Event-Based Vision Sensor Chip Market Insights

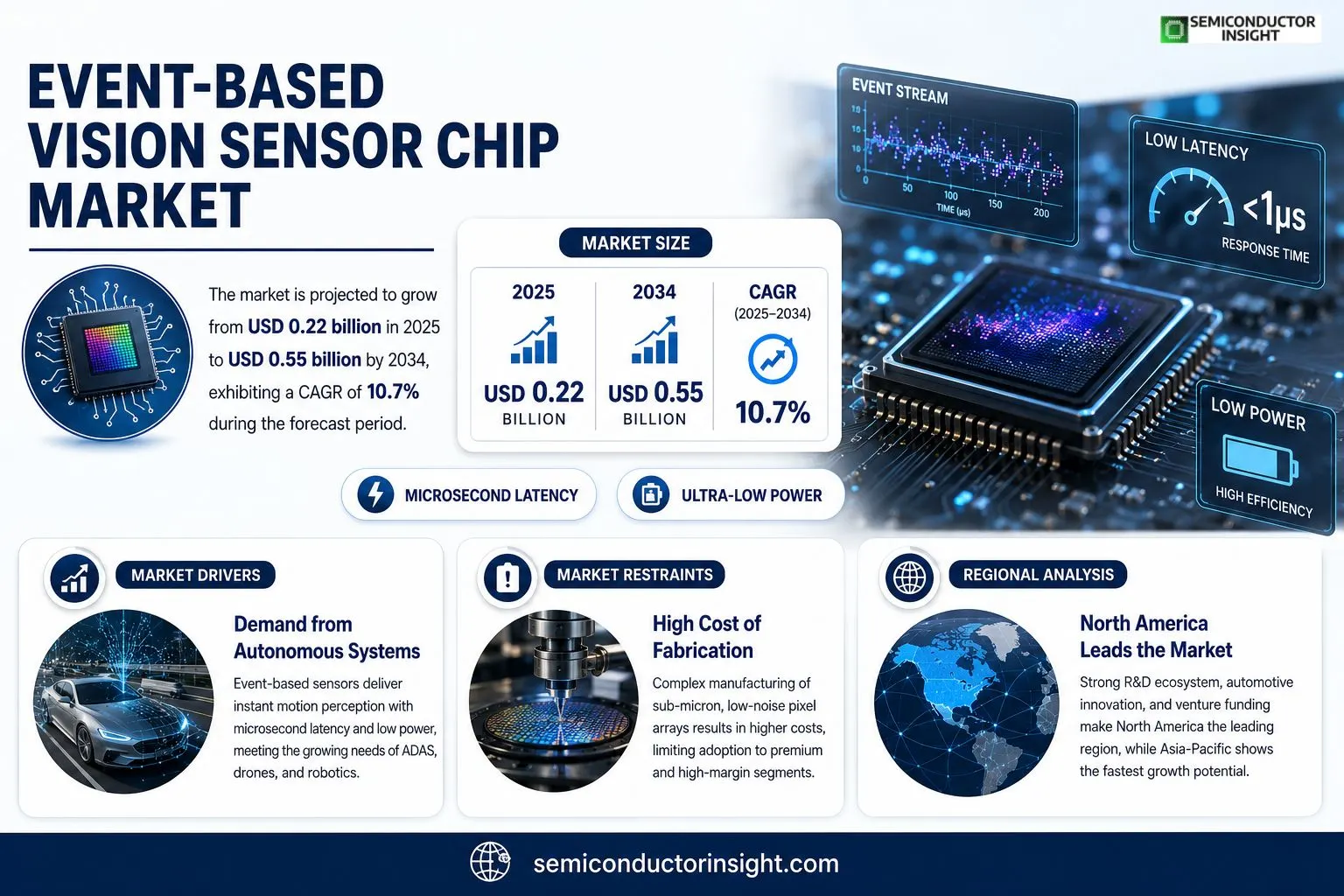

Event-Based Vision Sensor Chip market size was valued at USD 0.20 billion in 2025. The market is projected to grow from USD 0.22 billion in 2025 to USD 0.55 billion by 2034, exhibiting a CAGR of 10.7% during the forecast period.

Event‑Based Vision Sensor Chips are neuromorphic imaging devices that emit asynchronous events only when pixel‑level brightness changes occur, thereby emulating biological retinas. This architecture eliminates redundant frame data, delivering microsecond latency and dramatically lower power consumption compared with conventional frame‑based camerasattributes essential for edge AI applications such as autonomous navigation and industrial inspection.The market gains momentum because automotive manufacturers increasingly embed event‑cameras into advanced driver‑assistance systems seeking faster reaction times while preserving battery life.Robotics, augmented reality headsets and high‑speed drone guidance also benefit from the technology’s sparse data output.Recent collaborations, such as Sony’s March 2024 partnership with a leading automotive supplier to integrate event‑based modules into next‑generation ADAS platforms, illustrate growing commercial confidence.Investors are allocating capital toward startups pioneering stacked silicon processes that further shrink chip footprints and enhance pixel density, reinforcing the upward trajectory observed today.

MARKET DRIVERS

Advancements in Neuromorphic Imaging

The transition from frame‑based sensors to event‑driven architectures has unlocked latency levels below a microsecond, a capability that traditional CMOS cameras cannot match. Manufacturers are leveraging this advantage to target high‑speed robotics, where split‑second decisions translate directly into operational efficiency. As designers integrate on‑chip asynchronous processing, power budgets shrink, making the technology attractive for battery‑limited deployments.

Demand from Autonomous Systems

Automotive and drone platforms increasingly rely on continuous edge perception to navigate complex environments. Event-Based Vision Sensor Chip Market benefits from this shift because event sensors furnish sparse data streams that reduce bandwidth pressure on vehicle‑wide networks. Companies that couple these chips with AI inference engines are positioning themselves to capture a growing share of safety‑critical perception modules.

➤ “Event‑driven optics are redefining what real‑time vision can achieve in edge devices.”

Beyond mobility, industrial automation workshops are retrofitting existing lines with event sensors to monitor high‑velocity assembly processes. The ability to detect motion at the pixel level without motion blur offers a competitive edge in quality control, prompting equipment manufacturers to embed these chips into next‑generation vision modules.

MARKET CHALLENGES

Integration Complexity

Designing board‑level solutions around asynchronous pixel outputs demands expertise that many conventional OEMs lack. The need to synchronize event streams with deterministic control loops adds a layer of firmware development that stretches project timelines and budget allocations.

Other Challenges

Supply Chain Constraints

Limited foundry capacity for the specialized process nodes required by neuromorphic chips creates lead‑time volatility. End‑users often face allocation policies that prioritize larger volume customers, leaving niche innovators scrambling for inventory.

MARKET RESTRAINTS

High Cost of Fabrication

The manufacturing expense of sub‑micron, low‑noise pixel arrays remains a barrier for widespread adoption. While economies of scale could eventually lower unit costs, current price points restrict deployment to high‑margin segments such as aerospace and premium robotics, curbing broader market penetration.

MARKET OPPORTUNITIES

Emerging Applications in AR/VR

Augmented and virtual reality headsets demand ultra‑low latency eye‑tracking and gesture recognition to sustain immersion. Event‑based sensors, with their ability to transmit changes instantly, align perfectly with these requirements. Companies that package these chips with lightweight optics stand to gain early mover advantage as the AR/VR ecosystem matures.

Event-Based Vision Sensor Chip Market Trends

Neuromorphic Imaging Fuels Edge‑AI Adoption

Event-Based Vision Sensor Chip Market is being reshaped by devices that generate data only when pixel‑level brightness shifts occur. This selective output cuts frame redundancy, delivering microsecond‑scale latency while consuming a fraction of the power typical of conventional cameras. Such characteristics are compelling for edge‑AI workloads where bandwidth constraints and battery life are paramount. Manufacturers of autonomous systems are leveraging these chips to achieve faster reaction windows, especially in scenarios that demand split‑second decisions, such as high‑speed navigation and real‑time defect inspection.

Other Trends

Automotive Integration

Automotive OEMs are incorporating event‑based modules into advanced driver‑assistance architectures to tighten response loops without imposing additional electrical load on vehicle systems. A notable development is Sony’s March 2024 collaboration with a leading automotive supplier, which integrates event‑camera technology into next‑generation ADAS platforms. The partnership signals confidence that the low‑latency, low‑power profile aligns with the stringent safety and efficiency targets set by the industry.

Silicon Stacking Elevates Pixel Density

Investment flows are gravitating toward startups that perfect stacked silicon processes, a move that reduces overall chip footprint while boosting pixel counts. By layering sensor and processing tiers, designers can place more photodiodes within the same die area, enhancing spatial resolution without sacrificing the sparse data advantage. This technological refinement expands viable use cases, from augmented‑reality headsets that require high‑fidelity motion capture to lightweight drones that depend on rapid scene interpretation for obstacle avoidance.

COMPETITIVE LANDSCAPE

Key Industry Players

Event-Based Vision Sensor Chip Market: Competitive Overview

The leading segment of the market is anchored by a handful of firms that have converted neuromorphic research into commercially viable silicon. Prophesee, leveraging its Chronocam heritage, commands a sizable share through a portfolio that spans low‑power automotive modules to high‑resolution AR components. Sony Semiconductor Solutions complements this dominance with its global distribution network and a line of event‑camera IP that integrates directly into existing imaging pipelines. Samsung Electro‑Mechanics, benefiting from deep foundry relationships, has accelerated time‑to‑market for dense pixel arrays that promise microsecond response times. The concentration of these three manufacturers creates a tiered ecosystem: Prophesee drives early‑adopter innovation, Sony scales volume for consumer‑grade products, and Samsung supplies the high‑density chips required for complex edge‑AI deployments.Beyond the headline names, a cohort of specialist developers is expanding the competitive perimeter. iniVation focuses on high‑dynamic‑range sensors for industrial robotics, while ON Semiconductor supplies ruggedized event chips for automotive safety systems. STMicroelectronics has begun integrating event‑sensor cores into its broader automotive microcontroller portfolio, hinting at cross‑functional synergies. CEVA contributes optimized processing IP that reduces the computational load of event streams. Additional entrants such as Ambarella, AMS, and a handful of university spin‑outs are experimenting with hybrid architectures, indicating that the field remains fertile for niche innovation and potential consolidation.

List of Key Event-Based Vision Sensor Chip Companies Profiled

- Prophesee

- Sony Semiconductor Solutions

- Samsung Electro‑Mechanics

- iniVation

- ON Semiconductor

- STMicroelectronics

- CEVA

- Ambarella

- AMS

- Visionary Robotics Ltd.

- NeuroSilicon Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Dynamic Vision Sensors dominate the type landscape because they capture sparse, asynchronous events that mirror biological retinal behavior.

|

| By Application |

|

ADAS and Robotics emerge as the leading application domains because they demand rapid scene understanding while preserving battery life.

|

| By End User |

|

Automotive OEMs lead the end‑user segment because they are integrating event‑cameras into next‑generation safety suites.

|

| By Integration Level |

|

Embedded On‑Chip Processing is gaining traction as the preferred integration approach.

|

| By Market Drivers |

|

Latency‑Sensitive Edge AI drives adoption across automotive and robotics.

|

Regional Analysis: Event-Based Vision Sensor Chip Market

North America

Event-driven chips are finding footholds in autonomous mobility, where they enable rapid edge detection in complex lighting. Parallel advances in robotics benefit from the sensors’ asynchronous output, granting machines a more human‑like perception of motion.

The supply chain is anchored by a handful of specialized fabs capable of producing sub‑micron process nodes required for low‑latency chips. Partnerships between fabless designers and manufacturing partners mitigate capacity constraints.

Federal agencies have introduced streamlined testing pathways for AI‑enabled vision hardware, allowing quicker transition from prototype to field deployment, especially in defense and transportation.

Established semiconductor giants are acquiring niche start‑ups to embed event‑based architectures into broader product portfolios, while pure‑play innovators focus on specialized sensor‑software co‑design.

Europe

European manufacturers are leveraging strong university‑industry links to advance event‑based imaging for industrial automation. German engineering firms, in particular, value the chips’ ability to handle high‑contrast scenes without the overhead of frame‑based processing. The region’s emphasis on safety certification creates a rigorous validation environment, which, while extending time‑to‑market, builds confidence among automotive suppliers. Collaborative projects funded by EU research programs are fostering cross‑border development of standardized interfaces, positioning Europe as a hub for interoperable vision solutions.

Asia‑Pacific

In Asia‑Pacific, rapid adoption is visible in consumer electronics, where manufacturers seek ultra‑low‑power vision chips to extend battery life in wearable devices. Japanese firms are experimenting with event‑based sensors for augmented‑reality headsets, capitalizing on the technology’s high temporal resolution. Meanwhile, Chinese semiconductor players are scaling production capacity, driven by government incentives targeting next‑generation AI hardware. The diversity of applications across the region creates a competitive mosaic, prompting firms to tailor chip architectures for distinct market niches.

South America

South America’s engagement with Event-Based Vision Sensor Chip Market remains exploratory, with pilot projects in agricultural imaging leading the way. Brazilian research institutions are testing event‑driven sensors to monitor crop health, exploiting the chips’ capability to detect subtle motion in fluctuating light conditions. Although the region lacks large‑scale fabs, partnerships with overseas manufacturers enable local firms to integrate the technology into precision farming solutions, hinting at a gradual market build‑out.

Middle East & Africa

The Middle East & Africa are positioning event‑based vision chips within security and smart‑city initiatives. United Arab Emirates pilot programs are integrating the sensors into traffic‑monitoring networks, valuing the low‑latency data streams for real‑time incident response. In Africa, a few startups are exploring low‑cost event‑driven cameras for wildlife conservation, where power constraints and extreme environments demand the chips’ efficiency. Growing interest from government agencies suggests that demand could evolve from niche trials to broader deployments over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Event-Based Vision Sensor Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Event-Based Vision Sensor Chip Market?

-> Event-Based Vision Sensor Chip Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 1.02 billion by 2034, reflecting a CAGR of 9.5%.

Which key companies operate in Event-Based Vision Sensor Chip Market?

-> Key players include Prophesee, Sony Semiconductor Solutions, Samsung Electro‑Mechanics, among others.

What are the key growth drivers?

-> Key growth drivers include automotive manufacturers’ demand for instant motion perception, robotics applications requiring low latency, and advances in silicon‑photonic integration.

Which region dominates the market?

-> Asia-Pacific is a fast‑growing region, while Europe and North America hold significant shares.

What are the emerging trends?

-> Emerging trends include edge‑AI integration, neuromorphic processor convergence, and new chip families targeting AR/VR and autonomous navigation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...