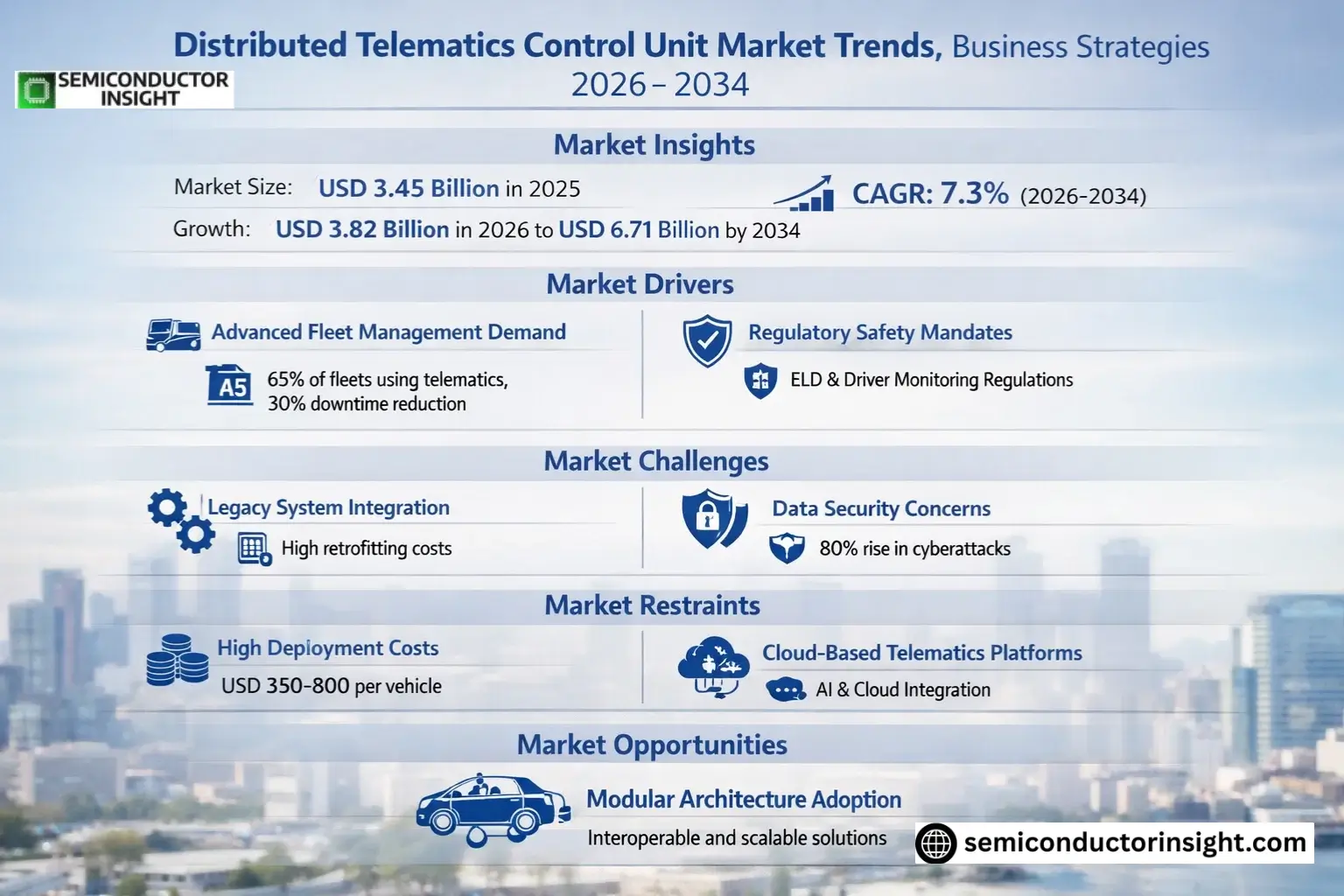

Market Insights

Global Distributed Telematics Control Unit Market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.82 billion in 2026 to USD 6.71 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period.

A distributed telematics control unit is a system that distributes control decisions and functions across multiple nodes within a vehicle’s network, enabling real-time data exchange and coordinated operations. These units integrate modules such as power management, emergency communication interfaces, wireless connectivity, and antenna systems to enhance vehicle telemetry and safety features. For instance, during emergencies, the system autonomously triggers alerts while maintaining uninterrupted power supply through its distributed architecture.

The market growth is driven by increasing adoption of connected vehicles, stringent regulatory mandates for vehicle safety, and advancements in IoT-enabled automotive technologies. Key players like Bosch, Continental, and Denso are investing in modular designs to support over-the-air updates and scalable solutions for electric and autonomous vehicles.

MARKET DRIVERS

Growing Demand for Advanced Fleet Management Solutions

Distributed Telematics Control Unit Market is experiencing robust growth driven by increasing adoption of smart fleet management systems. With over 65% of commercial fleets now using telematics solutions, the demand for decentralized control units has surged by 24% year-over-year. These units enable real-time vehicle diagnostics and predictive maintenance capabilities that reduce downtime by approximately 30%.

Regulatory Push for Driver Safety Monitoring

Stringent government regulations mandating electronic logging devices (ELDs) and driver behavior monitoring are accelerating market adoption. The European Union’s General Safety Regulation and U.S. FMCSA requirements have created a compliance-driven demand for distributed telematics solutions that can seamlessly integrate with existing vehicle architectures.

Emerging 5G network infrastructure is further enabling high-bandwidth applications like video telematics, creating additional growth opportunities for distributed TCU deployments.

MARKET CHALLENGES

Integration Complexities with Legacy Systems

While distributed telematics control units offer flexibility, many fleet operators face significant challenges retrofitting them into older vehicle models. Compatibility issues with proprietary OEM systems can increase installation costs by 40-60% for mixed fleet operators.

Other Challenges

Data Security Concerns

The distributed nature of these systems creates multiple potential vulnerabilities, with cyberattacks on commercial vehicle systems increasing by 80% since 2020. Implementing end-to-end encryption across all control units remains a critical challenge.

MARKET RESTRAINTS

High Initial Deployment Costs

The upfront investment required for distributed telematics control unit implementation remains a significant barrier, particularly for small and medium fleets. A complete system deployment can cost between USD 350-USD 800 per vehicle, with ROI periods extending beyond 18 months for many operators.

MARKET OPPORTUNITIES

Cloud-Based Telematics Platforms Integration

The emergence of AI-powered analytics platforms presents significant growth opportunities for distributed telematics control unit providers. Integration with cloud services allows for advanced features like dynamic routing optimization and fuel efficiency tracking, with adoption rates among fleet operators increasing by 35% annually.

Distributed Telematics Control Unit Market Trends

Modular Architecture Adoption Accelerating

Distributed Telematics Control Unit Market is witnessing increased preference for modular architectures that distribute functions across multiple vehicle nodes. This design approach improves system resilience while enabling targeted upgrades for specific telematics functions like emergency calling, charging management, and wireless connectivity. Leading manufacturers are developing interoperable modules that comply with evolving automotive communication protocols.

Other Trends

Regional Manufacturing Expansion

Major suppliers including Bosch, Continental and Denso are establishing localized production facilities in key automotive markets. This strategy addresses supply chain vulnerabilities while meeting regional content requirements. China’s growing intelligent connected vehicle sector is driving significant capacity additions for basic and advanced Distributed Telematics Control Unit variants.

Integration with Next-Gen Vehicle Networks

Development efforts are focused on ensuring Distributed Telematics Control Unit compatibility with emerging vehicle network architectures. The transition to domain-based electronic systems and zonal architectures requires distributed telematics solutions that can interface effectively with both legacy systems and new computing platforms. Wireless connection units are being upgraded to support 5G-V2X communication requirements.

Cybersecurity Prioritization

As distributed architectures increase potential attack surfaces, manufacturers are incorporating hardware-based security modules within telematics control units. Features like secure boot, encrypted data storage, and intrusion detection systems are becoming standard across product offerings from LG, Huawei and other leading suppliers.

Standardization Initiatives Gaining Momentum

Industry consortia are developing common standards for Distributed Telematics Control Unit interfaces and communication protocols. These efforts aim to reduce development costs while ensuring interoperability across vehicle platforms. Standardization is particularly critical for emergency call systems and vehicle-to-cloud data exchange functionalities.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Market Leaders Spearheading Innovation in Distributed TCU Solutions

Distributed Telematics Control Unit Market is dominated by established automotive electronics giants, with LG, Samsung, and Denso collectively holding significant market share. Bosch and Continental maintain strong positions through advanced R&D capabilities and extensive OEM partnerships, particularly in European and North American markets. These top players account for approximately 60% of global revenue, leveraging their integrated solutions combining hardware modules with cloud-based telematics platforms.

Emerging competition comes from specialized suppliers like Peiker and Visteon, focusing on high-reliability embedded systems. Chinese manufacturers Huawei and Xiamen Yaxun Zhilian Technology are rapidly expanding through cost-effective solutions for the Asia-Pacific region. Niche players like Laird and Flaircomm Microelectronics cater to specific connectivity requirements, while Magneti Marelli and Ficosa provide customized modules for premium vehicle segments.

List of Key Distributed Telematics Control Unit Companies Profiled

- LG Electronics

- Samsung Electronics

- Denso Corporation

- Bosch

- Continental AG

- Huawei Technologies

- Visteon Corporation

- Peiker Acustic

- Magneti Marelli

- Laird Connectivity

- Ficosa International

- Flaircomm Microelectronics

- Xiamen Yaxun Zhilian Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Advanced Telematics Control Units are witnessing higher adoption due to their enhanced connectivity features and comprehensive vehicle monitoring capabilities. Key factors driving demand include:

|

| By Application |

|

Commercial Vehicles represent the most significant application area due to:

|

| By End User |

|

OEMs dominate the adoption curve with several strategic advantages:

|

| By Communication Technology |

|

Cellular (4G/5G) technologies are becoming the preferred choice due to:

|

| By Deployment Architecture |

|

Distributed Architecture is gaining significant traction owing to:

|

Regional Analysis: Global Distributed Telematics Control Unit Market

North America

North America maintains technological leadership with advanced distributed TCU architectures that enable decentralized data processing. The region’s focus on reducing latency in critical vehicle communications drives innovation in edge computing capabilities within TCUs, particularly for autonomous vehicle applications.

Stringent regulations mandating electronic logging devices (ELDs) and advanced driver-assistance systems (ADAS) create a favorable landscape for distributed TCU adoption. Compliance requirements push fleet operators towards sophisticated telematics solutions with distributed processing capabilities.

The mature logistics and transportation sector drives substantial demand for distributed TCUs that offer scalable solutions for large vehicle fleets. Real-time diagnostics and predictive maintenance capabilities through distributed computing are particularly valued by North American fleet operators.

Strategic collaborations between automotive OEMs and cloud service providers are accelerating the deployment of distributed TCU solutions. These partnerships focus on integrating vehicle data with enterprise systems while maintaining optimal processing distribution.

Europe

Europe represents the second-largest market for Distributed Telematics Control Units, characterized by progressive automotive safety regulations and growing emphasis on connected mobility solutions. The European market benefits from strong automotive manufacturing capabilities and increasing adoption of software-defined vehicle architectures. GDPR-compliant data processing requirements are driving demand for distributed TCUs with localized data handling capabilities. The region shows particularly strong uptake in commercial vehicle segments, where fleet operators seek to optimize operations through advanced telematics with distributed intelligence.

Asia-Pacific

Asia-Pacific is witnessing rapid growth in the Distributed Telematics Control Unit Market, fueled by expanding vehicle production and digital transformation in transportation sectors. Emerging economies are investing heavily in smart mobility infrastructure, creating opportunities for decentralized telematics solutions. The region benefits from cost-effective manufacturing of telematics components and growing adoption in commercial logistics applications. Government initiatives promoting intelligent transportation systems are accelerating market penetration, particularly in China, Japan, and South Korea.

South America

South America presents developing potential for Distributed Telematics Control Units, with growth centered around fleet management applications in major economies like Brazil. Market adoption is progressing through localized solutions that address regional connectivity challenges and economic constraints. The mining and agriculture sectors demonstrate particular interest in ruggedized distributed TCU solutions capable of operating in remote environments with intermittent connectivity.

Middle East & Africa

The Middle East & Africa region shows emerging demand for Distributed Telematics Control Units, primarily driven by infrastructure development projects and commercial vehicle fleets. Oil and gas operations are adopting specialized distributed TCUs for asset tracking in harsh environments. The market benefits from government smart city initiatives and growing awareness of telematics benefits in vehicle security and maintenance optimization.

Report Scope

This market research report provides a comprehensive analysis of the Distributed Telematics Control Unit Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of telematics in powering advancements across industries such as automotive, telecommunications, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, telematics design trends, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Distributed Telematics Control Unit Market?

-> Distributed Telematics Control Unit Market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.82 billion in 2026 to USD 6.71 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period.

What is the market size in key regions?

-> The U.S. market size is estimated at USD million in 2025 while China is expected to reach USD million.

Who are the key players in Distributed Telematics Control Unit Market?

-> Key players include LG, Samsung, Denso, Bosch, Continental, Huawei, Visteon, Peiker, Magneti Marelli, and Laird, with the top five players holding approximately % market share in 2025.

What are the key product segments?

-> The market is segmented into Basic and Advanced product types, with the Basic segment projected to reach USD million by 2034.

What are the key applications?

-> Major applications include Intelligent Connected Vehicle Industry and Other sectors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...