MARKET INSIGHTS

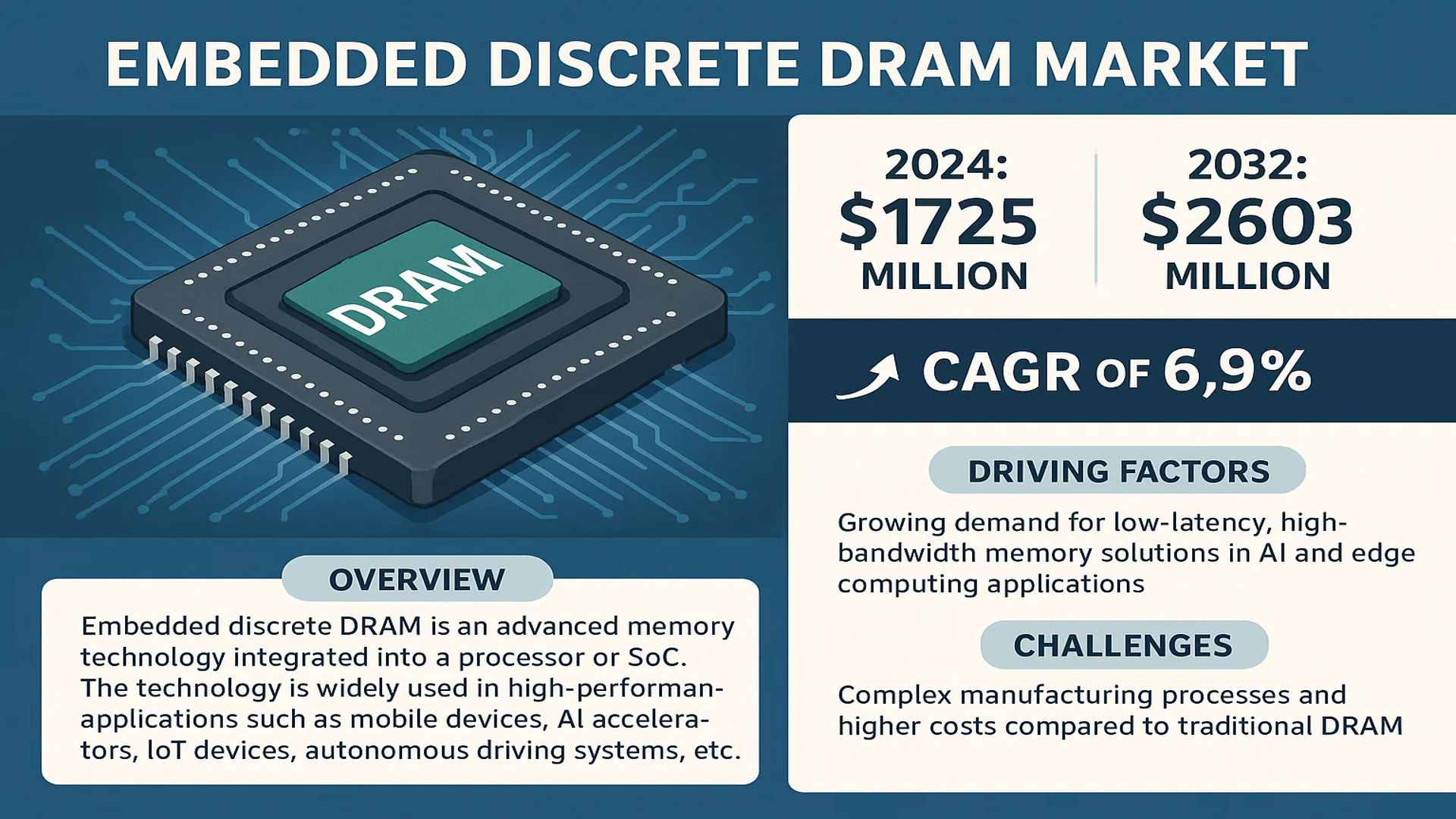

The global Embedded Discrete DRAM Market was valued at 1725 million in 2024 and is projected to reach US$ 2603 million by 2032, at a CAGR of 6.9% during the forecast period.

Embedded discrete DRAM is an advanced memory technology that integrates dynamic random access memory (DRAM) directly into a processor or system-on-chip (SoC). This integration significantly reduces data transmission latency and enhances energy efficiency by closely coupling memory with computing units. The technology is widely used in high-performance applications such as mobile devices, artificial intelligence accelerators, IoT devices, and autonomous driving systems. Key packaging technologies enabling this innovation include 2.5D and 3D integration, which provide high bandwidth while minimizing power consumption and space requirements.

The market growth is primarily driven by increasing demand for low-latency, high-bandwidth memory solutions in AI and edge computing applications. However, challenges such as complex manufacturing processes and higher costs compared to traditional DRAM may restrain expansion. Leading players like Samsung Electronics, SK Hynix, and Micron are investing heavily in R&D to overcome these barriers while expanding production capacities to meet growing demand from data centers and 5G infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for AI & Edge Computing Solutions to Propel Embedded DRAM Adoption

The global artificial intelligence market continues its explosive growth trajectory, with specialized AI chips expected to represent nearly 30% of total semiconductor revenue by 2030. This creates significant demand for high-bandwidth memory solutions like embedded discrete DRAM that can meet the intensive computational requirements of neural networks while maintaining energy efficiency. Unlike traditional discrete DRAM modules, embedded implementations reduce data transfer bottlenecks between processor and memory through innovative 2.5D and 3D packaging technologies. The edge computing revolution further amplifies this trend, as latency-sensitive applications in smart cities, industrial IoT, and autonomous vehicles require memory solutions that minimize power consumption while delivering real-time processing capabilities.

Mobile Device Miniaturization Drives Innovation in Embedded Memory Solutions

The smartphone industry’s relentless pursuit of thinner form factors and longer battery life creates perfect conditions for embedded DRAM adoption. As flagship smartphones increasingly incorporate advanced computational photography, on-device AI processing, and augmented reality features, the need for memory architectures that save space while reducing power consumption becomes critical. Process node shrink limitations below 7nm further incentivize innovative packaging approaches – with recent industry analyses showing that embedded DRAM solutions can reduce memory subsystem power consumption by up to 60% compared to conventional designs in mobile applications. This technological advantage positions embedded discrete DRAM as a key enabler for next-generation mobile devices.

Automotive Semiconductor Expansion Creates New Growth Vectors

The automotive industry’s transformation towards autonomous driving and advanced driver assistance systems (ADAS) represents a significant opportunity for embedded discrete DRAM providers. Modern vehicle architectures require failsafe memory solutions that combine high bandwidth with low latency, particularly for processing inputs from multiple high-resolution sensors in real time. The automotive semiconductor market is projected to grow at over 12% CAGR through 2030, with memory solutions accounting for an increasingly larger portion of bill-of-materials. Embedded DRAM’s ability to meet stringent automotive reliability standards while reducing system complexity makes it particularly attractive for functional safety applications in next-generation vehicles.

MARKET RESTRAINTS

High Development Costs and Technical Complexities Limit Market Penetration

While embedded discrete DRAM offers compelling technical advantages, its adoption faces significant economic barriers. The development of advanced packaging solutions like 2.5D and 3D integration requires substantial capital expenditure, with mask set costs for new designs exceeding conventional DRAM products by 3-5x. This pricing dynamic creates challenges for widespread adoption outside flagship applications where performance justifies the premium. Furthermore, the complex thermal management and signal integrity requirements of stacked memory configurations require specialized design expertise that remains concentrated among a limited number of semiconductor firms.

Limited Manufacturing Capacity Constrains Market Expansion

The semiconductor industry’s transition to advanced packaging technologies has outpaced the development of corresponding manufacturing infrastructure. Available capacity for 2.5D and 3D integration remains concentrated among a handful of foundries, creating potential supply chain bottlenecks as demand grows. This constraint is particularly acute for embedded DRAM solutions requiring sophisticated through-silicon via (TSV) technologies, where qualification cycles for new production lines can exceed 18 months. The resulting supply-demand imbalance could temporarily limit market growth despite strong underlying demand drivers.

Standardization Challenges Impede Ecosystem Development

The lack of industry-wide standards for embedded discrete DRAM interfaces creates integration challenges that hinder broader adoption. Unlike conventional DRAM technologies that benefit from well-established JEDEC specifications, emerging embedded solutions often require custom interfaces tailored to specific processor architectures. This fragmentation increases development costs for system integrators and limits interoperability between components from different vendors. The absence of common design rules for power delivery, signaling, and thermal management in 3D-stacked configurations further complicates the development of multi-vendor solutions.

MARKET CHALLENGES

Yield Optimization Remains Critical Challenge for Mass Production

Embedded discrete DRAM manufacturing faces unique yield challenges compared to conventional memory solutions. The complex interplay between logic devices and memory arrays in advanced packaging configurations compounds the impact of defects, with yield losses at any stage potentially rendering the entire stacked assembly unusable. Current industry estimates suggest that mature embedded DRAM production lines achieve yields 15-20% lower than comparable conventional DRAM processes. This yield gap represents a significant cost penalty that must be overcome through continued process refinement and design-for-manufacturing innovations.

Thermal Management Issues Demand Innovative Solutions

The tight integration of processing elements with memory arrays in embedded DRAM configurations creates formidable thermal management challenges. Memory cells exhibit temperature sensitivity that can impact retention characteristics, while densely packed logic devices generate significant heat. This thermal coupling can lead to performance throttling or reliability degradation if not properly addressed. Advanced packaging approaches compound these issues by introducing additional thermal interfaces and reducing the effectiveness of traditional cooling solutions. Recent studies suggest thermal considerations may limit maximum clock frequencies for some embedded DRAM configurations by 10-15% compared to discrete implementations.

MARKET OPPORTUNITIES

Emerging Memory-Centric Architectures Present Growth Potential

The semiconductor industry’s shift toward memory-centric computing architectures creates significant opportunities for embedded DRAM solutions. New computational paradigms like processing-in-memory (PIM) and near-memory computing rely on tight integration of logic and memory components to overcome data movement bottlenecks. These approaches could increase embedded DRAM attach rates in data center accelerators and high-performance computing applications by 3-4x over current levels within five years. The growing recognition of memory bandwidth as a critical performance limiter across multiple computing domains further strengthens the business case for adoption.

Heterogeneous Integration Trends Drive New Applications

Advancements in heterogeneous integration technologies enable novel combinations of processors, memory, and specialized accelerators that were previously unachievable. This trend opens new application areas for embedded discrete DRAM beyond traditional strongholds, including ultra-low-power wearable devices, high-performance medical imaging systems, and space-constrained industrial automation equipment. The ability to customize memory configurations for specific workload requirements while maintaining small form factors presents compelling value propositions across multiple industries.

Advanced Packaging Roadmaps Enable Cost Reductions

Ongoing innovations in semiconductor packaging technologies promise to address current cost barriers to embedded DRAM adoption. The development of high-density interconnect schemes, improved TSV processes, and wafer-level packaging techniques could reduce manufacturing costs by 30-40% over the next three years. These improvements, combined with increasing production volumes, will enhance the economic viability of embedded solutions for mid-range applications. Packaging technology roadmaps also indicate potential for mixed-node integration, allowing optimized pairing of mature memory processes with cutting-edge logic technologies to further optimize cost-performance tradeoffs.

EMBEDDED DISCRETE DRAM MARKET TRENDS

Rising Adoption in AI and Autonomous Driving to Drive Market Growth

The increasing integration of embedded discrete DRAM in artificial intelligence (AI) accelerators and autonomous driving systems is a key driver of market expansion. AI workloads, particularly those involving deep learning and neural network training, demand ultra-low latency and high-bandwidth memory solutions. Embedded DRAM, with its proximity to processing units, offers significant performance advantages, reducing data transfer bottlenecks. In the automotive sector, advanced driver-assistance systems (ADAS) and autonomous vehicles rely on embedded DRAM for real-time data processing. The market for autonomous vehicle semiconductors is projected to grow significantly, further fueling demand for high-performance memory solutions.

Other Trends

2.5D and 3D Integration Technologies

Advanced packaging techniques like 2.5D and 3D integration are transforming the embedded discrete DRAM landscape by enabling higher-density memory stacks with improved thermal efficiency. These technologies allow DRAM to be vertically integrated with processors using interposers or through-silicon vias (TSVs), dramatically increasing bandwidth while reducing power consumption. The 2.5D integration segment alone is expected to witness substantial growth due to its cost-effectiveness and scalability. Furthermore, 3D stacking continues to evolve, with major semiconductor players investing heavily in next-generation packaging solutions to meet the demands of high-performance computing.

Mobile Device Innovation and IoT Expansion

The proliferation of 5G-enabled smartphones and Internet of Things (IoT) devices is creating robust demand for embedded discrete DRAM solutions. Mobile device manufacturers are prioritizing power efficiency and compact form factors, making embedded DRAM particularly attractive compared to traditional discrete memory modules. In IoT applications, where energy consumption and space constraints are critical, embedded memory solutions offer significant advantages. The accelerating deployment of edge computing devices and wearables is further expanding the application scope for these memory technologies, with market projections indicating steady growth in these sectors through the forecast period.

Competitive Landscape and Regional Growth Patterns

The market is characterized by intense competition among leading semiconductor giants, with significant R&D investments focused on developing more efficient embedded memory solutions. While North America currently holds a substantial market share due to its concentration of AI and autonomous vehicle technology companies, the Asia-Pacific region is emerging as the fastest-growing market. China and South Korea, in particular, are witnessing rapid adoption of embedded DRAM technologies across various applications, supported by government initiatives in semiconductor self-sufficiency and smart manufacturing. Meanwhile, European markets show particular strength in automotive applications, with leading manufacturers integrating advanced memory solutions into next-generation vehicle architectures.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants and Niche Suppliers Battle for Market Dominance

The global embedded discrete DRAM market features a dynamic competitive landscape where established semiconductor leaders compete with specialized memory suppliers. Samsung Electronics and SK Hynix collectively dominate nearly 60% of the market share, leveraging their advanced process nodes and vertical integration capabilities. These Korean conglomerates continue to invest heavily in 3D-stacking technologies to maintain their leadership position.

Micron Technology has emerged as a strong contender, particularly in the North American market, where its partnerships with automotive and AI chip designers have driven significant growth. The company’s development of next-generation GDDR6-based embedded solutions positions it well for future market expansion.

Meanwhile, Taiwanese players Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics Corporation are gaining traction through their foundry services, enabling fabless semiconductor companies to integrate DRAM into advanced SoC designs. Their collaboration with packaging specialists in the development of chiplet architectures represents a key competitive advantage.

The market also features several specialized suppliers like Innodisk and Arcotek that focus on industrial and automotive applications. These companies compete through application-specific optimizations and reliability enhancements, particularly in extreme temperature environments.

List of Key Embedded Discrete DRAM Companies

- Samsung Electronics (South Korea)

- SK Hynix (South Korea)

- Micron Technology (U.S.)

- Taiwan Semiconductor Manufacturing Company (Taiwan)

- Kingston Technology (U.S.)

- Intel Corporation (U.S.)

- Kioxia (Japan)

- United Microelectronics Corporation (Taiwan)

- Innodisk Corporation (Taiwan)

- Arcotek (Taiwan)

- Elpida Memory (Japan)

Segment Analysis:

By Type

2.5D Integration Leads Market Growth Due to High Adoption in AI and Autonomous Systems

The market is segmented based on type into:

- 2.5D Integration

- Subvariants: Silicon interposer-based, organic interposer-based, and others

- 3D Integration

- Advanced Packaging

- Subvariants: Fan-out wafer-level packaging, chip-on-wafer, wafer-on-wafer

- Hybrid Solutions

By Application

AI Accelerators Show Highest Potential Due to Increasing Demand for High-Performance Computing

The market is segmented based on application into:

- Mobile Devices

- Artificial Intelligence

- Subapplications: Machine learning processors, neural network accelerators

- Autonomous Driving

- IoT Edge Devices

- High-Performance Computing

By End-User

Consumer Electronics Sector Drives Market Adoption Through Smartphone and Wearable Technologies

The market is segmented based on end-user into:

- Consumer Electronics

- Subsegments: Smartphones, tablets, wearables

- Automotive

- Data Centers

- Industrial Automation

- Medical Devices

By Technology Node

Sub-10nm Nodes Gain Traction for Power-Efficient Embedded Memory Solutions

The market is segmented based on technology node into:

- Above 28nm

- 16-28nm

- 10-16nm

- Below 10nm

- Subcategories: 7nm, 5nm, 3nm

Regional Analysis: Embedded Discrete DRAM Market

Asia-Pacific

The Asia-Pacific region dominates the global Embedded Discrete DRAM market, accounting for over 45% of the total revenue share in 2024, driven largely by China, South Korea, and Japan. This leadership stems from the region’s strong semiconductor manufacturing base, with key players like Samsung Electronics, SK Hynix, and Taiwan Semiconductor Manufacturing Company (TSMC) investing heavily in advanced packaging technologies such as 2.5D and 3D integration. The rapid adoption of AI accelerators, 5G-enabled mobile devices, and IoT applications further fuels demand for high-bandwidth, low-latency memory solutions. However, geopolitical tensions and export controls on semiconductor technologies present supply chain risks that companies must navigate strategically.

North America

North America is a hub for innovation in Embedded Discrete DRAM, with the U.S. leading in R&D and early adoption across AI data centers, autonomous vehicles, and edge computing. Major tech firms collaborate with memory manufacturers like Micron and Intel to develop customized solutions, particularly for high-performance computing (HPC) applications. The region benefits from substantial venture capital funding in AI startups and federal initiatives like the CHIPS Act, which allocated $52 billion to bolster domestic semiconductor production. Stringent IP protection laws also encourage proprietary technology development, though dependence on Asian foundries for manufacturing remains a vulnerability.

Europe

Europe’s market growth is propelled by automotive and industrial IoT applications, with Germany and France at the forefront. The region emphasizes energy-efficient designs to align with EU sustainability goals, driving demand for embedded DRAM in smart sensors and automotive ECUs. Collaborative research projects such as the EuroHPC initiative accelerate innovation, while stringent data privacy regulations shape memory architecture requirements. Nonetheless, slower adoption rates in consumer electronics compared to Asia and limited local DRAM production capacity restrain market expansion.

South America

The South American market shows nascent but promising growth, primarily in Brazil and Argentina, where telecom infrastructure upgrades and Industry 4.0 initiatives create opportunities for embedded memory solutions. Local manufacturers face challenges due to limited semiconductor ecosystem maturity and reliance on imported components, though increasing partnerships with global suppliers aim to bridge this gap. Economic volatility and inconsistent policy support continue to hinder large-scale investments in advanced packaging facilities.

Middle East & Africa

This emerging market is witnessing gradual adoption, led by smart city projects in the UAE and Saudi Arabia that incorporate AI and IoT technologies. While the lack of local semiconductor fabrication limits direct production, government-led technology diversification plans are attracting foreign memory suppliers to establish regional design centers. The emphasis on data localization in financial and healthcare sectors presents a unique growth niche for secure embedded memory solutions, albeit at a slower pace compared to other regions.

Report Scope

This market research report provides a comprehensive analysis of the Global Embedded Discrete DRAM Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1,725 million in 2024 and is projected to reach USD 2,603 million by 2032, growing at a CAGR of 6.9%.

- Segmentation Analysis: Detailed breakdown by type (2.5D Integration, 3D Integration) and application (Mobile Devices, Artificial Intelligence, Autonomous Driving) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading players including Samsung Electronics, SK Hynix, Micron, Intel, and Taiwan Semiconductor, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of advanced packaging technologies like 2.5D/3D integration and their impact on performance and power efficiency.

- Market Drivers & Restraints: Evaluation of factors such as AI/ML adoption, 5G expansion, and IoT growth versus challenges like supply chain constraints and fabrication complexity.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, foundries, OEMs, and investors regarding emerging opportunities.

The report employs primary and secondary research methodologies, including expert interviews and verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Embedded Discrete DRAM Market?

-> Embedded Discrete DRAM Market was valued at 1725 million in 2024 and is projected to reach US$ 2603 million by 2032, at a CAGR of 6.9% during the forecast period.

Which key companies operate in this market?

-> Major players include Samsung Electronics, SK Hynix, Micron, Intel, Taiwan Semiconductor, Kingston Technology, and Kioxia.

What are the key growth drivers?

-> Growth is driven by rising demand for high-performance computing, AI/ML applications, 5G adoption, and autonomous vehicles.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, with North America being a key innovation hub.

What are the emerging trends?

-> Key trends include 3D-stacked DRAM adoption, heterogeneous integration, and development of ultra-low-power solutions for edge devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...