Direct-to-Chip Cooling Distribution Unit Market Insights

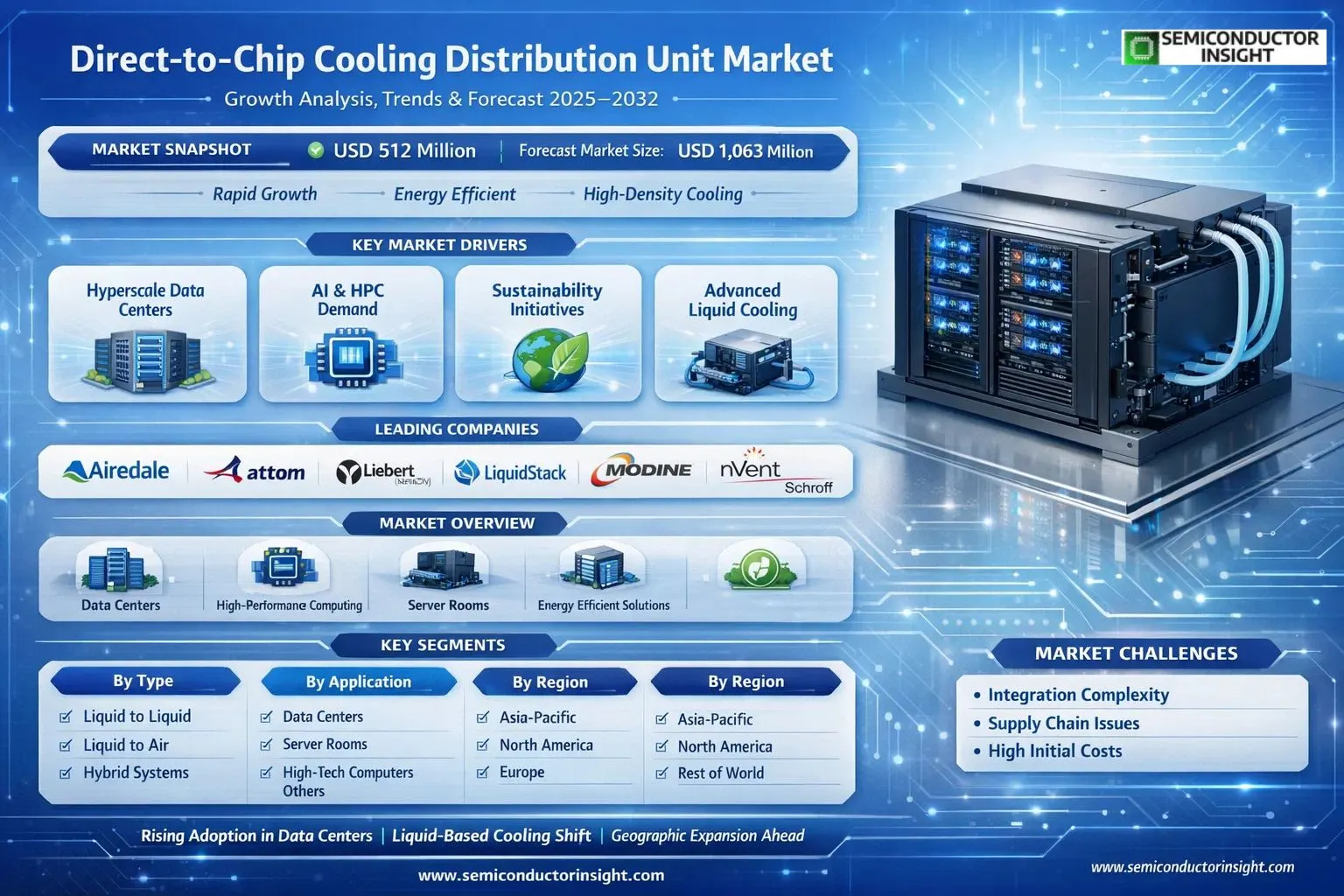

Global Direct-to-Chip Cooling Distribution Unit market size was valued at USD 512 million in 2025. The market is projected to reach USD 1,063 million by 2032, exhibiting a CAGR of 11.3% during the forecast period.

Direct-to-Chip Cooling Distribution Unit is a device specially designed for data center cooling. It achieves efficient heat dissipation by delivering coolant directly to the hotter components of the server, such as the CPU or GPU. The unit is usually located above the heat-generating components of the wiring board and absorbs and removes the heat from the chip through a single-phase cold plate or a two-phase cold plate. These cooling technologies can remove about 70-75% of the heat generated by the equipment in the rack, with the remaining heat managed through air cooling systems or other means.

The market is experiencing rapid growth due to several factors, including surging demand from hyperscale data centers, escalating power densities in servers driven by AI and HPC applications, and a global shift toward energy-efficient cooling to meet sustainability targets. Additionally, advancements in liquid cooling infrastructure are accelerating adoption. Initiatives by key players are fueling further expansion. Airedale, Attom Technology, Liebert, LiquidStack, Modine, and nVent Schroff are prominent companies operating in the market with diverse product portfolios.

MARKET DRIVERS

Surge in Hyperscale Data Centers

Direct-to-Chip Cooling Distribution Unit Market is propelled by the exponential growth of hyperscale data centers, driven by cloud computing demands. Major players like AWS, Google, and Microsoft are investing billions to expand facilities, necessitating advanced cooling solutions for high-density racks exceeding 100kW. Direct-to-chip systems efficiently manage heat dissipation, reducing energy consumption by up to 30% compared to air cooling.

AI and High-Performance Computing Boom

Advancements in AI workloads and high-performance computing (HPC) are key drivers, as GPUs and accelerators generate extreme thermal loads. The market benefits from a projected 25% CAGR through 2030, fueled by training large language models requiring precise coolant distribution to chips. This shift enhances reliability and supports denser server deployments.

➤ Energy efficiency regulations worldwide are accelerating adoption of liquid cooling technologies in Direct-to-Chip Cooling Distribution Unit Market.

Overall, these factors position the market for sustained expansion, with innovations in coolant flow management meeting the needs of next-generation computing infrastructures.

MARKET CHALLENGES

Integration Complexity and Retrofitting

One major challenge in Direct-to-Chip Cooling Distribution Unit Market is the complexity of integrating units into existing data center architectures. Retrofitting legacy air-cooled systems demands significant downtime and engineering expertise, often deterring smaller operators despite efficiency gains.

Other Challenges

Supply Chain Disruptions

Global semiconductor shortages and material constraints for pumps and heat exchangers have delayed deployments, increasing lead times by 20-30% and impacting project timelines in Direct-to-Chip Cooling Distribution Unit Market.Additionally, skilled labor shortages for installation and maintenance pose hurdles, as specialized knowledge in liquid cooling protocols is limited outside major tech hubs.

MARKET RESTRAINTS

High Initial Capital Costs

Direct-to-Chip Cooling Distribution Unit Market faces restraints from elevated upfront investments, with systems costing 2-3 times more than traditional air cooling setups. This deters adoption in cost-sensitive regions and among SMEs, limiting market penetration despite long-term savings.Standardization gaps across vendors further complicate scalability, as incompatible interfaces raise customization expenses. Regulatory hurdles in leak prevention and fluid safety also slow approvals in stringent markets like Europe.Competition from alternative cooling methods, such as immersion systems, adds pressure, fragmenting investments in Direct-to-Chip Cooling Distribution Unit Market.

MARKET OPPORTUNITIES

Expansion into Edge Computing and 5G

Growing edge computing and 5G deployments open vast opportunities for Direct-to-Chip Cooling Distribution Unit Market, where compact, efficient cooling is essential for distributed nodes handling real-time data processing.Emerging markets in Asia-Pacific, with data center investments surpassing $50 billion annually, provide fertile ground for modular DTC units tailored to high-density telecom equipment.Innovations in sustainable, low-GWP coolants align with green data center mandates, positioning the market for partnerships with hyperscalers targeting net-zero goals by 2030.

Direct-to-Chip Cooling Distribution Unit Market Trends

Rising Adoption in Data Centers for Efficient Heat Management

Direct-to-Chip Cooling Distribution Unit Market sees accelerated demand driven by the need for precise cooling in high-density computing environments. These units deliver coolant directly to critical components like CPUs and GPUs, utilizing single-phase or two-phase cold plates positioned above heat-generating areas on server boards. This targeted approach effectively addresses thermal challenges in modern data centers, where traditional air cooling falls short amid rising power densities from AI and cloud workloads.

Other Trends

Shift Toward Liquid-Based Cooling Segments

Within Direct-to-Chip Cooling Distribution Unit Market, liquid-to-liquid and liquid-to-air configurations dominate, catering to diverse operational needs. Liquid-to-liquid units facilitate seamless integration with facility water systems, enhancing overall energy efficiency. Meanwhile, liquid-to-air variants provide hybrid solutions, combining direct chip cooling with supplemental air handling. This segmentation reflects a broader industry pivot from legacy air-only systems to hybrid liquid technologies, optimizing heat rejection while minimizing retrofit complexities.

Geographic Expansion and Competitive Dynamics

Direct-to-Chip Cooling Distribution Unit Market exhibits strong regional variations, with North America leading due to advanced data center infrastructure, followed by rapid growth in Asia, particularly China, Japan, and South Korea. European markets emphasize energy regulations, spurring adoption in Germany and Nordic countries. Key players like Airedale, Liebert, LiquidStack, Modine, and nVent Schroff intensify competition through product innovations and strategic partnerships. Surveys indicate ongoing developments in response to demand surges, pricing pressures, and supply chain optimizations, alongside challenges like integration with existing racks. Applications extend beyond data centers to server rooms and high-tech computers, underscoring versatile deployment potential across sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Direct-to-Chip Cooling Distribution Unit Manufacturers by Revenue Share, 2025

Direct-to-Chip Cooling Distribution Unit Market exhibits a moderately concentrated structure, dominated by a handful of established players holding significant revenue shares. In 2025, the global top five manufacturers, including Liebert (Vertiv), LiquidStack, and Modine, accounted for a substantial portion of the $512 million market valuation. These leaders leverage advanced single-phase and two-phase cold plate technologies to deliver precise coolant distribution to high-heat components like CPUs and GPUs in data centers. Their competitive edge stems from robust R&D, strategic partnerships with hyperscalers, and scalability for high-density racks, where they remove 70-75% of generated heat effectively. Market growth at 11.3% CAGR through 2032 intensifies focus on energy-efficient Liquid-to-Liquid CDUs.

Beyond the frontrunners, niche players like Airedale, Attom Technology, and nVent Schroff carve out positions through specialized innovations tailored for server rooms and high-tech computing applications. Emerging competitors emphasize compact designs and hybrid air-liquid systems, addressing challenges in retrofitting legacy infrastructure. Regional dynamics favor North American and Asian firms, with intensifying rivalry via mergers, product launches, and expansions into China and Europe. This landscape fosters rapid evolution, driven by AI-driven demand for superior thermal management in data centers.

List of Key Direct-to-Chip Cooling Distribution Unit Companies Profiled

- Airedale

- Airedale International Air Conditioning

- Attom Technology

- Liebert (Vertiv)

- LiquidStack

- Modine Manufacturing

- nVent Schroff

- nVent

- CoolIT Systems

- CoolIT Systems

- Asetek

- Iceotope

- ZutaCore

- JetCool

- Chilldyne

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Leading Segment: Liquid to Liquid Cooling Distribution Unit

|

| By Application |

|

Leading Segment: Data Center

|

| By End User |

|

Leading Segment: Cloud Service Providers

|

| By Cooling Technology |

|

Leading Segment: Single-Phase Cooling

|

| By Deployment Type |

|

Leading Segment: Row-Based

|

Regional Analysis: Direct-to-Chip Cooling Distribution Unit Market

North America

Hyperscale data center expansions drive Direct-to-Chip Cooling Distribution Unit Market, with providers prioritizing liquid cooling for AI workloads. Innovation in coolant distribution enhances chip-level thermal control, reducing latency and boosting throughput in cloud environments.

Trends favor scalable distribution units integrated with smart monitoring systems, enabling predictive maintenance. Adoption surges in high-density computing, aligning with energy-efficient strategies amid rising power demands from advanced processors.

Vendors pursue partnerships with OEMs for seamless integration into rack systems. Focus on modular designs supports rapid deployment, while emphasis on low-maintenance units caters to enterprise needs in dynamic data landscapes.

Infrastructure retrofitting poses hurdles, yet innovations in plug-and-play units mitigate retrofit complexities. Regulatory pushes for green cooling propel advancements in eco-friendly refrigerants.

Europe

Europe’s Direct-to-Chip Cooling Distribution Unit Market grows steadily, propelled by stringent energy regulations and green data center mandates. The region prioritizes sustainable thermal solutions amid EU sustainability directives, fostering adoption in colocation facilities. Market dynamics revolve around precision-engineered units that minimize water usage and integrate with renewable energy sources. Leading enterprises collaborate on standardized interfaces to streamline deployments across diverse climates. Trends highlight retrofitting legacy infrastructure with direct-to-chip systems for improved PUE metrics. Business strategies emphasize localized manufacturing to reduce latency in supply chains, while R&D focuses on nanotechnology-enhanced coolants. Northern Europe’s cold climate advantages accelerate liquid cooling shifts, contrasting southern challenges managed through adaptive designs. Overall, Europe’s market balances innovation with compliance, positioning it as a key player in efficient cooling ecosystems.

Asia-Pacific

Asia-Pacific emerges as a dynamic hub in Direct-to-Chip Cooling Distribution Unit Market, fueled by explosive data center builds in cloud hubs like Singapore and Japan. Manufacturing prowess and semiconductor concentration drive demand for advanced distribution units supporting hyperscale expansions. Regional strategies leverage cost-effective scaling, with vendors customizing units for high-density AI servers. Trends toward edge computing in urban centers demand compact, high-flow coolants. Government incentives for digital transformation bolster infrastructure investments, particularly in India and China. Challenges include seismic adaptations in Japan, addressed via resilient designs. Business models prioritize volume production and rapid iteration, enhancing affordability. Asia-Pacific’s market thrives on collaborative ecosystems between tech firms and suppliers, shaping global supply trends.

South America

South America’s Direct-to-Chip Cooling Distribution Unit Market gains traction amid burgeoning cloud adoption in Brazil and emerging digital economies. Infrastructure investments target thermal efficiency in tropical climates, where direct-to-chip units excel in heat rejection. Market dynamics focus on affordable, ruggedized solutions for variable power grids. Trends include hybrid air-liquid systems bridging legacy setups to modern cooling. Regional players partner with international firms for technology transfer, emphasizing training for local deployment. Business strategies stress cost optimization and minimal downtime, vital for e-commerce growth. Sustainability efforts align with regional biodiversity goals through low-GWP refrigerants. South America’s potential lies in telecom expansions, driving niche innovations tailored to connectivity demands.

Middle East & Africa

The Middle East & Africa Direct-to-Chip Cooling Distribution Unit Market accelerates with sovereign data center initiatives in the Gulf and African tech corridors. Harsh climates necessitate robust cooling distributions for mission-critical operations. Trends favor oil-funded hyperscalers adopting liquid solutions for extreme reliability. Business strategies involve PPPs for smart city integrations, prioritizing dust-resistant designs. Africa’s solar-powered edges benefit from efficient units reducing energy footprints. Market growth hinges on skill development and supply chain localization. Regional dynamics blend innovation with resilience, positioning it for future leaps in high-performance computing.

Report Scope

This market research report provides a comprehensive analysis of Direct-to-Chip Cooling Distribution Unit Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of direct-to-chip cooling in managing heat dissipation for high-power chips like CPUs and GPUs in industries such as data centers, high-performance computing, server rooms, and high-tech computers.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Direct-to-Chip Cooling Distribution Unit Market?

-> Direct-to-Chip Cooling Distribution Unit Market was valued at USD 512 million in 2025 and is expected to reach USD 1063 million by 2032, exhibiting a CAGR of 11.3% during the forecast period.

Which key companies operate in Direct-to-Chip Cooling Distribution Unit Market?

-> Key players include Airedale, Attom Technology, Liebert, LiquidStack, Modine, nVent Schroff, among others.

What are the key growth drivers?

-> Key growth drivers include the expansion of data centers, increasing heat generation from CPUs and GPUs, and the need for efficient cooling solutions that remove 70-75% of rack heat.

Which region dominates the market?

-> North America, particularly the U.S., holds a significant share, while Asia, including China, is poised for rapid growth.

What are the emerging trends?

-> Emerging trends include use of single-phase and two-phase cold plates for direct coolant delivery to chips, alongside hybrid cooling with remaining air systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...