Edge AI vision processor chip with stereo depth engine Market Insights

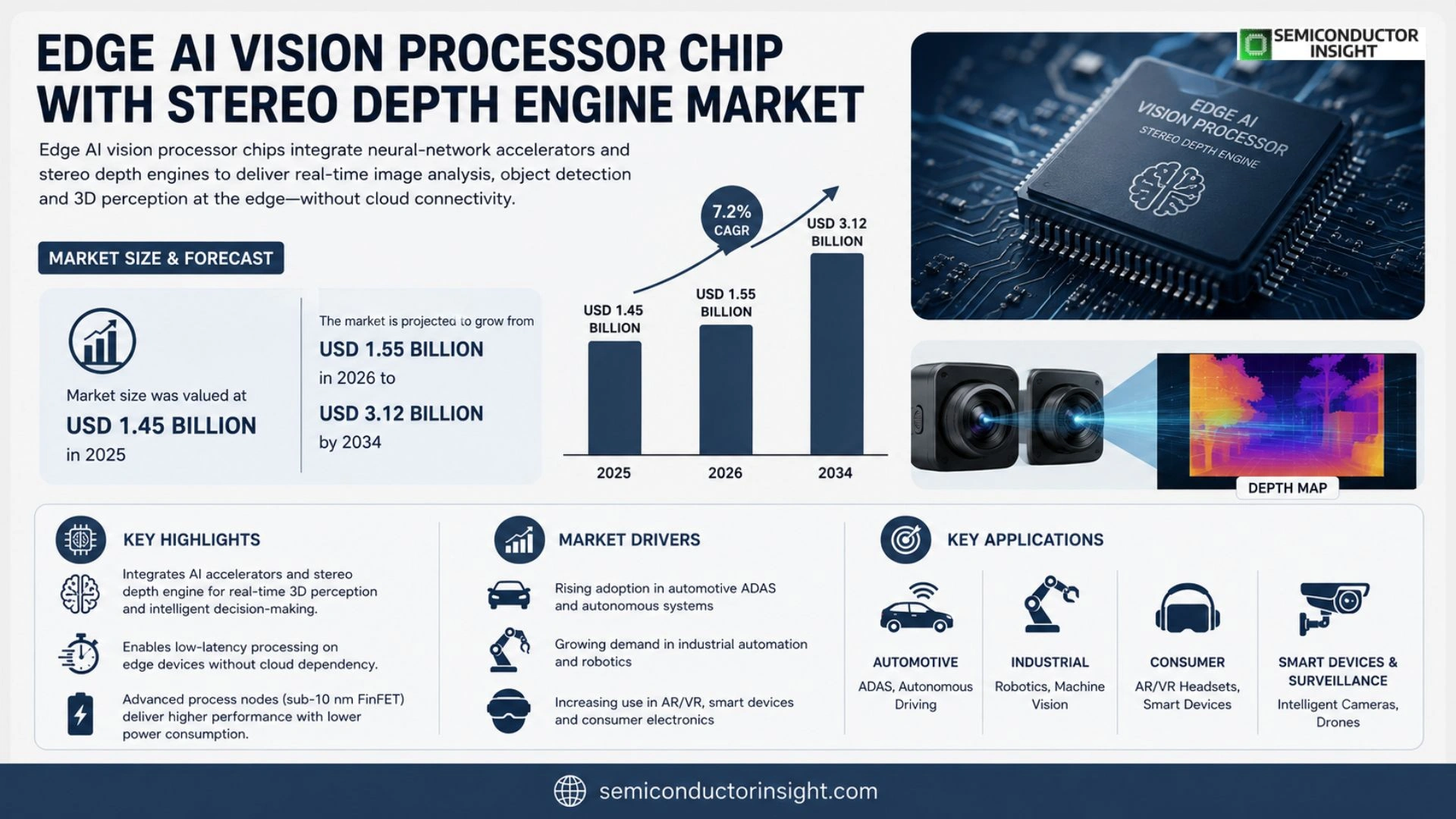

Global Edge AI vision processor chip with stereo depth engine market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period.

Edge AI vision processor chips integrate neural‑network accelerators directly on silicon, enabling real‑time image analysis, object detection and stereo depth perception without reliance on cloud connectivity. The built‑in stereo depth engine computes disparity maps from dual‑camera inputs, delivering accurate three‑dimensional scene reconstruction for applications such as autonomous robots, AR/VR headsets and advanced driver‑assistance systems.

The market is accelerating because demand for low‑latency visual intelligence on edge devices is surging across automotive, industrial automation and consumer electronics sectors. Furthermore, advancements in semiconductor process nodes (e.g., sub‑10 nm FinFET) are reducing power consumption while boosting compute density, making these chips attractive for battery‑operated platforms. Key players,including Qualcomm Snapdragon™ Vision Pro, Intel Movidius Myriad X VPU series and Apple’s Neural Engine,are expanding their portfolios through strategic partnerships and firmware optimizations, further fueling adoption.

MARKET DRIVERS

Rising Demand for Real‑Time Vision Analytics

The rapid expansion of smart manufacturing, surveillance, and augmented‑reality platforms is pushing manufacturers to adopt Edge AI vision processor chip with stereo depth engine Market solutions that can deliver sub‑second processing at the sensor level. Enterprises prefer on‑device inference to reduce bandwidth costs and protect proprietary visual data.

Advances in Low‑Power Edge AI Architectures

Recent semiconductor breakthroughs have slashed power envelopes by up to 45 % while preserving high‑throughput stereoscopic depth calculation. This efficiency enables battery‑operated drones and wearable devices to run sophisticated 3‑D perception algorithms without overheating.

➤ “Edge AI vision processors now provide millisecond‑level depth estimation, unlocking new use‑cases in robotics and automotive safety.”

Because these chips integrate dedicated tensor cores and mixed‑signal interfaces, system‑level designers can consolidate multiple vision functions,object detection, semantic segmentation, and depth mapping,into a single silicon footprint, accelerating time‑to‑market for innovative products.

MARKET CHALLENGES

Technical Complexity and Integration

Designing heterogeneous systems that combine stereo cameras, high‑speed memory, and AI accelerators demands deep expertise. Many OEMs encounter steep learning curves when optimizing firmware to exploit parallel depth engines efficiently.

Other Challenges

Manufacturing Yield Constraints

The fine‑line lithography required for sub‑micron AI cores can lead to lower wafer yields, driving up unit costs and limiting price competitiveness against legacy vision ASICs.

MARKET RESTRAINTS

High Development Costs

R&D programs for stereoscopic depth engines involve extensive sensor calibration, AI model training, and silicon validation. Investment cycles often exceed 18 months, deterring smaller startups from entering Edge AI vision processor chip with stereo depth engine Market.

Additionally, the need for specialized design houses and IP licensing inflates capital expenditures, creating a barrier for enterprises seeking rapid product diversification.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Robotics

Autonomous delivery robots and collaborative cobots are increasingly relying on on‑edge 3‑D perception to navigate dynamic environments. The ability to compute depth locally reduces latency and improves safety, making stereoscopic AI chips a strategic asset.

Beyond robotics, sectors such as precision agriculture and industrial inspection are piloting compact vision modules that embed stereo depth engines, promising a compound annual growth rate above 20 % over the next five years.

These trends suggest that vendors who can deliver low‑cost, power‑efficient solutions will capture a sizable share of the expanding Edge AI vision processor chip with stereo depth engine Market.

Edge AI vision processor chip with stereo depth engine Market Trends

Accelerating Adoption Driven by Low‑Latency Visual Intelligence

Edge AI vision processor chip with stereo depth engine Market is experiencing rapid expansion as device manufacturers prioritize on‑device image analysis to eliminate reliance on cloud connectivity. Valued at USD 1.45 billion in 2025, the market is expected to rise to USD 1.55 billion in 2026 and reach USD 3.12 billion by 2034, reflecting a steady compound annual growth rate of approximately 7.2 %. The surge is anchored in growing demand for real‑time object detection, depth perception, and three‑dimensional scene reconstruction across autonomous robotics, augmented‑reality headsets, and advanced driver‑assistance systems.

Other Trends

Technology Advancements and Power Efficiency

Recent progress in semiconductor process nodes, notably sub‑10 nm FinFET technologies, is delivering higher compute density while cutting power draw. Integrated neural‑network accelerators now support complex convolutional workloads alongside dedicated stereo depth engines that generate disparity maps from dual‑camera inputs. This combination enables battery‑powered edge devices to run sophisticated vision algorithms locally, extending operational life for mobile platforms and reducing latency to under 10 ms for critical safety functions.

Competitive Landscape and Strategic Partnerships

Key players such as Qualcomm Snapdragon™ Vision Pro, Intel Movidius Myriad X VPU series, and Apple’s Neural Engine are broadening their portfolios through firmware optimization and co‑development agreements with camera module suppliers. These collaborations accelerate time‑to‑market for integrated vision solutions and reinforce ecosystem compatibility. As manufacturers embed these chips into consumer electronics, industrial automation, and automotive platforms, the competitive pressure drives continuous innovation, further solidifying the market’s growth trajectory.

COMPETITIVE LANDSCAPE

Key Industry Players

Edge AI Vision Processor Chip with Stereo Depth Engine – Competitive Overview

The market is presently dominated by a handful of integrated‑system vendors that combine high‑performance neural‑network accelerators with dedicated stereo depth engines. Qualcomm’s Snapdragon Vision Pro line sets the benchmark for power‑efficient, on‑device disparity computation, while Intel’s Movidius Myriad X VPU series offers a flexible programmable fabric that has been adopted in autonomous‑robot platforms. Apple’s Neural Engine, embedded in its custom silicon, leverages advanced depth‑mapping pipelines for AR/VR headsets, and NVIDIA’s Jetson Xavier platform provides a GPU‑centric alternative for automotive ADAS applications. These leaders command the bulk of high‑volume contracts and drive the overall architecture standards, creating a market structure where differentiated compute‑density, sub‑10 nm process nodes, and extensive software ecosystems become decisive competitive advantages.

Beyond the headline players, a robust cohort of niche specialists expands the functional breadth of the ecosystem. MediaTek’s Dimensity Vision chips target consumer‑grade smart‑camera devices, while Ambarella’s CVflow processors focus on low‑power drone and surveillance markets. Samsung’s Exynos Vision series integrates a custom depth‑engine for premium smartphones. Chinese innovators such as Cambricon (MLU‑E), Horizon Robotics (Journey 3), and Graphcore (IPU) bring AI‑centric IP that is being re‑hosted on vision‑focused silicon. Synopsys offers DesignWare ARC processors with optional stereo modules for industrial IoT, Texas Instruments supplies the TDA series for automotive safety, Renesas provides the R‑Car family for embedded vision, and Veoneer delivers dedicated ADAS chips with built‑in depth perception. These companies often partner with OEMs or system integrators, supplying specialized solutions that complement the broader market while maintaining distinct value propositions.

List of Key Edge AI Vision Processor Companies Profiled

- Qualcomm Snapdragon Vision Pro

- Intel Movidius Myriad X

- Apple Neural Engine

- NVIDIA Jetson Xavier

- MediaTek Dimensity Vision

- Ambarella CVflow

- Samsung Exynos Vision

- Cambricon MLU‑E

- Horizon Robotics Journey 3

- Graphcore IPU

- Synopsys DesignWare ARC

- Texas Instruments TDA Series

- Renesas R‑Car Vision

- Veoneer ADAS Vision Chip

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Neural‑Network Accelerated Vision Processors

|

| By Application |

|

Advanced Driver‑Assistance Systems (ADAS)

|

| By End User |

|

Automotive Manufacturers

|

| By Technology |

|

Sub‑10 nm FinFET Processors

|

| By Market Driver |

|

Latency‑Critical Edge Intelligence

|

Regional Analysis: North America

The automotive sector is at the forefront of edge AI vision processor chip adoption, driven by the need for enhanced ADAS, autonomous driving capabilities, and in-cabin monitoring systems. The demand for robust and reliable stereo depth engine technology is particularly pronounced in this segment for accurate perception of the surrounding environment.

Industrial applications are witnessing increased adoption of edge AI vision processors for quality control, predictive maintenance, and robotic automation. The ability to perform real-time visual analysis on the factory floor enables improved efficiency, reduced downtime, and enhanced safety. Stereo depth engine technology is crucial for accurate 3D object detection and measurement in industrial settings.

The retail and security sectors are leveraging edge AI vision processors for applications such as customer behavior analysis, inventory management, and enhanced surveillance. The ability to analyze video feeds in real-time enables retailers to optimize store layouts, improve customer experience, and prevent theft. Security applications benefit from improved object detection and facial recognition capabilities.

Edge AI vision processors are finding applications in healthcare for medical image analysis, patient monitoring, and robotic surgery assistance. The computational power of edge devices allows for faster and more efficient processing of medical images, aiding in quicker diagnoses and improved patient care. Stereo depth engine applications are emerging for 3D imaging and surgical guidance.

Europe

Europe demonstrates strong growth potential for edge AI vision processor chip with stereo depth engine Market. Driven by robust manufacturing capabilities and a focus on industrial innovation, the region is actively investing in AI-powered solutions. European automotive manufacturers are heavily integrating advanced driver-assistance systems (ADAS) and autonomous driving technologies, generating demand for sophisticated edge AI vision processing. Furthermore, increasing regulatory focus on data privacy and security is promoting the adoption of edge computing solutions, enabling data processing closer to the source and minimizing data transmission risks. The industrial sector in Europe is also embracing edge AI for automation and quality control, contributing significantly to market expansion. Focus on energy efficiency and sustainable practices is fostering the development of power-efficient edge AI chip solutions.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for Edge AI vision processor chip with stereo depth engine Market. This rapid expansion is primarily driven by the burgeoning electronics manufacturing industry in countries like China, India, and South Korea. The Asia-Pacific region is a major hub for IoT device production, fueling demand for edge AI solutions for connected devices. The automotive industry in Asia-Pacific is also experiencing significant growth, with increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies in both passenger and commercial vehicles. The government initiatives promoting AI and smart manufacturing are further accelerating market growth. The strong presence of technology giants and a rapidly growing consumer base contribute to the region’s dominance in the market. The focus is on affordable and high-performance solutions for mass-market applications.

South America

South America is an emerging market with growing opportunities for Edge AI vision processor chip with stereo depth engine Market. The increasing adoption of IoT devices in agriculture, logistics, and retail is driving demand for edge AI solutions. The region’s agricultural sector is particularly interested in using edge AI for crop monitoring, yield prediction, and precision farming. The logistics industry is leveraging edge AI for warehouse automation, route optimization, and supply chain management. The growing adoption of security systems in urban areas is also contributing to market growth. While the market is still relatively nascent, the long-term growth potential is significant, fueled by increasing disposable incomes and government investments in technology infrastructure.

Middle East & Africa

The Middle East & Africa region presents a promising growth opportunity for Edge AI vision processor chip with stereo depth engine Market. Significant investments in smart city initiatives, infrastructure development, and autonomous vehicle testing are driving demand for edge AI solutions. The region’s automotive industry is witnessing increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies, particularly in countries like Saudi Arabia and the UAE. The growing focus on security and surveillance is also contributing to market growth. The tourism sector is also leveraging edge AI for enhanced customer experiences and security. The combination of government support, increasing disposable incomes, and growing technological awareness is expected to drive strong market expansion in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Edge AI vision processor chip with stereo depth engine Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Edge AI vision processor chip with stereo depth engine Market?

-> Edge AI vision processor chip with stereo depth engine market size was valued at USD 1.55 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 7.2%.

Which key companies operate Edge AI vision processor chip with stereo depth engine Market?

-> Key players include Qualcomm (Snapdragon™ Vision Pro), Intel (Movidius Myriad X VPU series), Apple (Neural Engine), and other semiconductor innovators expanding their edge‑AI portfolios.

What are the key growth drivers?

-> Key growth drivers include rising demand for low‑latency visual intelligence on edge devices, expanding applications in autonomous robotics, AR/VR, and advanced driver‑assistance systems, and continuous advancements in sub‑10 nm semiconductor process nodes that lower power consumption while increasing compute density.

Which region dominates the market?

-> The reference material does not specify a single dominant region; however, adoption is strong across automotive and industrial automation hubs in North America, Europe, and Asia‑Pacific.

What are the emerging trends?

-> Emerging trends include integration of AI accelerators directly on silicon for real‑time stereo depth perception, tighter coupling of AI/IoT edge solutions, and the development of energy‑efficient chips leveraging advanced FinFET technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...