MARKET INSIGHTS

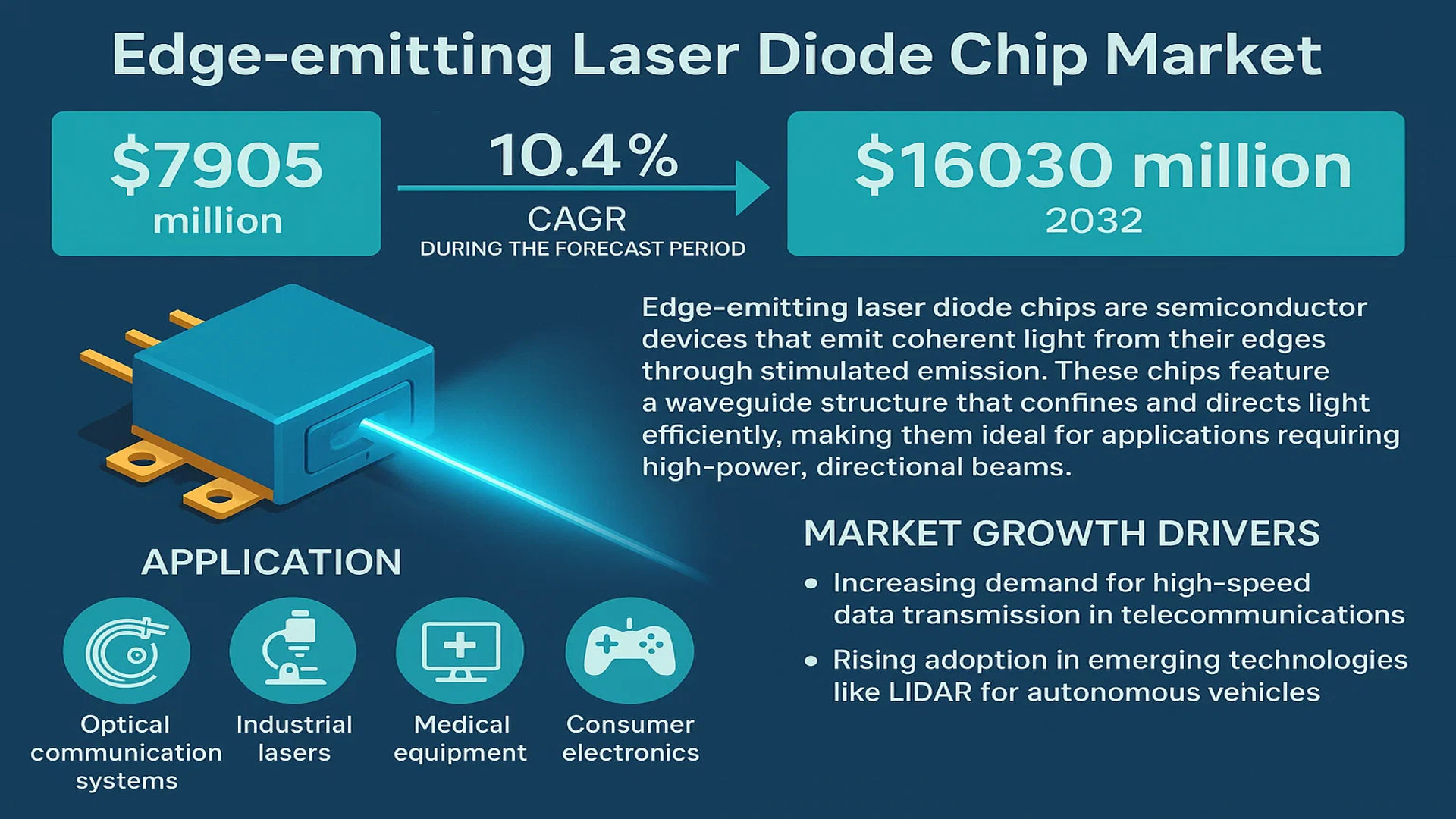

The global Edge-emitting Laser Diode Chip Market was valued at 7905 million in 2024 and is projected to reach US$ 16030 million by 2032, at a CAGR of 10.4% during the forecast period.

Edge-emitting laser diode chips are semiconductor devices that emit coherent light from their edges through stimulated emission. These chips feature a waveguide structure that confines and directs light efficiently, making them ideal for applications requiring high-power, directional beams. They are widely used in optical communication systems, industrial lasers, medical equipment, and consumer electronics.

The market growth is driven by increasing demand for high-speed data transmission in telecommunications and rising adoption in emerging technologies like LiDAR for autonomous vehicles. Furthermore, advancements in 5G infrastructure and data centers are accelerating market expansion. Key players like Lumentum, Coherent (II-VI), and Broadcom dominate the competitive landscape with continuous innovations in chip efficiency and wavelength ranges.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Speed Optical Communication Solutions Accelerates Market Growth

The global edge-emitting laser diode chip market is experiencing significant growth due to the exponential rise in data traffic and the subsequent need for high-bandwidth optical communication networks. As 5G deployment expands globally, the demand for 25G/100G/400G optical modules utilizing edge-emitting lasers has surged by over 35% since 2022. These chips enable faster data transfer rates with lower power consumption compared to alternatives, making them indispensable in data centers and telecom infrastructure. Recent technological advancements in distributed feedback (DFB) and electro-absorption modulated laser (EML) chips have further enhanced their performance in wavelength division multiplexing (WDM) applications.

Expansion of Data Centers Worldwide Creates Sustained Demand

The proliferation of hyperscale data centers continues to drive substantial demand for edge-emitting laser diode chips, particularly in North America and Asia-Pacific regions where cloud computing investments have grown by over 25% annually. These chips serve as critical components in optical transceivers used for server-to-server communication, with the EML chip segment accounting for nearly 45% of data center laser diode deployments in 2024. Major cloud service providers are increasingly adopting these solutions to support AI/ML workloads that require ultra-low latency optical interconnects.

Automotive LiDAR Applications Present New Growth Frontier

Emerging applications in autonomous vehicle technology are creating new opportunities for edge-emitting laser diodes, particularly in the 905nm wavelength range for LiDAR systems. With the automotive LiDAR market projected to grow at 28% CAGR through 2030, manufacturers are investing heavily in chip designs that offer higher peak power and temperature stability. This segment currently represents about 12% of total edge-emitting laser diode chip sales but is expected to nearly triple in market share by 2032 as autonomous driving adoption accelerates.

MARKET RESTRAINTS

Transition to Silicon Photonics Creates Competitive Pressure

The edge-emitting laser diode market faces growing competition from silicon photonics solutions that promise better integration with CMOS processes. While edge-emitting lasers currently maintain performance advantages in power output and spectral purity, the industry is witnessing increasing adoption of hybrid integration approaches that combine both technologies. This transition requires significant R&D investments from traditional laser diode manufacturers to maintain their competitive edge, particularly in cost-sensitive applications where silicon photonics solutions can offer 20-30% price advantages.

Complex Manufacturing Processes Limit Yield Improvements

The fabrication of edge-emitting laser diodes involves precision epitaxial growth and sophisticated wafer processing steps that contribute to lower manufacturing yields compared to simpler optoelectronic devices. The typical yield for high-performance EML chips remains below 65% due to stringent performance requirements in wavelength accuracy and linewidth characteristics. Additionally, the industry faces ongoing challenges in III-V material defect reduction and thermal management at higher power densities, which constrain both performance improvements and production scalability.

Supply Chain Vulnerabilities Impact Market Stability

The market continues to experience supply chain disruptions for critical raw materials such as gallium arsenide (GaAs) and indium phosphide (InP) substrates. Geopolitical factors have caused price fluctuations exceeding 40% for some specialized semiconductor materials since 2022. Manufacturers are responding by diversifying supplier networks and developing alternative material systems, but these transitions require lengthy qualification processes that temporarily constrain production capacity and new product introductions.

MARKET CHALLENGES

Thermal Management Constraints Limit Performance Scaling

As data rates push beyond 1.6Tbps in optical networks, edge-emitting lasers face increasing thermal challenges that degrade performance reliability. The current generation of high-speed EML chips experiences junction temperature rises exceeding 15°C under continuous operation, leading to wavelength drift and reduced modulation bandwidth. Advanced packaging solutions incorporating micro-TEC coolers can mitigate these issues but add 20-25% to overall component costs, creating difficult trade-offs between performance and commercial viability.

Standardization Gaps Hinder Seamless Integration

The industry currently lacks uniform standards for edge-emitting laser chip interfaces and performance specifications across different applications. This fragmentation requires manufacturers to maintain multiple product variants, increasing inventory costs and lengthening design cycles for system integrators. Recent efforts by industry consortia to establish common electrical and optical interfaces have made progress but remain incomplete, particularly for emerging applications in co-packaged optics architectures.

Intellectual Property Disputes Create Market Uncertainties

The market has witnessed increased patent litigation surrounding edge-emitting laser designs and manufacturing processes, with over 45 new IP cases filed globally in the past 18 months. These disputes primarily involve epitaxial layer structures and grating designs that determine key performance characteristics. While such challenges typically resolve through cross-licensing agreements, they temporarily disrupt product roadmaps and create uncertainties for customers evaluating long-term supplier commitments.

MARKET OPPORTUNITIES

Emerging Quantum Technology Applications Open New Markets

The development of quantum computing and communication systems is creating specialized demand for ultra-stable edge-emitting lasers with exceptional spectral purity. Applications in atomic clocks, quantum memory interfaces, and photonic quantum networks require laser chips with sub-MHz linewidths and precise wavelength control – specifications that align with recent advancements in DFB laser technology. This niche segment currently represents less than 5% of market volume but is growing at over 60% annually as quantum technology transitions from research to commercialization.

Medical and Biomedical Applications Drive Product Innovation

The healthcare sector is increasingly adopting edge-emitting lasers for precision diagnostic and therapeutic applications ranging from optical coherence tomography to minimally invasive surgical tools. Medical-grade laser chips require specialized certifications and reliability standards but command premium pricing with gross margins exceeding 60% in many cases. Recent developments in visible wavelength edge-emitting lasers (particularly in the 450-650nm range) are enabling new applications in fluorescence imaging and photodynamic therapy, with the medical laser diode market projected to grow at 18% CAGR through 2032.

Integrated Photonic Systems Create Demand for Custom Solutions

The growing adoption of photonic integrated circuits (PICs) is driving demand for application-specific laser diode chips designed for direct integration with silicon photonics and other hybrid platforms. These solutions require close collaboration between laser manufacturers and system integrators to optimize parameters such as beam shape, polarization, and coupling efficiency. The opportunity is particularly significant in optical sensing applications where customized edge-emitting lasers can provide performance advantages over generic alternatives, with some integrated photonic systems incorporating multiple laser chips operating at different wavelengths for multi-parameter sensing.

EDGE-EMITTING LASER DIODE CHIP MARKET TRENDS

Demand for High-Speed Data Transmission Fuels Market Expansion

The global edge-emitting laser diode chip market is witnessing significant growth due to the escalating demand for high-speed data transmission in telecommunications and data centers. With the rapid adoption of 5G technology and cloud computing, the need for efficient optical communication solutions has surged. EML (Electro-absorption Modulated Laser) chips, in particular, are gaining traction for their ability to support data rates exceeding 100 Gbps, making them indispensable in modern optical networks. The growing deployment of fiber-optic infrastructure across North America and Asia-Pacific is expected to drive the market further, with revenue projected to reach $16.03 billion by 2032.

Other Trends

Miniaturization and Energy Efficiency

The trend toward miniaturization in semiconductor technology is influencing the development of compact and energy-efficient edge-emitting laser diode chips. Advanced fabrication techniques, such as epitaxial growth and quantum well structures, are enabling higher output power with reduced energy consumption. This is particularly beneficial for applications in wearable devices, autonomous vehicles, and IoT sensors, where power efficiency is critical. Manufacturers are also focusing on reducing thermal noise and improving thermal management to enhance device longevity.

Industry Consolidation and Strategic Collaborations

The competitive landscape of the edge-emitting laser diode chip market is evolving through mergers, acquisitions, and strategic partnerships. Leading players such as Lumentum and Coherent (II-VI) are expanding their portfolios through acquisitions to strengthen their technological capabilities. Additionally, collaborations between semiconductor manufacturers and optical communication providers are fostering innovation in wavelength-division multiplexing (WDM) technologies. These efforts are expected to address the increasing demand for high-bandwidth applications while maintaining cost efficiency.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovations and Partnerships Drive Market Leadership

The global edge-emitting laser diode chip market is characterized by a mix of established leaders and emerging innovators, all competing to enhance their technological capabilities and market reach. As the demand for high-performance lasers in telecommunications, industrial, and consumer applications grows, companies are aggressively expanding their product portfolios through R&D investments and strategic acquisitions.

Lumentum and Coherent (II-VI) currently dominate the market, collectively holding a significant revenue share. Their leadership stems from vertical integration capabilities and strong intellectual property portfolios in semiconductor lasers. Both companies have recently introduced higher-power chips for 5G optical networks, aligning with the global push for faster data transmission.

Meanwhile, Broadcom and Sumitomo Electric are gaining traction through specialized EML (Electro-absorption Modulated Laser) solutions for datacenter applications. Their success underscores the importance of application-specific designs in this fragmented market segment. The growing adoption of cloud computing and AI infrastructure has particularly benefited these players in recent quarters.

Smaller but technologically agile firms like AdTech Optics and Inphenix are carving out niches in medical and scientific laser systems. Their ability to deliver custom wavelength solutions has attracted partnerships with biomedical device manufacturers. Meanwhile, Nanoplus continues to lead in ultra-narrow linewidth lasers for gas sensing applications – a segment projected to grow at 12% CAGR through 2032.

List of Key Edge-emitting Laser Diode Chip Companies Profiled

- Lumentum Holdings Inc. (U.S.)

- Coherent, Inc. (II-VI) (U.S.)

- Broadcom Inc. (U.S.)

- Sumitomo Electric Industries (Japan)

- Applied Optoelectronics (U.S.)

- Furukawa Electric Co., Ltd. (Japan)

- MACOM Technology Solutions (U.S.)

- AdTech Optics (U.S.)

- Inphenix (U.S.)

- nanoplus Nanosystems and Technologies GmbH (Germany)

- RPMC Lasers (U.S.)

- Frankfurt Laser Company (Germany)

The competitive landscape continues evolving with increasing M&A activity, particularly as larger players seek to acquire specialized photonics capabilities. Recent years have seen major corporations establish dedicated laser divisions through acquisitions, signaling this technology’s strategic importance across multiple industries. This consolidation trend is expected to accelerate as performance requirements become more demanding across applications from LiDAR to quantum computing.

Geographically, Western companies currently lead in R&D spending with about 65% of total industry investment, while Asian manufacturers are rapidly closing the gap through government-supported semiconductor initiatives. This East-West technology race adds another dynamic to an already complex competitive environment where technical superiority and manufacturing scale both determine market positioning.

Segment Analysis:

By Type

EML Chips Segment Dominates the Market Due to High Demand in High-Speed Optical Communication

The market is segmented based on type into:

- EML Chips

- Subtypes: C-band, L-band, and others

- DFB Chips

- Subtypes: Single-mode, Multi-mode, and others

- FP Chips

- Subtypes: High-power, Low-power, and others

- Others

By Application

Optical Communication Segment Leads Due to Rising Deployment of 5G and Data Center Networks

The market is segmented based on application into:

- Optical Communication

- Subtypes: Telecommunication, Data centers, and others

- Optical Storage

- Subtypes: Blu-ray, DVD, and others

- Industrial

- Subtypes: Material processing, Sensing, and others

- Medical

- Subtypes: Diagnostics, Surgery, and others

- Others

By End User

Telecommunication Providers Account for Largest Share Due to Network Infrastructure Expansion

The market is segmented based on end user into:

- Telecommunication Providers

- Data Center Operators

- Medical Equipment Manufacturers

- Industrial Automation Companies

- Consumer Electronics Manufacturers

- Others

Regional Analysis: Edge-emitting Laser Diode Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global edge-emitting laser diode chip market, accounting for the largest revenue share in 2024. This leadership position stems from rapid expansion in optical communication networks, particularly in China, Japan, and South Korea. China alone contributes over 40% of regional demand, driven by massive investments in 5G infrastructure and data centers. Japan maintains technological leadership in precision manufacturing, while South Korea’s semiconductor industry fuels demand for high-performance laser chips. The region benefits from strong government support for photonics research and an established electronics manufacturing ecosystem. However, intense price competition among regional players and strict export controls on advanced technologies present ongoing challenges.

North America

North America represents the second-largest market for edge-emitting laser diode chips, with the United States generating approximately 30% of global revenues in this segment. The market thrives on cutting-edge R&D activities in Silicon Valley and Boston’s photonics cluster, supported by defense and aerospace applications. The region shows particular strength in high-power and specialty laser diodes used in medical devices and industrial applications. While the market faces pressure from overseas competitors on price points, superior product performance and intellectual property protection help maintain North America’s competitive edge. Recent CHIPS Act funding allocations are expected to further strengthen domestic semiconductor manufacturing capabilities.

Europe

Europe maintains a strong position in the edge-emitting laser diode market through technological specialization and quality leadership. Germany’s photonics industry cluster accounts for nearly half of regional demand, with particular strength in automotive LiDAR and industrial sensing applications. The region benefits from Horizon Europe research funding and collaborative projects between universities and manufacturers. However, higher production costs compared to Asian competitors and complex regulatory environments create barriers to market growth. European manufacturers increasingly focus on niche applications like quantum technologies and biomedical instrumentation to maintain value-added differentiation.

Middle East & Africa

The MEA region represents the fastest-growing market for edge-emitting laser diode chips, albeit from a smaller base. Growth drivers include expanding fiber optic networks in Gulf Cooperation Council countries and increasing adoption in oilfield monitoring systems. Israel’s established photonics industry contributes specialized military and medical laser solutions. While the market shows promising potential, limited local manufacturing capabilities and reliance on imports constrain near-term expansion. Regional players are investing in assembly and testing facilities to gradually move up the value chain.

South America

South America remains a developing market for edge-emitting laser diode chips, with Brazil representing over 60% of regional demand. Primary applications include telecommunications infrastructure and scientific research equipment. The market faces challenges from economic volatility and limited local R&D investment. However, growing partnerships with global technology providers and increasing digitalization initiatives present opportunities for gradual market expansion over the forecast period.

Report Scope

This market research report provides a comprehensive analysis of the global Edge-emitting Laser Diode Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 7,905 million in 2024 and is projected to reach USD 16,030 million by 2032, growing at a CAGR of 10.4%.

- Segmentation Analysis: Detailed breakdown by product type (EML Chips, DFB Chips, FP Chips), application (Optical Communication, Optical Storage, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K.), Asia-Pacific (China, Japan, South Korea), and other regions.

- Competitive Landscape: Profiles of leading market participants including Lumentum, Coherent (II-VI), Broadcom, Sumitomo, and Applied Optoelectronics, covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies in laser diode fabrication, integration with optical communication systems, and advancements in waveguide structures.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for high-speed optical communication, along with challenges like supply chain constraints and manufacturing complexities.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, optical component suppliers, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs both primary and secondary research methodologies, including expert interviews and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Edge-emitting Laser Diode Chip Market?

-> Edge-emitting Laser Diode Chip Market was valued at 7905 million in 2024 and is projected to reach US$ 16030 million by 2032, at a CAGR of 10.4% during the forecast period.

Which key companies operate in this market?

-> Key players include Lumentum, Coherent (II-VI), Broadcom, Sumitomo, Applied Optoelectronics, Furukawa Electric, and Macom, among others.

What are the key growth drivers?

-> Growth is driven by increasing demand for optical communication systems, expansion of 5G networks, and rising adoption in industrial applications.

Which region dominates the market?

-> Asia-Pacific leads in market share, with North America and Europe being significant markets for high-end applications.

What are the emerging trends?

-> Emerging trends include development of higher-power chips, integration with silicon photonics, and advancements in wavelength-stabilized lasers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...