MARKET INSIGHTS

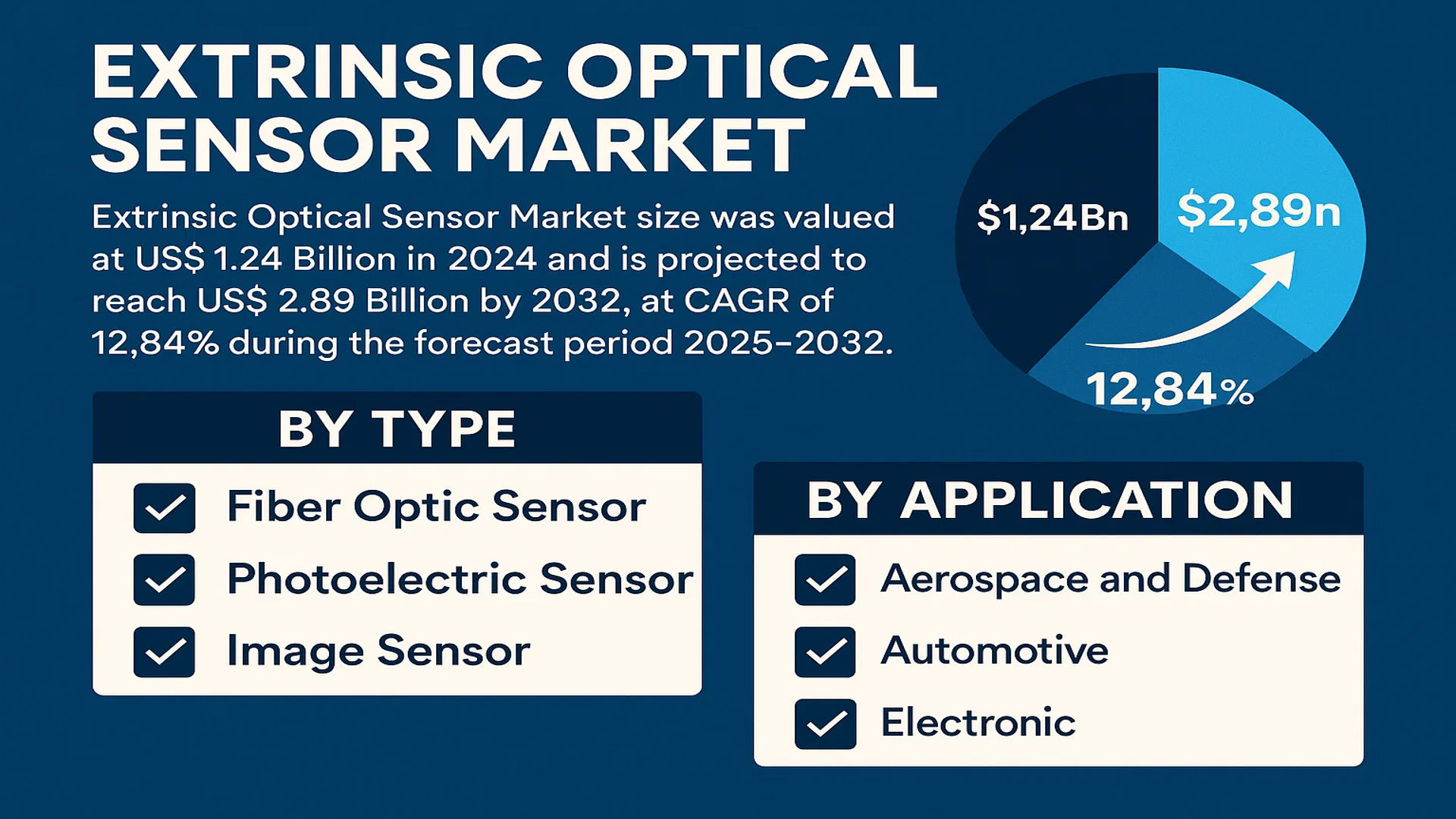

The global Extrinsic Optical Sensor Market size was valued at US$ 1.24 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 12.84% during the forecast period 2025–2032. While North America currently dominates the market with a 38% revenue share, Asia-Pacific is expected to witness the fastest growth at 7.2% CAGR through 2032.

Extrinsic optical sensors are specialized devices that detect and measure physical quantities by analyzing changes in light properties as it interacts with external environments. These sensors operate by transmitting light through optical fibers or other media to measure parameters such as temperature, pressure, strain, and chemical composition. Major product segments include fiber optic sensors, photoelectric sensors, and image sensors, with fiber optics accounting for 45% of market revenue in 2024 due to their widespread use in industrial applications.

The market growth is driven by increasing automation across industries, stringent safety regulations, and the need for precise measurement in harsh environments. Recent developments include Honeywell’s 2023 launch of next-generation industrial photoelectric sensors with enhanced range and accuracy, while AMS-OSRAM expanded its optical sensor portfolio through the 2022 acquisition of Princeton Optronics. Key challenges include high implementation costs and the need for specialized expertise in sensor calibration and maintenance.

MARKET DYNAMICS

MARKET DRIVERS

Industrial Automation and IoT Integration to Accelerate Market Expansion

The global extrinsic optical sensor market is witnessing substantial growth driven by increasing industrial automation across manufacturing sectors. These sensors play a critical role in smart factories by enabling precise measurement and monitoring in harsh environments where traditional sensors fail. The shift towards Industry 4.0 has significantly boosted demand, with optical sensors proving essential for predictive maintenance and quality control systems. Furthermore, integration with Internet of Things (IoT) platforms has expanded their applications, allowing real-time data collection and analysis for optimized operational efficiency. Factories utilizing these sensor solutions report reduced downtime by up to 20-30%, creating strong demand across automotive and electronics manufacturing sectors.

Advancements in Fiber Optic Technology to Propel Market Growth

Technological innovations in fiber optic-based extrinsic sensors are creating new opportunities across multiple industries. Recent developments in distributed sensing systems now allow single fiber cables to perform thousands of simultaneous measurements over kilometer-long distances. This breakthrough is particularly valuable for structural health monitoring in civil infrastructure and oil & gas pipelines. The defense sector has also increased adoption, with fiber optic sensors proving resistant to electromagnetic interference in radar and sonar systems. Market data indicates fiber optic sensor revenues grew by nearly 15% last year, outperforming other sensor types.

Growing Aerospace and Defense Applications to Stimulate Demand

Extrinsic optical sensors have become indispensable in aerospace applications due to their lightweight nature and immunity to electromagnetic interference. Modern aircraft incorporate hundreds of these sensors for structural monitoring, engine performance tracking, and flight control systems. The aviation industry’s increasing focus on fuel efficiency and predictive maintenance aligns perfectly with optical sensing capabilities. With global defense spending projected to exceed $2 trillion this year, substantial investments in next-generation aircraft and surveillance systems will continue driving market expansion throughout the forecast period.

MARKET RESTRAINTS

High Implementation Costs to Limit Market Penetration

While extrinsic optical sensors offer superior performance, their relatively high cost compared to conventional sensors restricts adoption in price-sensitive markets. The specialized materials and precision manufacturing required for optical components result in substantially higher unit prices. For small-to-medium enterprises, the total cost of ownership – including installation, calibration, and maintenance – often proves prohibitive. Industry analysis suggests optical sensor solutions typically command 30-50% price premiums over traditional alternatives, slowing uptake in developing economies and smaller industrial operations.

Complex Installation and Maintenance Requirements to Hinder Growth

The technical complexity associated with extrinsic optical sensor deployment presents another significant challenge. Unlike conventional sensors that offer plug-and-play functionality, optical systems frequently require specialized knowledge for proper installation and alignment. Many industrial facilities lack personnel trained in fiber optic handling and splicing techniques, necessitating expensive third-party service contracts. Additionally, environmental factors like temperature fluctuations and physical stress can degrade performance over time, creating ongoing maintenance burdens that some organizations find impractical.

Regulatory and Standardization Issues to Create Market Uncertainty

The absence of universal standards for optical sensor technologies generates uncertainty for both manufacturers and end-users. Various industries employ different communication protocols and performance metrics, forcing vendors to develop multiple product variants. This fragmentation increases development costs while complicating system integration efforts. In sectors like medical devices and aerospace, lengthy certification processes for new sensor technologies can delay product launches by 12-18 months, discouraging innovation and investment in research and development.

MARKET OPPORTUNITIES

Emerging Smart City Infrastructure to Open New Application Areas

Global smart city initiatives present substantial growth opportunities for extrinsic optical sensor providers. City planners increasingly deploy these sensors for critical infrastructure monitoring, including bridges, tunnels, and utility networks. Fiber optic-based strain and temperature sensors prove particularly valuable for early detection of structural weaknesses in aging urban infrastructure. With investments in smart city technologies projected to surpass $200 billion annually, this sector represents one of the most promising avenues for market expansion.

Medical and Healthcare Applications to Drive Future Innovation

The healthcare sector shows growing interest in extrinsic optical sensors for minimally invasive diagnostics and patient monitoring. Recent advancements in biocompatible sensor materials enable new applications in endoscopy, drug delivery monitoring, and implantable devices. Optical sensors offer distinct advantages in medical environments, being inherently safe for use near MRI machines and other sensitive equipment. As telemedicine and home healthcare solutions gain traction, demand for compact, high-precision optical sensing technologies should experience significant growth in coming years.

Autonomous Vehicle Development to Create Long-Term Growth Potential

Automotive manufacturers investing in autonomous driving technologies represent another key opportunity for sensor providers. Optical sensors serve critical functions in lidar systems and vehicle-to-everything (V2X) communication networks. Their immunity to radio frequency interference makes them particularly suitable for crowded urban environments with multiple signal sources. While still in early adoption phases, the autonomous vehicle sector’s projected 35% CAGR over the next decade suggests substantial long-term potential for optical sensor applications in transportation.

MARKET CHALLENGES

Competition from Alternative Sensing Technologies to Intensify

The extrinsic optical sensor market faces mounting competition from emerging sensing technologies. Advancements in wireless sensor networks, MEMS-based devices, and new generation capacitive sensors threaten to erode optical solutions’ value proposition. Some of these alternatives offer comparable performance at lower price points or with easier installation procedures. Market data indicates alternative technologies currently address nearly 40% of applications where optical sensors were traditionally dominant, forcing vendors to accelerate innovation and cost reduction efforts.

Global Supply Chain Vulnerabilities to Impact Market Stability

Specialized material requirements for optical sensors create supply chain vulnerabilities that challenge market stability. Rare earth elements and high-purity glass used in sensor fabrication come from limited geographic sources, exposing manufacturers to price volatility and availability risks. Recent disruptions have caused lead times for key optical components to extend beyond 6 months in some cases, forcing companies to maintain larger inventories and potentially reducing profit margins.

Data Security Concerns to Emerge as Critical Consideration

As extrinsic optical sensors become increasingly connected, cybersecurity risks present new challenges for the industry. Sensor networks in critical infrastructure and defense applications represent attractive targets for cyberattacks, creating demand for robust encryption and authentication protocols. Implementing these security measures without compromising sensor performance or response times adds engineering complexity and cost. Facilities handling sensitive data may hesitate to adopt connected sensor solutions until these security concerns are adequately addressed.

EXTRINSIC OPTICAL SENSOR MARKET TRENDS

Automotive and Industrial Automation Drive Demand for Optical Sensing Solutions

The global extrinsic optical sensor market is experiencing significant growth, driven by rising adoption in automotive safety systems and industrial automation. Advanced driver-assistance systems (ADAS) increasingly rely on fiber optic sensors for precise distance measurement and collision avoidance, with sales in this segment projected to grow by nearly 18% annually through 2032. Industrial automation’s shift toward Industry 4.0 standards has created demand for photoelectric sensors capable of operating in harsh environments where traditional electronic sensors fail. Market data shows that extrinsic optical sensors now account for over 35% of all industrial sensing applications where electromagnetic interference or extreme temperatures are concerns.

Other Trends

Miniaturization and Higher Spectral Resolution

Recent technological developments have focused on miniaturizing optical sensor components while improving spectral resolution capabilities. Latest-generation extrinsic sensors now achieve wavelength measurement accuracy below 0.01nm, enabling new applications in precision manufacturing and laboratory equipment. This trend has been particularly impactful in the electronics manufacturing sector, where components have shrunk below 10nm scales. The medical diagnostics field has also benefited, with novel fiber-optic-based sensors being integrated into minimally invasive surgical tools and patient monitoring systems.

Growing Defense and Aerospace Applications

The defense sector is emerging as a major growth area, with extrinsic optical sensors being deployed in aircraft structural health monitoring, missile guidance systems, and submarine communications. Governments worldwide are allocating larger budgets for these technologies, with defense-related optical sensor procurement increasing by an estimated 22% since 2022. These sensors offer distinct advantages in military applications because they are immune to electromagnetic pulses and difficult to detect. Aerospace manufacturers are also adopting distributed fiber-optic sensing systems that provide real-time monitoring across entire aircraft structures, representing a market segment expected to exceed $800 million by 2027.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Market Competition in the Extrinsic Optical Sensor Segment

The global extrinsic optical sensor market exhibits a competitive landscape with a mix of established technology conglomerates and specialized sensor manufacturers. AMS-OSRAM and Hamamatsu Photonics K.K. currently dominate the space, collectively holding over 25% market share in 2024. Their leadership stems from decades of photonics expertise and vertically integrated manufacturing capabilities.

Notably, Honeywell International has emerged as a key player in industrial applications, particularly for harsh environment sensing solutions. Meanwhile, Keyence Corporation and OMRON Corporation are gaining rapid traction through their compact, high-precision sensor offerings tailored for automation applications. The Asia-Pacific region has become a strategic battleground, with Panasonic Holdings Corporation expanding its production capacity by 30% in 2023 to meet regional demand.

The market sees continuous R&D investments, particularly in fiber optic sensing technologies which are projected to grow at 8.4% CAGR through 2030. Recent product launches demonstrate this innovation race – AMS-OSRAM introduced a new multi-parameter optical sensor platform in Q1 2024, while Texas Instruments unveiled a low-power optical sensing IC for IoT applications.

Mergers and acquisitions are reshaping the competitive dynamics. Analog Devices’ acquisition of Maxim Integrated in 2021 strengthened its position in industrial sensing, while STMicroelectronics has been actively partnering with automotive Tier 1 suppliers to develop next-generation LiDAR systems. These strategic moves are expected to significantly influence market shares in the coming years.

List of Key Extrinsic Optical Sensor Companies Profiled

- AMS-OSRAM (Austria)

- Analog Devices (U.S.)

- Broadcom (U.S.)

- Hamamatsu Photonics K.K. (Japan)

- Honeywell International (U.S.)

- ifm electronic gmbh (Germany)

- Keyence Corporation (Japan)

- OMRON Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- Rockwell Automation (U.S.)

- Rohm (Japan)

- STMicroelectronics (Switzerland)

- Texas Instruments Incorporated (U.S.)

- Vishay Intertechnology (U.S.)

Segment Analysis:

By Type

Fiber Optic Sensor Segment Dominates Due to High Demand in Critical Infrastructure Monitoring

The market is segmented based on type into:

- Fiber Optic Sensor

- Subtypes: Intensity-modulated, Phase-modulated, and Wavelength-modulated

- Photoelectric Sensor

- Image Sensor

- Others

By Application

Aerospace and Defense Leading Segment Due to High Reliability Requirements

The market is segmented based on application into:

- Aerospace and Defense

- Automotive

- Electronic

- Others

By End User

Industrial Sector Accounts for Significant Adoption Due to Process Automation Needs

The market is segmented based on end user into:

- Industrial

- Healthcare

- Telecommunications

- Energy

Regional Analysis: Extrinsic Optical Sensor Market

North America

The North American extrinsic optical sensor market is driven by advanced industrial automation, stringent safety regulations, and significant investments in defense and aerospace applications. The U.S. accounts for the highest market share, with a valuation estimated at several hundred million dollars in 2024, owing to strong demand in automotive manufacturing and medical device industries. Key players like Honeywell International and Texas Instruments Incorporated dominate, leveraging cutting-edge R&D to enhance fiber optic and photoelectric sensor technologies. While the U.S. remains the primary market, Canada and Mexico are gradually expanding due to increasing industrial automation initiatives.

Europe

Europe’s market thrives under strict regulatory frameworks, including EU directives on industrial safety and environmental monitoring, which mandate high-precision sensor deployments. Germany leads the region in manufacturing and automotive applications, while the UK and France focus on aerospace and defense. The adoption of image sensors is growing noticeably, particularly in automotive ADAS (Advanced Driver-Assistance Systems) and smart manufacturing. Despite economic uncertainties, technological advancements from companies like AMS-OSRAM and STMicroelectronics ensure sustained growth. However, high production costs remain a barrier for small-scale adopters.

Asia-Pacific

The Asia-Pacific region exhibits the fastest growth, driven by China, Japan, and South Korea’s leadership in electronics and automotive production. China alone is projected to reach a market value in the hundreds of millions by 2032, supported by government initiatives like “Made in China 2025” to boost smart manufacturing. Fiber optic sensors dominate due to their cost-effectiveness and high durability, especially in infrastructure monitoring and industrial automation. India’s market is emerging rapidly, spurred by increasing automotive and semiconductor investments. However, price sensitivity in Southeast Asian markets limits the adoption of high-end sensor technologies.

South America

South America’s market remains in the nascent stage, with Brazil leading in industrial and automotive sensor applications. While economic instability restricts large-scale deployments, government projects in oil & gas and mining sectors are creating opportunities for environmental and structural monitoring sensors. The lack of local manufacturing means most demand is met through imports, hindering affordability. Nevertheless, gradual infrastructure modernization efforts in Argentina and Chile suggest long-term potential for optical sensor integration.

Middle East & Africa

The MEA region is emerging, with UAE, Saudi Arabia, and Israel pioneering smart city projects and energy sector automation. Fiber optic sensors are increasingly used in oil pipelines and structural health monitoring, while defense investments in Israel drive demand for high-precision optical sensors. Limited local production results in heavy reliance on imports, slowing market expansion. However, ongoing urbanization and Industry 4.0 initiatives are expected to accelerate adoption over the coming decade.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Extrinsic Optical Sensor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Extrinsic Optical Sensor market was valued at US$ 1.24 billion in 2024 and is projected to reach US$ 2.89 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Fiber Optic Sensor, Photoelectric Sensor, Image Sensor, Others), application (Aerospace and Defense, Automotive, Electronics, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis for the U.S. (estimated at USD million in 2024) and China.

- Competitive Landscape: Profiles of leading market participants including AMS-OSRAM, Analog Devices, Broadcom, Hamamatsu Photonics K.K., Honeywell International, ifm electronic gmbh, Keyence Corporation, and OMRON Corporation, covering their market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging optical sensing technologies, integration with IoT systems, and advancements in fiber optic measurement techniques.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as industrial automation demand, along with challenges like high implementation costs and technical complexities.

- Stakeholder Analysis: Insights for sensor manufacturers, system integrators, component suppliers, and investors regarding the evolving market ecosystem and strategic opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy and reliability of insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Extrinsic Optical Sensor Market?

-> Extrinsic Optical Sensor Market size was valued at US$ 1.24 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 12.84% during the forecast period 2025–2032.

Which key companies operate in Global Extrinsic Optical Sensor Market?

-> Key players include AMS-OSRAM, Analog Devices, Broadcom, Hamamatsu Photonics K.K., Honeywell International, ifm electronic gmbh, Keyence Corporation, and OMRON Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for precise measurement systems, and advancements in optical sensing technologies.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America currently holds significant market share.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with AI for predictive maintenance, and development of harsh-environment capable optical sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...