Fab-Lite Market Insights

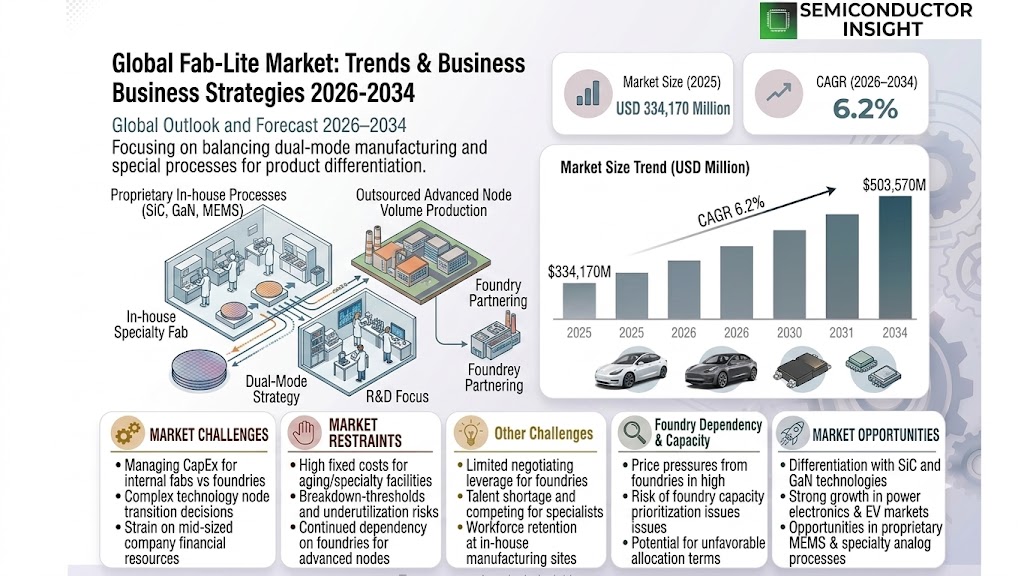

Global Fab-Lite market size was valued at USD 334,170 million in 2025. The market is projected to grow from USD 354,420 million in 2026 to USD 503,570 million by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Fab-Lite semiconductor fabrication model represents a hybrid approach that sits between the fully fabless and fully integrated device manufacturer (IDM) models. Three primary semiconductor business models have defined the industry for several decades , Fabless, IDM, and Pure-Play Foundries , and Fab-Lite model has emerged as a pragmatic, low-cost solution for semiconductor-dependent companies seeking to maintain partial manufacturing control without the full burden of operating a dedicated foundry. This model encompasses two key transitions: the fabless-to-Fab-Lite model and the IDM-to-Fab-Lite model.

The market is gaining considerable momentum as major IDMs increasingly rely on external foundries for a significant share of their production requirements. Over 80 percent of IDMs reported using external production for some portion of their front-end fabrication. Intel, for instance, sources up to 20 percent of its production through TSMC, while Analog Devices externally sources 50 percent of its wafer requirements. STMicroelectronics subcontracted approximately 20% of its total silicon production to external foundries in 2023, and in the same year, approximately 63% of Microchip Technology’s sales came from products manufactured at outside wafer foundries. Key players operating across Fab-Lite landscape include Maxscend Microelectronics Company Limited, GalaxyCore, Hot Chip Technology, Texas Instruments, Renesas, STMicroelectronics, Infineon, NXP, Onsemi, and Analog Devices, Inc., among others.

MARKET DRIVERS

Rising Demand for Cost-Efficient Semiconductor Manufacturing Models

Fab-Lite market is gaining significant traction as semiconductor companies seek a balanced approach between the capital-intensive fabless model and the asset-heavy integrated device manufacturer (IDM) structure. Under Fab-Lite model, companies retain partial in-house fabrication capabilities while outsourcing high-volume or advanced-node production to foundries. This hybrid strategy allows firms to exercise greater control over proprietary process technologies without bearing the full financial burden of maintaining a complete wafer fabrication infrastructure. As global chip demand continues to grow across automotive, industrial, and communications sectors, Fab-Lite approach is increasingly being recognized as a strategically viable path for mid-sized semiconductor companies.

Strategic Flexibility Amid Geopolitical Supply Chain Pressures

Geopolitical tensions and supply chain disruptions experienced in recent years have underscored the vulnerabilities associated with complete dependence on third-party foundries. Fab-Lite market has benefited from this shift in strategic thinking, as companies look to de-risk their manufacturing exposure while maintaining operational agility. By retaining selective in-house fabrication for critical or differentiated technologies, Fab-Lite companies can respond more effectively to supply disruptions, lead time volatility, and export control regulations. Governments in key regions, including North America, Europe, and parts of Asia, have introduced policies and incentives encouraging domestic semiconductor manufacturing capacity, further supporting Fab-Lite model as a practical and fundable middle ground.

➤ Government-backed semiconductor initiatives and regional chip sovereignty programs are creating a favorable policy environment that directly accelerates investment in Fab-Lite manufacturing infrastructure worldwide.

Furthermore, the growing complexity of heterogeneous integration and chiplet-based architectures is driving semiconductor companies to maintain tighter process control over specific technology nodes. Fab-Lite players are well-positioned to leverage mature or specialty nodes in-house , such as analog, MEMS, or power devices , while outsourcing leading-edge digital logic to advanced foundries. This division of manufacturing responsibility aligns well with evolving product roadmaps across the automotive electronics, industrial automation, and defense electronics segments, reinforcing the long-term growth momentum of Fab-Lite market.

MARKET CHALLENGES

Balancing Capital Expenditure With Operational Efficiency in Dual-Mode Manufacturing

One of the most significant challenges facing Fab-Lite market is the inherent complexity of managing both in-house fabrication assets and external foundry relationships simultaneously. Unlike pure fabless companies that can concentrate resources entirely on design and product development, Fab-Lite firms must allocate capital toward maintaining aging or specialty fabs, hiring specialized process engineers, and ensuring equipment is updated in line with evolving technology standards. This dual operational model can strain financial resources, particularly for mid-sized companies with limited balance sheets, making it difficult to sustain both manufacturing investment and competitive R&D spending at the same time.

Other Challenges

Technology Node Transition Complexity

As leading-edge process nodes continue to advance rapidly, Fab-Lite companies face the challenge of deciding which technology generations to retain in-house versus outsource. The cost of upgrading internal fab infrastructure to keep pace with sub-10nm processes is prohibitive for most Fab-Lite participants, creating a risk of technology gaps that could affect product competitiveness in high-performance computing or advanced mobile applications. Managing the inflection points between in-house and outsourced node strategies requires careful long-term planning and constant market intelligence.

Talent Retention and Specialized Workforce Constraints

Maintaining a skilled semiconductor process engineering workforce is a persistent challenge within Fab-Lite market. As Global semiconductor industry faces a well-documented talent shortage, Fab-Lite companies must compete with both large IDMs and leading foundries for experienced process engineers, equipment specialists, and yield improvement experts. The inability to offer the scale and career development pathways of larger organizations can make talent acquisition and retention difficult, directly impacting operational efficiency and innovation capacity within in-house fabrication facilities.

MARKET RESTRAINTS

High Fixed Costs Associated With Maintaining In-House Fabrication Facilities

A primary restraint on the growth of Fab-Lite market is the substantial fixed cost burden associated with owning and operating semiconductor fabrication facilities, even on a partial basis. Wafer fab infrastructure requires continuous investment in cleanroom maintenance, equipment depreciation, utility costs, and process qualification activities. For companies operating on thinner margins or navigating cyclical demand downturns, these fixed costs can become disproportionately burdensome compared to a purely fabless structure. The break-even thresholds for in-house fab utilization are high, and periods of reduced demand can lead to underutilization, further eroding the economic rationale for Fab-Lite approach in certain business environments.

Foundry Dependency and Capacity Allocation Limitations

Despite retaining some internal manufacturing capability, Fab-Lite companies remain partially dependent on external foundries for volume production or advanced-node requirements. This residual dependency exposes them to many of the same risks affecting fully fabless firms, including foundry capacity constraints, pricing pressures during periods of high industry demand, and prioritization challenges when foundries allocate capacity to larger customers. The limited negotiating leverage that smaller Fab-Lite companies hold relative to high-volume fabless clients can result in unfavorable lead times and allocation terms, partially undermining the strategic control advantages that Fab-Lite model is intended to provide. These dynamics collectively act as a structural restraint on the market’s scalability and profitability potential.

MARKET OPPORTUNITIES

Specialty Process Technologies as a Differentiated Competitive Advantage

Fab-Lite market presents a compelling opportunity for companies that focus their in-house fabrication capabilities on specialty and differentiated process technologies where foundry availability is limited or where proprietary know-how provides a meaningful competitive moat. Technologies such as silicon carbide (SiC), gallium nitride (GaN), MEMS, high-voltage CMOS, and specialized analog processes are areas where maintaining internal fabrication expertise can translate directly into product differentiation and margin protection. The accelerating adoption of wide-bandgap semiconductors in electric vehicles and power electronics, in particular, is creating a favorable environment for Fab-Lite companies with in-house SiC or GaN process capabilities to capture premium market positioning.

Expansion Into Defense, Aerospace, and Regulated Electronics Markets

Defense, aerospace, and other regulated industries often require stringent supply chain traceability, controlled manufacturing environments, and trusted fabrication sources , requirements that are difficult to fulfill through standard commercial foundry channels. Fab-Lite market is uniquely positioned to address these sectors by offering the security and process auditability of in-house fabrication while maintaining the design flexibility associated with a leaner manufacturing structure. As global defense budgets continue to prioritize domestic semiconductor sourcing and governments tighten regulations around trusted supplier programs, Fab-Lite companies with domestically located fabrication assets stand to benefit significantly from increased contract opportunities in these high-value, long-lifecycle end markets.

Strategic Mergers, Acquisitions, and Partnership Ecosystems

The evolving semiconductor landscape is creating fertile ground for consolidation and strategic collaboration that can strengthen Fab-Lite market’s overall value proposition. Larger semiconductor companies seeking to acquire specialty process capabilities without full IDM investment, as well as private equity interest in undervalued fab assets, are contributing to an active mergers and acquisitions environment that benefits established Fab-Lite participants. Additionally, collaborative models between Fab-Lite companies and equipment suppliers, materials providers, and regional governments are emerging as powerful mechanisms to share capital burdens and accelerate technology development. These ecosystem-level partnerships are expected to enhance the long-term viability and competitiveness of Fab-Lite model in an increasingly complex global semiconductor supply chain.

Fab-Lite Market () Trends

Shift from Traditional Semiconductor Models Driving Fab-Lite Adoption

Fab-Lite market is experiencing a significant structural transformation as semiconductor companies seek to balance the flexibility of the fabless model with the strategic control of Integrated Device Manufacturers (IDMs). Fab-Lite approach has emerged as a compelling middle ground, enabling companies to retain ownership of select fabrication processes while outsourcing a portion of wafer production to external foundries. This hybrid strategy is gaining traction across Global semiconductor industry, with over 80 percent of IDMs now reported to use external production for some portion of their front-end fabrication. Companies such as Texas Instruments, STMicroelectronics, Renesas, Infineon, NXP, Microchip Technology, Onsemi, and Analog Devices have actively embraced the IDM-to-Fab-Lite transition, externally sourcing meaningful shares of their wafer requirements to optimize cost structures and enhance supply chain resilience.

Other Trends

Growing External Sourcing Among Leading IDMs

A defining trend within Fab-Lite market is the measurable increase in external wafer sourcing by established IDMs. Texas Instruments reported externally sourcing approximately 20 percent of its production in both 2022 and 2023, while Analog Devices sourced around 50 percent of its wafer requirements from outside foundries during the same period. STMicroelectronics subcontracted roughly 20 percent of the value of its total silicon production to external foundries in 2023, and approximately 63 percent of Microchip Technology’s sales in 2023 came from products manufactured at outside wafer foundries. Even Intel, a historically vertically integrated manufacturer, is recognized as one of TSMC’s top customers, with up to 20 percent of its production utilizing external foundry capacity. These figures underscore a clear and accelerating industry shift toward Fab-Lite model.

Fabless-to-Fab-Lite Model Gaining Momentum

Alongside the IDM-to-Fab-Lite transition, the fabless-to-Fab-Lite segment is also witnessing notable momentum. Companies such as Maxscend Microelectronics Company Limited, GalaxyCore, and Hot Chip Technology are among the key players navigating this evolution, seeking to acquire selective in-house fabrication capabilities to improve product differentiation and reduce dependency on third-party foundries. This transition reflects a broader industry recognition that some degree of manufacturing control can be a strategic competitive advantage, particularly for specialized analog, sensor, and mixed-signal semiconductor applications.

Regional Dynamics and Competitive Landscape Shaping Fab-Lite Market

From a regional perspective, North America and Asia remain the dominant geographies influencing Fab-Lite market dynamics, with China increasingly asserting its presence through domestic semiconductor investment and policy-driven manufacturing expansion. The competitive landscape encompasses a diverse set of global players, including Navitas, Sony Semiconductor Solutions Corporation, Toshiba, and Suzhou Yuanxin Microelectronics Technology, alongside the major IDMs already pursuing Fab-Lite strategies. Application segments driving demand include Analog IC, Micro IC, Logic IC, Discrete IC, Sensors IC, Memory IC, and Optoelectronics, reflecting the broad cross-industry relevance of Fab-Lite model across automotive, industrial, consumer electronics, and communications end markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Fab-Lite Semiconductor Market: Navigating the Intersection of Fabless Agility and IDM Control

Global Fab-Lite market, valued at approximately USD 334,170 million in 2025 and projected to reach USD 503,570 million by 2034 at a CAGR of 6.2%, is characterized by a dynamic and increasingly competitive landscape. Fab-Lite model has emerged as a strategically compelling hybrid approach, enabling semiconductor companies to retain selective in-house fabrication capabilities while leveraging the cost efficiencies and advanced process nodes offered by pure-play foundries such as TSMC and GlobalFoundries. Leading Integrated Device Manufacturers (IDMs) including Texas Instruments, STMicroelectronics, Infineon, NXP Semiconductors, Renesas Electronics, Analog Devices, Microchip Technology, and Onsemi have progressively transitioned toward this model, externally sourcing anywhere from 20% to over 60% of their wafer requirements. This strategic flexibility allows these incumbents to optimize capital expenditure, access cutting-edge process technologies, and respond more rapidly to fluctuating end-market demand across automotive, industrial, and consumer electronics segments.

Beyond the established IDM-to-Fab-Lite transitions, a growing cohort of companies migrating from the fabless model is reshaping competitive dynamics. Players such as Maxscend Microelectronics, GalaxyCore, Hot Chip Technology, Suzhou Yuanxin Microelectronics Technology, and Navitas Semiconductor are strategically investing in selective front-end fabrication assets to gain greater process differentiation, tighter supply chain control, and improved margins on high-value product lines. Sony Semiconductor Solutions Corporation further strengthens the competitive field with its specialized sensor fabrication expertise under a Fab-Lite structure. The competitive intensity is amplified by geopolitical factors, semiconductor supply chain realignment, and government-backed incentives across the United States, Europe, and Asia that are accelerating domestic fabrication investments. Companies that can effectively balance internal fab utilization with external foundry partnerships are best positioned to capture share in this evolving, high-growth market.

List of Key Fab-Lite Companies Profiled

- Maxscend Microelectronics Company Limited

- GalaxyCore

- Hot Chip Technology

- Suzhou Yuanxin Microelectronics Technology

- Renesas Electronics

- Navitas Semiconductor

- Texas Instruments (TI)

- STMicroelectronics

- Sony Semiconductor Solutions Corporation (SSS)

- Infineon Technologies

- NXP Semiconductors

- Microchip Technology

- Onsemi

- Toshiba Electronic Devices & Storage Corporation

- Analog Devices, Inc. (ADI)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

IDM to Fab-Lite represents the dominant transition model, driven by the strategic need of established Integrated Device Manufacturers to balance internal fabrication capabilities with external foundry partnerships.

|

| By Application |

|

Analog IC stands out as the leading application segment within Fab-Lite market, owing to the maturity and process-specificity of analog semiconductor manufacturing.

|

| By End User |

|

Automotive is the leading end-user segment for Fab-Lite semiconductor solutions, fueled by the accelerating electrification of vehicles and the increasing integration of advanced driver-assistance systems (ADAS).

|

| By Manufacturing Strategy |

|

Internal Fab with External Outsourcing is the predominant manufacturing strategy among established players in Fab-Lite market, reflecting the industry’s preference for maintaining proprietary process control while leveraging external capacity for volume scaling.

|

| By Technology Node |

|

Mature Node (28nm and above) dominates Fab-Lite market by technology node, as the majority of analog, power, and mixed-signal semiconductors are manufactured using established process geometries that do not require cutting-edge lithography infrastructure.

|

Regional Analysis: Fab-Lite Market

Asia-Pacific

Asia-Pacific’s Fab-Lite market thrives on a culture of continuous innovation, with semiconductor design houses in Taiwan and South Korea pioneering system-on-chip architectures and advanced node designs. The region’s emphasis on intellectual property development over pure manufacturing volume makes Fab-Lite model a natural strategic fit, enabling faster product iteration cycles and stronger competitive differentiation in global markets.

The region hosts the world’s most advanced and diverse foundry ecosystem, giving Fab-Lite companies unparalleled access to cutting-edge manufacturing nodes and specialized process technologies. Strategic proximity to leading foundries reduces logistical complexity, shortens time-to-market, and enables tighter collaboration between design and production teams, reinforcing Asia-Pacific’s structural advantage in Fab-Lite market.

National semiconductor strategies across China, Japan, South Korea, and India are catalyzing growth in Fab-Lite market by funding research institutions, subsidizing design centers, and incentivizing technology partnerships. These policy frameworks reduce financial barriers for emerging Fab-Lite enterprises while encouraging multinational collaborations that elevate the region’s overall technological competitiveness and long-term market positioning.

Surging demand for AI accelerators, 5G chipsets, electric vehicle semiconductors, and IoT devices is propelling Fab-Lite market adoption throughout Asia-Pacific. Regional electronics manufacturers and system integrators are increasingly partnering with Fab-Lite design firms to source customized, application-specific solutions that balance performance, power efficiency, and cost , cementing the region’s role as both a supply and demand powerhouse.

North America

North America represents a significant and strategically vital region within Global Fab-Lite market, anchored by the United States’ strong tradition of semiconductor design excellence and innovation. Leading technology companies headquartered in Silicon Valley and across major technology corridors have long embraced Fab-Lite philosophy, leveraging world-class design capabilities while outsourcing volume manufacturing to trusted foundry partners. The renewed focus on domestic semiconductor resilience, reinforced through targeted legislative initiatives, is encouraging a recalibration of how Fab-Lite companies balance design autonomy with manufacturing security. Demand from defense electronics, data center infrastructure, and advanced automotive systems is creating sustained growth opportunities. Canada and Mexico are also contributing to regional supply chain diversification efforts, supporting broader Fab-Lite market expansion across the continent through the forecast period ending 2034.

Europe

Europe occupies a distinctive position in Fab-Lite market, characterized by its concentration of highly specialized semiconductor design firms serving automotive, industrial automation, and healthcare electronics sectors. Germany, the Netherlands, France, and Sweden are home to established Fab-Lite enterprises that have cultivated deep domain expertise and long-standing foundry relationships with global manufacturing partners. The European Chips Act and associated funding mechanisms are strengthening regional design capabilities and encouraging strategic investment in semiconductor intellectual property development. Europe’s Fab-Lite market is further supported by a strong regulatory environment that emphasizes supply chain transparency, data security, and environmental sustainability , factors that increasingly influence procurement decisions. As smart mobility and Industry 4.0 applications expand, European Fab-Lite companies are well-positioned to serve sophisticated, high-reliability end markets.

South America

South America remains an emerging participant in Global Fab-Lite market, with Brazil leading regional development efforts through its expanding technology sector and growing pool of engineering graduates. While the region does not yet host a mature semiconductor design ecosystem, increasing foreign direct investment, improving telecommunications infrastructure, and rising domestic demand for consumer electronics and industrial automation solutions are creating favorable conditions for Fab-Lite market growth. Government programs in Brazil and Chile aimed at fostering technology entrepreneurship and digital transformation are beginning to attract the attention of global Fab-Lite firms seeking new design partnerships and talent pools. Over the 2026–2034 forecast horizon, South America is expected to transition gradually from a peripheral to a more active participant in Fab-Lite market value chain.

Middle East & Africa

The Middle East and Africa region represents a nascent but increasingly promising frontier for Fab-Lite market, driven by ambitious national diversification strategies and accelerating digital infrastructure investment. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are actively cultivating technology ecosystems that include semiconductor design capabilities as part of broader economic transformation agendas. Israel, long recognized as a global hub for chip design innovation, continues to anchor the region’s Fab-Lite credentials, with a vibrant community of fabless and Fab-Lite design firms operating across communications, cybersecurity, and advanced computing domains. Africa’s expanding mobile connectivity landscape and growing appetite for localized technology solutions present long-term demand opportunities. While manufacturing infrastructure remains limited across much of the region, Fab-Lite model’s design-centric nature makes it particularly well-suited for regional market entry strategies through the forecast period.

Report Scope

This market research report provides a comprehensive analysis of Fab-Lite Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Fab-Lite Market?

-> Global Fab-Lite Market was valued at USD 334,170 million in 2025 and is expected to reach USD 503,570 million by 2034, growing at a CAGR of 6.2% during the forecast period.

Which key companies operate in Fab-Lite Market?

-> Key players include Maxscend Microelectronics Company Limited, GalaxyCore, Hot Chip Technology, Suzhou Yuanxin Microelectronics Technology, Renesas, Navitas, Texas Instruments (TI), STMicroelectronics, Sony Semiconductor Solutions Corporation (SSS), Infineon, NXP, Microchip Technology, Onsemi, Toshiba, and Analog Devices, Inc. (ADI), among others.

What are the key growth drivers of Fab-Lite Market?

-> Key growth drivers include rising adoption of Fab-Lite model as a low-cost semiconductor manufacturing solution, increasing external foundry sourcing by IDMs (over 80% of IDMs use external front-end fabrication), growing demand for semiconductors across automotive, consumer electronics, and industrial sectors, and the strategic shift of companies from fully fabless or fully integrated models toward the flexible Fab-Lite approach.

Which region dominates Fab-Lite Market?

-> Asia is a dominant and fastest-growing region in Fab-Lite Market, with China and Japan being key contributors, while North America remains a significant market driven by major players such as Texas Instruments, Analog Devices, and Microchip Technology.

What are the emerging trends in Fab-Lite Market?

-> Emerging trends include the transition of IDMs toward Fab-Lite model (e.g., Analog Devices externally sourcing 50% of wafer requirements, Microchip Technology sourcing 63% of sales from outside foundries), increased collaboration between IDMs and pure-play foundries, growing investments in advanced semiconductor nodes, and the strategic diversification of supply chains to reduce dependency on single fabrication sources.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...