates into massive demand for fiber optic connectors, with the market for these components in FTTx applications projected to grow at a CAGR of approximately 9% over the next five years.

➤ The standardization and miniaturization of connectors like the LC and MTP/MPO types are enabling higher port densities in communication equipment, a critical factor for next-generation network architectures.

Furthermore, advancements in connector technology that reduce insertion loss and reflectivity are allowing for longer transmission distances and more complex network topologies, meeting the stringent requirements of modern telecommunications and enterprise networks.

MARKET CHALLENGES

High Installation and Maintenance Costs

The initial capital expenditure for deploying fiber optic networks, including the cost of connectors, fusion splicers, and skilled labor for precise terminations, remains a significant barrier. Maintaining the physical integrity of connectors against contamination and damage in harsh environments also adds to the total cost of ownership, posing a challenge for widespread adoption, especially in cost-sensitive markets.

Other Challenges

Intense Price Competition

The market is characterized by the presence of numerous global and regional manufacturers, leading to intense price competition. This pressure can squeeze profit margins and potentially compromise on quality, especially from low-cost producers, creating challenges for established players who invest heavily in R&D.

Technical Complexity and Skill Shortage

The precise alignment required for low-loss optical connections demands highly skilled technicians. A global shortage of trained personnel capable of handling advanced fiber optic installation and testing equipment can delay project timelines and increase operational costs.

MARKET RESTRAINTS

Maturity in Key Geographic Markets

The fiber optic connector market in developed regions like North America and parts of Europe is reaching a stage of maturation. While upgrades and replacements continue, the explosive growth phase from initial fiber deployment has slowed. This relative saturation acts as a restraint on the overall market growth rate, shifting the focus towards emerging economies for significant expansion.

Competition from Alternative Technologies

In specific short-range applications, such as within data center racks or consumer electronics, advanced copper-based solutions (e.g., Direct Attach Copper Cables) and emerging wireless technologies like Li-Fi present competitive alternatives. For connections under a few meters where extreme bandwidth is not critical, these alternatives can offer a more cost-effective solution, restraining fiber optic connector uptake in these niche segments.

MARKET OPPORTUNITIES

Growth in Emerging Economies

Significant opportunities lie in the Asia-Pacific, Latin America, and Middle East & Africa regions, where telecommunications infrastructure is still being extensively developed. Government digitalization programs and private investments are fueling the demand for fiber optic connectivity, creating a substantial and growing market for connectors. This region is expected to account for over 50% of the global market growth in the coming years.

Adoption in New Industrial Applications

Beyond traditional telecom and data centers, fiber optic connectors are finding new opportunities in industrial automation, military & aerospace, and medical devices. The inherent advantages of immunity to electromagnetic interference, small size, and high bandwidth are making them the preferred choice for sophisticated sensing, imaging, and control systems in these demanding sectors.

Development of Advanced Connector Designs

The ongoing push for higher density and faster deployment is driving innovation in connector design. Opportunities abound for companies developing field-installable connectors, multi-fiber push-on (MPO) connectors for high-speed data centers, and robust connectors for harsh industrial environments, opening new revenue streams.

Fiber Optic Connector Market Trends

Sustained Market Growth Fueled by Global Connectivity Demands

The global Fiber Optic Connector market, valued at $2.748 billion in 2024, is projected to grow steadily to reach $3.113 billion by 2032, representing a Compound Annual Growth Rate (CAGR) of 1.8%. This consistent growth is primarily driven by the escalating global demand for high-speed data transmission across telecommunications, data centers, and broadband networks. The precision engineering of these connectors, which align optical fibers at a microscopic scale of 0.1um, is fundamental to enabling the high-speed internet, cloud computing, and 5G infrastructure rollouts that define the modern digital economy. As global data consumption continues to surge, the need for reliable and efficient fiber optic connectivity solutions remains a powerful market driver.

Other Trends

Dominance of the Asia-Pacific Region

Asia is the largest market for fiber optic connectors, accounting for a 68% share of global production. China and Taiwan are the largest consumers in the region, collectively holding a 44% market share in Asia, followed by Japan and South Korea. The regions of India and Southeast Asia are exhibiting particularly high growth rates in both production and consumption, driven by massive infrastructure investments and expanding internet penetration. This regional concentration underscores the critical role of Asia-Pacific in the global supply chain and its influence on market dynamics.

Technological Diversification and Competitive Landscape

The market features a diverse range of connector types including SC, FC, LC, and ST connectors, each serving different application needs in residential, commercial, and public sectors. The competitive landscape is characterized by a low concentration; the top six listed companies, including CommScope, Amphenol, Molex, Sumitomo Electric, FIT, and China Fiber Optic, collectively hold approximately 46% of the market share. This indicates a fragmented but highly competitive environment where technological innovation, cost efficiency, and strategic partnerships are key factors for maintaining and growing market position. As demand evolves, manufacturers are continuously developing more compact, high-density, and easier-to-install connector solutions to meet the requirements of next-generation networks.

COMPETITIVE LANDSCAPE

Key Industry Players

A Fragmented Market Dominated by Global Connectivity Giants

The global fiber optic connector market is characterized by moderate concentration, where the top six companies account for approximately 46% of the total market share. The competitive landscape is led by a cohort of established global players with extensive portfolios and technological expertise. CommScope and Amphenol are prominent leaders, leveraging their broad reach in communication infrastructure and interconnect solutions. Molex (a subsidiary of Koch Industries) and Japan’s Sumitomo Electric are also dominant forces, providing high-precision components critical for data centers and telecommunications networks. Foxconn Interconnect Technology (FIT) stands out as a significant player, recognized as the world’s largest manufacturing foundry for fiber optic connectors, underlining the industry’s reliance on scaled production capabilities.

Beyond the top tier, the market supports a diverse ecosystem of specialized and regional manufacturers that secure strong positions in niche applications. Companies like Corning, a leader in optical fiber and cable, and Huber+Suhner, known for high-performance connectivity, cater to demanding environments. Japanese connectors specialists such as JAE and Hirose offer advanced miniaturized solutions. Radiall, 3M, and Senko Advanced Components are other key contributors with strong technological offerings. In the Asia-Pacific region, which dominates both production and consumption, local players like China Fiber Optic, Yazaki, Sunsea Telecommunications, and Jonhon are significant, particularly in the cost-sensitive and rapidly growing Chinese market. This structure ensures robust competition, driving continuous innovation in connector design, durability, and performance to meet the escalating demands of 5G, FTTx, and hyperscale data centers.

List of Key Fiber Optic Connector Companies Profiled

- CommScope

- Amphenol Corporation

- Molex (Koch Industries)

- Sumitomo Electric Industries, Ltd.

- Foxconn Interconnect Technology (FIT)

- Corning Incorporated

- HUBER + SUHNER AG

- Radiall

- 3M

- Japan Aviation Electronics Industry, Ltd. (JAE)

- Senko Advanced Components

- Yazaki Corporation

- Rosenberger-OSI

- AFL

- LEMO

- Hirose Electric Co., Ltd.

- China Fiber Optic

- Sunsea Telecommunications Co., Ltd.

- Jonhon

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

LC Connector demonstrates a commanding presence due to its compact size, which is ideally suited for high-density applications in modern data centers and telecommunications racks. This segment’s dominance is further reinforced by its push-pull latching mechanism, which offers superior ease of use and reliability compared to twist-type connectors. The relentless global demand for higher bandwidth and more compact network equipment continues to drive the adoption of LC connectors across both new installations and upgrade projects, establishing it as the preferred choice for future-proof network infrastructure. |

| By Application |

|

Data Centers represent the most critical and rapidly evolving application segment, fueled by the exponential growth of cloud computing, big data analytics, and hyperscale computing requirements. The demanding environment of data centers necessitates connectors that offer exceptional performance, minimal insertion loss, and the ability to support immense data throughput. Continuous technological advancements and the global construction of new hyperscale facilities create a sustained and robust demand for high-performance fiber optic connectors, making this application area a primary driver of market innovation and growth. |

| By End User |

|

Internet Content Providers (ICP)/Cloud Giants are the dominant force, driving market trends through massive capital expenditures on global network infrastructure to support their expanding services. This end-user segment demands connectors that guarantee ultra-low latency and supreme reliability for their mission-critical operations. Their continuous investment in building and upgrading data centers and long-haul networks directly translates into significant and consistent procurement volumes, positioning them as the most influential buyers whose technical specifications often set de facto industry standards. |

| By Connector Standard |

|

Multi-fiber Push-On (MPO/MTP) Connectors are gaining remarkable traction as the leading segment within this category, primarily due to the industry-wide shift towards high-density fiber deployment. The ability of MPO connectors to terminate multiple fibers simultaneously offers unparalleled efficiency for 40G, 100G, and emerging 400G Ethernet applications, drastically reducing installation time and physical space requirements in data centers. This trend is central to supporting the backbone of modern cloud infrastructure and is a key focus area for connector manufacturers’ research and development efforts. |

| By Installation Environment |

|

Indoor installations constitute the most significant segment, driven by the proliferation of fiber-to-the-desk, local area networks within corporate buildings, and the expansive growth of hyperscale data centers. Connectors for indoor use prioritize factors like dust resistance, ease of handling for frequent reconfigurations, and high density. The relentless digital transformation across all business sectors ensures that the demand for reliable indoor fiber optic connectivity remains the cornerstone of the market, with ongoing innovations focused on simplifying installation and maintenance processes for end-users. |

Regional Analysis: Fiber Optic Connector Market

Asia-Pacific’s dominance is heavily rooted in its extensive manufacturing capabilities, particularly in China, Taiwan, and South Korea. These countries host the world’s leading producers of fiber optic components, creating a highly efficient and competitive supply chain. This concentration allows for rapid innovation cycles and cost-effective production, making it the primary sourcing region for global markets and reinforcing its leadership position through economies of scale and technical expertise.

Proactive government policies are a key differentiator. National broadband plans and digital economy visions are not just aspirational but are backed by significant public investment. These initiatives mandate extensive fiber optic deployment, creating a predictable and large-scale demand for connectors. This top-down approach ensures long-term market stability and growth, attracting further private investment and technological advancement within the region.

The relentless rollout of 5G infrastructure and the construction of massive hyperscale data centers are major demand drivers. Each new 5G tower requires fiber connectivity, while data centers rely on vast internal fiber networks for server interconnection. The high population density and rapid urbanization in the region intensify this demand, making it the epicenter for next-generation connectivity projects that depend on advanced fiber optic connectors.

The competitive market environment in Asia-Pacific fosters a strong focus on research and development. Local companies are pioneers in developing smaller, denser, and higher-performance connector solutions like MPO/MTP arrays to meet the demands of modern data centers and 5G networks. This culture of innovation ensures that the region remains at the cutting edge, constantly pushing the capabilities and applications of fiber optic connectivity.

North America

The North American fiber optic connector market is characterized by its maturity and a strong focus on upgrading existing infrastructure to support soaring data consumption. The region, led by the United States, is experiencing significant demand driven by the ongoing deployment of fiber-to-the-premises (FTTP) to replace aging copper networks, particularly in suburban and rural areas. Furthermore, the insatiable growth of cloud computing, streaming services, and the Internet of Things (IoT) is fueling massive investments in hyperscale data centers, which are heavily reliant on high-density fiber optic interconnects. The market is also influenced by substantial investments from telecommunications giants in expanding their 5G network backhaul capabilities. Regulatory support and federal funding initiatives aimed at closing the digital divide are providing additional impetus for widespread fiber deployment, ensuring a steady demand for reliable and high-performance connector solutions.

Europe

Europe represents a stable and technologically advanced market for fiber optic connectors, driven by the European Union’s ambitious digital agenda and stringent regulations promoting high-speed internet access. The Green Deal and initiatives like the Digital Compass are pushing member states to accelerate the rollout of gigabit-capable networks, creating a consistent demand for fiber infrastructure components. Markets in Western Europe, such as Germany, the UK, and France, are leading in FTTH/B deployments, while Eastern European countries are undergoing rapid network modernization. The region shows a strong emphasis on quality, reliability, and standardization, with a growing focus on sustainable and energy-efficient network solutions. The presence of major industrial and automotive sectors also drives demand for specialized fiber optic connectors used in manufacturing automation and harsh environments, adding a unique dimension to the market dynamics.

South America

The South American market is in a growth phase, with potential largely tied to economic stability and increasing digitalization efforts. Brazil is the dominant player, with ongoing investments from major telecommunication operators to expand fiber optic coverage in urban centers and, gradually, to underserved regions. Government initiatives aimed at improving national connectivity are providing a foundation for growth, though progress can be uneven across the continent. The market demand is primarily fueled by the consumer broadband segment, with a growing middle class adopting high-speed internet services. While the pace of adoption is slower compared to other regions, the significant infrastructure gap presents a substantial long-term opportunity for fiber optic connector suppliers as countries prioritize closing their digital divides and supporting economic development through improved connectivity.

Middle East & Africa

The Middle East & Africa region exhibits a bifurcated market dynamic. The Gulf Cooperation Council (GCC) countries in the Middle East are characterized by ambitious, government-led visions to create smart cities and knowledge-based economies, driving high investment in cutting-edge fiber optic infrastructure. These projects require advanced, high-capacity connectors. In contrast, many parts of Africa are focused on foundational connectivity, with market growth driven by mobile network operators expanding their fiber backhaul to support escalating mobile data traffic. Pan-continental submarine cable landings are also creating hubs of connectivity, spurring local fiber network development. The region presents a landscape of high-growth potential, albeit with challenges related to varying levels of economic development and infrastructure readiness, making it a market of strategic long-term interest.

Report Scope

This market research report provides a comprehensive analysis of the Fiber Optic Connector Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Fiber Optic Connector Market?

-> Global Fiber Optic Connector Market was valued at USD 2748 million in 2024 and is projected to reach USD 3113 million by 2032, exhibiting a CAGR of 1.8% during the forecast period.

Which key companies operate in Fiber Optic Connector Market?

-> Key players include CommScope, Amphenol, Molex, Sumitomo Electric, FIT, and China Fiber Optic, among others. The top 6 companies account for approximately 46% of the market.

What are the key growth drivers?

-> Key growth drivers include the expansion of telecommunication networks, increasing demand for high-speed data transmission, modular network management, and cross-connect flexibility provided by the connectors.

Which region dominates the market?

-> Asia is the largest market for fiber optic connectors, accounting for a 68% share of global production. China and Taiwan are the largest consumers within the region. India and Southeast Asia are high-growth regions.

What are the emerging trends?

-> Emerging trends include the adoption of various connector types such as SC, FC, ST, LC, and E2000 connectors, alongside ongoing technological precision advancements in fiber alignment. High growth in consumption from developing regions is also a significant trend.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...