MARKET INSIGHTS

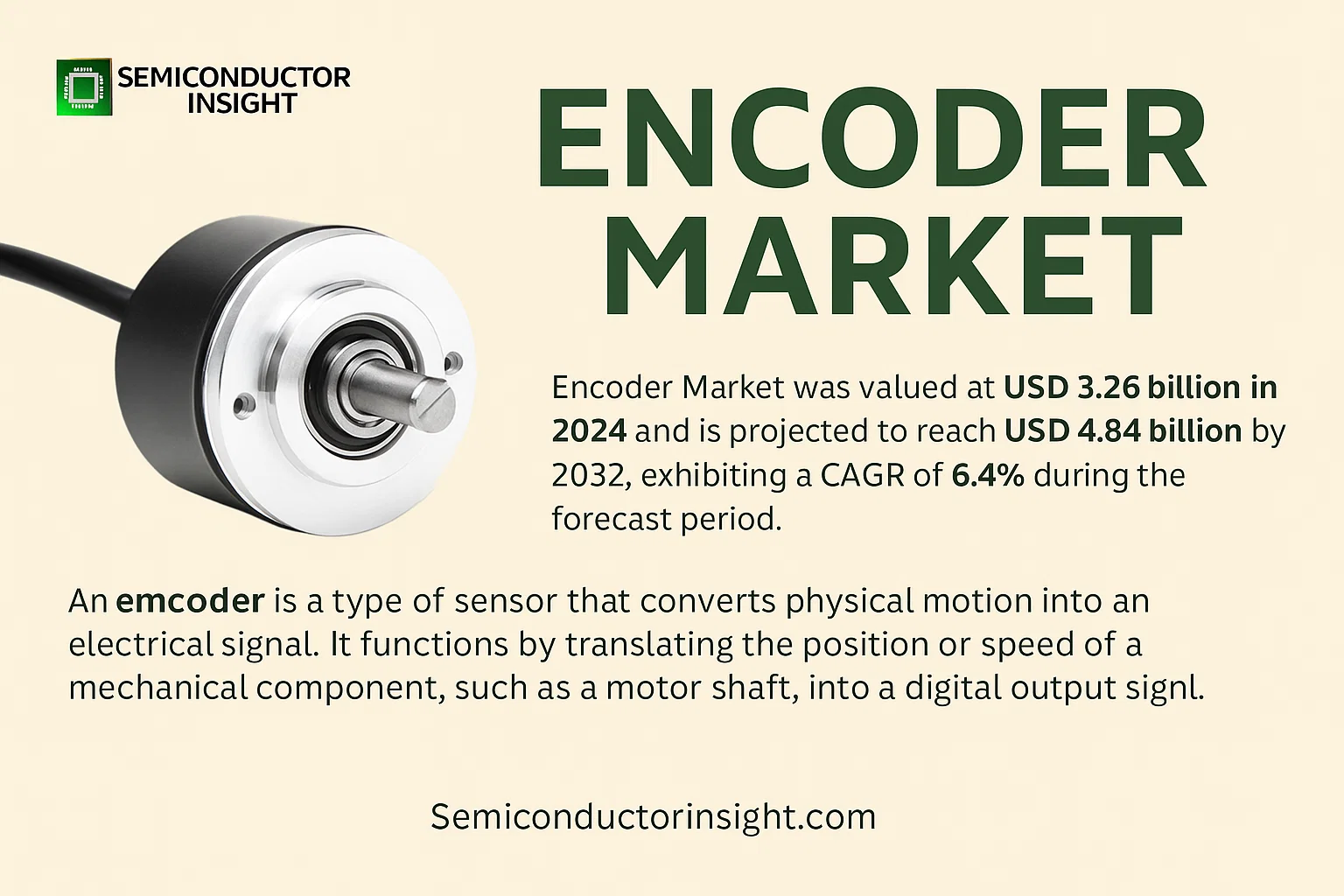

Global Encoder Market was valued at USD 3.26 billion in 2024 and is projected to reach USD 4.84 billion by 2032, exhibiting a CAGR of 6.4% during the forecast period.

An encoder is a type of sensor that converts physical motion into an electrical signal. It functions by translating the position or speed of a mechanical component, such as a motor shaft, into a digital output signal. This signal can then be used by control systems for precise monitoring and control of motion. Encoders are categorized based on their sensing technology, with optical, magnetic, and capacitive types being the most common. They are further classified by their output signal type (incremental or absolute) and by their physical form (rotary or linear).

The growth of the encoder market is primarily driven by the increasing automation across industries such as manufacturing, automotive, and healthcare. The demand for high-precision motion control in applications like CNC machines, robotics, and automated assembly lines is a significant contributor. Furthermore, the rise of Industry 4.0 and the Industrial Internet of Things (IIoT) has increased the need for sensors, including encoders, to provide data for predictive maintenance and operational efficiency. However, the market faces challenges such as the high cost of high-resolution encoders and the complexity of integrating them into existing systems.

Regionally, Asia Pacific is expected to witness the highest growth rate, driven by rapid industrialization and increasing investments in automation in countries like China, Japan, and South Korea. North America and Europe remain significant markets due to their well-established industrial bases and early adoption of advanced manufacturing technologies.

MARKET DRIVERS

Proliferation of Industrial Automation

The global push towards Industry 4.0 and smart manufacturing is a primary driver for the encoder market. Encoders are critical components in automated systems, providing precise feedback for motion control in robotics, CNC machinery, and assembly lines. The demand for higher productivity, accuracy, and efficiency is leading to increased adoption of automation across sectors, directly fueling encoder sales.

Growth in Electric Vehicles and Automotive Electronics

The rapid expansion of the electric vehicle (EV) market and advanced driver-assistance systems (ADAS) creates significant demand for high-performance encoders. They are essential for monitoring motor speed and position in EV powertrains, electronic power steering, and throttle control. The automotive industry’s shift towards electrification and automation represents a major growth vector for encoder manufacturers.

➤ The rise of collaborative robots (cobots) is a key trend, with encoders enabling the precise and safe human-robot interaction required for these applications.

Furthermore, technological advancements leading to the development of miniaturized, high-resolution encoders are expanding their use in medical devices, aerospace, and consumer electronics, opening up new application areas and driving market growth.

MARKET CHALLENGES

Price Pressure and Intense Competition

The encoder market is highly competitive, with numerous global and regional players. This environment creates significant price pressure, particularly for standard incremental encoders. Manufacturers face the dual challenge of maintaining profit margins while investing in research and development for next-generation products to stay ahead.

Other Challenges

Technical Complexity in Harsh Environments

Designing encoders that can reliably operate in extreme conditions—such as high temperatures, strong vibrations, and exposure to contaminants like dust and moisture—remains a significant engineering challenge, often requiring specialized and costlier designs.

Supply Chain Disruptions

Reliance on semiconductors and specific raw materials makes the encoder market vulnerable to global supply chain bottlenecks, which can lead to production delays and increased component costs.

MARKET RESTRAINTS

High Cost of Advanced Absolute Encoders

While offering superior performance, absolute encoders are significantly more expensive than their incremental counterparts. This higher cost can be a barrier to adoption, particularly for small and medium-sized enterprises or in cost-sensitive applications where the added functionality may not justify the investment, thereby restraining market growth in certain segments.

Market Maturity in Traditional Sectors

Certain established industrial sectors already have a high penetration rate of encoder technology. Growth in these mature markets is largely dependent on replacement cycles and incremental upgrades rather than new implementations, which can slow the overall market expansion rate.

MARKET OPPORTUNITIES

Expansion into Renewable Energy

The growing renewable energy sector, particularly wind power, presents a substantial opportunity. Encoders are vital for pitch and yaw control in wind turbines, ensuring optimal blade angle for maximum energy capture. The global focus on clean energy is driving investments in new wind farms and the maintenance of existing ones, creating a sustained demand for robust encoders.

Adoption of Industrial IoT and Predictive Maintenance

The integration of encoders with Industrial Internet of Things (IIoT) platforms enables predictive maintenance strategies. Smart encoders with built-in diagnostics can monitor their own health and the condition of the machinery they are installed on, providing data to prevent unplanned downtime. This value-added capability is a key differentiator and a significant growth opportunity.

Emerging Applications in Healthcare and Logistics

New applications in medical robotics for surgery and rehabilitation, as well as in automated guided vehicles (AGVs) and automated storage and retrieval systems (AS/RS) for warehouses, are emerging as promising markets for high-precision encoder solutions.

Encoder Market TrendRobust Market Growth and Segment Dynamics

The global encoder market is on a strong growth trajectory, valued at $3,268 million in 2024 and projected to reach $4,837 million by 2032, reflecting a Compound Annual Growth Rate (CAGR) of 6.4%. As a critical sensor technology, an encoder converts mechanical motion into digital signals, providing essential feedback for position, speed, and direction in automated systems. The market is fundamentally segmented by measurement method into rotary and linear encoders, with rotary encoders commanding a dominant 68% market share in 2023, a position expected to be maintained due to their extensive application range and established use across various industries.

Other Trends

Rising Preference for Absolute Encoders

The market is witnessing a notable shift in encoding technology. While incremental encoders have traditionally held a price advantage, the market share of absolute encoders is steadily increasing as their price gap with incremental types narrows. Absolute encoders, which provide a unique position value upon power-up without requiring a homing routine, are becoming the preferred choice in new equipment for their reliability and operational efficiency, particularly in applications demanding high precision and safety.

Geographical and Application-Led Expansion

Geographically, Europe, led by Germany, Italy, and France, holds the majority of the global market share, home to industry leaders like Heidenhain and Tamagawa Seiki. However, manufacturers in China, such as Zhejiang Reagle Sensing, are making significant technological strides, increasing their revenue and capturing a notable share of the domestic servo encoder market. From an application perspective, the machine tool sector is the largest end-user, accounting for 30% of the market in 2023. Concurrently, the robotics industry is a powerful growth driver, with the proliferation of industrial robots, AGVs, and medical robots fueling demand. Encoders are forecasted to constitute 25.4% of the robot market by 2030, underscoring their critical role in automation and Industry 4.0 advancements.

COMPETITIVE LANDSCAPE

Key Industry Players

A Technologically Advanced Market Dominated by Established Global Leaders

The global encoder market is characterized by a high degree of technological expertise and is led by a few major international corporations that hold significant market share. European and Japanese manufacturers, such as Heidenhain and Tamagawa Seiki, are widely recognized as technology leaders, particularly in the high-precision segment. These companies have established strong brand reputations through decades of innovation, offering encoders with exceptional accuracy, reliability, and durability that are essential for demanding applications in machine tools, robotics, and semiconductor manufacturing. The competitive dynamics are shaped by continuous R&D investments to improve resolution, miniaturization, and communication protocols like EtherCAT and PROFINET. The market structure is moderately concentrated, with the top five companies accounting for a substantial portion of the global revenue, creating significant barriers to entry for new players due to the required technical know-how and capital investment.

Beyond the dominant leaders, a diverse group of significant players competes in various niche segments and regional markets. Companies like Baumer, Pepperl+Fuchs, and Omron offer extensive portfolios catering to a broad range of industrial automation needs. Sensata Technologies and Rockwell Automation leverage their strong positions in broader industrial sectors to provide integrated encoder solutions. Meanwhile, specialized firms such as Renishaw excel in high-accuracy linear encoders for metrology. A notable trend is the growing presence of Chinese manufacturers like Zhejiang Reagle Sensing, which are rapidly closing the technology gap and capturing market share in the domestic and regional markets by offering cost-competitive products, particularly for servo motor applications. This creates a multi-tiered competitive environment with global giants, strong niche specialists, and emerging regional contenders.

List of Key Encoder Companies Profiled

- Heidenhain

- Tamagawa Seiki

- Sick

- Renishaw

- Pepperl+Fuchs

- Dynapar

- Baumer

- Sensata Technologies

- Broadcom

- Omron

- TR Electronic

- Balluff

- Rockwell Automation

- Bourns

- Zhejiang Reagle Sensing

- TE Connectivity

- Fagor Automation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Rotary Encoders are the dominant product category, primarily due to their extensive measurement range and suitability for a vast array of industrial automation applications involving rotational motion. They are fundamental components on motors like servos and steppers. Conversely, Linear Encoders are specialized for high-precision, short-distance linear displacement measurement, often commanding a higher price point in applications like CNC machine tools where absolute positional accuracy in a closed-loop system is critical. The technological choice between these types is dictated by the specific motion profile and precision requirements of the application. |

| By Application |

|

Machine Tools represent the largest application segment, driven by the extensive use of encoders for precision positioning and feedback in CNC systems. The Robots segment is identified as the most dynamic and rapidly growing area, fueled by the proliferation of industrial robots, AGVs, and other automated systems where encoders are indispensable for joint positioning and motion control. This segment’s growth is expected to continue robustly as automation and new industrialization trends accelerate globally, solidifying the encoder’s role as a core robotic component. |

| By End User |

|

Industrial Manufacturing is the leading end-user segment, encompassing the broadest use of encoders across sectors like machine tools, packaging, and textiles. The Automotive industry is a significant and mature user, particularly in automated production lines. The Healthcare & Medical Devices segment demands extremely high reliability and precision for equipment like surgical robots and diagnostic machinery. Meanwhile, the Logistics & Warehousing sector is experiencing substantial growth due to automation in material handling, and the Electronics & Semiconductor industry relies on encoders for the precise motion control required in manufacturing sensitive components. |

| By Technology |

|

Optical Encoders are traditionally the leading technology, prized for their high resolution and accuracy, making them suitable for demanding applications like precision machining. However, Magnetic Encoders are gaining significant traction due to their inherent robustness, reliability in harsh environments with contaminants like dust and oil, and generally lower cost structure. Inductive and Capacitive technologies offer unique advantages in specific niches, often providing contactless operation and high durability, but they cater to more specialized application requirements compared to the broader adoption of optical and magnetic principles. |

| By Output Signal |

|

Absolute Encoders are increasingly becoming the preferred choice, especially for new equipment, as they provide a unique position value immediately upon power-up without requiring a homing sequence, which is critical for safety and operational efficiency in complex automated systems like robotics. While Incremental Encoders have historically held a cost advantage for applications where knowing the absolute position is not essential, the performance benefits and falling price gap of absolute encoders are driving a steady market share shift. The trend towards smarter, more interconnected industrial systems favors the inherent advantages of absolute positioning technology. |

Regional Analysis: Encoder Market

The region is the world’s largest producer and consumer of industrial robots. This creates consistent, high-volume demand for encoders used for precise positioning and speed control in automated assembly, welding, and material handling applications, driving continuous market expansion.

National policies like “Made in China 2025” and similar initiatives in India and Southeast Asia actively subsidize and promote the adoption of automated machinery. This top-down support accelerates the integration of encoder-based systems in small and medium-sized enterprises.

The concentration of global consumer electronics and semiconductor fabrication plants in the region necessitates ultra-precision motion control. Encoders are critical components in CNC machinery, pick-and-place systems, and inspection equipment used throughout these supply chains.

A dense network of local component manufacturers provides cost-effective encoder solutions, making automation more accessible. This ecosystem fosters innovation and rapid customization to meet the specific needs of diverse regional industries, from textiles to heavy machinery.

North America

North America remains a highly significant and technologically advanced market for encoders, characterized by a strong focus on innovation and high-value applications. The region’s well-established aerospace, defense, and medical device industries demand encoders with exceptional reliability, precision, and the ability to operate in harsh environments. There is a notable trend towards the adoption of sophisticated networked encoders with advanced communication protocols like EtherCAT and PROFINET, integrating seamlessly into larger Industrial Internet of Things (IIoT) ecosystems. The push for reshoring manufacturing and modernizing existing industrial infrastructure also creates steady demand for encoder upgrades and replacements. While the market growth is mature compared to Asia-Pacific, it is driven by a need for premium, high-performance products that enhance operational efficiency and data acquisition in smart factories.

Europe

Europe is a cornerstone of the global encoder market, distinguished by its leadership in high-end industrial machinery, automotive manufacturing, and renewable energy sectors. German and Italian machine tool builders, renowned for their precision and quality, are major consumers of high-resolution encoders. The region’s strong commitment to sustainability is driving demand in wind turbine pitch control systems and solar tracking applications, where encoders ensure optimal energy capture. Strict regulatory standards for machine safety and energy efficiency further necessitate the use of reliable feedback devices. The European market is characterized by a strong preference for quality and long-term reliability over cost, supporting a vibrant landscape of specialized encoder manufacturers who focus on innovative solutions for complex motion control challenges.

South America

The encoder market in South America is emerging, with growth primarily fueled by the mining, agriculture, and oil and gas industries. Countries like Brazil and Chile are investing in automating their extensive natural resource extraction operations, where encoders are used in heavy machinery for positioning and control. The market is cost-sensitive, with a higher adoption rate of robust, incremental encoders suited for harsh environments rather than complex absolute systems. While industrial automation adoption is slower than in other regions due to economic volatility, there is a growing recognition of the efficiency gains offered by encoder technology. The market potential is significant, but realization depends heavily on sustained economic stability and increased investment in industrial modernization.

Middle East & Africa

The encoder market in the Middle East & Africa is nascent but shows promising growth avenues, particularly linked to infrastructure development and economic diversification efforts. In the Middle East, oil and gas operations continue to be a key application area, while ambitious projects like NEOM in Saudi Arabia are creating demand for automation technologies in construction and smart city infrastructure. In Africa, growth is sporadic, with pockets of demand emerging from the mining sector in countries like South Africa and the gradual modernization of manufacturing in North Africa. The region presents a long-term opportunity, with market development closely tied to foreign investment, political stability, and the pace of large-scale industrial and infrastructure projects.

Report Scope

This market research report provides a comprehensive analysis of the Encoder Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Encoder Market?

-> Global Encoder Market was valued at USD 3268 million in 2024 and is projected to reach USD 4837 million by 2032, at a CAGR of 6.4% during the forecast period.

Which key companies operate in Encoder Market?

-> Key players include Heidenhain, Tamagawa Seiki, Sick, Renishaw, Pepperl+Fuchs, Baumer, and Zhejiang Reagle Sensing, among others.

What are the key growth drivers?

-> Key growth drivers include the surge in demand for encoders driven by the robot market—including industrial robots, AGV/AMR mobile robots, and medical robots—and the machine tool market, which accounted for 30% of the market share in 2023.

Which region dominates the market?

-> Europe occupies the vast majority of the market share for encoder production, with key production areas in Germany, Italy, and France.

What are the emerging trends?

-> Emerging trends include the increasing market share of absolute encoders over incremental types and the growing role of encoders as core components in robotics, with an expected 25.4% share of the robot market by 2030.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...