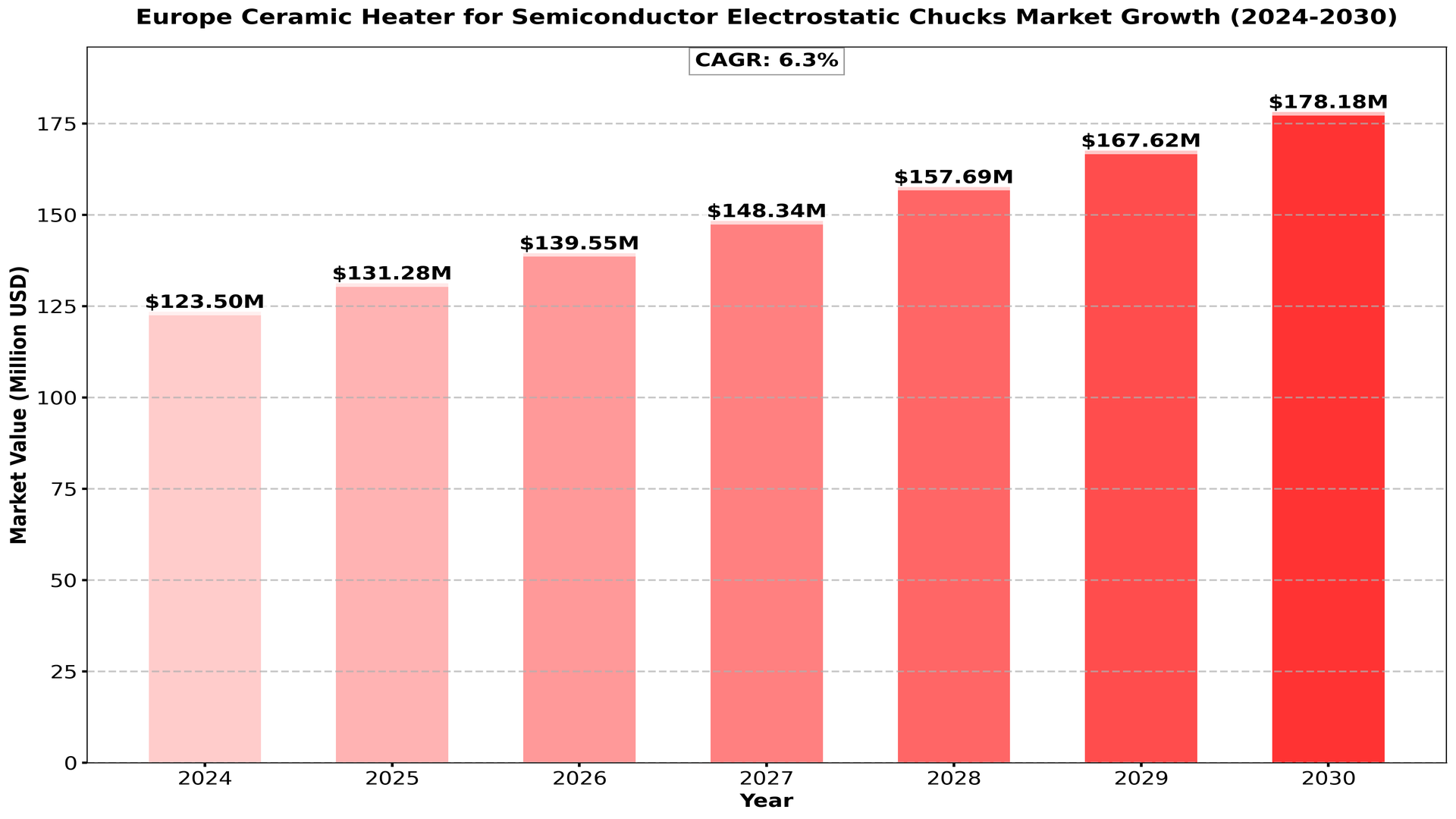

Europe Ceramic Heater for Semiconductor Electrostatic Chucks market size was valued at US$ 123.5 million in 2024 and is projected to reach US$ 178 million by 2030, at a CAGR of 6.3% during the forecast period 2024-2030.

Ceramic heaters for semiconductor electrostatic chucks are used to control wafer temperature during semiconductor manufacturing processes.

Market growth is driven by the expanding semiconductor industry in Europe and the need for precise temperature control in advanced chip manufacturing. The trend towards larger wafer sizes and more complex processes is increasing demand for high-performance chuck heating solutions. Ongoing research in ceramic materials and heater designs is enhancing temperature uniformity and control precision.

Report Includes

This report is an essential reference for who looks for detailed information on Europe Ceramic Heater for Semiconductor Electrostatic Chucks. The report covers data on Europe markets including historical and future trends for supply, market size, prices, trading, competition and value chain as well as Europe major vendors¡¯ information. In addition to the data part, the report also provides overview of Ceramic Heater for Semiconductor Electrostatic Chucks, including classification, application, manufacturing technology, industry chain analysis and latest market dynamics. Finally, a customization report in order to meet user’s requirements is also available.

This report aims to provide a comprehensive presentation of the Europe Ceramic Heater for Semiconductor Electrostatic Chucks, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Ceramic Heater for Semiconductor Electrostatic Chucks. This report contains market size and forecasts of Ceramic Heater for Semiconductor Electrostatic Chucks in Europe, including the following market information:

We surveyed the Ceramic Heater for Semiconductor Electrostatic Chucks manufacturers, suppliers, distributors and industry experts on this industry, involving the sales, revenue, demand, price change, product type, recent development and plan, industry trends, drivers, challenges, obstacles, and potential risks.

Total Market by Segment:

by Country

• Germany

• United Kingdom

• France

• Italy

• Spain

• Netherlands

• Belgium

by Products type:

• Alumina (Al2O3) Heater

• Aluminum Nitride (AlN) Heater

• Others

by Application:

• CVD Equipment

• PVD Equipment

• Etching Equipment

• Others

key players include: (At least 8-10 companies included)

• Kyocera Corporation

• NGK Insulators, Ltd.

• CoorsTek, Inc.

• Morgan Advanced Materials

• CeramTec GmbH

• Saint-Gobain Ceramic Materials

• Ferro Corporation

• H.C. Starck GmbH

• Corning Incorporated

• Murata Manufacturing Co., Ltd.

Including or excluding key companies relevant to your analysis.

Competitor Analysis

The report also provides analysis of leading market participants including:

• Key companies Ceramic Heater for Semiconductor Electrostatic Chucks revenues in Europe market, 2019-2024 (Estimated), ($ millions)

• Key companies Ceramic Heater for Semiconductor Electrostatic Chucks revenues share in Europe market, 2023 (%)

• Key companies Ceramic Heater for Semiconductor Electrostatic Chucks sales in Europe market, 2019-2024 (Estimated),

• Key companies Ceramic Heater for Semiconductor Electrostatic Chucks sales share in Europe market, 2023 (%)

Drivers:

- Growing Semiconductor Industry: Europe’s semiconductor industry is expanding due to the increasing demand for electronics, automotive applications, and renewable energy systems. The region’s strong focus on technology-driven sectors such as AI, IoT, and 5G fuels the need for more advanced semiconductor manufacturing equipment, which includes ceramic heaters for electrostatic chucks (ESCs).

- Adoption of Advanced Manufacturing Technologies: Semiconductor manufacturers are increasingly turning to advanced wafer processing techniques, which demand high-temperature stability and uniform heating. Ceramic heaters provide precise thermal control, essential for enhancing wafer quality during etching and deposition processes. The shift towards miniaturization and complex chip architectures further elevates demand for these high-performance heaters.

- Increased Investment in Semiconductor Fabrication: Governments across Europe, notably in Germany, France, and the Netherlands, are investing in semiconductor fabs and facilities. These investments create a positive ecosystem for equipment manufacturers, including those supplying ceramic heaters, to meet the rising demand from fabs and semiconductor foundries.

- Advancements in Electric Vehicles (EVs): The rise in electric vehicles, which require more semiconductor components, especially power semiconductors like silicon carbide (SiC) and gallium nitride (GaN), is boosting demand for precise and reliable ESC ceramic heaters in production processes.

Restraints:

- High Initial Cost of Ceramic Heaters: Ceramic heaters, while highly efficient, can be expensive to produce due to the complexity of their design and the materials used. This high cost is passed on to semiconductor manufacturers, potentially limiting adoption, especially among smaller fabs that may prefer cost-effective alternatives.

- Economic Uncertainty in Europe: Europe is facing some economic headwinds due to geopolitical tensions, inflationary pressures, and energy crises. These factors can impact overall investment in semiconductor manufacturing, particularly in capital-intensive areas like fabrication equipment, including ceramic heaters.

- Slow Recovery from Supply Chain Disruptions: The semiconductor industry has been experiencing supply chain bottlenecks since the COVID-19 pandemic, with delays in the procurement of raw materials and essential components. This has slowed production timelines for semiconductor manufacturers and, in turn, impacted the demand for supporting equipment like ceramic heaters.

Opportunities

- European Union’s Push for Semiconductor Sovereignty: The EU Chips Act aims to double Europe’s global market share in semiconductor production by 2030. This drive for local production offers significant opportunities for manufacturers of semiconductor equipment, including ceramic heaters for ESCs, as the region builds new fabs and expands existing facilities.

- Increasing Use of Power Semiconductors: The rise in renewable energy systems, power grids, and electric transportation is driving demand for power semiconductors. With Europe aiming to transition to greener energy sources, there’s an increasing need for ceramic heaters to support the production of power semiconductors used in energy-efficient technologies like solar inverters and EV charging stations.

- Innovations in Heater Materials and Design: Ongoing research in ceramic materials and heater designs that improve durability, energy efficiency, and thermal uniformity presents an opportunity for market growth. Nanotechnology and smart materials may lead to ceramic heaters that offer even greater precision and control, attracting more semiconductor manufacturers.

- Expansion in Emerging Markets: Central and Eastern European countries, such as Poland and Hungary, are rapidly developing their semiconductor capabilities, providing untapped markets for ceramic heater suppliers. These regions are increasingly seen as alternatives for semiconductor fabs due to favorable business conditions and lower operating costs compared to Western Europe.

Challenges

- Technical Complexity: Ceramic heaters require complex design specifications to meet the stringent requirements of semiconductor manufacturing. Achieving the necessary thermal uniformity, resistance to chemical exposure, and long-term reliability can be technically challenging, which may delay product development and commercialization timelines.

- Competition from Alternative Heating Technologies: While ceramic heaters offer excellent performance, alternative heating technologies such as metal heaters or halogen lamps are also being adopted in the semiconductor industry. These alternatives can be more cost-effective for certain applications, creating a challenge for ceramic heater manufacturers to differentiate their products.

- Stringent Environmental Regulations: Europe has some of the world’s most stringent environmental regulations, especially concerning the use of certain materials and energy consumption in manufacturing. Compliance with these regulations can add to the operational costs of ceramic heater manufacturers and slow down innovation in materials that are subject to heavy regulatory scrutiny.

- Dependence on Imports for Raw Materials: The production of ceramic heaters relies on the availability of high-quality raw materials such as alumina and silicon nitride, much of which is imported from non-European countries. Any disruptions in the global supply chain or trade restrictions can negatively impact production timelines and costs for European manufacturers.

Key Points of this Report:

• The depth industry chain includes analysis value chain analysis, porter five forces model analysis and cost structure analysis

• The report covers Europe and country-wise market of Ceramic Heater for Semiconductor Electrostatic Chucks

• It describes present situation, historical background and future forecast

• Comprehensive data showing Ceramic Heater for Semiconductor Electrostatic Chucks capacities, production, consumption, trade statistics, and prices in the recent years are provided

• The report indicates a wealth of information on Ceramic Heater for Semiconductor Electrostatic Chucks manufacturers

• Ceramic Heater for Semiconductor Electrostatic Chucks forecast for next five years, including market volumes and prices is also provided

• Raw Material Supply and Downstream Consumer Information is also included

• Any other user’s requirements which is feasible for us

Reasons to Purchase this Report:

• Analyzing the outlook of the market with the recent trends and SWOT analysis

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• Market segmentation analysis including qualitative and quantitative research incorporating the impact of economic and non-economic aspects

• Regional and country level analysis integrating the demand and supply forces that are influencing the growth of the market.

• Market value (USD Million) and volume (Units Million) data for each segment and sub-segment

• Distribution Channel sales Analysis by Value

• Competitive landscape involving the market share of major players, along with the new projects and strategies adopted by players in the past five years

• Comprehensive company profiles covering the product offerings, key financial information, recent developments, SWOT analysis, and strategies employed by the major market players

• 1-year analyst support, along with the data support in excel format.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...