Edge Computing Processor Market Insights

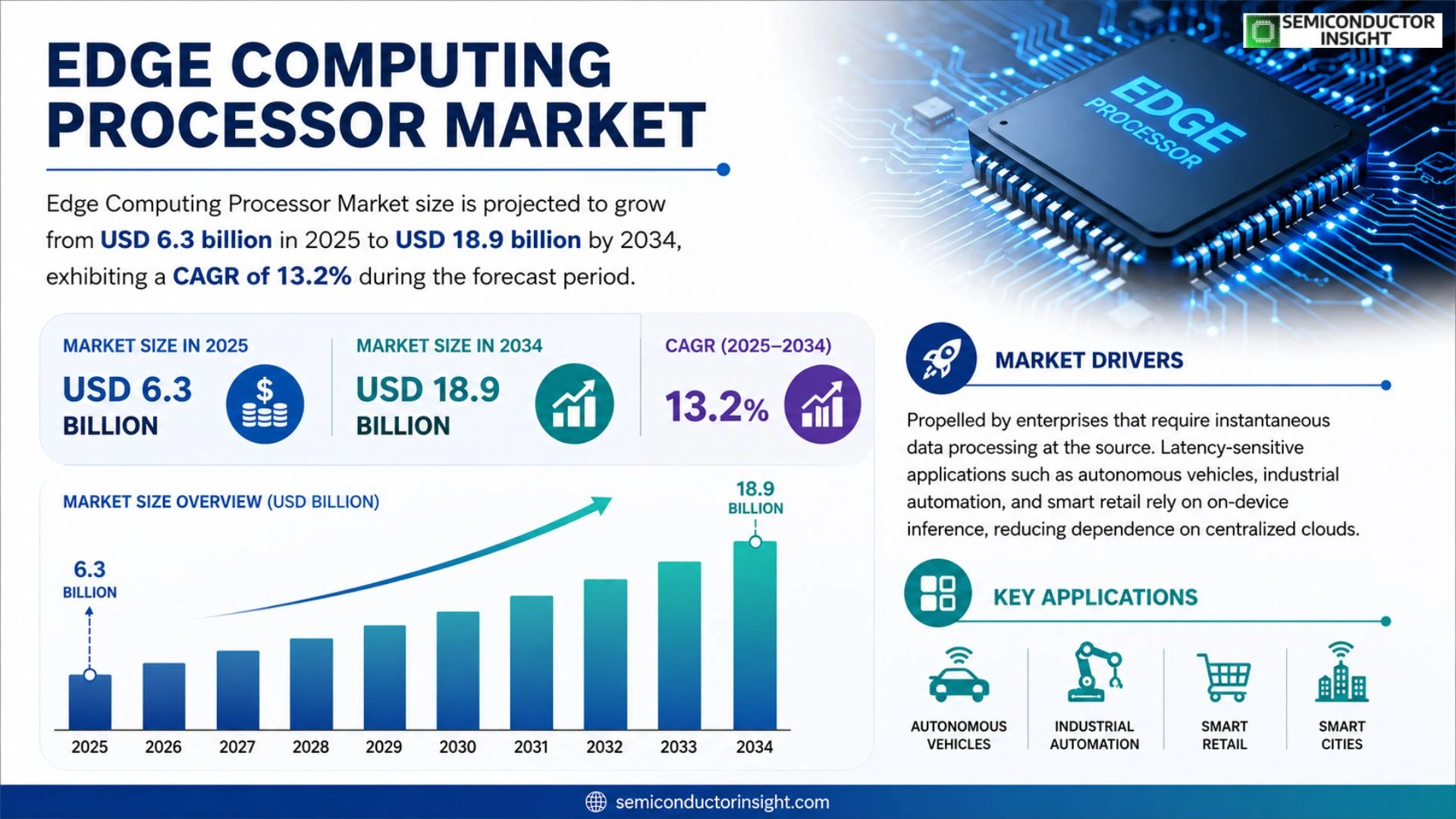

Global Edge Computing Processor Market size was valued at USD 6.0 billion in 2025. The market is projected to grow from USD 6.3 billion in 2025 to USD 18.9 billion by 2034, exhibiting a CAGR of 13.2% during the forecast period.

Edge computing processors are purpose‑built semiconductor devices that enable real‑time analytics and AI inference close to data sources, thereby reducing latency, bandwidth consumption and energy use compared with centralized cloud processing.

The market is accelerating because of surging IoT deployments, rising demand for autonomous systems and regulatory pressure for data sovereignty; meanwhile leading vendors such as NVIDIA, Qualcomm, Intel and Arm are expanding their portfolios through strategic alliances,e.g., Qualcomm’s partnership with Samsung announced in February 2024,to meet diverse workload requirements.

MARKET DRIVERS

Growing Demand for Real‑Time Analytics

Edge Computing Processor Market is being propelled by enterprises that require instantaneous data processing at the source. Latency-sensitive applications such as autonomous vehicles, industrial automation, and smart retail rely on on‑device inference, reducing dependence on centralized clouds. Analysts estimate that by 2030, more than 45% of enterprise workloads will be executed at the edge, driving processor adoption.

Advancements in Low‑Power Chip Design

Recent breakthroughs in sub‑7 nm process nodes and heterogeneous integration have enabled processors that deliver high compute density while consuming less than 2 W per unit. These efficiencies lower the total cost of ownership for edge deployments in remote locations, where power availability is limited. Consequently, OEMs are accelerating the rollout of edge gateways equipped with such processors.

➤ “Edge‑optimized processors are expected to capture 30% of new IoT device shipments by 2026, outpacing traditional CPUs.”

In parallel, the proliferation of 5G networks provides the bandwidth needed for massive edge ecosystems. The combined effect of ultra‑low latency connectivity and specialized processors fuels a virtuous cycle that expands Edge Computing Processor Market across telecom, manufacturing, and healthcare sectors.

MARKET CHALLENGES

Complexity of Software Stack Integration

Developers must harmonize diverse operating systems, middleware, and AI frameworks to fully exploit edge processors. This integration complexity raises development costs and prolongs time‑to‑market, especially for small‑and‑medium enterprises lacking dedicated engineering resources.

Other Challenges

Security Concerns

Deploying compute resources outside controlled data‑center environments exposes devices to physical tampering and cyber attacks. Robust secure boot, enclave technologies, and remote attestation are required, increasing silicon and firmware expenses.

MARKET RESTRAINTS

High Initial Capital Expenditure

While edge processors lower operational costs over time, the upfront investment for ruggedized hardware, custom board design, and qualification testing remains substantial. Enterprises in price‑sensitive markets often defer migration, opting for legacy cloud solutions.

Furthermore, the fragmented nature of standards across different industries hampers economies of scale. Without a unified ecosystem, manufacturers must produce multiple variants to meet specific regulatory and performance requirements, constraining broader market adoption.

MARKET OPPORTUNITIES

Emergence of AI‑Accelerated Edge Processors

Integrating dedicated AI accelerators into edge CPUs opens new revenue streams in computer‑vision, predictive maintenance, and localized speech recognition. Companies that bundle inference engines with power‑efficient silicon can secure premium contracts in sectors such as autonomous logistics and remote health monitoring.

Another untapped avenue lies in modular edge platforms that support plug‑and‑play processor upgrades. This approach reduces lifecycle costs and appeals to operators seeking future‑proof solutions, positioning them to capture a larger share of Edge Computing Processor Market as technology evolves.

Edge Computing Processor Market Trends

Rising Demand for Real‑Time Edge Analytics

Edge Computing Processor Market is being reshaped by the accelerating adoption of Internet of Things (IoT) devices across manufacturing, logistics, and smart‑city projects. As data sources multiply at the network edge, processors that can deliver AI inference with sub‑millisecond latency become essential. Vendors are prioritizing architectures that combine low power consumption with heterogeneous compute units, allowing real‑time analytics to run locally while preserving bandwidth for critical traffic. This shift reduces reliance on centralized cloud resources and aligns with emerging data‑sovereignty regulations that require processing within specific jurisdictions. In addition, built‑in security features such as hardware root of trust are becoming standard, strengthening the protection of edge workloads. The ability to process video streams for augmented reality and remote‑assistance applications further amplifies the strategic importance of edge processors.

Other Trends

AI‑Optimized Edge Chips

AI‑optimized edge chips are emerging as a distinct sub‑segment. By integrating dedicated neural‑network accelerators, these processors support on‑device model execution for applications such as predictive maintenance and autonomous navigation. Companies are investing in silicon‑level optimizations that minimize inference latency and energy draw, which is crucial for battery‑operated edge nodes. The trend is reinforced by growing developer ecosystems offering pre‑trained models that can be fine‑tuned for edge workloads, speeding time‑to‑market for new services. Multi‑tenant edge platforms are also gaining traction, enabling service providers to host diverse AI workloads on shared hardware while maintaining isolation and performance guarantees.

Strategic Alliances and Portf olio Expansion

Leading suppliers are strengthening their market position through strategic alliances and portfolio diversification. Qualcomm’s collaboration with Samsung to embed next‑generation edge processors in mobile platforms exemplifies a move toward tighter hardware‑software integration. Intel and Arm are extending reference designs that simplify customer adoption of heterogeneous compute blocks. Meanwhile, NVIDIA is leveraging its GPU expertise to deliver edge‑ready AI acceleration kits that address high‑performance workloads in autonomous vehicles and industrial robotics. These partnerships accelerate ecosystem maturity, lower entry barriers for OEMs, and support compliance with regional data‑handling regulations. Sustainability considerations are also prompting designers to adopt ultra‑low‑power processes, further broadening the appeal of edge computing solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Edge Computing Processor Market – Competitive Overview

Edge Computing Processor Market is dominated by a handful of large semiconductor firms that command extensive IP portfolios, advanced manufacturing capabilities, and deep AI inference expertise. NVIDIA leads the segment with its Jetson series, delivering high‑performance GPU‑accelerated cores that are widely adopted in autonomous vehicles and industrial IoT gateways. Qualcomm follows with its Snapdragon 600 Series Edge AI platform, leveraging 5G connectivity and low‑power designs, while Intel’s Xeon E‑Series and Atom based edge processors provide a flexible x86 ecosystem for data‑center‑to‑edge workloads. Arm’s ecosystem of licensable CPU cores underpins many heterogeneous solutions, enabling rapid customization for latency‑critical applications. The market structure therefore resembles an oligopolistic tier at the top, complemented by a vibrant layer of niche innovators that address specific verticals such as wearables, automotive safety, and telecom edge nodes.

Beyond the marquee vendors, several specialized players enrich the competitive landscape with differentiated technologies. MediaTek supplies cost‑effective AI‑on‑chip solutions for consumer‑grade edge devices, while Texas Instruments offers robust analog‑centric System‑on‑Chip (SoC) families for industrial sensing. AMD, after acquiring Xilinx, brings adaptive FPGA‑based edge compute that excels in reconfigurable workloads. Samsung Electronics contributes Exynos‑based edge processors with integrated 5G modems. Marvell’s OCTEON™ line targets high‑throughput networking edge functions, and NXP delivers ultra‑low‑power Arm‑based MCUs for automotive gateways. Additional contributors include Renesas, Huawei HiSilicon, SiFive (RISC‑V cores), Green Hills Software (safe‑RTOS‑enabled processors), and Cadence (IP‑centric design platforms). These companies collectively ensure that customers can select processors aligned with performance, power, security, and regulatory requirements across the rapidly expanding edge ecosystem.

List of Key Edge Computing Processor Companies Profiled

- NVIDIA

- Qualcomm

- Intel

- Arm

- MediaTek

- Texas Instruments

- AMD

- Samsung Electronics

- Marvell Technology Group

- NXP Semiconductors

- Renesas Electronics

- Huawei HiSilicon

- SiFive

- Green Hills Software

- Cadence Design Systems

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ARM‑based CPUs dominate due to:

|

| By Application |

|

Industrial IoT stands out because:

|

| By End User |

|

Telecommunications lead the adoption curve as they:

|

| By Architecture |

|

System‑on‑Module is favored because:

|

| By Integration Level |

|

Integrated Edge Nodes gain traction as they:

|

Regional Analysis: North America

North America

The industrial sector in North America is a major driver of edge computing processor demand. Manufacturers are deploying edge devices for real-time monitoring, predictive maintenance, and process optimization. The need for reliable and secure edge processing solutions in factories and industrial facilities is increasing rapidly.

The healthcare industry in North America is leveraging edge computing processors for applications such as remote patient monitoring, medical imaging analysis, and real-time diagnostics. The ability to process data locally enables faster decision-making and improved patient outcomes.

Retailers in North America are adopting edge computing to enhance the customer experience, optimize inventory management, and improve security. Edge devices enable real-time analytics of customer behavior, personalized marketing, and fraud detection.

North American cities are implementing edge computing solutions to improve public safety, traffic management, and environmental monitoring. Deploying edge devices at various locations enables real-time data collection and analysis for better urban planning and resource management.

Europe

Europe represents the second-largest market for edge computing processors. The region is witnessing growing adoption across various sectors, including manufacturing, automotive, and energy. Stringent data privacy regulations, such as GDPR, are influencing the deployment of edge solutions, with a focus on data processing within geographical boundaries. The automotive industry in Europe is a key driver, with increasing demand for autonomous driving capabilities and connected car services requiring low-latency edge processing.

Asia-Pacific

Asia-Pacific is expected to be the fastest-growing market for edge computing processors due to rapid industrialization, increasing digitalization, and government initiatives promoting technological advancements. China, Japan, and South Korea are key markets within the region, driven by strong manufacturing sectors and a growing demand for smart infrastructure. The proliferation of IoT devices and the increasing need for real-time data processing are also contributing to market growth in Asia-Pacific.

South America

South America is an emerging market for edge computing processors with significant potential for growth. The region’s expanding industrial sector, particularly in areas like agriculture and mining, is driving demand for edge solutions. Increasing internet penetration and the growing adoption of IoT technologies are also contributing to market expansion. However, challenges such as limited infrastructure and high upfront costs may hinder the pace of adoption.

Middle East & Africa

The Middle East and Africa represent a promising, albeit nascent, market for edge computing processors. Investments in smart cities, industrial modernization, and digital transformation are expected to drive future growth. The region’s focus on infrastructure development and the increasing adoption of 5G technologies will create opportunities for edge computing deployments. The energy sector in the Middle East is a key driver, with applications in oil and gas exploration, monitoring, and optimization.

Report Scope

This market research report provides a comprehensive analysis of the Edge Computing Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Edge Computing Processor Market?

-> Global Edge Computing Processor Market size was valued at USD 6.0 billion in 2025. The market is projected to grow from USD 6.3 billion in 2025 to USD 18.9 billion by 2034, exhibiting a CAGR of 13.2%

Which key companies operate Edge Computing Processor Market?

-> Key players include NVIDIA, Qualcomm, Intel, and Arm, among others.

What are the key growth drivers?

-> Key growth drivers include surging IoT deployments, rising demand for autonomous systems, and regulatory pressure for data sovereignty.

Which region dominates the market?

-> The market exhibits strong activity across North America, Europe, and Asia‑Pacific, with no single region monopolizing demand.

What are the emerging trends?

-> Emerging trends include edge AI inference, real‑time analytics close to the data source, and tighter integration of semiconductor design with IoT and autonomous workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...