MARKET INSIGHTS

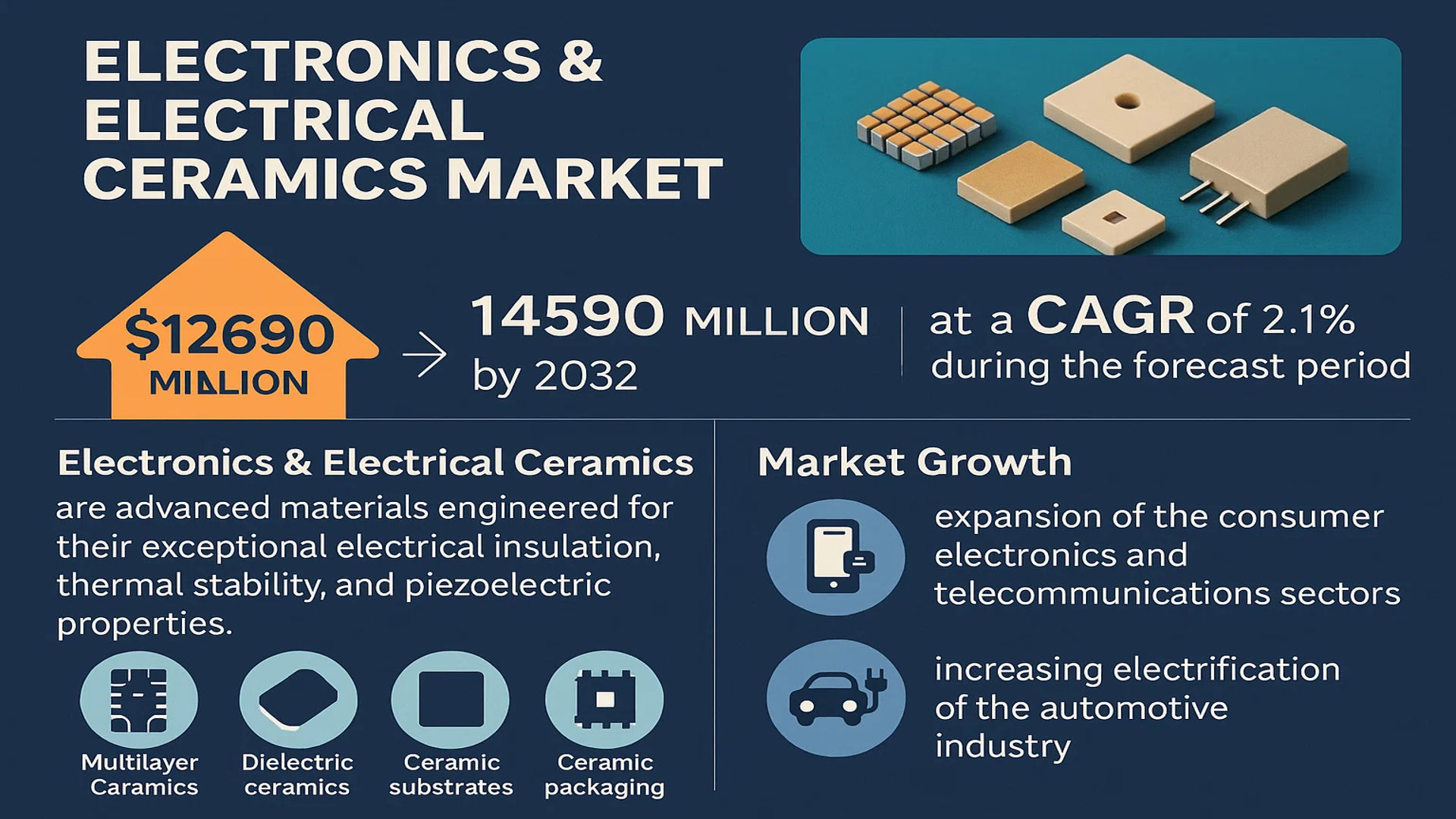

The global Electronics & Electrical Ceramics Market was valued at 12690 million in 2024 and is projected to reach US$ 14590 million by 2032, at a CAGR of 2.1% during the forecast period.

Electronics & Electrical Ceramics are advanced materials engineered for their exceptional electrical insulation, thermal stability, and piezoelectric properties. These ceramics are fundamental components in a vast array of devices, facilitating functions such as energy storage, signal transmission, and circuit protection. Key product types include Multilayer Ceramic Capacitors (MLCC), dielectric ceramics, ceramic substrates, and ceramic packaging, which are indispensable in modern electronics.

The market’s steady growth is primarily driven by the relentless expansion of the consumer electronics and telecommunications sectors, alongside the increasing electrification of the automotive industry. However, the market faces headwinds from the volatility in raw material prices and intense competition. China dominates as the largest sales market, accounting for approximately 45% of global consumption, largely due to its massive electronics manufacturing base. The Multilayer Ceramic Capacitor (MLCC) segment is the largest product category, holding a 40% market share, because of its critical role in miniaturizing and enhancing the performance of electronic circuits. Leading players such as Murata Manufacturing, Kyocera, and Samsung Electro-Mechanics (SEMCO) collectively command a significant portion of the market, continuously innovating to meet the demands for higher performance and reliability.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Consumer Electronics and IoT Devices to Accelerate Market Expansion

The global electronics and electrical ceramics market is witnessing robust growth driven by the exponential proliferation of consumer electronics and Internet of Things (IoT) devices. Smartphones, tablets, wearables, and smart home appliances increasingly rely on advanced ceramic components such as multilayer ceramic capacitors (MLCCs), which account for approximately 40% of the market share. The demand for MLCCs has surged due to their essential role in miniaturization, high-frequency performance, and stability in electronic circuits. With over 15 billion IoT devices currently active worldwide and projections indicating growth to 25 billion by 2030, the need for reliable, high-performance ceramics in sensors, actuators, and communication modules continues to expand. This trend is particularly pronounced in the Asia-Pacific region, where manufacturing hubs in China, Japan, and South Korea dominate production and consumption.

Advancements in Renewable Energy Infrastructure to Fuel Demand

Another significant driver is the global transition toward renewable energy and smart grid infrastructure. Electrical ceramics are critical in power transmission systems, solar inverters, wind turbines, and energy storage devices due to their excellent insulation properties, thermal stability, and durability. The push for decarbonization has accelerated investments in green energy projects, with global renewable energy capacity growing by nearly 10% annually. Ceramic substrates and insulators are essential in high-voltage applications, ensuring safety and efficiency in energy distribution networks. For instance, the expansion of ultra-high-voltage transmission projects in China and grid modernization initiatives in Europe and North America are creating sustained demand for advanced dielectric and insulating ceramics.

Growth in Automotive Electronics and Electrification to Boost Market

The automotive industry’s shift toward electrification and advanced driver-assistance systems (ADAS) is further propelling the electronics and electrical ceramics market. Modern vehicles incorporate numerous electronic control units, sensors, and power management systems that depend on ceramic components for reliability under harsh operating conditions. The electric vehicle (EV) revolution, in particular, relies heavily on ceramics for battery management systems, onboard chargers, and power electronics. Global EV sales surpassed 10 million units in 2023 and are expected to double by 2028, directly increasing the consumption of ceramics used in capacitors, substrates, and packaging solutions. This automotive trend complements broader industrial electrification efforts, including automation and robotics, which also utilize ceramic-based electronic components.

MARKET CHALLENGES

Volatility in Raw Material Prices and Supply Chain Disruptions to Impede Growth

Despite strong demand, the electronics and electrical ceramics market faces significant challenges related to raw material sourcing and supply chain stability. Key raw materials such as barium titanate, alumina, and zirconia are subject to price fluctuations due to geopolitical tensions, trade restrictions, and limited mining outputs. For example, prices of certain ceramic powders increased by over 20% in the past two years, squeezing profit margins for manufacturers. Additionally, supply chain disruptions, exacerbated by global logistics constraints and regional production bottlenecks, have led to extended lead times and inventory shortages. These factors are particularly critical for MLCC production, where even minor supply imbalances can cause significant market volatility and affect the availability of electronic components worldwide.

Other Challenges

Technical Complexities in Manufacturing

Producing high-purity, defect-free ceramics requires advanced manufacturing techniques and stringent quality control, which involve substantial capital investment and expertise. Sintering processes, for instance, must be meticulously controlled to achieve desired electrical properties, and even slight deviations can result in batch failures. This complexity increases production costs and limits scalability for smaller manufacturers.

Environmental and Regulatory Compliance

Stricter environmental regulations concerning the use of certain heavy metals and rare-earth elements in ceramics pose compliance challenges. Manufacturers must invest in cleaner production technologies and alternative materials, which can increase operational costs and slow down innovation cycles.

MARKET RESTRAINTS

High Initial Investment and Slow Adoption in Emerging Economies to Limit Growth

The high capital expenditure required for establishing ceramics manufacturing facilities acts as a major restraint. Advanced production equipment, cleanroom environments, and R&D investments necessitate significant financial resources, deterring new entrants and limiting capacity expansion among existing players. Moreover, in price-sensitive emerging economies, the adoption of high-performance ceramics is slower due to cost concerns and the prevalence of alternative materials. While developed regions rapidly integrate advanced ceramics into electronics and energy systems, emerging markets often prioritize lower-cost solutions, delaying widespread adoption. This disparity is evident in regions such as Southeast Asia and Africa, where ceramic consumption in electronics remains below global averages despite growing electronics manufacturing.

MARKET OPPORTUNITIES

Innovation in 5G Infrastructure and Aerospace Electronics to Unlock New Avenues

The rollout of 5G technology and the expansion of aerospace and defense electronics present lucrative opportunities for the electronics and electrical ceramics market. 5G networks require components that operate at higher frequencies with minimal signal loss, a niche where ceramics excel. Base stations, antennas, and RF modules increasingly incorporate ceramic substrates and capacitors to meet performance demands. Similarly, the aerospace sector relies on ceramics for their lightweight, high-temperature resistance, and reliability in critical systems such as avionics and satellite communications. With global 5G infrastructure investments exceeding $200 billion annually and aerospace electronics growing at 6% per year, ceramics manufacturers are poised to benefit from these high-value applications.

Strategic Collaborations and R&D Focus to Enhance Market Position

Leading market players are actively engaging in collaborations, mergers, and acquisitions to strengthen their technological capabilities and geographic reach. Recent partnerships between ceramic manufacturers and electronics giants have accelerated innovation in miniaturized components and next-generation materials. Additionally, increased R&D spending—accounting for up to 8% of revenue for top companies—is driving developments in nanotechnology-based ceramics and eco-friendly production processes. These efforts are not only expanding application horizons but also reducing production costs over time, making advanced ceramics more accessible across industries.

ELECTRONICS & ELECTRICAL CERAMICS MARKET TRENDS

Miniaturization and High-Frequency Demands Propel Multilayer Ceramic Capacitor (MLCC) Growth

The relentless drive towards miniaturization in consumer electronics and the escalating requirements for high-frequency performance in 5G infrastructure and automotive electronics are significantly accelerating the demand for Multilayer Ceramic Capacitors (MLCCs). As the largest product segment, commanding approximately 40% of the global market, MLCCs are fundamental components that provide essential functions like noise suppression, filtering, and energy storage in increasingly compact and powerful devices. This trend is compelling manufacturers to innovate in material science, developing advanced ceramic dielectrics with higher volumetric efficiency and superior electrical properties to meet the stringent specifications of next-generation applications. The proliferation of Internet of Things (IoT) devices, which often require hundreds of capacitors per unit, further amplifies this demand, creating a robust and sustained growth trajectory for this critical segment.

Other Trends

Rapid Expansion of 5G Infrastructure and Electric Vehicles

The global rollout of 5G networks and the accelerating adoption of electric vehicles (EVs) are creating substantial new avenues for electronics and electrical ceramics. 5G base stations require a dense array of high-frequency, high-power ceramic components, including substrates and capacitors, to handle increased data throughput and energy demands. Similarly, the EV revolution relies heavily on advanced ceramics for numerous applications, from sensors and battery management systems to power electronics and charging infrastructure. Ceramic substrates are particularly vital in power modules for their excellent thermal conductivity and electrical insulation, ensuring the reliability and efficiency of electric drivetrains. This dual thrust from telecommunications and automotive electrification is a primary catalyst for market expansion beyond traditional consumer applications.

Strategic Focus on Supply Chain Resilience and Regional Production

Recent global disruptions have underscored the critical importance of supply chain resilience, prompting a significant strategic shift within the industry. With China historically dominating sales with a share of about 45%, there is a concerted effort by OEMs and governments alike to diversify manufacturing bases and reduce geopolitical risks. This is fostering increased investment and production capacity in regions like Southeast Asia, Europe, and North America. Furthermore, leading players, who collectively hold a market share of around 55%, are heavily investing in research and development to create next-generation materials that offer enhanced performance, such as higher temperature stability and improved dielectric constants, to maintain a competitive edge. This focus on innovation, coupled with strategic capacity expansion outside of traditional hubs, is reshaping the global competitive landscape and ensuring a more stable supply for key end-use industries like medical devices and energy infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Technological Innovation and Geographic Expansion

The global electronics & electrical ceramics market exhibits a semi-consolidated structure, dominated by a handful of major players who collectively hold a significant market share. Kyocera Corporation and Murata Manufacturing are the unequivocal leaders, primarily due to their extensive product portfolios, which are heavily concentrated in high-volume segments like Multilayer Ceramic Capacitors (MLCCs), and their formidable global manufacturing and distribution networks. Their leadership is further cemented by continuous investment in research and development, allowing them to pioneer advanced materials for next-generation electronics.

Taiyo Yuden, Samsung Electro-Mechanics (SEMCO), and TDK Corporation also command substantial portions of the market. The sustained growth of these companies is intrinsically linked to the booming consumer electronics and automotive sectors, which are major end-users of ceramic components. Their strategies are heavily focused on scaling production capacity to meet relentless global demand, particularly for miniaturized and high-performance capacitors.

Furthermore, these established players are actively engaged in strategic initiatives, including capacity expansions in key regions like Southeast Asia and strategic mergers and acquisitions, to consolidate their market positions and tap into emerging application areas. This is crucial for maintaining growth momentum in a market that, while growing, is becoming increasingly competitive.

Meanwhile, other significant participants like NGK Insulators and CeramTec are strengthening their foothold by specializing in niche, high-value applications such as ceramics for energy transmission and medical devices. Their growth is driven by deep technical expertise and forming strategic partnerships with industrial giants, ensuring a diversified and resilient presence within the competitive landscape.

List of Key Electronics & Electrical Ceramics Companies Profiled

- Kyocera Corporation (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- Taiyo Yuden Co., Ltd. (Japan)

- Samsung Electro-Mechanics (SEMCO) (South Korea)

- TDK Corporation (Japan)

- NGK Insulators, Ltd. (Japan)

- CeramTec GmbH (Germany)

- ChaoZhou Three-circle (Group) Co., Ltd. (China)

- Guangdong Fenghua Advanced Technology Holding Co., Ltd. (China)

- Morgan Advanced Materials (UK)

Segment Analysis:

By Type

Multilayer Ceramic Capacitor (MLCC) Segment Dominates the Market Due to Pervasive Use in Modern Electronics

The market is segmented based on type into:

- Multilayer Ceramic Capacitor (MLCC)

- Dielectric Ceramics

- Ceramic Substrates

- Ceramic Packing

- Others

By Application

Home Appliances Segment Leads Due to High Volume Integration and Expanding Consumer Demand

The market is segmented based on application into:

- Consumer Electronics

- Home Appliances

- Medical Devices

- Power Grids and Energy

- Others

Regional Analysis: Electronics & Electrical Ceramics Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the Electronics & Electrical Ceramics market, accounting for approximately 45% of global sales, a dominance driven overwhelmingly by China’s massive manufacturing ecosystem. This region is the primary production hub for key components like Multilayer Ceramic Capacitors (MLCCs), which represent about 40% of the product segment. China’s strategic focus on advancing its electronics supply chain, coupled with substantial government support for high-tech industries, fuels continuous capacity expansion from major domestic players like ChaoZhou Three-circle and Guangdong Fenghua Advanced Technology. Japan and South Korea remain critical innovation centers, home to global titans such as Murata Manufacturing, TDK, and Taiyo Yuden, whose R&D efforts in miniaturization and high-frequency applications set industry standards. Demand is primarily propelled by the vast consumer electronics and home appliance sectors, though growth is increasingly supported by infrastructure modernization in power grids and renewable energy projects. While cost-competitiveness remains a key advantage, the region is also navigating a strategic pivot towards producing higher-value, specialized ceramics to maintain its edge amidst rising labor costs and global supply chain diversification efforts.

North America

The North American market is characterized by high-value, innovation-driven demand, particularly for advanced ceramics used in specialized applications within the medical, aerospace, defense, and telecommunications sectors. While the region’s volume consumption is lower than Asia-Pacific, its focus on cutting-edge technologies like 5G infrastructure, electric vehicles (EVs), and advanced medical imaging equipment creates a premium market segment. Stringent quality standards and regulatory requirements, especially from agencies like the FDA and FCC, compel manufacturers to utilize high-reliability components, fostering demand for precision electrical ceramics. The United States’ initiatives to onshore critical electronics manufacturing, supported by policies like the CHIPS and Science Act, are gradually encouraging local production and R&D investments. Key players like Kyocera (through its North American operations) and Morgan Advanced Materials have a significant presence, catering to the need for robust thermal management solutions, ceramic substrates for power electronics, and components for next-generation communication networks. The market’s growth is therefore less about volume and more about technological sophistication and supply chain resilience.

Europe

Europe maintains a strong position as a hub for high-performance and specialty ceramics, driven by its robust automotive, industrial, and renewable energy sectors. The region’s stringent environmental regulations, such as the EU’s RoHS and REACH directives, push manufacturers towards advanced, reliable, and environmentally compliant materials, benefiting suppliers of high-quality electrical ceramics. Germany is the regional powerhouse, with a strong manufacturing base that demands precision components for automotive electronics (particularly for the transition to electric vehicles) and industrial automation. Companies like CeramTec are globally recognized for their expertise in advanced technical ceramics used in demanding applications. Furthermore, Europe’s significant investments in upgrading its power grid infrastructure and expanding renewable energy capacity, as part of initiatives like the European Green Deal, are generating steady demand for ceramic insulators and components used in energy transmission and distribution. The market is mature and values quality, sustainability, and innovation over pure cost considerations.

South America

The South American market for Electronics & Electrical Ceramics is in a developing phase, with growth primarily tied to the expansion of its consumer electronics and appliance industries, as well as gradual modernization of energy infrastructure. Brazil and Argentina are the main markets, where local assembly of electronic goods creates demand for components like MLCCs. However, the region’s progress is often tempered by economic volatility, currency fluctuations, and less mature local supply chains, which can hinder large-scale manufacturing investments and make imports of advanced components costly. While there is a baseline demand for ceramics used in power transmission and distribution, the adoption of the latest high-tech ceramics is slower compared to more developed regions. The market potential is recognized, but unlocking it fully requires greater economic stability and increased investment in local industrial capabilities to reduce reliance on imported components.

Middle East & Africa

The Middle East & Africa region represents an emerging market with long-term growth potential, though its current share of the global electronics and electrical ceramics market is relatively small. Growth is primarily driven by infrastructure development, particularly in the Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE, where investments in smart city projects, telecommunications (5G rollout), and power generation/distribution create opportunities. The demand is largely met through imports, as there is limited local manufacturing capacity for these advanced materials. In Africa, the market is even more nascent, with growth sporadic and concentrated in a few more developed economies. Challenges include a lack of a significant local electronics manufacturing base, reliance on imports, and, in many areas, limited investment in the high-tech industrial sectors that are the primary consumers of these advanced materials. Nonetheless, the ongoing urbanization and digitalization trends across the region point toward a gradual increase in market importance over the coming decade.

Report Scope

This market research report provides a comprehensive analysis of the global Electronics & Electrical Ceramics market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Electronics & Electrical Ceramics Market?

-> Electronics & Electrical Ceramics Market was valued at 12690 million in 2024 and is projected to reach US$ 14590 million by 2032, at a CAGR of 2.1% during the forecast period.

Which key companies operate in Global Electronics & Electrical Ceramics Market?

-> Key players include Kyocera Corporation, Murata Manufacturing, Samsung Electro-Mechanics (SEMCO), TDK Corp, and Taiyo Yuden, among others. The top five manufacturers hold a combined market share of approximately 55%.

What are the key growth drivers?

-> Key growth drivers include rising demand for consumer electronics, expansion of 5G infrastructure, increasing adoption of electric vehicles, and the need for advanced medical devices.

Which region dominates the market?

-> Asia-Pacific is the largest market, with China alone accounting for approximately 45% of global sales, followed by Japan and Europe.

What are the emerging trends?

-> Emerging trends include miniaturization of components, development of ultra-high-capacitance MLCCs, integration of ceramics in IoT devices, and sustainable manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...