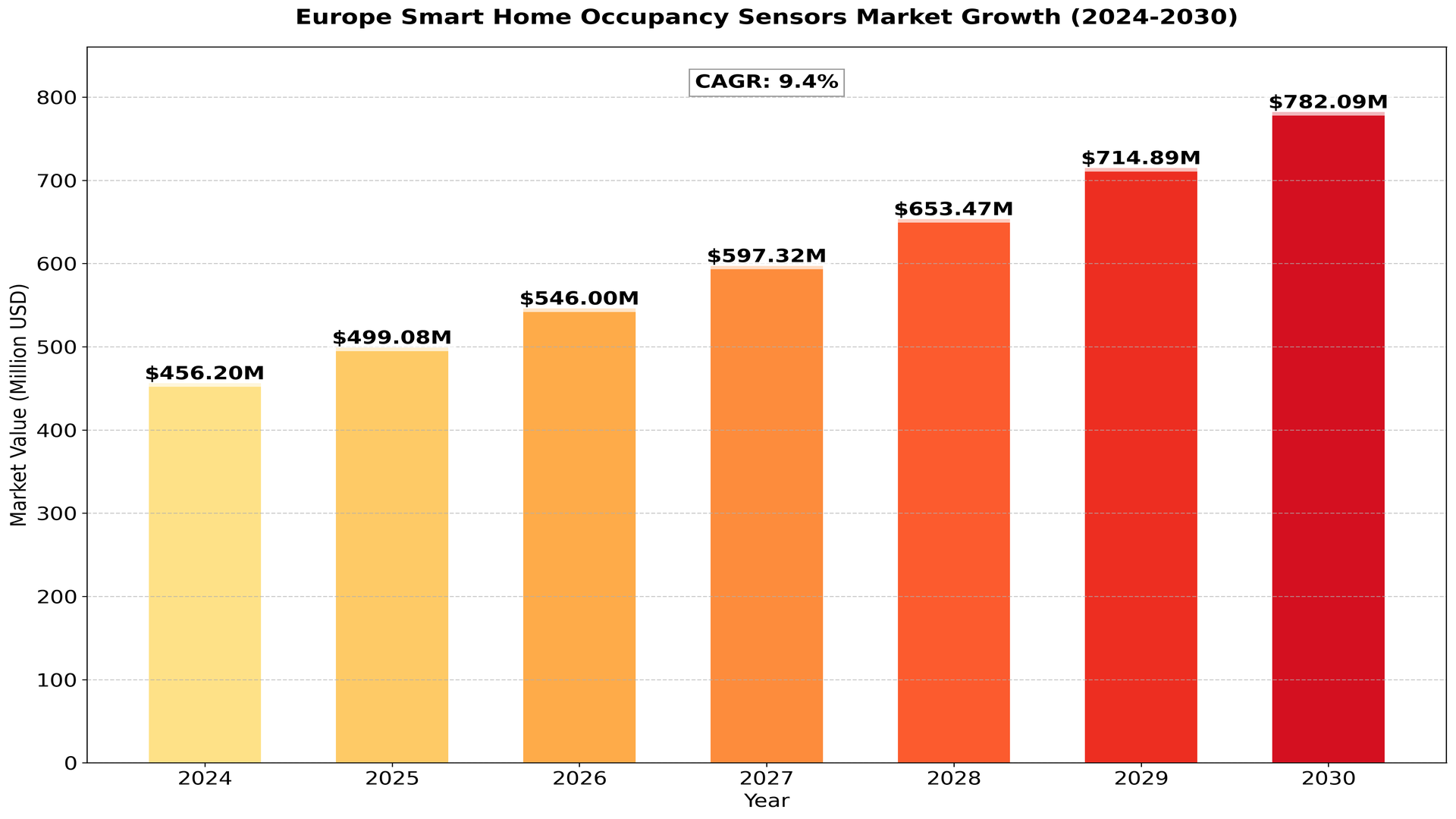

Europe Smart Home Occupancy Sensors Market size was valued at US$ 456.2 million in 2024 and is projected to reach US$ 782.9 million by 2030, at a CAGR of 9.4% during the forecast period 2024-2030.

Smart home occupancy sensors detect the presence of people in a room to automate lighting, HVAC, and other home systems.

The market is expanding due to growing demand for energy-efficient home automation solutions. Integration with smart lighting and HVAC systems is driving adoption. Advancements in sensor accuracy and false trigger reduction are improving user experience and energy savings.

Report Includes

This report is an essential reference for who looks for detailed information on Europe Smart Home Occupancy Sensors. The report covers data on Europe markets including historical and future trends for supply, market size, prices, trading, competition and value chain as well as Europe major vendors¡¯ information. In addition to the data part, the report also provides overview of Smart Home Occupancy Sensors, including classification, application, manufacturing technology, industry chain analysis and latest market dynamics. Finally, a customization report in order to meet user’s requirements is also available.

This report aims to provide a comprehensive presentation of the Europe Smart Home Occupancy Sensors, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Smart Home Occupancy Sensors. This report contains market size and forecasts of Smart Home Occupancy Sensors in Europe, including the following market information:

We surveyed the Smart Home Occupancy Sensors manufacturers, suppliers, distributors and industry experts on this industry, involving the sales, revenue, demand, price change, product type, recent development and plan, industry trends, drivers, challenges, obstacles, and potential risks.

Total Market by Segment:

by Country

• Germany

• United Kingdom

• France

• Italy

• Spain

• Netherlands

• Belgium

by Products type:

• PIR Sensors

• Ultrasonic Sensors

• Dual-technology Occupancy Sensors

• Others

by Application:

• Lighting Systems

• HVAC Systems

• Security & Surveillance Systems

• Others

key players include: (At least 8-10 companies included)

• Legrand

• Schneider Electric

• Siemens

• Honeywell

• Philips Lighting (Signify)

• ABB

• Fibaro

• Lutron Electronics

• Osram Licht AG

• Eve Systems

Including or excluding key companies relevant to your analysis.

Competitor Analysis

The report also provides analysis of leading market participants including:

• Key companies Smart Home Occupancy Sensors revenues in Europe market, 2019-2024 (Estimated), ($ millions)

• Key companies Smart Home Occupancy Sensors revenues share in Europe market, 2023 (%)

• Key companies Smart Home Occupancy Sensors sales in Europe market, 2019-2024 (Estimated),

• Key companies Smart Home Occupancy Sensors sales share in Europe market, 2023 (%)

Drivers

- Increasing Adoption of Smart Home Technologies

The rising trend of smart home automation is significantly driving the demand for occupancy sensors in Europe. As consumers become more interested in enhancing home security, convenience, and energy efficiency, smart home devices, including occupancy sensors, have gained traction. These sensors play a vital role in automating lighting, heating, and security systems, which enhances overall home comfort and functionality. - Growing Awareness of Energy Efficiency

Energy efficiency has become a top priority for consumers and businesses alike, driven by rising energy costs and environmental concerns. Occupancy sensors contribute to energy savings by ensuring that lights and HVAC systems operate only when spaces are occupied. This increased focus on reducing energy consumption aligns with Europe’s broader sustainability goals, promoting the adoption of occupancy sensors in residential settings. - Integration with Smart Home Ecosystems

The development of interconnected smart home ecosystems has facilitated the integration of occupancy sensors with various devices such as smart thermostats, lighting controls, and security systems. This interoperability enhances user experience by allowing for centralized control and automation of multiple devices, thereby boosting the market for occupancy sensors. - Government Initiatives and Regulations

European governments are increasingly implementing initiatives and regulations to promote energy-efficient solutions in homes. These initiatives encourage the adoption of smart home technologies, including occupancy sensors. Grants, subsidies, and incentives for energy-efficient renovations and installations are further stimulating the market by making these technologies more accessible to homeowners.

Restraints

- High Initial Costs

The cost of smart home occupancy sensors and the required infrastructure can be relatively high compared to traditional systems. While prices have been decreasing over time, the upfront investment may deter some consumers, particularly in budget-sensitive markets. This initial cost barrier can limit the growth of the occupancy sensor market in Europe. - Complexity of Installation and Integration

The installation of smart home systems can be complex, requiring technical expertise, especially for integrating occupancy sensors into existing home automation systems. This complexity may deter homeowners from adopting such technologies, particularly those who prefer simple, plug-and-play solutions. - Privacy Concerns

As occupancy sensors are designed to monitor human presence, concerns regarding privacy and data security can restrain market growth. Consumers may be hesitant to install devices that continuously monitor activity in their homes due to fears of potential misuse of data. Addressing these privacy concerns through transparent data handling practices and robust security measures is essential for market acceptance. - Technological Limitations

While occupancy sensors have advanced, they still face challenges such as false positives or negatives in detecting presence. Factors like furniture placement, pets, and environmental conditions can affect their accuracy. Any limitations in performance can lead to user dissatisfaction and reduce the willingness to adopt these technologies.

Opportunities

- Growth of IoT and Smart City Initiatives

The Internet of Things (IoT) is revolutionizing the smart home market, creating significant opportunities for occupancy sensors. As IoT technologies evolve, occupancy sensors can be integrated into broader smart city initiatives, enhancing urban planning, energy management, and public safety. This integration presents a chance for manufacturers to develop innovative solutions catering to both residential and urban markets. - Emerging Markets in Europe

While Western Europe has seen substantial adoption of smart home technologies, emerging markets in Eastern Europe present untapped opportunities. As economic conditions improve and consumer awareness of smart home benefits increases, the demand for occupancy sensors is expected to grow in these regions. Manufacturers can capitalize on this potential by tailoring products to meet the specific needs of these markets. - Technological Advancements

Continuous advancements in sensor technology, such as the development of more accurate and energy-efficient sensors, present opportunities for innovation. New technologies, including machine learning and AI, can enhance the functionality of occupancy sensors, enabling them to learn user behavior and improve energy management over time. This innovation can attract more consumers and expand market reach. - Integration with Energy Management Systems

The integration of occupancy sensors with energy management systems offers opportunities for enhanced energy efficiency in homes. As consumers increasingly seek to optimize their energy use, occupancy sensors can play a crucial role in intelligent energy management solutions, providing insights and automation that lead to significant cost savings and environmental benefits.

Challenges

- Market Competition

The smart home occupancy sensor market is becoming increasingly competitive, with numerous players offering various products and solutions. This competition can lead to price wars, impacting profit margins for manufacturers. To succeed, companies must differentiate their offerings through innovative features, superior technology, and exceptional customer service. - Interoperability Issues

The diverse range of smart home products and ecosystems can create challenges related to interoperability. Consumers may face difficulties in ensuring that occupancy sensors work seamlessly with other devices and platforms. Addressing these interoperability issues is critical for encouraging widespread adoption and user satisfaction. - Consumer Education and Awareness

Despite the growth of smart home technologies, many consumers remain unaware of the benefits and functionalities of occupancy sensors. Educating potential customers about the advantages of these sensors and how they can improve home automation is essential for driving adoption. Manufacturers and retailers need to invest in marketing and educational initiatives to raise awareness and inform consumers. - Regulatory and Compliance Challenges

As the smart home market continues to evolve, compliance with various regulations, including data protection laws and energy efficiency standards, becomes increasingly complex. Companies must navigate these regulations to ensure their products meet necessary requirements. Failing to comply can result in legal issues and damage to brand reputation.

Key Points of this Report:

• The depth industry chain includes analysis value chain analysis, porter five forces model analysis and cost structure analysis

• The report covers Europe and country-wise market of Smart Home Occupancy Sensors

• It describes present situation, historical background and future forecast

• Comprehensive data showing Smart Home Occupancy Sensors capacities, production, consumption, trade statistics, and prices in the recent years are provided

• The report indicates a wealth of information on Smart Home Occupancy Sensors manufacturers

• Smart Home Occupancy Sensors forecast for next five years, including market volumes and prices is also provided

• Raw Material Supply and Downstream Consumer Information is also included

• Any other user’s requirements which is feasible for us

Reasons to Purchase this Report:

• Analyzing the outlook of the market with the recent trends and SWOT analysis

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• Market segmentation analysis including qualitative and quantitative research incorporating the impact of economic and non-economic aspects

• Regional and country level analysis integrating the demand and supply forces that are influencing the growth of the market.

• Market value (USD Million) and volume (Units Million) data for each segment and sub-segment

• Distribution Channel sales Analysis by Value

• Competitive landscape involving the market share of major players, along with the new projects and strategies adopted by players in the past five years

• Comprehensive company profiles covering the product offerings, key financial information, recent developments, SWOT analysis, and strategies employed by the major market players

• 1-year analyst support, along with the data support in excel format.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...