EV Electronic Components Market Insights

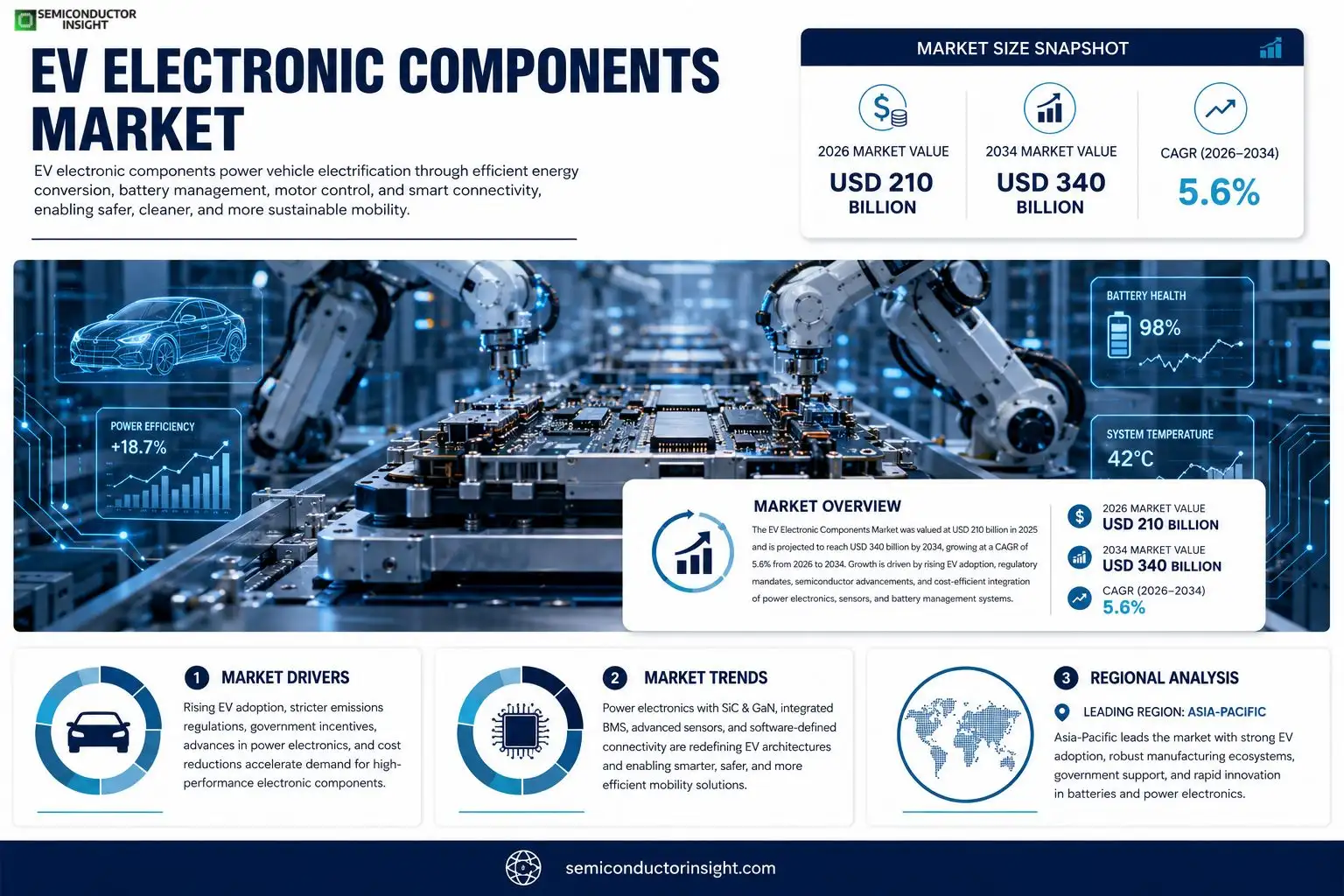

EV Electronic Components market size was valued at USD 210 billion in 2025. The market is projected to grow from USD 210 billion in 2025 to USD 340 billion by 2034, exhibiting a CAGR of 5.6%.

EV electronic components, including power electronics, battery‑management systems, electric‑drive modules,charging‑infrastructure hardware,sensors,and wiring harnesses,are essential for vehicle electrification.These parts convertelectricalenergy,manage battery health,control motor functions,and ensure safety.The market is experiencing rapid growth because of rising EV adoption driven by stricter emissions regulations,government incentives,and consumer demand for sustainable mobility.Furthermore,advances in semiconductor technologyand cost reductions accelerate component integration.Key players such as Bosch,Continental,Denso,Samsung SDI,and Infineonare expanding portfolios through strategic partnershipsand R&D investments.

MARKET DRIVERS

Increasing Adoption of Electric Vehicles

The rapid growth of battery‑electric cars worldwide is creating a surge in demand for high‑performance modules, converters, and sensors. Automakers are scaling production, which directly fuels the expansion of EV Electronic Components Market. This adoption is supported by governmental incentives and a broad consumer shift toward low‑emission mobility.

Advancements in Power Electronics

Innovations in silicon‑carbide (SiC) and gallium‑nitride (GaN) technologies are delivering higher efficiency and reduced weight for inverter and charger systems. Manufacturers that integrate these components can achieve longer vehicle range, positioning them favorably in a competitive market.

➤ “Component efficiency gains of 15‑20% are now considered a baseline for next‑generation EV platforms.”

Overall, the convergence of policy support, consumer awareness, and technological breakthroughs forms a robust foundation that accelerates growth across EV Electronic Components Market.

MARKET CHALLENGES

Supply Chain Constraints

Global shortages of semiconductors and rare‑earth materials have led to production bottlenecks. OEMs often face extended lead times, which increase inventory costs and can delay vehicle launches.

Other Challenges

High Material Costs

The price volatility of lithium, cobalt, and silicon‑carbide substrates adds pressure to component pricing, compressing margins for suppliers in EV Electronic Components Market.

MARKET RESTRAINTS

High Capital Expenditure

Establishing state‑of‑the‑art manufacturing lines for advanced power modules requires multi‑billion‑dollar investments. Smaller firms often lack the financial capacity to compete, limiting market diversification.Furthermore, the long payback period for new equipment can discourage entry, reinforcing concentration among a few large players within EV Electronic Components Market.

MARKET OPPORTUNITIES

Emerging Markets and New Vehicle Architectures

Regions such as Southeast Asia and Eastern Europe are witnessing rapid EV rollout, creating fresh demand for localized component production. Investors can capitalize on these growth pockets by establishing joint ventures or regional assembly hubs.Additionally, the shift toward modular vehicle platforms opens avenues for standardized electronic modules, potentially reducing development costs and accelerating time‑to‑market for suppliers in EV Electronic Components Market.

EV Electronic Components Market Trends

Accelerated Adoption of Power Electronics

EV Electronic Components Market is being reshaped by the rapid expansion of power electronics, which now dominate new‑vehicle architectures. Silicon‑carbide (SiC) and gallium‑nitride (GaN) devices are replacing traditional silicon in inverters, providing up to 30 % lower conduction losses and enabling higher voltage operation. This efficiency gain reduces cooling system weight and frees up packaging space, allowing designers to integrate more functions within a single module. Automakers are therefore shortening development cycles as they can source consolidated converter solutions from a smaller pool of qualified suppliers, driving cost parity with internal‑combustion‑engine platforms.

Other Trends

Battery‑Management System Integration

Battery‑management systems (BMS) are moving toward monolithic silicon designs that combine monitoring, balancing, and safety functions on a single die. Integrated BMS solutions cut wiring harness mass by roughly 15 % and improve fault detection latency, which is critical for high‑energy packs exceeding 100 kWh. In practice, this integration supports more accurate state‑of‑charge estimation, extending usable range by a few percent and enhancing consumer confidence in long‑distance EV travel. Leading suppliers are partnering with semiconductor foundries to co‑develop temperature‑aware architectures that maintain performance across wide operating ranges.

Sensor and Connectivity Proliferation

Advanced driver‑assistance systems (ADAS) and over‑the‑air (OTA) update capabilities are fueling a surge in vehicle sensors and high‑speed communication hardware. Ultrasonic, radar, and lidar arrays are now standard on many midsize EVs, while automotive‑grade Ethernet is replacing legacy CAN networks for data‑intensive applications. This shift enables real‑time sensor fusion and rapid software rollout, reducing the need for physical service visits. Simultaneously, cost reductions in MEMS manufacturing have lowered the price of inertial measurement units, making precise motion tracking accessible to a broader range of models. The combined effect is a more intelligent, adaptable vehicle platform that can evolve throughout its lifecycle without major hardware changes.

COMPETITIVE LANDSCAPEKey Industry Players

EV Electronic Components Market Competitive Landscape

EV Electronic Components Market is dominated by a handful of multinational engineering groups that control the majority of power‑electronics, battery‑management and motor‑drive modules. Bosch, Continental and Denso each leverage extensive automotive supply chains to deliver integrated inverter and charger solutions, accounting for roughly one‑third of global shipments in 2025. Samsung SDI and Infineon complement this core with advanced semiconductor and energy‑storage technologies, accelerating integration of silicon‑carbide devices that improve efficiency and reduce weight. Strategic joint ventures—such as Bosch’s partnership with Samsung SDI on next‑generation power modules—have deepened the competitive moat and raised entry barriers for smaller entrants. With the market valued at USD 210 billion in 2025 and projected to reach USD 340 billion by 2034, the top five players collectively generate over USD 120 billion in revenue, reinforcing their ability to invest heavily in silicon‑carbide and gallium‑nitride research. Their global footprint across Europe, North America and Asia further consolidates supply‑chain resilience, positioning them as primary drivers of component standardization and pricing power in an oligopolistic landscape.Beyond the dominant tier, a vibrant set of niche and regionally focused firms enriches the ecosystem with specialized sensors, wiring harnesses, and high‑voltage charging hardware. Companies such as NXP Semiconductors and Texas Instruments supply automotive‑grade microcontrollers and power‑management ICs that enable sophisticated vehicle‑to‑infrastructure communication. European supplier Valeo and Japanese titan Hitachi Automotive Systems excel in advanced driver‑assistance sensors and thermal‑management modules, while Chinese powerhouses BYD, LG Energy Solution and ZF Friedrichshafen expand rapidly in battery‑pack integration and electric‑drive assemblies. Emerging players like Aptiv and Magna International focus on modular electric‑drive platforms and flexible wiring‑harness architectures, capitalizing on cost‑reduction trends and localized production incentives. These companies, though smaller in revenue, drive innovation through focused R&D, strategic collaborations with OEMs, and agile manufacturing, ensuring a competitive depth that supports the market’s 5.6 % CAGR through 2034.

List of Key EV Electronic Components Companies Profiled

- Bosch

- Continental

- Denso

- Samsung SDI

- Infineon

- Texas Instruments

- NXP Semiconductors

- Magna International

- Aptiv

- Valeo

- LG Energy Solution

- Panasonic

- BYD

- Hitachi Automotive Systems

- ZF Friedrichshafen

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Power Electronics

|

| By Application |

|

Passenger Vehicles

|

| By End User |

|

OEMs

|

| By Technology |

|

Silicon Carbide Devices

|

| By Vehicle Architecture |

|

Dedicated EV Platforms

|

Regional Analysis: North America

North America

The demand for robust power electronics is surging in North America’s EV market, driven by the need for efficient motor control and onboard charging systems. Innovations in silicon carbide (SiC) and gallium nitride (GaN) semiconductors are enabling higher power density and improved energy efficiency in these components.

Sophisticated BMS are essential for ensuring the safe and optimal operation of EV batteries. North American manufacturers are focusing on developing BMS with advanced algorithms for state-of-charge estimation, thermal management, and cell balancing to maximize battery performance and longevity.

The integration of advanced driver-assistance systems (ADAS) is a key trend in North American EVs. This includes electronic control units (ECUs) for features like adaptive cruise control, lane keeping assist, and automatic emergency braking, driving innovation in sensor technology and processing power.

The expansion of public and private EV charging networks is significantly boosting the demand for components used in on-board chargers and charging station electronics. This includes power conversion systems and communication modules for seamless charging experiences.

Europe

Europe represents a significant and rapidly evolving market for EV electronic components, characterized by ambitious emission reduction targets and proactive government policies supporting the transition to electric mobility. With stringent regulatory frameworks like the European Union’s emissions standards, the demand for advanced electronic systems in EVs is consistently high. The region’s robust automotive industry, particularly in Germany, France, and the UK, serves as a major driver for component manufacturers. Innovation in battery technology and charging infrastructure is also gaining momentum, with significant investments in research and development. Business strategies in Europe emphasize sustainability, circular economy principles, and close collaboration with automotive OEMs to meet evolving regulatory requirements. The focus is on developing energy-efficient and long-lasting electronic components that contribute to the overall performance and environmental footprint of EVs.

Asia-Pacific

Asia-Pacific is poised to become the largest market for EV electronic components globally, driven by rapid economic growth, increasing urbanization, and government initiatives promoting electric vehicle adoption in countries like China, Japan, and South Korea. China, in particular, is a dominant force in the EV market, with significant investments in domestic battery and component manufacturing. The region boasts a well-established electronics manufacturing ecosystem, providing a competitive advantage for component suppliers. Innovation in battery technology, particularly lithium-ion batteries, is heavily concentrated in Asia-Pacific. Business strategies in the region emphasize cost competitiveness, localization of manufacturing, and catering to the specific needs of local automotive OEMs. The focus is on scaling up production capacity, developing advanced electronic solutions, and establishing strong supply chains to meet the growing demand for EV electronic components.

South America

South America presents a growing but relatively nascent market for EV electronic components. While EV adoption rates are currently lower compared to North America and Europe, governments in countries like Brazil and Chile are implementing policies to encourage the transition to electric mobility. The increasing focus on sustainability and the growing awareness of environmental issues are driving demand for EVs. The automotive industry in the region is undergoing transformation, with local manufacturers exploring opportunities in electric vehicle production. The business strategy is focused on providing cost-effective solutions and adapting to the specific needs of the regional market.

Middle East & Africa

The Middle East and Africa represent a promising long-term market for EV electronic components, with significant potential for growth driven by increasing urbanization, rising disposable incomes, and government initiatives promoting sustainable transportation. Countries like the UAE, Saudi Arabia, and South Africa are investing in electric vehicle infrastructure and implementing policies to encourage EV adoption. The automotive industry in the region is diversifying, with a growing interest in electric vehicles. Business strategies in the region focus on providing customized solutions and adapting to the unique challenges of the local market.

Report Scope

This market research report provides a comprehensive analysis of the EV Electronic Components Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of EV Electronic Components Market?

-> EV Electronic Components Market was valued at USD 210 billion in 2025 and is expected to reach USD 340 billion by 2034, exhibiting a CAGR of 5.6%.

Which key companies operate in EV Electronic Components Market?

-> Key players include Bosch, Continental, Denso, Samsung SDI, and Infineon, among others.

What are the key growth drivers?

-> Key growth drivers include rising EV adoption, stricter emissions regulations, government incentives, consumer demand for sustainable mobility, advances in semiconductor technology, and cost reductions that accelerate component integration.

Which region dominates the market?

-> The reference does not specify a single dominant region; market activity is strong across North America, Europe, and Asia‑Pacific, with Asia‑Pacific showing rapid growth due to high EV adoption rates.

What are the emerging trends?

-> Emerging trends include advanced power electronics, integrated battery‑management systems, smart charging‑infrastructure hardware, and the incorporation of AI/IoT for predictive maintenance and performance optimization.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...