EV Power Electronics Market Insights

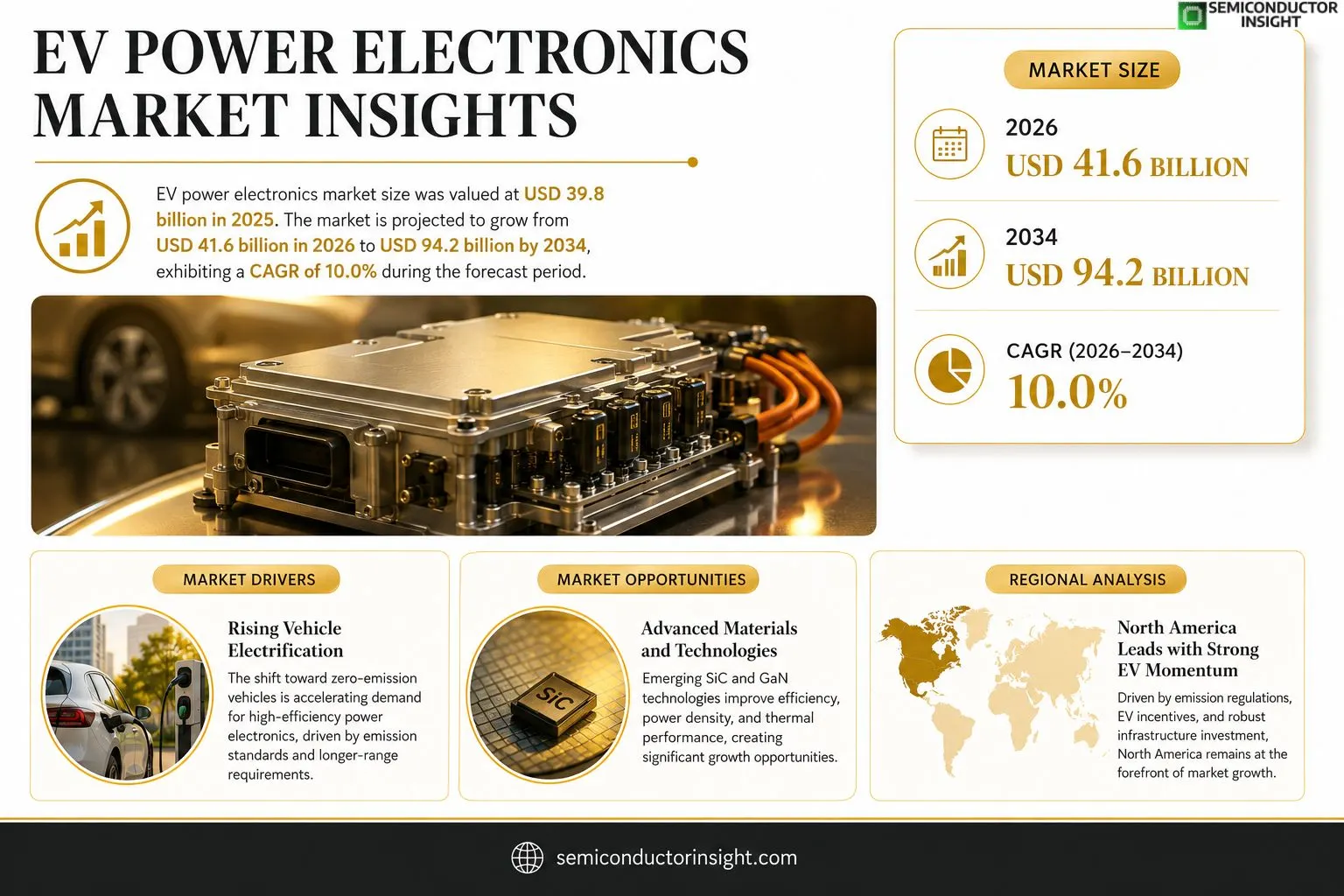

EV power electronics market size was valued at USD 39.8 billion in 2025. The market is projected to grow from USD 41.6 billion in 2026 to USD 94.2 billion by 2034, exhibiting a CAGR of 10.0% during the forecast period.

EV power electronics comprise high‑efficiency converters, inverters, onboard chargers and DC‑DC converters that manage electrical energy flow between batteries, motors and auxiliary systems in electric vehicles. These components enable precise torque control, regenerative braking and optimal battery utilization while meeting stringent automotive reliability standards.The market is experiencing rapid expansion because of accelerating electric‑vehicle adoption worldwide, supportive government incentives and tightening emissions regulations. Furthermore, advances in silicon‑carbide (SiC) and gallium‑nitride (GaN) semiconductor technologies are reducing weight and improving efficiency of power modules. Key players such as Bosch Sustainability Solutions, Continental AG, Infineon Technologies and Mitsubishi Electric are investing heavily in R&D and strategic partnerships,evident from Infineon’s March 2024 joint venture with a leading automaker to co‑develop next‑generation SiC modules,driving further market growth.

MARKET DRIVERS

Rising Vehicle Electrification

The shift toward zero‑emission vehicles is accelerating demand for high‑efficiency converters, inverters and thermal‑management modules. As manufacturers target longer range and faster charging, EV Power Electronics Market benefits from increased OEM investment in silicon‑carbide and gallium‑nitride technologies.

Policy Incentives and Infrastructure

Government subsidies, stricter emissions standards, and expanding fast‑charging networks create a favorable regulatory environment. These policies reduce total cost of ownership and stimulate higher unit sales of electric drivetrains, directly boosting component demand.

➤ “By 2028, power‑electronics revenue is projected to grow at a CAGR above 12% driven by automotive electrification.”

In addition, economies of scale are lowering component prices, allowing midsize and compact cars to adopt advanced power‑electronics solutions, further expanding the addressable market.

MARKET CHALLENGES

Thermal Management Complexity

Effective heat dissipation remains a technical hurdle, especially for high‑power inverters operating at elevated temperatures. Inadequate cooling can reduce reliability, prompting OEMs to demand more robust designs, which raises development costs.

Other Challenges

Supply‑Chain Vulnerabilities

Limited raw material availability for silicon‑carbide wafers and the concentration of semiconductor foundries in a few regions expose the industry to geopolitical and logistic disruptions.

MARKET RESTRAINTS

High Initial Capital Outlay

Manufacturers must invest heavily in new production lines and validation processes for next‑generation power modules. This upfront expense can deter smaller players and slow adoption rates in emerging markets.The lack of standardized testing frameworks also adds to development timelines, creating uncertainty for investors and slowing market expansion.

MARKET OPPORTUNITIES

Integration of Advanced Materials

Emerging materials such as graphene‑enhanced conductors and wide‑bandgap semiconductors present opportunities to improve efficiency and reduce weight. Early adopters can capture premium segments and differentiate their EV platforms.Furthermore, the rise of vehicle‑to‑grid (V2G) technologies opens new revenue streams for power‑electronics suppliers, as bidirectional converters become essential for grid stability and ancillary services.

EV Power Electronics Market Trends

Accelerating Adoption and Efficiency Gains

EV Power Electronics Market continues to expand as electric‑vehicle registrations rise sharply. High‑efficiency converters, inverters, onboard chargers and DC‑DC converters are now standard in most new EV models, enabling precise torque control, regenerative braking and optimal battery utilization. In 2025 the market value reached approximately USD 39.8 billion, and projections indicate a rise to USD 94.2 billion by 2034. This growth reflects tighter emissions standards, expanding charging infrastructure, and strong government incentives that push automakers to adopt advanced power electronics. As vehicle ranges increase, manufacturers rely on power modules that can deliver higher voltage conversion while minimizing losses, directly supporting the consumer demand for longer‑lasting EVs.

Other Trends

Silicon‑Carbide (SiC) and Gallium‑Nitride (GaN) Adoption

SiC and GaN semiconductor technologies are gaining market share due to their superior power density and thermal performance. By reducing module weight and improving conversion efficiency, these materials support longer vehicle range and lower cooling requirements. Major industry players such as Infineon Technologies and Mitsubishi Electric have announced joint development programs in 2024, accelerating the rollout of next‑generation SiC power modules across premium and mass‑market EV lines. Early adopters report efficiency improvements of up to 15 % compared with traditional silicon devices, translating into measurable fuel‑economy benefits for end users.

Strategic Partnerships and R&D Investment

Leading manufacturers are consolidating R&D efforts through strategic partnerships. Bosch Sustainability Solutions and Continental AG have formed joint ventures to co‑develop integrated power electronics architectures, targeting modular designs that simplify vehicle assembly and reduce part count. These collaborations lower time‑to‑market for new technologies and create economies of scale that decrease component costs. Investment in advanced packaging, such as wafer‑level packaging for SiC devices, further enhances reliability while meeting the stringent automotive qualification standards required for high‑volume production.

Regulatory Influence and Supply‑Chain Localization

Regulatory frameworks in Europe, China and the United States now mandate higher efficiency thresholds for EV powertrain components, prompting OEMs to prioritize low‑loss converters and high‑frequency inverters. Concurrently, geopolitical considerations are driving supply‑chain localization, with manufacturers establishing silicon‑carbide fabs in Europe and North America to mitigate reliance on a single region. This shift not only secures material availability but also aligns with national policies encouraging domestic clean‑technology production, reinforcing the overall market momentum.

COMPETITIVE LANDSCAPEKey Industry Players

EV Power Electronics Market – Competitive Overview

The EV power electronics sector is dominated by a handful of multinational technology groups that combine deep semiconductor expertise with automotive‑grade reliability. Bosch Sustainability Solutions leverages its extensive automotive systems portfolio to supply high‑efficiency inverters and DC‑DC converters for premium OEMs. Infineon Technologies, backed by its aggressive SiC road‑map, has secured multiple joint ventures with leading car manufacturers to co‑develop next‑generation modules, positioning it as a market leader in performance‑critical applications. Continental AG and Mitsubishi Electric similarly command large market shares through vertically integrated product lines that span from onboard chargers to traction inverters, benefitting from strong sales networks and long‑term supply contracts. Collectively, these four firms shape the market structure, capturing the majority of Tier‑1 contracts and setting technology standards that drive overall industry growth.Beyond the marquee players, a vibrant ecosystem of specialized firms fuels innovation in niche and emerging segments. Texas Instruments and NXP Semiconductors focus on power‑management ICs that enable compact charger designs for mass‑market EVs. STMicroelectronics and ON Semiconductor deliver silicon‑carbide and gallium‑nitride solutions tailored for high‑power density applications. Valeo and Delphi Technologies (now part of BorgWarner) concentrate on integrated power modules for European OEMs, while Hitachi Automotive Systems and Samsung Electronics expand the portfolio with advanced thermal‑management and packaging technologies. Smaller but agile companies such as Semikron, XP Power, and Schneider Electric provide customized converter platforms that serve fleet‑scale conversions and specialty vehicle manufacturers, ensuring a competitive and diversified supply landscape.

List of Key EV Power Electronics Companies Profiled

- Bosch Sustainability Solutions

- Infineon Technologies

- Continental AG

- Mitsubishi Electric

- Texas Instruments

- NXP Semiconductors

- STMicroelectronics

- ON Semiconductor

- Valeo

- Delphi Technologies

- Hitachi Automotive Systems

- Samsung Electronics

- Schneider Electric

- Semikron

- XP Power

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Inverters

|

| By Application |

|

Traction Drive

|

| By End User |

|

OEMs

|

| By Technology |

|

Silicon‑Carbide

|

| By Vehicle Architecture |

|

Battery Electric Vehicles

|

Regional Analysis: North America

North America

The automotive industry in North America is undergoing a significant transformation with a strong push towards electrification. This transition necessitates advanced power electronics for motor drives, power inverters, and onboard charging systems. Key trends include the integration of power electronics with vehicle control systems and the development of high-efficiency power modules.

The expansion of EV charging infrastructure is a critical enabler for widespread EV adoption in North America. Investment in fast-charging stations and smart charging technologies is growing rapidly. This development creates significant opportunities for power electronics companies to provide solutions for charging infrastructure and grid integration.

Government policies and incentives play a crucial role in driving the EV market in North America. Emission standards and tax credits for EV purchases are stimulating demand and fostering innovation in the power electronics sector. Regulations promoting energy efficiency also contribute to the growth of the market.

Continuous advancements in power electronics technology, such as SiC and GaN semiconductors, are leading to improved efficiency, power density, and reliability. These advancements are essential for meeting the evolving demands of EV powertrains and charging infrastructure.

Europe

Europe is another significant player in EV Power Electronics Market, driven by ambitious climate goals and a strong focus on sustainable transportation. The region’s stringent emissions regulations and supportive government policies are accelerating the adoption of electric vehicles. Germany, France, and the UK are leading markets, with substantial investments in EV manufacturing and charging infrastructure. The demand for power electronics is particularly strong in passenger vehicles, commercial vehicles, and electric buses. The focus is shifting towards creating integrated power solutions that enhance vehicle performance and energy efficiency. Innovation in battery technology and charging infrastructure is further boosting the demand for advanced power electronics. The European Union’s push for a greener economy is a major catalyst for this market.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for EV Power Electronics. China is the dominant market, with a massive domestic EV market and significant government support. Other key markets include Japan, South Korea, and India. The region’s rapid industrialization, increasing urbanization, and growing environmental awareness are driving the adoption of electric vehicles. The demand for power electronics is strong across various applications, including passenger vehicles, commercial vehicles, and industrial equipment. The focus is on cost-effective solutions and localized manufacturing to cater to the vast market. The development of advanced battery technologies and smart charging infrastructure is a key driver of growth in this region.

South America

South America is an emerging market for EV Power Electronics, with growing interest in electric vehicles and increasing government support for sustainable transportation. Brazil and Argentina are the leading markets, with a focus on electric buses and light commercial vehicles. The region faces challenges related to infrastructure development and high vehicle costs, but the long-term outlook remains positive. The demand for power electronics is expected to increase as EV adoption accelerates and infrastructure investments expand.

Middle East & Africa

The Middle East and Africa represent a relatively nascent market for EV Power Electronics, with potential for significant growth in the coming years. Countries like the UAE, Saudi Arabia, and South Africa are investing in EV infrastructure and promoting the adoption of electric vehicles. The demand for power electronics is expected to rise as EV adoption accelerates and government regulations become more stringent. The region’s focus on renewable energy and sustainable development is a key driver for the emerging EV market.

Report Scope

This market research report provides a comprehensive analysis of the EV Power Electronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakup by product type, technology, application, and end‑user industry to identify high‑growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of EV Power Electronics Market?

-> EV Power Electronics Market was valued at USD 39.8 billion in 2025 and is expected to reach USD 94.2 billion by 2034, reflecting a CAGR of 10.0% over the forecast period.

Which key companies operate in EV Power Electronics Market?

-> Key players include Bosch Sustainability Solutions, Continental AG, Infineon Technologies, and Mitsubishi Electric, among others.

What are the key growth drivers?

-> Key growth drivers include accelerating electric‑vehicle adoption worldwide, supportive government incentives, tightening emissions regulations, and advances in silicon‑carbide (SiC) and gallium‑nitride (GaN) semiconductor technologies.

Which region dominates the market?

-> The reference does not specify a single dominant region.

What are the emerging trends?

-> Emerging trends include the adoption of SiC and GaN semiconductor technologies that improve efficiency and reduce weight of power modules.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...