Market Insights

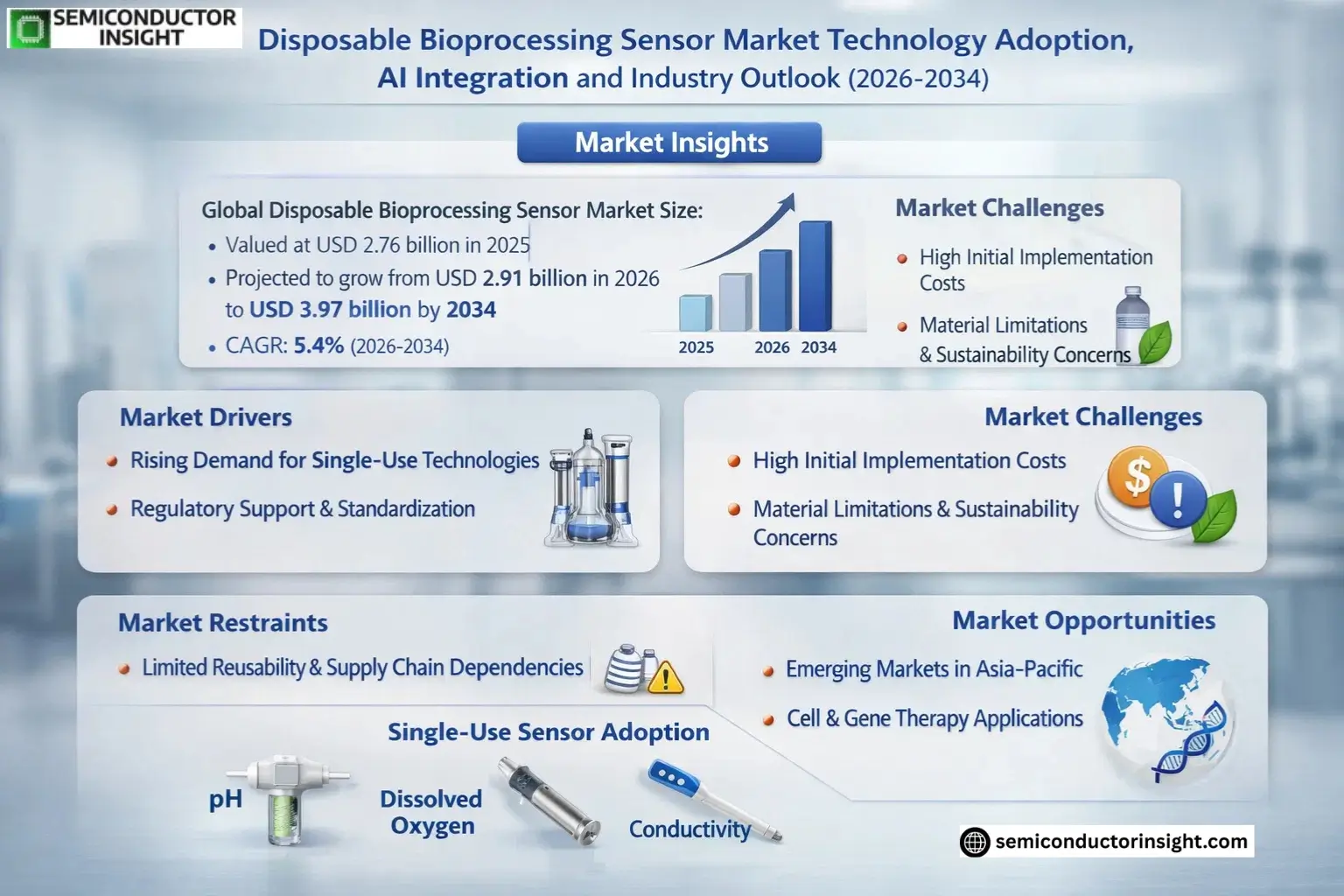

Global Disposable Bioprocessing Sensor Market size was valued at USD 2.76 billion in 2025. The market is projected to grow from USD 2.91 billion in 2026 to USD 3.97 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period.

Disposable bioprocessing sensors are single-use devices designed for monitoring critical parameters in biopharmaceutical and bioprocessing applications. These sensors eliminate the need for cleaning or recalibration between batches, reducing contamination risks while improving operational efficiency in upstream and downstream processes.

The market growth is driven by increasing adoption of single-use technologies in biomanufacturing, particularly for monoclonal antibodies and cell/gene therapies where sterility requirements are stringent. With pharmaceutical companies prioritizing flexible production systems, disposable sensors offering real-time monitoring of pH, dissolved oxygen, and conductivity parameters are gaining traction across bioreactor applications.

MARKET DRIVERS

Rising Demand for Single-Use Technologies

Disposable Bioprocessing Sensor Market is experiencing significant growth due to the increasing adoption of single-use technologies in biopharmaceutical manufacturing. These sensors reduce cross-contamination risks and improve operational efficiency, meeting the industry’s demand for cost-effective and flexible solutions. Global shift toward biologics and personalized medicines further accelerates this trend.

Regulatory Support and Standardization

Stringent regulatory frameworks by agencies like the FDA and EMA promote the use of disposable bioprocessing sensors for ensuring product safety and quality. Standardized disposable systems reduce validation time and compliance costs, making them critical components in modern biomanufacturing facilities.

Additionally, advancements in sensor accuracy and connectivity with IoT-enabled systems enhance real-time monitoring, further propelling market expansion.

MARKET CHALLENGES

High Initial Implementation Costs

Despite their advantages, disposable bioprocessing sensors face adoption barriers due to higher initial costs compared to traditional sensors. Small and mid-sized biopharma companies may find it challenging to justify the upfront investment, slowing market penetration in certain segments.

Other Challenges

Material Limitations and Sustainability Concerns

The reliance on plastic-based disposable sensors raises environmental concerns, pushing manufacturers to develop biodegradable alternatives without compromising performance or sterility.

MARKET RESTRAINTS

Limited Reusability and Supply Chain Dependencies

The disposable nature of these sensors creates ongoing supply chain demands for replacements, which can lead to operational vulnerabilities during raw material shortages or geopolitical disruptions. Manufacturers must balance cost efficiency with reliable sourcing strategies.

MARKET OPPORTUNITIES

Emerging Markets and Cell Therapy Applications

Asia-Pacific regions show untapped potential for disposable bioprocessing sensors, with increasing biopharmaceutical production in countries like China and India. Additionally, the rise of cell and gene therapies necessitates scalable, contamination-free sensor solutions, creating new revenue streams for market players.

Disposable Bioprocessing Sensor Market Trends

Adoption of Single-Use Technology Driving Sensor Demand

The biopharmaceutical industry’s shift toward single-use systems is accelerating the adoption of disposable bioprocessing sensors. These sensors eliminate cross-contamination risks while reducing cleaning and sterilization cycles, particularly valuable in upstream applications where they account for over 73% of usage. Key parameters monitored include pH, dissolved oxygen, and conductivity, with optical and electrochemical sensors being the dominant technologies.

Other Trends

Product Bundling Enhancing Value Proposition

Leading manufacturers are increasingly offering sensor systems bundled with disposable components and control software, creating higher-margin integrated solutions. This approach improves data reliability while maintaining gross margins between 60-75% for premium probes. The trend reflects the industry’s need for validated, audit-ready sensor packages in GMP environments.

Emerging Applications in Cell and Gene Therapy

The expansion of cell and gene therapy pipelines is creating new demand for disposable sensor solutions. Single-use systems enable faster batch changeovers critical for personalized medicine production, with sensors providing real-time process monitoring. This application segment shows above-average growth potential as therapy approvals increase globally.

Regional Market Development Patterns

North America and Europe currently lead in disposable bioprocessing sensor adoption, supported by established biopharmaceutical infrastructure. However, Asia-Pacific markets are growing rapidly due to increased biomanufacturing investments in China and India, particularly for biosimilar production. Local manufacturers are expanding sensor portfolios to meet regional demand.

Industry Consolidation and Standardization

Recent mergers among sensor manufacturers aim to create integrated single-use platforms with standardized interfaces. This consolidation drives economies of scale while addressing the industry’s need for compatible components. The trend is expected to continue as companies seek to optimize sensor manufacturing and distribution networks globally.

COMPETITIVE LANDSCAPE

Key Industry Players

Disposable Bioprocessing Sensor Market Dominated by Life Science Giants and Specialized Manufacturers

Global Disposable Bioprocessing Sensor Market is characterized by the dominance of established life science corporations with integrated product portfolios. Thermo Fisher Scientific leads the market through its comprehensive offering of single-use pH, dissolved oxygen, and conductivity sensors bundled with bioprocessing systems. Danaher Corporation follows closely with its subsidiaries Pall Corporation and Cytiva, leveraging strong OEM relationships in biomanufacturing. Second-tier players like Sartorius and METTLER TOLEDO compete through specialized sensor technologies and regional distribution networks, particularly in European biopharma hubs.

Niche players focus on innovation in optical sensing (PreSens Precision Sensing) and customized solutions for cell/gene therapy applications (Hamilton Company). The market has seen increasing vertical integration, with sensor manufacturers like Equflow B.V. being acquired by fluid handling specialists (Parker-Hannifin). Emerging competitors from Asia, particularly in polymer substrate sensors, are gaining traction in cost-sensitive markets through partnerships with local bioprocessing equipment providers.

List of Key Disposable Bioprocessing Sensor Companies Profiled

- Thermo Fisher Scientific

- Danaher Corporation

- Sartorius AG

- METTLER TOLEDO

- Hamilton Company

- Broadley-James Corporation

- PreSens Precision Sensing GmbH

- Parker-Hannifin Corporation

- Dover Corporation

- Equflow B.V

- Emerson Electric Co.

- Eppendorf AG

- Avantor

- Polestar Technologies, Inc.

- Getinge AB

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

pH Sensors dominate due to critical role in bioprocess monitoring

|

| By Application |

|

Biopharmaceuticals remains primary growth driver

|

| By End User |

|

CDMOs show fastest adoption rate

|

| By Sensing Technology |

|

Optical Sensors gaining traction in critical applications

|

| By Material Type |

|

Polymer Substrate dominates market

|

Regional Analysis: Global Disposable Bioprocessing Sensor Market

North American manufacturers lead in adopting smart disposable sensors with IoT connectivity, particularly for monoclonal antibody production. The region shows strong preference for pH and dissolved oxygen sensors compatible with single-use bioreactors. Biopharma companies prioritize sensors with predictive analytics capabilities to enhance process efficiency.

Advanced AI-driven sensor platforms are being deployed across major bioproduction facilities, enabling real-time quality monitoring. Machine learning algorithms analyze sensor data to predict batch anomalies, reducing failure rates. Leading contract manufacturers integrate sensor data with digital twins for process optimization.

The FDA’s Process Analytical Technology initiative drives sensor adoption for continuous monitoring. Compliance with USP <1079> guidelines remains critical for sensor manufacturers. Recent guidance documents encourage implementation of smart sensors for improved data integrity in biologics production.

Strategic collaborations between sensor manufacturers and bioprocessing equipment providers are accelerating innovation. Major CDMOs partner with tech firms to develop customized sensor solutions. University spin-offs contribute novel sensor technologies, particularly in single-use applications.

Europe

Europe maintains strong growth in disposable bioprocessing sensor adoption, with Germany and Switzerland leading in biopharmaceutical manufacturing. The region emphasizes sustainable sensor solutions with reduced environmental impact. EMA guidelines promote sensor technologies that enable continuous manufacturing processes. European manufacturers focus on sensor standardization and interoperability across single-use systems, with increasing investment in sensor technologies for cell and gene therapy production.

Asia-Pacific

The Asia-Pacific Disposable Bioprocessing Sensor Market experiences rapid expansion, driven by biopharma capacity expansion in China and India. Singapore and South Korea emerge as innovation hubs for sensor technologies. Regional manufacturers prioritize cost-effective solutions while improving accuracy. Government initiatives support localization of sensor production, particularly for vaccine manufacturing applications, creating new growth opportunities.

South America

South America shows growing interest in disposable sensors, particularly for vaccine and biosimilar production. Brazil dominates regional demand, with increasing technology transfer agreements with global biopharma companies. Limited local manufacturing capability creates import dependency, though regional partnerships aim to develop localized sensor solutions.

Middle East & Africa

The MEA region demonstrates nascent growth in disposable bioprocessing sensor adoption, focused on vaccine production facilities. UAE and South Africa lead infrastructure development with technology partnerships. Market growth is constrained by limited biomanufacturing capacity, though pandemic preparedness initiatives drive long-term sensor technology investments.

Report Scope

This market research report provides a comprehensive analysis of the Disposable Bioprocessing Sensor Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of disposable sensors in bioprocessing applications across industries such as biopharmaceuticals, cell and gene therapy, and academic research.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of single-use systems, sensor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Disposable Bioprocessing Sensor Market?

-> Disposable Bioprocessing Sensor Market size was valued at USD 2.76 billion in 2025. The market is projected to grow from USD 2.91 billion in 2026 to USD 3.97 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period.

What is the growth rate (CAGR) of the Disposable Bioprocessing Sensor Market?

-> The market is projected to grow at a CAGR of 5.4% during the forecast period (2025-2034).

Which key companies operate in Disposable Bioprocessing Sensor Market?

-> Key players include Thermo Fisher Scientific, Danaher, Sartorius, METTLER TOLEDO, Hamilton Company, Broadley-James Corporation, PreSens Precision Sensing GmbH, Parker-Hannifin Corporation, and Dover Corporation among others.

What are the key growth drivers?

-> Key growth drivers include migration towards single-use biomanufacturing, demand for flexible and data-driven processes, expansion of biopharmaceutical pipelines, and advantages of reduced contamination risk and improved efficiency.

What are the major product types in this market?

-> Major product types include pH Sensors, Dissolved Oxygen Sensors, Conductivity Sensors, and others.

Which application segment holds the largest market share?

-> Biopharmaceuticals account for the largest application share, with upstream applications representing approximately 73% of single-use probe and sensor revenue.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...