MARKET INSIGHTS

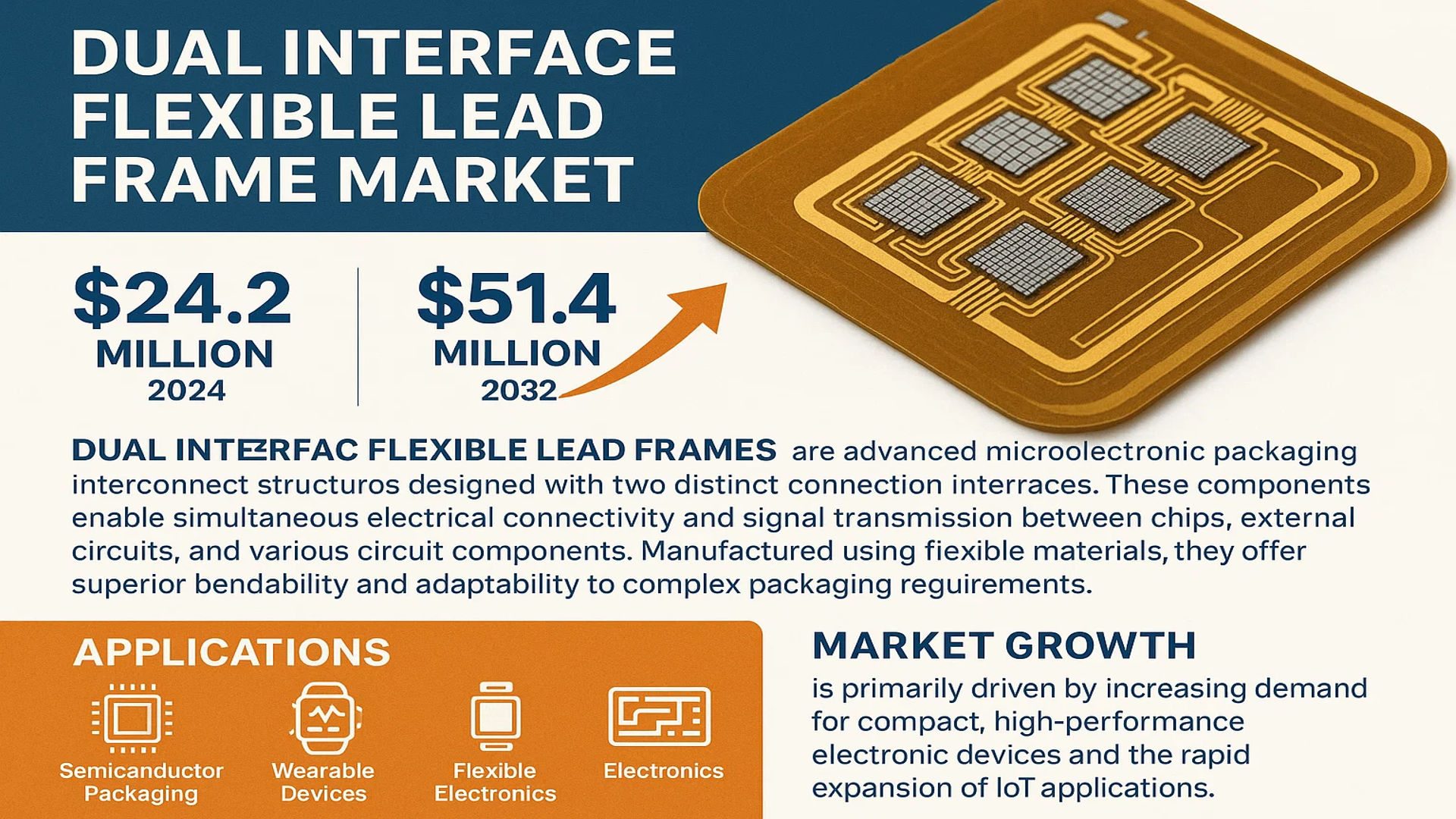

The global Dual Interface Flexible Lead Frame Market was valued at 24.2 million in 2024 and is projected to reach US$ 51.4 million by 2032, at a CAGR of 11.5% during the forecast period.

Dual interface flexible lead frames are advanced microelectronic packaging interconnect structures designed with two distinct connection interfaces. These components enable simultaneous electrical connectivity and signal transmission between chips, external circuits, and various circuit components. Manufactured using flexible materials, they offer superior bendability and adaptability to complex packaging requirements. Their applications span across semiconductor packaging, wearable devices, and flexible electronics, playing a pivotal role in enabling device miniaturization and performance enhancements.

Market growth is primarily driven by increasing demand for compact, high-performance electronic devices and the rapid expansion of IoT applications. The 6PIN segment is expected to witness significant adoption, particularly in financial cards and ETC systems. Key players such as Linxens, LG Innotek, and New Henghui Electronics dominate the competitive landscape, collectively holding a substantial market share. Technological advancements in semiconductor packaging and rising investments in flexible electronics further contribute to market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Miniaturized Electronics to Propel Dual Interface Flexible Lead Frame Adoption

The relentless trend toward electronic miniaturization across industries is accelerating demand for dual interface flexible lead frames. With smartphones, wearables, and IoT devices requiring increasingly compact yet high-performance components, flexible lead frames provide the ideal interconnect solution. Studies indicate that the semiconductor packaging market, where these components play a critical role, continues expanding at nearly 9% annually. Dual interface configurations are particularly valuable in space-constrained applications because they can simultaneously handle multiple connection types while maintaining flexibility for complex form factors. As consumer electronics shrink in size but grow in functionality, manufacturers are adopting these advanced packaging solutions at unprecedented rates.

Rise of Contactless Payment Systems Driving Financial Card Applications

The global shift toward contactless financial transactions represents a major growth driver for dual interface flexible lead frames. These components form the backbone of modern smart cards that combine both contact and contactless functionality. With contactless payment transactions projected to exceed $10 trillion annually in coming years, card manufacturers are rapidly upgrading production capabilities. Financial institutions worldwide continue replacing traditional magnetic stripe cards with dual-interface chip cards that offer enhanced security and convenience. This transition creates sustained demand for the specialized lead frames that enable these hybrid payment solutions while meeting stringent banking industry durability requirements.

Furthermore, government initiatives promoting cashless economies across emerging markets are compounding this effect, with several Asian and European nations mandating dual-interface payment cards as the new standard for financial transactions.

MARKET RESTRAINTS

High Production Costs Limit Widespread Market Adoption

While dual interface flexible lead frames offer significant technical advantages, their manufacturing complexity creates substantial cost barriers. The specialized materials and precision fabrication processes required can increase production expenses by 30-40% compared to conventional lead frames. Many small and medium electronics manufacturers find these costs prohibitive, particularly in price-sensitive consumer markets. The sophisticated electroplating and micro-machining techniques demand both expensive equipment and highly trained operators, further elevating overhead expenses. Until economies of scale and manufacturing innovations can reduce these cost premiums, widespread adoption across all market segments remains constrained.

Other Restraints

Material Compatibility Challenges

Finding substrate materials that maintain flexibility while withstanding repeated stress cycles presents ongoing technical challenges. The thermal expansion properties must precisely match semiconductor components to prevent reliability issues, requiring extensive materials research and testing.

Supply Chain Complexities

The specialized nature of raw materials creates vulnerability to supply disruptions. Recent semiconductor industry shortages have highlighted how single-supplier dependencies for key materials can jeopardize production schedules across entire electronics value chains.

MARKET OPPORTUNITIES

Automotive Electronics Revolution Offers Significant Growth Potential

The automotive industry’s electrification and digital transformation represents a major opportunity for dual interface flexible lead frame manufacturers. Modern vehicles incorporate hundreds of electronic control units requiring robust yet compact interconnects able to withstand harsh operating environments. The increasing adoption of advanced driver assistance systems (ADAS) and in-vehicle networking solutions creates strong demand for specialized packaging technologies. With automotive electronics content per vehicle projected to triple in the next decade, component suppliers are actively developing automotive-grade versions of flexible lead frames that meet rigorous industry reliability standards.

Medical Wearables Expand Application Horizons

The booming medical wearable device sector presents another promising avenue for market expansion. Next-generation health monitors require biocompatible, flexible electronics that can conform to the human body while maintaining signal integrity. Dual interface lead frames enable the hybrid functionality needed in devices that combine biosensing with wireless data transmission. The global medical wearables market continues growing rapidly, with particular strength in continuous glucose monitors, cardiac patches, and neurological sensors – all applications where these advanced interconnects provide distinct advantages over traditional packaging solutions.

MARKET CHALLENGES

Technical Limitations in High-Frequency Applications Pose Development Hurdles

While dual interface flexible lead frames excel in many applications, their performance in high-frequency environments presents ongoing engineering challenges. Signal integrity becomes increasingly difficult to maintain as operating frequencies exceed 5GHz, limiting their use in cutting-edge wireless and RF applications. The flexible substrate materials that provide mechanical advantages can introduce unwanted parasitic effects at higher frequencies. Manufacturers are investing heavily in advanced simulation tools and new material formulations to overcome these limitations, but achieving performance parity with rigid substrates remains technically demanding.

Other Challenges

Standardization Gaps

The rapid evolution of flexible packaging technologies has outpaced industry standardization efforts. Differing specifications across manufacturers create compatibility concerns that slow adoption in conservative industries like aerospace and medical equipment.

Environmental Compliance Concerns

Increasingly stringent regulations regarding hazardous substances in electronics manufacturing require continuous reformulation of materials and processes. The lead frames must comply with multiple regional regulations while maintaining performance characteristics, adding complexity to global supply chains.

DUAL INTERFACE FLEXIBLE LEAD FRAME MARKET TRENDS

Growth in Semiconductor Miniaturization Driving Demand for Flexible Lead Frames

The semiconductor industry’s push toward miniaturization and high-density packaging is fueling the adoption of dual interface flexible lead frames. These components enable thinner, more compact designs while maintaining robust electrical connectivity—a critical requirement for next-generation devices. With the global semiconductor packaging market projected to exceed $60 billion by 2027, demand for advanced interconnect solutions continues to accelerate. Dual interface models effectively address the challenges of signal integrity in space-constrained applications like foldable smartphones and IoT sensors, where traditional rigid lead frames struggle to meet performance requirements.

Other Trends

Expansion in Contactless Payment Infrastructure

The global shift toward cashless transactions is creating substantial opportunities for dual interface flexible lead frames in payment card applications. Financial institutions are increasingly adopting hybrid cards combining both contact and contactless functionalities, with over 3.4 billion dual interface payment cards expected to be in circulation by 2026. This trend is particularly strong in Europe and Asia-Pacific regions where governments are mandating EMV chip card migrations, driving card reissuance cycles that typically incorporate the latest flexible lead frame technologies.

Material Innovation Enhancing Performance Characteristics

Manufacturers are achieving performance breakthroughs through novel material compositions in flexible lead frame production. The integration of high-performance polyimide substrates with advanced copper alloys has yielded products with superior thermal stability (withstanding temperatures up to 400°C) while maintaining flexibility. Such innovations are critical for automotive electronics applications where lead frames must endure engine compartment conditions while enabling complex three-dimensional packaging configurations demanded by ADAS sensor arrays and infotainment systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Leadership

The global dual interface flexible lead frame market features a moderately competitive structure with major players dominating revenue shares while regional participants compete through localized solutions. Linxens emerges as a market leader, leveraging its decades-long expertise in microconnectors and secure identity solutions. The company’s stronghold in Europe and Asia, coupled with its continuous R&D investment in flexible electronics, positions it favorably for future growth.

LG Innotek represents another pivotal player, particularly in the Asia-Pacific region, where its vertically integrated semiconductor components business provides cost advantages. The company has recently expanded its portfolio to include advanced lead frame solutions for automotive electronics, capitalizing on the growing demand for connected vehicle technologies.

Mid-sized competitors like New Henghui Electronics are gaining traction through specialized offerings for financial cards and government ID applications. With the 6PIN segment projected for significant growth, companies are actively developing thinner, more durable interfaces that meet emerging industry standards for contactless payment systems.

Market dynamics show increasing collaboration between lead frame manufacturers and semiconductor packaging firms to develop integrated solutions. Several industry leaders have formed strategic alliances with chipset providers to create optimized packages for IoT devices and wearables, creating new revenue streams while improving technical specifications.

List of Key Dual Interface Flexible Lead Frame Companies

- Linxens (France)

- LG Innotek (South Korea)

- New Henghui Electronics (China)

- Mitsui High-tec (Japan)

- ASM Pacific Technology (Hong Kong)

- POSSEHL Electronics (Germany)

- Signetics (South Korea)

- Jentech Precision Industrial (Taiwan)

- WuXi Micro Just-Tech (China)

Segment Analysis:

By Type

6PIN Lead Frames Hold Majority Share Due to Compact Design and High Compatibility

The market is segmented based on type into:

- 6PIN

- 8PIN

- Others

By Application

Financial Cards Emerge as Key Application Segment Owing to Increased Adoption of Contactless Payments

The market is segmented based on application into:

- Financial Card

- ETC Card

- Others

By Material

Copper-based Lead Frames Maintain Dominance Due to Superior Electrical Conductivity

The market is segmented based on material composition into:

- Copper Alloy

- Iron-Nickel Alloy

- Other Metal Alloys

By End-Use Industry

Consumer Electronics Leads Market Demand Fueled by Miniaturization Trends

The market is segmented based on end-use industries into:

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

- Others

Regional Analysis: Dual Interface Flexible Lead Frame Market

Asia-Pacific

The Asia-Pacific region dominates the Dual Interface Flexible Lead Frame market, accounting for the largest revenue share due to its thriving semiconductor and electronics manufacturing sector. China leads the regional market, with significant investments in miniaturized and flexible electronics, particularly for applications like financial cards and wearables. The presence of major semiconductor foundries and packaging companies, coupled with cost-effective production capabilities, drives adoption. However, intellectual property concerns and competitive pricing pressures create challenges for premium-grade solutions. Japan and South Korea also contribute substantially, leveraging their advanced semiconductor ecosystems and strong R&D focus on next-generation packaging technologies.

North America

North America represents the second-largest market, characterized by high-value applications in secure financial cards and advanced wearables. The U.S. leads regional demand, supported by stringent security requirements for payment cards and government-issued IDs. Major technology firms are adopting Dual Interface Flexible Lead Frames for compact, high-reliability IoT devices. While the market shows steady growth, it faces constraints from higher production costs and shifting supply chains. Canada’s emerging semiconductor packaging sector presents new opportunities, though adoption remains limited to niche applications.

Europe

Europe maintains a strong position in the Dual Interface Flexible Lead Frame market, particularly for banking and transportation card applications. Germany and France lead regional adoption, with their well-established smart card industries and emphasis on secure transaction technologies. The EU’s focus on digital identity solutions and contactless payments drives demand for advanced lead frame solutions. However, the market faces slower growth compared to Asia, hampered by higher production costs and stringent environmental regulations affecting material choices. The region remains a hub for innovation, with several key players developing next-generation flexible electronics solutions.

Middle East & Africa

The MEA region shows emerging potential for Dual Interface Flexible Lead Frames, particularly in GCC countries adopting advanced financial technologies and national ID programs. While still a developing market, increasing urbanization and digital payment adoption create growth opportunities. The lack of local manufacturing capabilities and reliance on imports currently limit market expansion. South Africa and UAE lead regional adoption, though volumes remain relatively small compared to other regions. Future growth will depend on infrastructure development and regional economic stability.

South America

South America presents limited but growing opportunities for Dual Interface Flexible Lead Frames, primarily in Brazil’s financial sector and Colombia’s transportation card applications. Economic volatility and currency fluctuations continue to challenge consistent market growth. While some local manufacturers have begun adopting these technologies for domestic smart card production, most advanced solutions are imported. The region shows long-term potential as digital payment systems become more widespread, though adoption will likely follow rather than lead global trends.

Report Scope

This market research report provides a comprehensive analysis of the global Dual Interface Flexible Lead Frame market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 24.2 million in 2024 and is projected to reach USD 51.4 million by 2032, growing at a CAGR of 11.5%.

- Segmentation Analysis: Detailed breakdown by product type (6PIN, 8PIN), application (Financial Card, ETC Card, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market due to strong semiconductor manufacturing presence.

- Competitive Landscape: Profiles of leading market participants including Linxens, LGInnotek, and New Henghui Electronics, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in flexible electronics, miniaturization trends, and evolving packaging standards for semiconductor devices.

- Market Drivers & Restraints: Evaluation of factors driving market growth (demand for flexible electronics, semiconductor industry expansion) along with challenges (material costs, technical complexity).

- Stakeholder Analysis: Insights for component suppliers, semiconductor manufacturers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Dual Interface Flexible Lead Frame Market?

-> Dual Interface Flexible Lead Frame Market was valued at 24.2 million in 2024 and is projected to reach US$ 51.4 million by 2032, at a CAGR of 11.5% during the forecast period.

Which key companies operate in Global Dual Interface Flexible Lead Frame Market?

-> Key players include Linxens, LGInnotek, and New Henghui Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for flexible electronics, growth in semiconductor packaging, and miniaturization trends in electronic devices.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven by strong semiconductor manufacturing presence in countries like China, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include development of advanced materials for better flexibility, integration with IoT devices, and increasing adoption in wearable technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...