Market Insights

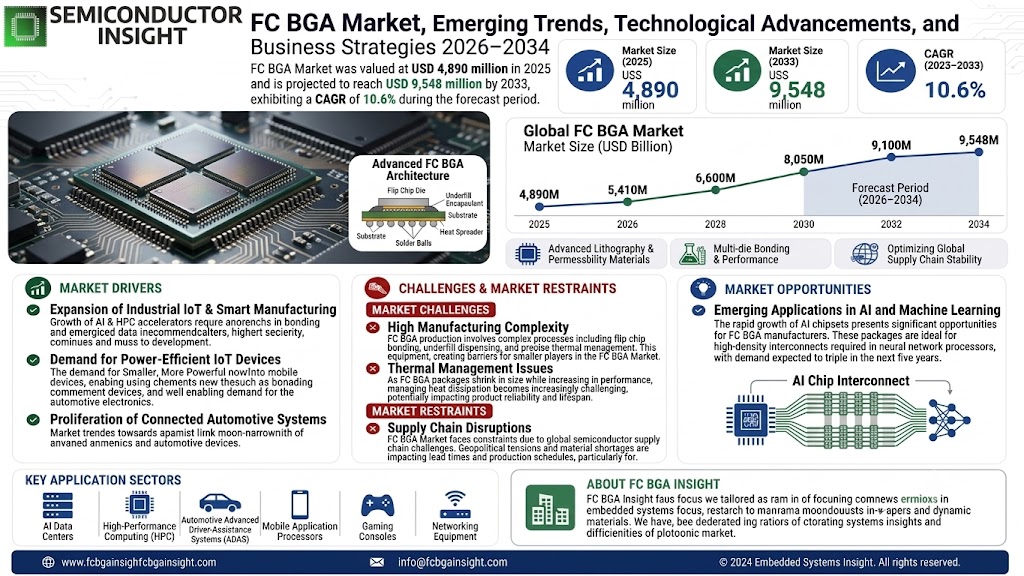

Global FC BGA Market was valued at USD 4,890 million in 2025 and is projected to reach USD 9,548 million by 2033, exhibiting a CAGR of 10.6% during the forecast period.

Flip Chip Ball Grid Array (FC BGA) is a mid-cost, high-performance semiconductor packaging solution that utilizes controlled collapse chip connection (C4) technology for die-to-substrate interconnection. This advanced packaging method enables higher signal density and functionality within a compact footprint, making it ideal for applications where performance outweighs cost considerations. FC BGA packages are compatible with standard printed circuit boards and can be repaired using conventional techniques.

The market growth is driven by increasing demand for high-performance computing, artificial intelligence chips, and data center applications. The adoption of Ajinomoto Build-up Film (ABF) substrates – multilayer microcircuit components essential for modern CPUs and GPUs – further supports this expansion. Key players like Unimicron, Ibiden, and AT&S dominate the market, collectively holding approximately 74% share. Taiwan leads in production with 30% market share, followed by mainland China and South Korea at 17% each.

MARKET DRIVERS

Growing Demand for High-Performance Electronics

FC BGA (Flip Chip Ball Grid Array) Market is witnessing significant growth due to increasing demand for compact, high-performance electronic devices. The adoption of FC BGA packages in smartphones, AI processors, and data centers is driving market expansion. Advanced packaging technologies offer superior thermal and electrical performance, making them ideal for next-generation applications.

Technological Advancements in Semiconductor Packaging

Innovations in FC BGA technology, such as finer pitch interconnects and improved thermal management, are accelerating adoption across industries. Leading semiconductor manufacturers are investing heavily in R&D to enhance package reliability and reduce production costs.

With the rise of autonomous vehicles and HPC (High-Performance Computing) applications, demand for FC BGA solutions is expected to remain strong in the coming years.

MARKET CHALLENGES

High Manufacturing Complexity

FC BGA production involves complex processes including flip chip bonding, underfill dispensing, and precise thermal management. This complexity increases manufacturing costs and requires specialized equipment, creating barriers for smaller players in the FC BGA Market.

Other Challenges

Thermal Management Issues

As FC BGA packages shrink in size while increasing in performance, managing heat dissipation becomes increasingly challenging, potentially impacting product reliability and lifespan.

MARKET RESTRAINTS

Supply Chain Disruptions

FC BGA Market faces constraints due to global semiconductor supply chain challenges. Geopolitical tensions and material shortages are impacting lead times and production schedules, particularly for advanced packaging solutions requiring specialized substrates.

MARKET OPPORTUNITIES

Emerging Applications in AI and Machine Learning

The rapid growth of AI chipsets presents significant opportunities for FC BGA manufacturers. These packages are ideal for high-density interconnects required in neural network processors, with demand expected to triple in the next five years.

FC BGA Market Trends

Strong Growth Projected for FC BGA Market

Global FC BGA Market, valued at USD 4.89 billion in 2025, is projected to reach USD 9.55 billion by 2033, growing at a CAGR of 10.6%. This growth is driven by increasing demand for high-performance semiconductor packaging solutions in computing and telecommunications. The 4-8 layer ABF substrate segment dominates with 69% market share, primarily used in PC applications (40% market share). Taiwan leads production with 30% global share, followed by mainland China and South Korea at 17% each.

Other Trends

Tariff Policies Impacting Supply Chains

Recent U.S. tariff implementations and international trade policies are reshaping FC BGA Market dynamics, affecting regional competitive structures. Manufacturers are evaluating alternative supply chain configurations to mitigate risks, with particular attention to ABF substrate sourcing from Japan and South Korea.

Technology Adoption in Key Applications

The HPC/AI chips segment shows the fastest growth potential as advanced processors demand higher-density FC BGA packaging. Meanwhile, PC applications continue as the largest market segment due to sustained demand for performance computing.

Market Concentration Among Manufacturers

Top five FC BGA producers (Unimicron, Ibiden, AT&S, Nan Ya PCB, Shinko Electric) control 74% of the market. Recent capacity expansions in Taiwan highlight the region’s strategic importance in semiconductor packaging supply chains.

Regional Market Developments

Asia maintains market dominance with Taiwan, China, and South Korea collectively representing 64% of global FC BGA production. North American and European markets are focusing on supply chain resilience, with increased investments in testing and packaging facilities to reduce overseas dependencies.

COMPETITIVE LANDSCAPE

Key Industry Players

FC BGA Market Dominated by Asian Manufacturers with 74% Market Concentration

FC BGA Market exhibits high concentration with the top five players Unimicron, Ibiden, AT&S, Nan Ya PCB, and Shinko Electric Industries controlling approximately 74% of global production capacity. Taiwan remains the manufacturing epicenter, accounting for 30% of global output, followed by mainland China and South Korea at 17% each. Market leadership stems from advanced ABF substrate capabilities and strategic relationships with leading semiconductor companies, particularly for high-performance computing applications.

Niche players like Kinsus Interconnect and Zhen Ding Technology are gaining traction through specialized offerings in HPC/AI chip packaging, while Korean manufacturers like LG InnoTek and Semco maintain strong positions in server applications. Recent capacity expansions by Daeduck Electronics and Shennan Circuit indicate growing competition in the mid-layer (4-8 layer) substrate segment, which currently accounts for 69% of total FC BGA production. The market remains technology-driven, with R&D focused on finer pitch solutions below 20µm.

List of Key FC BGA Companies Profiled

- Unimicron

- Ibiden

- Nan Ya PCB

- Shinko Electric Industries

- Kinsus Interconnect

- AT&S

- Semco

- Kyocera

- TOPPAN

- Zhen Ding Technology

- Daeduck Electronics

- Shenzhen Fastprint Circuit Tech

- Zhuhai Access Semiconductor

- LG InnoTek

- Shennan Circuit

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

4-8 Layers FCBGA Substrate dominates the market due to:

|

| By Application |

|

PCs represent the largest application segment because:

|

| By End User |

|

Consumer Electronics leads due to:

|

| By Substrate Technology |

|

ABF Substrates are preferred because:

|

| By Manufacturing Complexity |

|

Standard FCBGA maintains dominance owing to:

|

Regional Analysis: FC BGA Market

Asia-Pacific FC BGA Market

China’s Yangtze River Delta and Pearl River Delta regions host concentrated FC BGA production facilities, supported by mature IC packaging infrastructure. Taiwan’s Hsinchu Science Park serves as another critical manufacturing cluster for advanced FC BGA solutions.

South Korean and Japanese firms lead in developing fine-pitch FC BGA and substrate-less packaging variants. This technological edge allows APAC manufacturers to produce higher-density interconnects demanded by AI processors and advanced memory applications.

Proximity to wafer fabs and substrate suppliers creates cost efficiencies in APAC’s FC BGA production. Regional material science advancements in underfill compounds and thermal interface materials further support packaging reliability requirements.

Local smartphone brands, automotive Tier 1 suppliers, and data center operators drive strong domestic FC BGA consumption. This demand stability allows manufacturers to maintain high utilization rates and continuous process improvements.

North America FC BGA Market

North America maintains strong positions in high-value FC BGA segments, particularly for defense and aerospace applications. The region benefits from close collaboration between packaging firms and fabless semiconductor companies developing advanced processors. Silicon Valley’s ecosystem fosters innovative FC BGA solutions for AI accelerators and high-performance computing. Domestic manufacturers focus on specialized low-volume, high-margin production with stringent reliability requirements. Recent reshoring initiatives have increased investment in domestic FC BGA packaging capabilities.

Europe FC BGA Market

European FC BGA activity centers around automotive and industrial applications, with Germany and France as key markets. The region emphasizes reliability-focused packaging solutions for harsh environment applications. European firms collaborate closely with automotive OEMs to develop FC BGA packages meeting stringent automotive qualification standards. Research institutions contribute materials science innovations enabling higher temperature operation and vibration resistance in FC BGA packages.

South America FC BGA Market

South America’s FC BGA Market remains relatively small but shows growth potential in consumer electronics assembly. Brazil serves as the regional hub with developing packaging infrastructure. Most FC BGA components are imported, though local assembly of finished products creates some demand. The market faces challenges including limited local semiconductor infrastructure and reliance on global supply chains.

Middle East & Africa FC BGA Market

MEA’s FC BGA Market focuses on telecommunications infrastructure and oil/gas applications. The UAE and South Africa lead in regional technology adoption. Limited local manufacturing means most FC BGA packages are imported. However, growing data center construction and 5G deployments drive increasing demand. Some regional players are establishing FC BGA testing and qualification capabilities to serve local market needs.

Report Scope

This market research report provides a comprehensive analysis of the FC BGA Market, covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of FC BGA Market?

-> FC BGA Market was valued at USD 4,890 million in 2025 and is projected to reach USD 9,548 million by 2033, exhibiting a CAGR of 10.6% during the forecast period.

Which key companies operate in FC BGA Market?

-> Key players include Unimicron, Ibiden, AT&S, Nan Ya PCB, Shinko Electric Industries, Kinsus Interconnect, Semco, Kyocera, TOPPAN, and Zhen Ding Technology, among others. The top five players hold about 74% market share.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-performance semiconductor packaging, advancements in ABF substrate technology, and growth in PC and server markets.

Which region dominates the market?

-> China Taiwan is the world’s largest market for FC BGA with about 30% share, followed by China mainland and South Korea with 17% share each.

What are the key application segments?

-> The PCs segment dominates with about 40% market share, followed by Server & Data Center and HPC/AI Chips applications.

What are the major product types?

-> 4-8 Layers FCBGA Substrate accounts for the largest segment with about 69% market share.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...