MARKET INSIGHTS

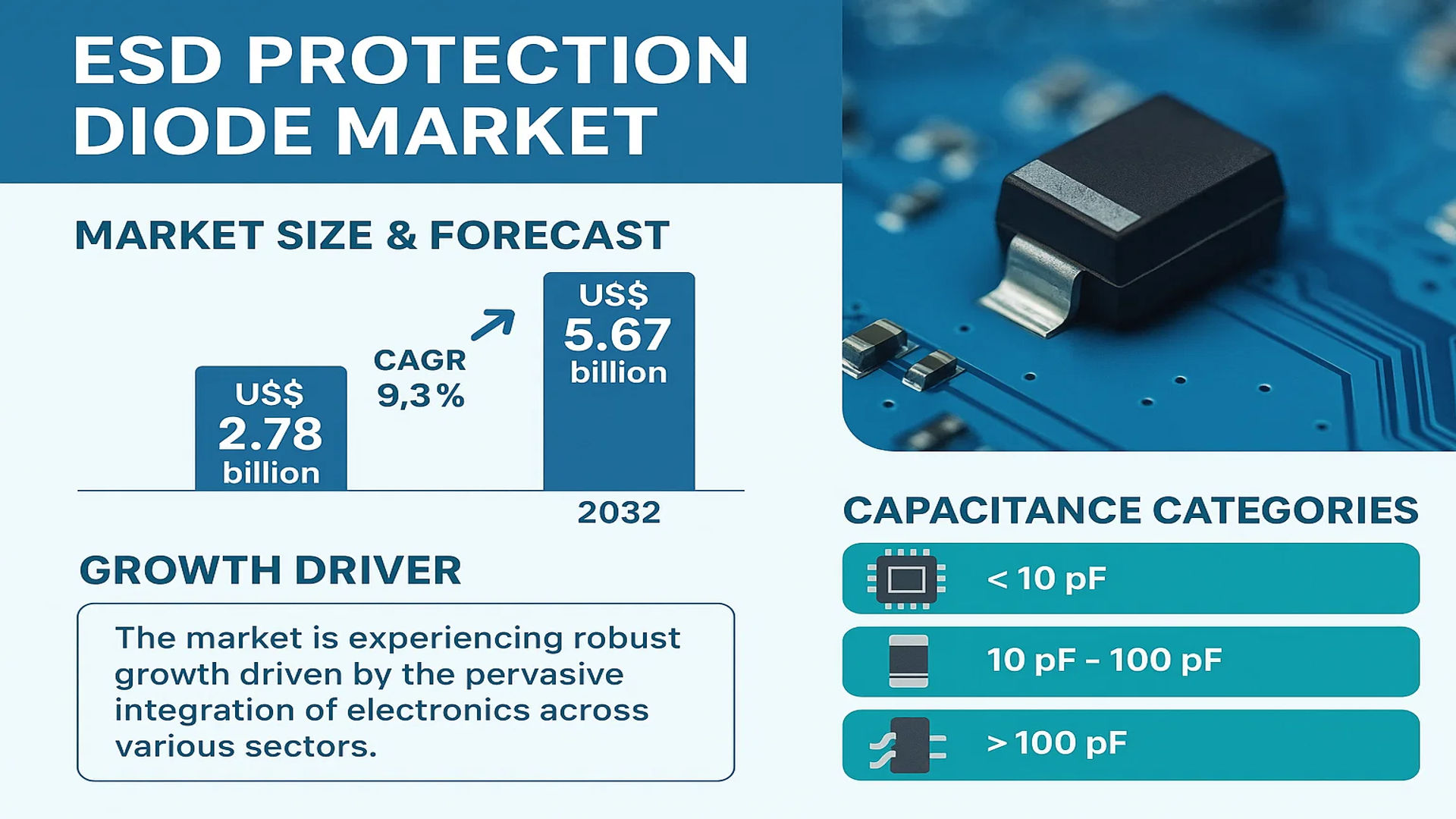

The global ESD Protection Diode Market size was valued at US$ 2.78 billion in 2024 and is projected to reach US$ 5.67 billion by 2032, at a CAGR of 9.3% during the forecast period 2025-2032

An ESD (Electrostatic Discharge) Protection Diode is a specialized semiconductor device engineered to safeguard sensitive electronic circuits from voltage spikes caused by electrostatic discharge. These diodes function by providing a low-impedance path to ground for transient currents, thereby clamping the voltage to a safe level and preventing damage to integrated circuits. They are categorized based on their capacitance, with common types including those below 10 pF, between 10 pF and 100 pF, and above 100 pF, each suited for different application bandwidths.

The market is experiencing robust growth driven by the pervasive integration of electronics across various sectors. The proliferation of consumer electronics and the rapid electrification of automotive systems are primary growth drivers because these applications are highly susceptible to ESD events. Furthermore, the expansion of 5G infrastructure and the Internet of Things (IoT) is creating substantial demand for reliable circuit protection. Key industry players, including Vishay, ON Semiconductor, and Infineon, are continuously innovating to develop diodes with lower clamping voltages and faster response times, further fueling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Consumer Electronics and Miniaturization Trends to Drive Market Expansion

The global ESD protection diode market is experiencing robust growth driven by the exponential expansion of consumer electronics. With over 1.5 billion smartphones shipped annually and the Internet of Things (IoT) ecosystem expanding rapidly, the demand for effective electrostatic discharge protection has become critical. Modern electronic devices are increasingly compact and operate at higher frequencies, making them more vulnerable to ESD events that can cause permanent damage. The miniaturization trend in electronics has pushed manufacturers to integrate advanced ESD protection solutions directly into integrated circuits and system designs. This integration is particularly important in 5G-enabled devices, wearable technology, and advanced automotive electronics where component density and signal integrity are paramount. The consumer electronics segment accounted for approximately 35% of the total ESD protection diode market revenue in 2024, demonstrating its significant influence on market dynamics.

Growing Automotive Electronics Adoption to Accelerate Market Growth

The automotive industry’s rapid transition toward electrification and advanced driver-assistance systems (ADAS) is creating substantial demand for ESD protection diodes. Modern vehicles incorporate hundreds of electronic control units and sensors that require robust protection against electrostatic discharge. The average premium vehicle now contains over 3,000 semiconductor chips, each requiring ESD protection to ensure reliability and safety. The automotive electronics segment is projected to grow at a compound annual growth rate of approximately 11.2% through 2032, significantly outpacing the overall market growth. This acceleration is driven by mandatory safety regulations, increasing vehicle electrification, and the integration of sophisticated infotainment systems. Furthermore, the transition to electric vehicles, which contain up to twice the electronic content of conventional vehicles, is creating additional demand for high-performance ESD protection solutions.

Stringent Regulatory Standards and Quality Requirements to Fuel Market Development

Increasing regulatory requirements across multiple industries are compelling manufacturers to implement comprehensive ESD protection strategies. International standards such as IEC 61000-4-2 mandate specific levels of ESD protection for electronic equipment, driving the adoption of protection diodes across various applications. The industrial sector, particularly in power distribution and control systems, requires ESD protection diodes that can withstand harsh environmental conditions and provide reliable operation over extended periods. Medical electronics represent another growth area, where equipment must meet rigorous safety standards and ensure patient safety. The medical electronics segment is expected to grow at approximately 10.8% annually, driven by increasing healthcare digitization and the adoption of advanced medical devices. These regulatory frameworks and quality requirements are creating a sustained demand for high-performance ESD protection solutions across multiple market segments.

MARKET CHALLENGES

Performance Trade-offs and Design Complexity to Challenge Market Penetration

The ESD protection diode market faces significant challenges related to performance trade-offs and increasing design complexity. As electronic devices operate at higher frequencies and lower voltages, designing effective ESD protection becomes increasingly difficult. Protection diodes must provide robust ESD protection while maintaining signal integrity and minimizing parasitic capacitance. This challenge is particularly acute in high-speed interfaces such as USB 3.2, HDMI 2.1, and Thunderbolt connections, where capacitance values above 0.5 pF can degrade signal quality. Design engineers must balance protection level requirements with performance specifications, often requiring custom solutions that increase development time and cost. Additionally, the integration of ESD protection into advanced semiconductor processes below 28nm presents technical challenges that require specialized expertise and additional design validation.

Other Challenges

Cost Pressure and Price Sensitivity

The market faces intense cost pressure, particularly in consumer electronics where profit margins are increasingly thin. While premium devices can accommodate higher-cost protection solutions, the mass market requires cost-effective solutions that maintain performance standards. The average selling price of ESD protection diodes has declined by approximately 15% over the past three years, putting pressure on manufacturer profitability. This price sensitivity is particularly challenging for suppliers developing advanced protection technologies that require significant research and development investment.

Technical Standardization Issues

The lack of universal technical standards across different regions and applications creates compatibility challenges for manufacturers. While international standards exist, their implementation varies across industries and geographical markets. This fragmentation requires manufacturers to develop multiple product variants to meet different regional requirements, increasing production complexity and inventory costs. The absence of unified testing methodologies also makes it difficult to compare protection performance across different products and manufacturers.

MARKET RESTRAINTS

Economic Volatility and Supply Chain Constraints to Restrain Market Growth

Global economic uncertainty and ongoing supply chain disruptions present significant restraints for the ESD protection diode market. The semiconductor industry has experienced cyclical demand patterns and supply constraints that affect the availability of raw materials and manufacturing capacity. Geopolitical tensions and trade restrictions have created additional challenges for global supply chains, particularly affecting the availability of silicon wafers and specialized packaging materials. These constraints have led to extended lead times and price volatility for ESD protection components. The automotive industry’s semiconductor shortage crisis demonstrated how supply chain disruptions can significantly impact component availability and pricing. While the situation has improved, residual effects continue to affect market stability and growth prospects.

Technical Limitations in Advanced Applications to Hinder Market Expansion

Technical limitations in meeting the requirements of emerging applications present another significant restraint for market growth. As electronic systems advance toward higher frequencies and lower operating voltages, conventional ESD protection technologies face performance limitations. The development of protection solutions for applications beyond 10 GHz and below 1V operating voltages requires substantial research investment and faces fundamental physical limitations. Additionally, the integration of ESD protection in advanced packaging technologies such as 2.5D and 3D IC packaging presents new challenges that existing solutions may not adequately address. These technical barriers require continued innovation but also create adoption hurdles for new technologies in cost-sensitive applications.

Competition from Alternative Protection Technologies to Limit Market Share

The ESD protection diode market faces increasing competition from alternative protection technologies that threaten to limit market share growth. Traditional diode-based protection must compete with emerging technologies including polymer-based protection devices, varistors, and integrated protection solutions. While diodes offer superior performance in many applications, alternative technologies provide cost advantages in price-sensitive markets. Additionally, the integration of ESD protection within system-on-chip designs reduces the need for discrete protection components in some applications. This trend toward integrated protection is particularly evident in mobile devices and wearable technology where space constraints drive design decisions. The competition from these alternative approaches requires diode manufacturers to continuously innovate and demonstrate clear performance advantages to maintain market position.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure and IoT Expansion to Create Significant Growth Opportunities

The global rollout of 5G infrastructure and the continued expansion of IoT ecosystems present substantial growth opportunities for the ESD protection diode market. 5G networks require extensive infrastructure including base stations, small cells, and network equipment that all require robust ESD protection. The IoT market is projected to grow to over 30 billion connected devices by 2030, each requiring protection against electrostatic discharge. This massive device expansion creates opportunities for ESD protection diode manufacturers across multiple market segments including industrial IoT, smart cities, and connected healthcare. The requirement for reliable operation in diverse environmental conditions and the critical nature of many IoT applications drive the need for high-performance protection solutions that can ensure long-term reliability and functionality.

Advancements in Electric Vehicle Technology to Drive New Application Opportunities

The rapid advancement of electric vehicle technology is creating new and substantial opportunities for ESD protection diode manufacturers. Modern electric vehicles incorporate sophisticated battery management systems, charging infrastructure, and power electronics that require advanced protection solutions. The high-voltage systems in electric vehicles, typically operating at 400V or 800V, present unique protection challenges that require specialized diode technologies. The global electric vehicle market is expected to grow at a compound annual growth rate of over 25% through 2030, creating corresponding demand for specialized protection components. Additionally, the development of wireless charging systems and vehicle-to-grid technology requires innovative protection solutions that can handle high power levels while maintaining reliability and safety standards.

Innovation in Semiconductor Materials and Packaging to Enable New Market Segments

Ongoing innovation in semiconductor materials and advanced packaging technologies is creating opportunities for new market segments and applications. The development of wide-bandgap semiconductors using materials such as silicon carbide and gallium nitride requires corresponding advances in ESD protection technology. These materials operate at higher temperatures and voltages than traditional silicon-based devices, necessitating protection solutions that can match their performance characteristics. Additionally, advanced packaging technologies including system-in-package and fan-out wafer-level packaging create opportunities for integrated protection solutions that offer space savings and improved performance. The research and development in these areas is driving innovation across the protection diode market and creating opportunities for manufacturers who can develop solutions that address the unique requirements of these emerging technologies.

ESD PROTECTION DIODE MARKET TRENDS

Miniaturization and Integration in Consumer Electronics Driving Market Expansion

The relentless drive towards smaller, more powerful, and connected electronic devices is a primary catalyst for the ESD protection diode market. As manufacturers pack more functionality into increasingly compact form factors, the inherent vulnerability of advanced semiconductor nodes to electrostatic discharge (ESD) surges dramatically. Components built on sub-10nm processes are significantly more susceptible to damage from transient voltage spikes, necessitating robust and integrated protection solutions. This trend is particularly evident in the smartphone and wearable technology sectors, where the demand for ultra-low capacitance diodes below 10 pF is paramount to preserve signal integrity in high-speed data lines. The market for these low-capacitance diodes is projected to grow at a CAGR exceeding 11% through 2032, outpacing the overall market average. Furthermore, the integration of ESD protection directly into interface ICs and within advanced system-in-package (SiP) designs represents a significant evolution, moving beyond discrete components to offer space-saving and performance-optimized solutions for next-generation electronics.

Other Trends

Automotive Electrification and Advanced Driver-Assistance Systems (ADAS)

The automotive industry’s rapid transition towards electrification and autonomy is creating substantial new demand for highly reliable ESD protection. Modern vehicles are essentially data centers on wheels, equipped with a proliferating number of electronic control units (ECUs), sophisticated sensors (LiDAR, radar, cameras), and high-speed communication networks like CAN FD and Automotive Ethernet. Each of these connection points is a potential entry point for ESD events, which can cause latent failures or immediate malfunctions, posing significant safety risks. Consequently, automotive-grade ESD protection diodes, which must meet stringent AEC-Q101 qualifications and operate reliably across a wide temperature range from -40°C to +150°C, are experiencing accelerated adoption. The automotive electronics segment is expected to account for over 25% of the total market demand by 2030, driven by the imperative to ensure the functional safety and longevity of electronic systems in harsh automotive environments.

Proliferation of High-Speed Data Interfaces and 5G Infrastructure

The global deployment of 5G networks and the widespread adoption of high-speed data interfaces, such as USB4, Thunderbolt, and HDMI 2.1, are fundamentally reshaping ESD protection requirements. These interfaces operate at multi-gigabit data rates, making them extremely sensitive to any parasitic capacitance that can degrade signal quality and cause data errors. This has led to a surge in demand for ESD diodes with exceptionally low capacitance, often below 0.5 pF, that can protect ports without impairing performance. Beyond consumer devices, the 5G infrastructure itself, including massive MIMO antennas and small cell base stations, requires robust surge protection solutions capable of handling high levels of transient energy from environmental factors like lightning. The need to protect sensitive RF components and power amplifiers in this infrastructure is a critical growth vector, with the telecommunications application segment forecast to be one of the fastest-growing over the next decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Focus on Innovation and Strategic Expansion to Secure Market Position

The global ESD protection diode market exhibits a fragmented yet competitive structure, characterized by the presence of numerous established semiconductor giants alongside specialized regional manufacturers. This dynamic is driven by the critical need for robust electrostatic discharge protection across a widening array of electronic applications, from consumer devices to automotive systems. Intense competition centers on technological innovation, product reliability, and cost-effectiveness.

Infineon Technologies AG and NXP Semiconductors N.V. are dominant forces, collectively holding a significant portion of the global market share. Their leadership is largely attributed to extensive R&D investments, broad and advanced product portfolios covering various capacitance ranges, and strong, established relationships with major OEMs in the automotive and industrial sectors. Furthermore, their global manufacturing and distribution networks provide a substantial competitive edge in meeting worldwide demand.

Meanwhile, Texas Instruments and STMicroelectronics are aggressively strengthening their market positions. They are achieving this through strategic product launches designed for next-generation high-speed data interfaces and through significant expansion of their production capacities to mitigate supply chain vulnerabilities. Their focus on developing ultra-low capacitance diodes for high-frequency applications positions them favorably in the rapidly growing consumer electronics and telecommunications segments.

The competitive landscape also features strong players from the Asia-Pacific region, particularly China. Companies like BrightKing and LANGTUO compete effectively by offering cost-optimized solutions, which has allowed them to capture considerable market share in price-sensitive segments and within their domestic market. Their growth strategy often involves scaling production and forming strategic partnerships to expand their international footprint.

List of Key ESD Protection Diode Companies Profiled

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Vishay Intertechnology, Inc. (U.S.)

- ON Semiconductor Corporation (U.S.)

- Littelfuse, Inc. (U.S.)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- BrightKing (China)

- Yint (China)

- Galaxy Electrical (China)

- SOCAY (China)

- LANGTUO (China)

- LAN Technology (China)

Segment Analysis:

By Type

Below 10 pF Segment Dominates the Market Due to High Demand in High-Speed Data Line Protection

The market is segmented based on type into:

- Below 10 pF

- 10 pF~100 pF

- Above 100 pF

By Application

Consumer Electronics Segment Leads Due to Pervasive Use in Smartphones and Portable Devices

The market is segmented based on application into:

- Consumer Electronics

- Automotive Electronics

- Industrial Power Distribution

- Lighting

- Security Systems

- Medical Electronics

- Home/Office Applications

- Power Supply

- Other

By End User

Electronics Manufacturing Segment Holds Largest Share Due to High Volume Production Needs

The market is segmented based on end user into:

- Electronics Manufacturing

- Automotive Industry

- Telecommunications

- Healthcare Equipment Manufacturers

- Industrial Equipment Producers

By Technology

TVS Diode Arrays Lead the Market Owing to Superior Multi-Line Protection Capabilities

The market is segmented based on technology into:

- TVS Diodes

- TVS Diode Arrays

- ESD Suppressor ICs

- Polymer ESD Suppressors

- Ceramic ESD Suppressors

Regional Analysis: ESD Protection Diode Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global ESD Protection Diode market, accounting for over 55% of global consumption by volume in 2024. This dominance is fueled by its position as the world’s manufacturing hub for consumer electronics, automotive components, and industrial equipment. China, in particular, is the epicenter of both production and consumption, driven by massive domestic demand and a vast export-oriented manufacturing sector. Key local manufacturers like BrightKing, Yint, and SOCAY operate alongside global giants such as Toshiba and Infineon, creating a highly competitive and cost-sensitive landscape. The region’s growth is further propelled by rapid urbanization, government initiatives promoting domestic semiconductor production, and the relentless miniaturization of electronics, which increases the need for robust, space-efficient ESD protection solutions. While cost remains a primary driver, there is a noticeable and growing demand for higher-performance diodes, especially in the automotive and industrial sectors, as product reliability standards continue to rise.

North America

North America represents a highly advanced and innovation-driven market for ESD protection diodes. Characterized by stringent quality and reliability standards, demand is primarily fueled by the aerospace, defense, medical electronics, and automotive industries, where component failure is not an option. The presence of major technology corporations and leading semiconductor design houses, including Texas Instruments and Littelfuse, creates a strong demand for high-performance, low-capacitance diodes. Regulations and standards from bodies like the Automotive Electronics Council (AEC-Q101) mandate the use of qualified components, pushing the adoption of advanced ESD protection solutions. Furthermore, significant investments in next-generation technologies such as 5G infrastructure, electric vehicles, and advanced computing are key growth drivers. The market is less price-sensitive compared to Asia-Pacific, with a greater emphasis on product performance, technical support, and supply chain reliability.

Europe

The European market is shaped by a strong regulatory framework and a focus on high-quality industrial and automotive manufacturing. Strict directives, including the Restriction of Hazardous Substances (RoHS) and the Waste Electrical and Electronic Equipment (WEEE) directive, influence component selection, favoring environmentally compliant products. Germany, as the region’s industrial powerhouse, has a particularly strong demand for ESD protection in automotive electronics, industrial automation, and power distribution systems. Leading companies like Infineon, NXP, and STMicroelectronics are headquartered in the region, driving innovation in semiconductor technology. The market is mature and demands diodes that offer not only robust protection but also low power consumption and high integration to support the region’s goals of energy efficiency and technological sophistication in end-products.

South America

The South American market for ESD protection diodes is emerging and is primarily driven by the gradual expansion of its consumer electronics and automotive manufacturing sectors. Countries like Brazil and Argentina are the main contributors to regional demand. However, market growth is often tempered by economic volatility, which impacts manufacturing investment and consumer spending power. While there is a baseline demand for ESD protection across all electronic devices, the adoption of advanced, higher-specification diodes is slower compared to more developed regions. Price sensitivity is a significant factor, leading to a higher volume of standard, cost-effective solutions. Nonetheless, as local industries continue to develop and integrate more sophisticated electronics, the demand for reliable ESD protection is expected to see steady, long-term growth.

Middle East & Africa

The ESD protection diode market in the Middle East & Africa is in a nascent stage of development. Demand is currently concentrated in a few key areas: telecommunications infrastructure projects, oil & gas industry automation, and consumer electronics imports. The UAE, Saudi Arabia, and Israel are the most active markets within the region, often driven by government-led initiatives to diversify economies and develop technological infrastructure. However, the market faces challenges, including a limited local manufacturing base, which results in a heavy reliance on imports, and a general lack of stringent electronic component regulations. Consequently, market growth is incremental, with demand primarily for standard protection components rather than cutting-edge solutions. The long-term potential is tied to broader economic development and increased investment in technological modernization across the region.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global ESD Protection Diode Market?

-> ESD Protection Diode Market size was valued at US$ 2.78 billion in 2024 and is projected to reach US$ 5.67 billion by 2032, at a CAGR of 9.3% during the forecast period 2025-2032.

Which key companies operate in Global ESD Protection Diode Market?

-> Key players include Vishay, ON Semiconductor, Toshiba, Texas Instruments, Littelfuse, Infineon, NXP, STMicroelectronics, BrightKing, Yint, Galaxy Electrical, SOCAY, LANGTUO, and LAN Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for consumer electronics, automotive electronics expansion, stringent ESD protection standards, and growth in IoT-connected devices.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 65% of global revenue in 2024, driven by strong manufacturing presence in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of components, integration with advanced packaging technologies, development of ultra-low capacitance diodes, and adoption in 5G infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...