MARKET INSIGHTS

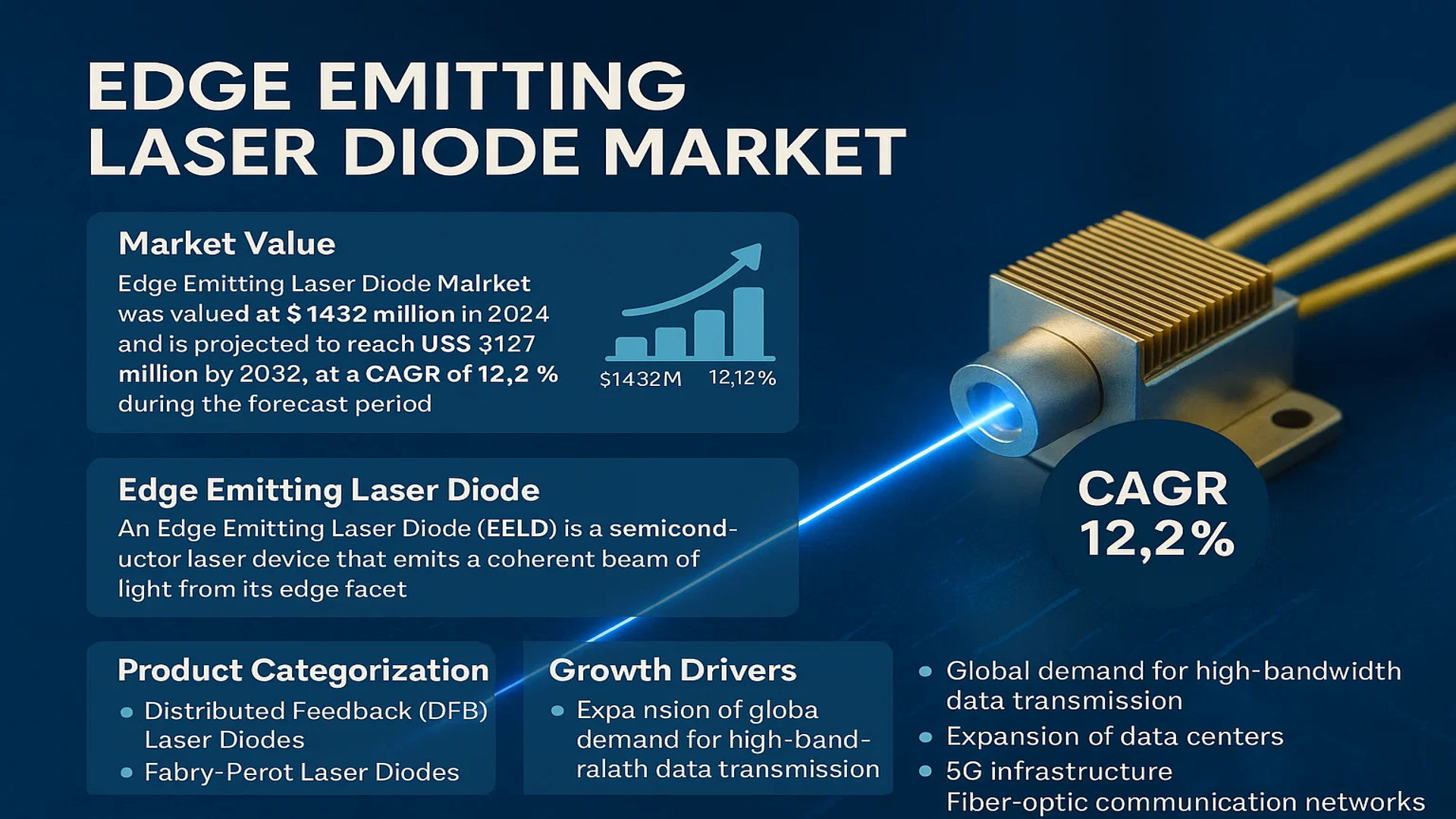

The global Edge Emitting Laser Diode Market was valued at 1432 million in 2024 and is projected to reach US$ 3127 million by 2032, at a CAGR of 12.2% during the forecast period.

An Edge Emitting Laser Diode (EELD) is a semiconductor laser device that emits a coherent beam of light from its edge facet. These components are fundamental to numerous high-technology applications because they offer high power, excellent beam quality, and high-speed modulation capabilities. EELDs are predominantly categorized into types such as Distributed Feedback (DFB) Laser Diodes and Fabry-Perot Laser Diodes, each serving distinct purposes in precision and high-data-rate systems.

The market’s robust growth is primarily fueled by the insatiable global demand for high-bandwidth data transmission, driven by the expansion of data centers, 5G infrastructure, and fiber-optic communication networks. The Communications application segment, which held a significant share of the market in 2024, is projected to grow at a CAGR of 10.24% and account for approximately 38.25% of the market by 2030. Furthermore, emerging applications in LiDAR for autonomous vehicles, industrial material processing, and advanced medical equipment are creating new, high-growth avenues for EELD adoption. The market is characterized by a competitive landscape where the top three players—Coherent Corp., Lumentum, and Sony—collectively held a revenue share of approximately 45% in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Speed Data Communication to Propel Market Growth

The global edge emitting laser diode market is experiencing robust growth driven by the escalating demand for high-speed data communication across datacom and telecom sectors. With data traffic projected to exceed 180 zettabytes annually by 2025, network infrastructure requires advanced optical components capable of supporting higher bandwidths and faster transmission rates. Edge emitting laser diodes, particularly distributed feedback (DFB) types, are essential in fiber optic communication systems for their superior modulation capabilities and wavelength stability. The proliferation of 5G networks, cloud computing services, and hyperscale data centers has accelerated adoption, with the communications segment expected to maintain a 38.25% market share by 2030. Major technology firms are investing over $200 billion annually in data center expansion, creating sustained demand for EELDs in transceivers and active optical cables.

Expansion of LiDAR and Sensing Applications to Accelerate Market Penetration

Emerging applications in light detection and ranging (LiDAR) systems and 3D sensing technologies represent significant growth opportunities for edge emitting laser diodes. The automotive LiDAR market is projected to grow at over 30% CAGR through 2030, driven by increasing adoption of autonomous driving technologies and advanced driver assistance systems (ADAS). EELDs provide the necessary high-power pulsed operation and beam quality required for long-range detection in automotive and industrial LiDAR systems. Additionally, the industrial automation sector utilizes EELDs in precision measurement, material processing, and quality control applications. The medical segment is witnessing increased adoption in surgical instruments, dermatology equipment, and diagnostic systems, with the global medical laser market expected to surpass $8 billion by 2027.

Technological Advancements and Product Innovation to Fuel Market Expansion

Continuous innovation in semiconductor laser technology is driving performance improvements and cost reductions in edge emitting laser diodes. Manufacturers are developing devices with higher output power, improved wall-plug efficiency, and enhanced reliability while reducing package sizes and power consumption. Recent advancements include the development of narrow linewidth EELDs for coherent communication systems and high-brightness diodes for material processing applications. The industry is witnessing a trend toward higher integration, with EELDs being combined with modulators, photodetectors, and passive components on single chips. These innovations are enabling new applications in quantum computing, optical atomic clocks, and precision metrology, expanding the addressable market beyond traditional communication applications.

MARKET CHALLENGES

Intense Price Pressure and Manufacturing Complexity to Constrain Profit Margins

The edge emitting laser diode market faces significant challenges from intense price competition and complex manufacturing processes. While the market is projected to reach $3127 million by 2032, manufacturers operate within slim profit margins due to pricing pressures from high-volume customers in the telecommunications and consumer electronics sectors. The fabrication of EELDs requires sophisticated epitaxial growth techniques, precise lithography, and complex packaging processes, contributing to high capital expenditure and production costs. The industry’s fragmentation, with the top three players holding approximately 45% market share, creates a competitive environment where price often outweighs performance considerations. Additionally, the need for customized solutions for different applications increases R&D expenses without guaranteed volume production, particularly affecting smaller manufacturers.

Other Challenges

Thermal Management and Reliability Concerns

Edge emitting laser diodes generate significant heat during operation, requiring advanced thermal management solutions to maintain performance and longevity. High-power applications particularly face challenges in heat dissipation, which can lead to wavelength drift, reduced efficiency, and accelerated aging. The reliability requirements for telecommunications applications exceed 100,000 hours of operation, necessitating robust packaging and precise control of operating conditions. These thermal challenges become more pronounced as power densities increase and package sizes decrease, creating engineering hurdles that increase development costs and time-to-market for new products.

Supply Chain Vulnerabilities and Material Sourcing

The global semiconductor supply chain disruptions have affected the availability of gallium arsenide and indium phosphide substrates essential for EELD manufacturing. Geopolitical tensions and trade restrictions have created uncertainties in material sourcing, particularly for specialty gases and epitaxial wafers. The industry’s reliance on a limited number of substrate suppliers creates vulnerability to price fluctuations and supply interruptions. These challenges are compounded by the increasing demand for compound semiconductors across multiple industries, straining production capacity and leading to extended lead times for critical materials.

MARKET RESTRAINTS

Competition from Alternative Technologies to Limit Market Growth Potential

Edge emitting laser diodes face increasing competition from alternative light source technologies, particularly vertical cavity surface emitting lasers (VCSELs) and silicon photonics. VCSELs offer advantages in manufacturing scalability, beam quality, and integration capabilities for short-reach data communication and sensing applications. The VCSEL market is growing at approximately 18% annually, capturing applications in smartphone facial recognition, automotive LiDAR, and data center interconnects. Silicon photonics technology is advancing rapidly, enabling the integration of optical components with electronic circuits on standard silicon substrates, potentially disrupting traditional III-V semiconductor laser markets. These competing technologies benefit from larger manufacturing scales and existing semiconductor infrastructure, creating price pressures and application erosion for traditional EELDs.

Technical Limitations in Emerging Applications to Restrict Market Expansion

While edge emitting laser diodes excel in many applications, they face technical limitations in emerging fields that require specific performance characteristics. The beam quality and divergence characteristics of EELDs present challenges in applications requiring circular symmetric beams or precise beam shaping. The need for external optics to correct astigmatism and elliptical beam profiles increases system complexity and cost compared to alternative technologies. Additionally, EELDs typically operate in specific wavelength ranges limited by available semiconductor materials, restricting their use in applications requiring wavelengths outside the 630-1700 nm range. These technical constraints become particularly relevant in biomedical applications, quantum technology, and certain industrial processing applications where alternative light sources may offer superior performance.

Regulatory Compliance and Standardization Requirements to Impede Innovation Pace

The edge emitting laser diode industry must navigate complex regulatory landscapes and standardization requirements that vary across regions and applications. Telecommunications equipment must comply with numerous international standards regarding performance, safety, and interoperability. Medical applications require approval from regulatory bodies, involving rigorous testing and documentation processes that can take several years and significant investment. Industrial lasers face safety regulations regarding emission classifications and protective measures. These compliance requirements create barriers to market entry and slow the introduction of new products, particularly for small and medium-sized enterprises lacking dedicated regulatory resources. The need to maintain multiple product versions for different regulatory environments increases inventory costs and complicates manufacturing planning.

MARKET OPPORTUNITIES

Integration with Photonic Integrated Circuits to Open New Application Frontiers

The integration of edge emitting laser diodes with photonic integrated circuits (PICs) represents a significant growth opportunity for the market. As the demand for higher data rates and more compact optical systems increases, the ability to combine EELDs with modulators, detectors, and passive components on single chips becomes increasingly valuable. The photonic integrated circuit market is projected to grow at over 20% CAGR, driven by demands from data centers, telecommunications, and sensing applications. Recent advancements in heterogeneous integration techniques enable the combination of III-V semiconductor lasers with silicon photonics platforms, creating highly functional and cost-effective solutions. This integration trend is particularly relevant for coherent communication systems, quantum information processing, and advanced sensing applications where size, power consumption, and performance are critical factors.

Expansion in Medical and Biotechnology Applications to Drive Specialty Market Growth

Edge emitting laser diodes are finding increasing applications in medical diagnostics, therapeutics, and biotechnology instrumentation, creating specialized market segments with higher margins. The global medical laser market continues to grow at approximately 12% annually, with applications ranging from surgical procedures and dermatology to flow cytometry and DNA sequencing. EELDs provide specific wavelengths required for various medical applications, including 810 nm for ophthalmology, 980 nm for surgical procedures, and 1470 nm for vascular treatments. The precision and reliability of EELDs make them suitable for minimally invasive procedures and diagnostic equipment requiring stable optical performance. Additionally, the life sciences sector utilizes EELDs in analytical instruments such as flow cytometers and DNA sequencers, where specific wavelength requirements and stability are critical for accurate results.

Emerging Applications in Quantum Technology and Advanced Computing to Create New Markets

The development of quantum technologies and advanced computing systems presents groundbreaking opportunities for edge emitting laser diodes. Quantum computing, quantum communication, and quantum sensing systems require highly stable, narrow-linewidth lasers with specific wavelength characteristics. EELDs are being developed for these applications with linewidths below 1 kHz and precise wavelength control capabilities. The quantum technology market is in its early stages but is projected to grow exponentially as applications mature. Additionally, optical computing and neuromorphic computing research utilizes EELDs for optical interconnects and signal processing. These emerging applications typically require lower volumes but higher performance specifications, creating opportunities for specialized manufacturers to develop premium products with advanced technical capabilities and higher profit margins.

EDGE EMITTING LASER DIODE MARKET TRENDS

Rising Demand in Data Communications to Drive Market Expansion

The relentless growth in data consumption, driven by cloud computing, streaming services, and the Internet of Things (IoT), is fundamentally increasing the need for high-speed optical communication networks. This demand directly fuels the adoption of edge-emitting laser diodes (EELDs), which are critical components in transceivers for data centers and telecommunications infrastructure. While the global market was valued at approximately 1432 million in 2024, projections indicate it will surge to over 3127 million by 2032, representing a compound annual growth rate of 12.2%. The communications industry segment alone is forecast to grow at a 10.24% CAGR and is expected to hold a dominant 38.25% market share by 2030. This growth is underpinned by the expansion of data center infrastructure by major web and cloud service providers, necessitating higher network capacity both within and between facilities. The inherent advantages of EELDs, including their high output power and ability to support high data rates, make them indispensable for meeting these escalating bandwidth requirements.

Other Trends

Technological Advancements in Integration and Efficiency

Manufacturers are heavily focused on enhancing the performance characteristics of EELDs to stay competitive. A key development trend involves the monolithic integration of EELDs with other optoelectronic components, such as optical modulators and photodetectors, on a single chip. This integration significantly improves device performance, reduces power consumption, and lowers overall system costs. Furthermore, relentless R&D efforts are aimed at achieving higher data transfer speeds and greater wall-plug efficiency to meet the stringent power budgets of modern data centers. Innovations in materials and fabrication processes are leading to more reliable and higher-performing devices, particularly in the widely used Distributed Feedback (DFB) laser diode segment, which is crucial for wavelength-stable applications in dense wavelength division multiplexing (DWDM) systems.

Emergence of New Application Areas Beyond Communications

While the communications sector remains the primary driver, new and diverse applications are emerging as significant growth vectors for the EELD market. Light Detection and Ranging (LiDAR) systems for autonomous vehicles and advanced driver-assistance systems (ADAS) represent a rapidly expanding frontier, requiring high-power, pulsed EELDs for accurate object detection and mapping. Similarly, the adoption of 3D sensing technologies in consumer electronics for facial recognition and augmented reality is creating substantial demand. The medical field also presents promising opportunities, with EELDs being integral to advanced surgical tools, diagnostic equipment, and therapeutic devices like photodynamic therapy. These burgeoning applications are poised to become potential killer markets in the medium to long term, diversifying revenue streams for manufacturers beyond the traditionally dominant telecom and datacom sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global Edge Emitting Laser Diode (EELD) market is highly fragmented and diverse, characterized by a mix of large, established corporations and specialized niche players. This fragmentation arises because each application segment—from telecommunications to medical devices—operates within its own specific supply chain and value chain dynamics. Consequently, manufacturers must strategically position themselves across different business models to effectively serve these varied markets.

Coherent Corp. and Lumentum Holdings Inc. are dominant forces in this space, collectively holding a significant portion of market revenue. In 2024, the top three players commanded approximately 45% of the global market share by revenue, underscoring a semi-consolidated structure at the very top. Their leadership is primarily driven by extensive product portfolios, deep expertise in photonics, and strong relationships with key customers in the datacom and telecom sectors, which are the largest application areas.

Meanwhile, companies like Sony and ams OSRAM also maintain considerable influence, particularly through their innovations in consumer electronics and industrial applications. These players are aggressively investing in R&D to develop higher-speed, more efficient EELDs that meet the escalating demands for data transmission capacity. Their growth is further propelled by strategic expansions and partnerships aimed at capturing emerging opportunities in LiDAR for autonomous vehicles and 3D sensing technologies.

Additionally, specialized firms such as Anritsu and Jenoptik are strengthening their market positions by focusing on high-precision applications in metrology and medical devices. These companies compete not only on technological superiority but also on reliability and compliance with stringent industry standards, which are critical in healthcare and scientific fields.

Looking forward, the competitive intensity is expected to increase as companies ramp up their investments in integrated photonics and pursue strategic mergers and acquisitions to enhance their technological capabilities and geographic reach. This dynamic environment ensures continuous innovation but also presents challenges related to pricing pressures and the need for constant technological advancement.

List of Key Edge Emitting Laser Diode Companies Profiled

- Coherent Corp. (U.S.)

- Lumentum Holdings Inc. (U.S.)

- Sony Group Corporation (Japan)

- ams OSRAM AG (Austria)

- Anritsu Corporation (Japan)

- Jenoptik AG (Germany)

- Hamamatsu Photonics K.K. (Japan)

- MKS Instruments, Inc. (U.S.)

- MACOM Technology Solutions Holdings, Inc. (U.S.)

- TOPTICA Photonics AG (Germany)

- Applied Optoelectronics, Inc. (U.S.)

- QD Laser, Inc. (Japan)

- Innolume GmbH (Germany)

- Photodigm, Inc. (U.S.)

- Modulight, Inc. (Finland)

Segment Analysis:

By Type

DFB Laser Diode Segment Commands Significant Market Share Due to Superior Performance in High-Speed Communications

The market is segmented based on type into:

- DFB Laser Diode

- Fabry Perot Laser Diode

- Other

By Application

Communications Segment Leads the Market Owing to Exponential Growth in Data Center and Telecom Infrastructure

The market is segmented based on application into:

- Communications

- Industrial

- Medical

- Others

By Wavelength

Near-Infrared Wavelengths Dominate the Market Driven by Widespread Use in Fiber Optic Communication Systems

The market is segmented based on wavelength into:

- Near-Infrared (NIR)

- Short-Wavelength Infrared (SWIR)

- Mid-Wavelength Infrared (MWIR)

- Long-Wavelength Infrared (LWIR)

By Power Output

High-Power Laser Diodes are Gaining Traction for Their Critical Role in Industrial Manufacturing and Medical Applications

The market is segmented based on power output into:

- Low Power

- Medium Power

- High Power

Regional Analysis: Edge Emitting Laser Diode Market

Asia-Pacific

The Asia-Pacific region dominates the global Edge Emitting Laser Diode market, accounting for over 45% of total consumption by volume. This leadership is driven by massive telecommunications infrastructure expansion, particularly in China, which houses the world’s largest fiber optic network with over 10 million kilometers of deployed fiber. China’s “Digital China” initiative and substantial 5G investments, alongside India’s rapidly growing data center and broadband projects, create sustained demand for high-speed DFB and FP laser diodes. Japan and South Korea remain innovation hubs, with companies like Sony and Hamamatsu driving R&D in advanced applications like LiDAR and precision medical equipment. While cost sensitivity keeps conventional EELDs prevalent, there is a marked shift toward higher-performance, energy-efficient components to support next-generation networks and emerging industrial automation.

North America

North America represents a high-value, technologically advanced market characterized by significant investments in data communication infrastructure and defense applications. The United States, in particular, is a major consumer, driven by web and cloud service giants expanding data center capacities. The region’s focus is on high-data-rate, low-power-consumption EELDs for 100G/400G transceivers. Defense and aerospace sectors also contribute substantially to demand, utilizing EELDs in rangefinding, targeting systems, and secure communications. Regulatory standards and corporate sustainability goals are pushing manufacturers toward more efficient and reliable laser diodes. Key players like Coherent Corp. and Lumentum have a strong presence, focusing on innovation and integration with other photonic components.

Europe

Europe’s market is shaped by stringent regulatory frameworks and a strong emphasis on research and development, particularly in the automotive, medical, and industrial sectors. The EU’s focus on green technology and energy efficiency drives demand for EELDs with lower power consumption and higher integration. Germany, the U.K., and France are central to regional growth, with automotive LiDAR and medical laser systems presenting significant opportunities. The region’s well-established telecommunications infrastructure is gradually upgrading to support higher bandwidths, though at a more measured pace than Asia-Pacific. Companies like ams OSRAM and Jenoptik are key innovators, focusing on custom solutions and high-reliability applications that meet rigorous EU standards.

South America

South America is an emerging market with growth potential primarily driven by gradual improvements in telecommunications infrastructure. Brazil and Argentina are the main contributors, with increasing investments in broadband and data center projects. However, economic volatility and budget constraints often delay large-scale deployments. The adoption of advanced EELDs is slower compared to other regions, with a focus on cost-effective solutions for basic communication needs. The medical and industrial sectors show nascent but growing interest, though the market remains challenged by limited local manufacturing and reliance on imports.

Middle East & Africa

The Middle East & Africa region is in the early stages of EELD market development. Growth is concentrated in more economically stable countries like Israel, Saudi Arabia, and the UAE, which are investing in smart city initiatives, telecommunications, and defense. Israel’s strong tech ecosystem supports innovation in medical and security applications of EELDs. However, the broader region faces challenges such as limited technological infrastructure, funding gaps, and political instability, which restrain widespread adoption. Long-term growth is anticipated as digital transformation efforts gain momentum, particularly in urban centers and special economic zones.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Edge Emitting Laser Diode markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Edge Emitting Laser Diode Market?

-> Edge Emitting Laser Diode Market was valued at 1432 million in 2024 and is projected to reach US$ 3127 million by 2032, at a CAGR of 12.2% during the forecast period.

Which key companies operate in Global Edge Emitting Laser Diode Market?

-> Key players include Coherent Corp., Lumentum, Sony, ams OSRAM, Anritsu, and Jenoptik, among others.

What are the key growth drivers?

-> Key growth drivers include expanding data center infrastructure, rising demand in optical communications, and emerging applications in LiDAR and 3D sensing.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include higher data transfer speeds, integration with other optoelectronic components, and lower power consumption designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...