MARKET INSIGHTS

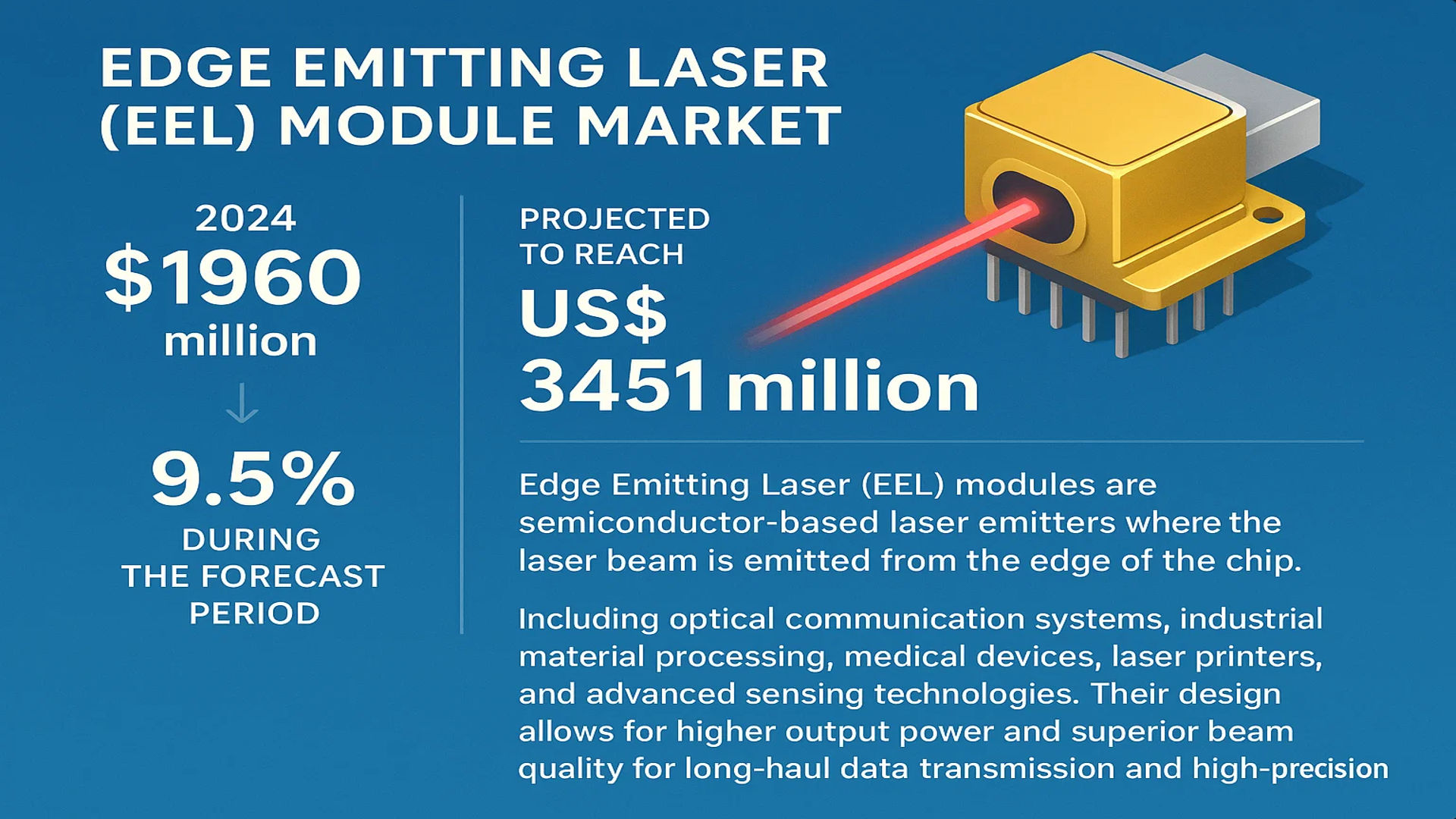

The global Edge Emitting Laser (EEL) Module Market was valued at 1960 million in 2024 and is projected to reach US$ 3451 million by 2032, at a CAGR of 9.5% during the forecast period.

Edge Emitting Laser (EEL) modules are semiconductor-based laser emitters where the laser beam is emitted from the edge of the chip. These components are fundamental to numerous high-performance applications, including optical communication systems, industrial material processing, medical devices, laser printers, and advanced sensing technologies. Their design allows for higher output power and superior beam quality compared to alternatives like Vertical-Cavity Surface-Emitting Lasers (VCSELs), making them indispensable for long-haul data transmission and high-precision tasks.

The market’s robust growth is primarily driven by the relentless global expansion of data centers and the deployment of 5G infrastructure, which necessitates high-speed, reliable optical transceivers. Furthermore, increasing automation in manufacturing is fueling demand for EEL modules in industrial laser systems for cutting, welding, and marking. Key industry players, such as Coherent Corp., Lumentum, and ams OSRAM, are continuously advancing product portfolios to cater to these evolving demands, ensuring the market’s upward trajectory.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of 5G and Fiber Optic Networks to Drive Market Growth

The global rollout of 5G infrastructure and the continuous expansion of fiber optic networks are significantly driving the Edge Emitting Laser (EEL) Module market. EEL modules are critical components in optical communication systems, providing the necessary high-power, coherent light sources for data transmission. With 5G deployments accelerating worldwide, demand for high-speed data centers and telecommunications equipment has surged. Over 300 operators across more than 100 countries have invested in 5G networks, requiring advanced photonic components. EEL modules, particularly distributed feedback (DFB) lasers, are essential for achieving the high data rates and low latency required by modern networks. This infrastructure expansion is creating sustained demand, with optical communication applications accounting for approximately 62% of the total EEL module market revenue in 2024.

Growing Adoption in Industrial and Medical Applications to Boost Market Expansion

The industrial and medical sectors are increasingly adopting EEL modules, contributing substantially to market growth. In industrial applications, EEL modules are used in material processing, laser cutting, welding, and precision manufacturing systems. The medical field utilizes these lasers in diagnostic equipment, surgical procedures, and therapeutic devices. The global medical laser market, which heavily relies on EEL technology, is projected to grow at approximately 8.2% annually through 2030. This growth is driven by advancements in minimally invasive surgeries and diagnostic technologies. EEL modules offer superior beam quality and power efficiency compared to alternative technologies, making them the preferred choice for applications requiring precision and reliability. The expanding adoption across these diverse sectors is creating new revenue streams and driving innovation in EEL module design and functionality.

Furthermore, technological advancements in semiconductor manufacturing are enabling higher production yields and improved performance characteristics. Manufacturers are developing EEL modules with enhanced thermal stability, longer lifespan, and reduced power consumption, making them more attractive across various applications. These improvements are particularly crucial for medical devices where reliability and precision are paramount, and for industrial applications where operational efficiency directly impacts profitability.

MARKET RESTRAINTS

High Manufacturing Costs and Technical Complexity to Limit Market Penetration

The Edge Emitting Laser Module market faces significant restraints due to high manufacturing costs and technical complexities involved in production. EEL modules require sophisticated semiconductor fabrication processes, clean room environments, and precision assembly techniques. The manufacturing yield rates for high-quality EEL modules typically range between 65-75%, contributing to higher per-unit costs compared to alternative technologies like VCSELs. This cost structure makes EEL modules less competitive in price-sensitive applications, particularly in consumer electronics and some automotive applications. The complex epitaxial growth processes and precise alignment requirements during packaging add substantial production expenses, limiting market penetration in cost-conscious segments.

Additionally, the technical expertise required for designing and manufacturing EEL modules presents another significant restraint. The development of these components demands specialized knowledge in semiconductor physics, optical engineering, and thermal management. The shortage of skilled professionals in these specialized fields can delay product development cycles and increase labor costs. This expertise gap is particularly pronounced in emerging markets where photonics education and training programs are still developing. The combination of high capital investment requirements and specialized human resources creates barriers to entry for new market participants and can slow down innovation cycles for existing manufacturers.

MARKET OPPORTUNITIES

Emerging Applications in LiDAR and Autonomous Vehicles to Create New Growth Avenues

The rapid development of autonomous vehicle technology and LiDAR systems presents substantial opportunities for the EEL Module market. EEL modules are becoming increasingly important in automotive LiDAR applications due to their ability to provide high-power, coherent light sources necessary for long-range detection and accurate environmental mapping. The autonomous vehicle market is projected to experience compound annual growth exceeding 18% through 2030, driving corresponding demand for advanced sensing technologies. EEL-based LiDAR systems offer superior performance in terms of range and resolution compared to alternative technologies, making them ideal for safety-critical automotive applications. This emerging application segment represents a significant growth opportunity, particularly as regulatory frameworks for autonomous vehicles evolve and consumer acceptance increases.

Furthermore, advancements in quantum technologies and scientific research applications are opening new opportunities for EEL modules. These lasers are essential components in quantum computing systems, atomic clocks, and precision measurement instruments. The global quantum computing market is expected to grow substantially, with investments in quantum technology research increasing by approximately 25% annually. EEL modules capable of providing stable, single-frequency operation are particularly valuable in these applications. The expanding research and development activities in quantum technologies, coupled with government funding initiatives worldwide, are creating new demand segments for high-performance EEL modules with specific technical characteristics.

MARKET CHALLENGES

Intense Competition from Alternative Technologies to Challenge Market Position

The EEL Module market faces significant challenges from competing technologies, particularly Vertical Cavity Surface Emitting Lasers (VCSELs) and other photonic solutions. VCSEL technology has advanced substantially in recent years, offering advantages in manufacturing scalability, cost efficiency, and integration capabilities. In consumer electronics and short-range data communication applications, VCSELs have captured market share due to their lower production costs and easier packaging requirements. The competitive pressure is particularly intense in applications where cost considerations outweigh performance requirements. This technological competition forces EEL manufacturers to continuously innovate and demonstrate clear performance advantages to maintain their market position.

Other Challenges

Supply Chain Vulnerabilities

The EEL Module market faces challenges related to supply chain vulnerabilities and component availability. The manufacturing process relies on specialized semiconductor materials, precision optical components, and advanced packaging materials. Disruptions in the supply of these critical components can significantly impact production schedules and product availability. The recent global semiconductor shortage highlighted these vulnerabilities, with lead times for certain photonic components extending beyond 12 months. Additionally, geopolitical factors and trade restrictions can affect the availability of rare earth materials and specialized manufacturing equipment, creating uncertainty in production planning and cost management.

Technical Performance Requirements

Meeting increasingly stringent technical performance requirements presents ongoing challenges for EEL module manufacturers. Applications in optical communications demand higher data rates, lower noise figures, and improved thermal stability. Industrial applications require higher power outputs and better beam quality, while medical applications need enhanced reliability and safety features. Achieving these performance improvements while maintaining cost competitiveness requires substantial research and development investment. The rapid pace of technological change means that products can become obsolete quickly, necessitating continuous innovation and product development to remain competitive in the market.

EDGE EMITTING LASER (EEL) MODULE MARKET TRENDS

Accelerated 5G Infrastructure Deployment to Emerge as a Dominant Trend

The global rollout of 5G networks is a primary catalyst for the Edge Emitting Laser (EEL) Module market, driving unprecedented demand for high-speed optical communication components. EEL modules, particularly Distributed Feedback (DFB) lasers, are integral to the transceivers used in 5G fronthaul and midhaul networks due to their superior single-mode performance and high modulation bandwidths capable of supporting data rates exceeding 100 Gbps. This infrastructure build-out is not a future projection but a current reality, with over 2.3 million 5G base stations deployed globally as of late 2023, each requiring multiple high-performance laser sources. The transition to higher network densities and the forthcoming shift to 6G research are further cementing the necessity for reliable, high-power EEL modules. While the demand is robust, manufacturers face the challenge of scaling production to meet volume requirements while maintaining the stringent performance and reliability standards demanded by telecommunications giants.

Other Trends

Expansion in Industrial Laser Processing and Material Sciences

Beyond telecommunications, the industrial sector is experiencing a significant surge in the adoption of high-power EEL modules for precision manufacturing applications. These lasers are the workhorses in material processing tasks such as cutting, welding, and drilling of metals and polymers, where their high brightness and ability to be efficiently fiber-coupled provide distinct advantages over other laser types. The global industrial laser market, a key consumer of EEL modules, is projected to maintain a strong growth trajectory, driven by automation in automotive and aerospace manufacturing. Recent advancements have focused on increasing output power and improving beam quality for ultrafast processing applications, enabling finer details and higher throughput. This trend is closely linked to the broader adoption of Industry 4.0 principles, where automated, laser-based systems are central to smart factory operations.

Advancements in Medical and Life Sciences Applications

The medical field represents a high-growth, high-value segment for EEL modules, leveraging their specific wavelengths for therapeutic and diagnostic instruments. There is a notable increase in their use in minimally invasive surgical systems, optical coherence tomography (OCT) for ophthalmology and cardiology, and flow cytometry for cell analysis. A key driver is the wavelength flexibility of EEL technology, which allows for tailoring output to specific biological interactions, such as tissue ablation or fluorescence excitation. The medical laser systems market, heavily reliant on these precise light sources, continues to expand as new surgical techniques and diagnostic modalities are developed and commercialized. This growth is further supported by an aging global population and increasing healthcare expenditure, which fuels the adoption of advanced medical technologies that incorporate sophisticated laser modules for improved patient outcomes.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Strategic Partnerships to Maintain Market Position

The global Edge Emitting Laser (EEL) Module market exhibits a moderately consolidated competitive structure, characterized by the presence of established multinational corporations, specialized mid-tier manufacturers, and innovative niche players. This dynamic ecosystem is driven by continuous technological advancement, particularly in materials science and photonic integration, as companies compete to meet the escalating performance demands of high-speed data communication, industrial manufacturing, and emerging medical applications.

Coherent Corp. and Lumentum Holdings Inc. are recognized as dominant forces in this landscape, collectively commanding a significant portion of the market share. Their leadership stems from decades of photonics expertise, comprehensive product portfolios spanning multiple wavelengths and power classes, and extensive global distribution networks. Both companies have made substantial investments in developing high-power EEL modules for material processing and advanced distributed feedback (DFB) lasers for telecommunications, enabling them to serve diverse industrial and communication sectors effectively.

ams OSRAM and II-VI Incorporated (now Coherent Corp.) have also established strong market positions through vertical integration and mastery of semiconductor laser fabrication. These companies leverage their in-house epitaxial growth and wafer processing capabilities to produce highly reliable EEL chips, giving them cost and performance advantages in competitive market segments. Their growth is further propelled by strategic acquisitions, such as Coherent’s merger with II-VI, which expanded their technological breadth and customer base across multiple continents.

Meanwhile, Broadcom Inc. maintains a formidable presence in the communication segment, specializing in high-performance EELs for data center transceivers and network infrastructure. Their expertise in indium phosphide-based laser design enables them to produce devices that meet the stringent requirements of 400G and 800G optical modules, which are critical for next-generation data centers. Because of this focus on high-growth applications, Broadcom continues to capture value in the expanding optical communication market.

Japanese players including Sony Corporation and Hamamatsu Photonics contribute significantly to the market through their excellence in precision manufacturing and sensor applications. Sony’s expertise in consumer electronics and imaging systems drives demand for its EEL modules in laser projection and sensing, while Hamamatsu’s strong focus on scientific and medical instruments ensures a steady demand for its high-quality laser sources. Both companies benefit from robust R&D cultures and strong relationships with industrial customers in Asia and globally.

Furthermore, specialized manufacturers like TOPTICA Photonics AG and QD Laser, Inc. are strengthening their positions through innovation in niche segments. TOPTICA’s emphasis on tunable and narrow-linewidth EELs caters to scientific research and metrology applications, whereas QD Laser’s development of wavelength-stabilized lasers addresses needs in gas sensing and medical diagnostics. Their targeted approaches allow them to compete effectively against larger players by offering differentiated, high-value solutions.

The competitive strategies observed across the market include aggressive patenting of new laser structures, pursuit of strategic mergers to gain complementary technologies, and expansion into emerging applications such as lidar for autonomous vehicles and quantum computing. As the market continues to grow, driven by 5G deployment and increasing automation, these companies are expected to further intensify their R&D efforts and global expansion initiatives to secure and enhance their market shares.

List of Key Edge Emitting Laser (EEL) Module Companies Profiled

- Coherent Corp. (U.S.)

- Lumentum Holdings Inc. (U.S.)

- Sony Corporation (Japan)

- ams OSRAM AG (Austria)

- Broadcom Inc. (U.S.)

- Anritsu Corporation (Japan)

- Jenoptik AG (Germany)

- Hamamatsu Photonics K.K. (Japan)

- MKS Instruments, Inc. (U.S.)

- MACOM Technology Solutions (U.S.)

- TOPTICA Photonics AG (Germany)

- Applied Optoelectronics, Inc. (U.S.)

- QD Laser, Inc. (Japan)

- Innolume GmbH (Germany)

- Photodigm, Inc. (U.S.)

Segment Analysis:

By Type

Distributed Feedback Laser Segment Dominates the Market Due to Superior Spectral Purity and High-Speed Data Transmission Capabilities

The market is segmented based on type into:

- Distributed Feedback Laser

- Fabry-Perot Laser

- Others

By Application

Optical Communication Segment Leads Due to Massive Deployment in Data Centers and 5G Infrastructure

The market is segmented based on application into:

- Optical Communication

- Industrial

- Medical

- Others

By Wavelength

1310nm and 1550nm Wavelengths Hold Significant Share Owing to Their Low Attenuation in Optical Fibers

The market is segmented based on wavelength into:

- 780nm – 980nm

- 1310nm

- 1550nm

- Others

By Power Output

Medium Power Output Modules (10mW – 100mW) are Highly Sought After for Balanced Performance in Various Applications

The market is segmented based on power output into:

- Low Power (<10mW)

- Medium Power (10mW – 100mW)

- High Power (>100mW)

Regional Analysis: Edge Emitting Laser (EEL) Module Market

Asia-Pacific

The Asia-Pacific region dominates the global EEL module market, accounting for over 45% of total consumption by volume. This leadership is primarily driven by China, which hosts the world’s largest manufacturing base for telecommunications equipment and consumer electronics. The massive rollout of 5G infrastructure, with China alone deploying over 2.3 million 5G base stations by the end of 2023, creates sustained demand for high-speed optical communication modules utilizing EELs. Japan and South Korea are also critical hubs, home to leading technology firms and advanced R&D centers focused on next-generation photonics. While cost-competitive manufacturing drives high-volume adoption, there is a simultaneous push toward innovation in industrial laser processing and medical applications. However, the market faces challenges from increasing competition and the gradual adoption of alternative technologies like VCSELs in some sensing applications.

North America

North America represents a high-value, innovation-driven market for EEL modules, characterized by significant investments in research and development and advanced manufacturing. The United States, in particular, is a key region due to its strong telecommunications sector, defense contracts, and leading medical device industry. Major cloud service providers and data centers are driving demand for high-performance optical transceivers to support ever-increasing data traffic. Furthermore, stringent regulatory standards in the medical field necessitate the use of highly reliable laser sources for diagnostic and therapeutic equipment. While the region’s manufacturing volume is lower than Asia-Pacific, its focus on high-power, high-precision industrial lasers and specialized applications results in a premium market segment. Companies here are heavily invested in developing new materials and designs to push the performance boundaries of EEL technology.

Europe

Europe maintains a strong position in the global EEL module market, distinguished by its emphasis on precision engineering, quality, and adherence to strict regulatory frameworks. The region is a leader in automotive LiDAR, industrial manufacturing, and scientific research applications, where the superior beam quality and power output of EELs are often required. Germany, with its robust industrial base, and the Benelux countries, with significant photonics research clusters, are central to the region’s activity. The European market is driven by innovation and a focus on developing environmentally sustainable and energy-efficient laser technologies. However, higher production costs compared to Asian manufacturers and complex supply chains present ongoing challenges for market players, pushing them to compete on performance and specialization rather than cost.

South America

The South American market for EEL modules is nascent but shows potential for gradual growth. Brazil and Argentina are the primary markets, where demand is largely linked to telecommunications infrastructure upgrades and the gradual modernization of industrial manufacturing sectors. The adoption of fiber-optic networks to improve internet connectivity is a key driver. However, economic volatility, currency fluctuations, and a reliance on imported technology components often hinder more rapid market expansion. The region currently has limited local manufacturing capability for advanced photonics, making it a net importer of EEL modules. Growth is expected to be steady but slower than in other regions, heavily dependent on economic stability and foreign investment in technology infrastructure.

Middle East & Africa

The EEL module market in the Middle East & Africa is in its early stages of development. Growth is concentrated in a few nations, notably Israel, a recognized global leader in technology and innovation with a strong defense sector that utilizes laser systems, and the UAE, which is investing in smart city and telecommunications infrastructure. Saudi Arabia’s Vision 2030 initiative is also expected to spur investment in advanced technologies, including those that incorporate photonics. Across the broader region, market development is constrained by limited local manufacturing, a focus on cost-effective solutions, and underdeveloped industrial and telecommunications infrastructure in many areas. Long-term growth is anticipated as digital transformation efforts gain momentum, but it will likely remain a niche market compared to other global regions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Edge Emitting Laser (EEL) Module markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Edge Emitting Laser (EEL) Module Market?

-> Edge Emitting Laser (EEL) Module Market was valued at 1960 million in 2024 and is projected to reach US$ 3451 million by 2032, at a CAGR of 9.5% during the forecast period.

Which key companies operate in Global Edge Emitting Laser (EEL) Module Market?

-> Key players include Coherent Corp., Lumentum, Sony, ams OSRAM, Broadcom, Anritsu, Jenoptik, Hamamatsu, MKS Instruments, and MACOM, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of 5G infrastructure, rising demand for high-speed data communication, increased adoption in industrial automation and medical applications, and advancements in optical sensing technologies.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing regional market, driven by substantial manufacturing and telecommunications infrastructure development in countries like China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of higher-power and more efficient EEL modules, integration with silicon photonics, increased use in LiDAR systems for autonomous vehicles, and growing applications in quantum computing and biomedical devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...