MARKET INSIGHTS

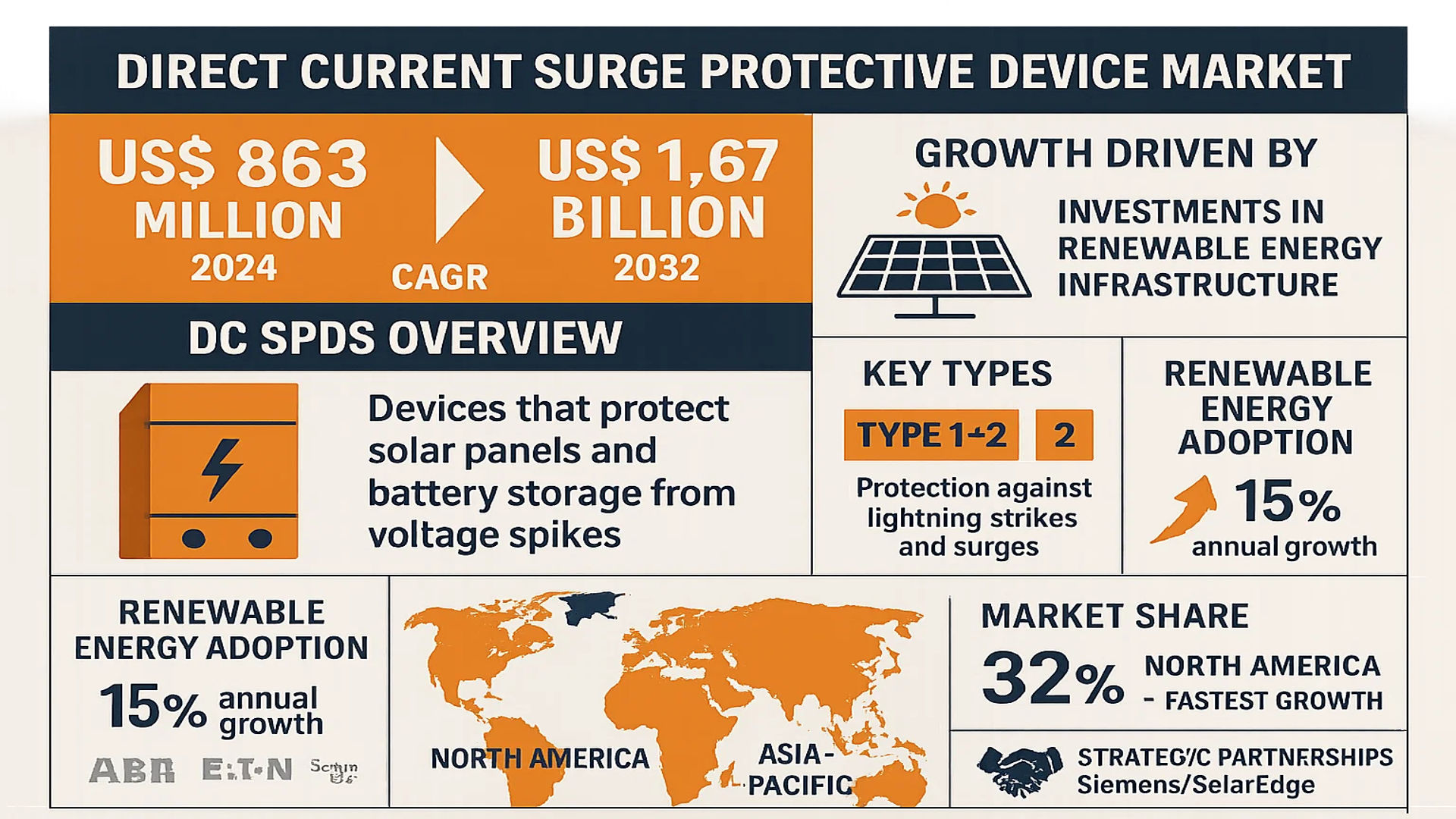

The global Direct Current Surge Protective Device Market size was valued at US$ 863 million in 2024 and is projected to reach US$ 1.67 billion by 2032, at a CAGR of 8.7% during the forecast period 2025-2032. Growth is primarily driven by increasing investments in renewable energy infrastructure, particularly solar power systems, where DC SPDs are critical for protecting sensitive components from voltage spikes.

Direct Current Surge Protective Devices are specialized components designed to safeguard DC electrical systems, such as solar panels and battery storage, from transient overvoltage events. These devices work by diverting excess current away from connected equipment, preventing damage to inverters, charge controllers, and other expensive components. Key types include Type 1+2 and Type 2 SPDs, which offer varying levels of protection against both direct lightning strikes and induced surges.

The market is experiencing significant expansion due to the global shift toward renewable energy adoption, with solar installations growing at 15% annually. North America currently leads in market share (32%), while Asia-Pacific shows the fastest growth trajectory due to large-scale solar projects in China and India. Major players like ABB, Eaton, and Schneider Electric are expanding their DC SPD portfolios through strategic partnerships—such as Siemens’ 2023 collaboration with SolarEdge to develop integrated protection solutions for commercial solar arrays.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Solar Energy Adoption Driving Demand for DC Surge Protection

The global shift toward renewable energy, particularly solar power, has become a significant driver for the Direct Current Surge Protective Device (DC SPD) market. With solar photovoltaic (PV) capacity expected to grow at a CAGR of over 8% through 2030, the need for protecting these systems from voltage surges has intensified. DC SPDs are critical components in solar installations, safeguarding inverters, charge controllers, and battery banks from potentially devastating electrical transients. Recent advancements in solar panel efficiency and energy storage systems have further amplified the requirement for robust surge protection solutions. Large-scale solar farms increasingly incorporate Type 1+2 SPDs as standard protection, with installations in North America and Asia-Pacific leading this trend.

Stringent Electrical Safety Regulations Accelerating Market Penetration

Governments and international standards bodies have implemented rigorous electrical safety protocols that mandate surge protection in DC applications. The International Electrotechnical Commission (IEC) standards 61643-31 and 61643-41 specifically address DC surge protection requirements for photovoltaic systems and low-voltage DC circuits. These regulations compel manufacturers to integrate SPDs in new installations while retrofit markets emerge for older systems. The commercial segment has shown particularly strong compliance-driven adoption, with data centers and telecom infrastructure requiring surge protection to maintain uptime and protect sensitive equipment. This regulatory push has elevated DC SPDs from optional protection to essential system components across industries.

Technological Advancements in SPD Design Enhancing Market Appeal

Innovations in surge protection technology are driving product differentiation and market expansion. Modern DC SPDs now feature advanced thermal protection, remote monitoring capabilities, and extended lifespans exceeding 15 years in some cases. The development of hybrid SPDs that combine multiple protection components into single devices has reduced installation complexity while improving reliability. Leading manufacturers have recently introduced smart SPDs with IoT connectivity, enabling predictive maintenance and real-time performance monitoring. These technological enhancements are particularly valuable in industrial applications where system downtime carries significant financial implications. The market has responded positively to these innovations, with premium-priced advanced SPD models gaining market share despite higher costs.

MARKET RESTRAINTS

High Initial Cost of Advanced DC SPDs Limiting Widespread Adoption

While DC surge protective devices offer essential protection, their premium pricing structure creates barriers to universal adoption. High-quality Type 1+2 combo units can cost 30-50% more than basic models, making them prohibitive for residential users and small-scale commercial projects. The situation is particularly acute in developing markets where price sensitivity remains high and electrical safety budgets are constrained. Furthermore, the total cost of ownership extends beyond device procurement to include installation labor and periodic maintenance, adding financial burdens. This cost barrier often leads to under-protected systems or the use of substandard products that fail during actual surge events, ultimately damaging market reputation.

Complex System Integration Challenges Hindering Market Growth

Integrating DC SPDs into existing electrical infrastructure presents significant technical challenges that restrain market expansion. Solar arrays and battery storage systems require careful coordination between SPDs and other protective devices to create comprehensive protection strategies. Many installers lack the specialized training needed to properly size and place DC SPDs, leading to suboptimal installations. The rapid evolution of DC power systems in renewable energy and electric vehicle charging infrastructure further complicates integration, as protection requirements change with system voltage and topology. These challenges are particularly prevalent in retrofit applications where older electrical systems were not designed with modern surge protection needs in mind.

MARKET OPPORTUNITIES

Expanding EV Charging Infrastructure Creating New Application Areas

The burgeoning electric vehicle market presents significant growth opportunities for DC surge protection solutions. High-power DC fast charging stations operating at 400V or higher require robust surge protection to safeguard both charging equipment and connected vehicles. With global EV charging infrastructure investments projected to increase by 25% annually through 2030, this represents a substantial greenfield market for SPD manufacturers. The automotive industry’s shift toward 800V architectures in next-generation EVs will further drive demand for high-voltage DC protection solutions. Strategic partnerships between SPD manufacturers and charging station providers are already emerging to capitalize on this opportunity.

Smart Grid Deployments Opening New Market Verticals

The modernization of electrical grids with smart technologies creates substantial opportunities for DC SPD applications. Smart grid components like distributed energy resource interfaces, microgrid interconnections, and advanced metering infrastructure increasingly utilize DC power architectures requiring specialized protection. These projects often have generous budgets for reliability-enhancing components, allowing for premium SPD solutions. The integration of renewable energy sources into grid infrastructure has also created demand for customized protection solutions that bridge AC and DC systems. As utilities worldwide accelerate smart grid investments, the addressable market for DC surge protection in this sector continues to expand markedly.

MARKET CHALLENGES

Lack of Standardization Across DC Applications Creating Compatibility Issues

The DC surge protection market faces significant challenges due to varying voltage levels and system architectures across applications. Unlike relatively standardized AC power systems, DC implementations range from low-voltage 48V telecom systems to 1500V solar arrays and beyond. This diversity complicates product development and inventory management for manufacturers while creating confusion among installers. The absence of universal testing standards for DC SPD performance under real-world conditions further exacerbates these issues. Market education becomes increasingly difficult when products designed for one DC application may be unsuitable for another despite superficial similarities.

Performance Verification Difficulties Impacting Market Confidence

Validating the real-world effectiveness of DC surge protection devices presents ongoing challenges for the industry. Unlike AC systems where standardized test waveforms exist, DC applications lack universally accepted testing protocols. Field conditions including varying DC voltages and complex transient patterns make laboratory testing scenarios difficult to develop. This leads to situations where SPDs certified to laboratory standards may underperform in actual installations. The industry has struggled to develop meaningful performance metrics that help end-users compare products across manufacturers and select appropriate protection levels for their specific applications.

DIRECT CURRENT SURGE PROTECTIVE DEVICE MARKET TRENDS

Rising Demand for Solar Energy Solutions Drives Market Growth

The global Direct Current (DC) Surge Protective Device (SPD) market is experiencing significant growth due to the increasing adoption of renewable energy solutions, particularly solar power. DC SPDs play a critical role in protecting sensitive solar components from voltage surges, ensuring system longevity and efficiency. With solar installations projected to grow by over 8% annually through 2030, the demand for reliable surge protection in photovoltaic (PV) systems continues to rise. Furthermore, government incentives for clean energy adoption across North America, Europe, and Asia-Pacific regions are accelerating market expansion.

Other Trends

Technological Advancements in SPD Design

Manufacturers are developing next-generation DC SPDs with enhanced durability and faster response times to meet evolving industry requirements. Recent innovations include modular designs allowing for easier maintenance and remote monitoring capabilities for predictive failure analysis. These advancements are particularly crucial for industrial applications where downtime can result in significant financial losses. The integration of IoT-enabled SPDs that provide real-time performance data is gaining traction among commercial solar farm operators.

Increasing Focus on Grid Modernization Projects

Utilities worldwide are investing heavily in grid modernization to accommodate distributed energy resources, creating substantial opportunities for DC SPD manufacturers. In the United States alone, the Department of Energy has allocated over $3 billion for smart grid enhancement projects that require advanced surge protection components. The transition to smart grids necessitates robust protection solutions capable of handling both AC and DC circuits, as modern grids increasingly incorporate battery storage systems and microgrid architectures.

Growing Industrial Automation Adoption

The expanding industrial automation sector represents another key growth driver for DC SPDs. Manufacturing facilities, data centers, and transportation infrastructure increasingly rely on DC power systems that require protection against electrical disturbances. Between 2024-2032, the market for industrial-grade DC SPDs is expected to grow at a 6.5% CAGR, driven by the digital transformation of traditional manufacturing processes and the expansion of 5G infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Strategize Through Innovation and Expansion

The global Direct Current Surge Protective Device (DC SPD) market features a moderately consolidated competitive structure, with established multinational corporations competing alongside specialized regional players. According to 2024 market data, the top five companies account for approximately 45-50% of total revenue, indicating strong market concentration among industry leaders.

ABB and Siemens currently dominate the sector, leveraging their extensive electrical component portfolios and global distribution networks. ABB’s OVR PV range and Siemens’ 5SVSPD DC series have become industry benchmarks for solar application protection. These market leaders are increasingly focusing on Type 1+2 SPD solutions, which combine lightning and surge protection – a segment projected to grow at a 9.2% CAGR through 2030.

Meanwhile, Schneider Electric and Eaton are making significant inroads through strategic acquisitions and technological partnerships. Schneider’s 2023 acquisition of DC specialist SolarEdge Protection expanded its product capabilities, while Eaton has been innovating in the 1000V DC protection segment to accommodate higher-voltage solar arrays.

Regional players like Phoenix Contact (Germany) and Beny Electric (China) are gaining market share through specialized solutions and competitive pricing strategies. Phoenix Contact’s VAL-US series has become particularly popular in European commercial solar installations, showcasing how mid-size companies can compete through technical specialization.

List of Key Direct Current Surge Protective Device Manufacturers

- ABB Ltd. (Switzerland)

- Eaton Corporation (Ireland)

- Siemens AG (Germany)

- Schneider Electric (France)

- General Electric (U.S.)

- Littelfuse (U.S.)

- Leviton Manufacturing (U.S.)

- Phoenix Contact (Germany)

- Legrand SA (France)

- Beny Electric (China)

The competitive landscape continues to evolve as companies invest in compact design improvements and smart monitoring capabilities for DC SPDs. Future market dynamics will likely be shaped by the increasing integration of IoT functionality and advanced thermal protection systems in next-generation surge protection solutions.

Segment Analysis:

By Type

Type 1+2 Surge Protective Devices Segment Dominates Due to Comprehensive Protection in Renewable Energy Applications

The market is segmented based on type into:

- Type 1+2 Surge Protective Devices

- Subtypes: Combined surge protection for DC power systems, hybrid SPDs

- Type 2 Surge Protective Devices

- Subtypes: Secondary protection devices, standalone DC SPDs

- Specialized DC SPDs

- Subtypes: Solar-specific SPDs, telecom DC SPDs, and others

By Application

Industrial Sector Leads Market Adoption Due to Critical Infrastructure Protection Needs

The market is segmented based on application into:

- Residential

- Commercial

- Industrial

- Utility-Scale Renewable Energy

- Telecommunications

By Power Rating

Medium Voltage Segment Accounts for Significant Share Due to Solar Farm Deployments

The market is segmented based on power rating into:

- Low Voltage SPDs (Below 1kV)

- Medium Voltage SPDs (1kV-5kV)

- High Voltage SPDs (Above 5kV)

By End-Use Industry

Renewable Energy Sector Shows Strongest Growth Potential with Increasing Solar Installations

The market is segmented based on end-use industry into:

- Solar Energy

- Wind Energy

- Telecommunications

- Data Centers

- Transportation Infrastructure

Regional Analysis: Direct Current Surge Protective Device Market

Asia-Pacific

The Asia-Pacific region dominates the global DC SPD market, driven by rapid solar energy adoption and infrastructure modernization. China leads with over 35% of global market share in 2024, fueled by its aggressive renewable energy targets, including 1,200 GW solar capacity by 2030. India follows with rising demand for Type 1+2 SPDs in utility-scale solar projects, supported by initiatives like the Production Linked Incentive (PLI) scheme. Japan and South Korea prioritize advanced DC protection for hybrid energy systems, though high costs of premium brands like Mitsubishi Electric and Fuji Electric limit penetration in price-sensitive markets. While commercial and industrial applications dominate, residential solar adoption is accelerating SPD demand across ASEAN nations.

North America

Stringent safety regulations, including UL 1449 4th Edition standards, and robust solar investments position North America as the second-largest DC SPD market. The U.S. accounts for 80% of regional revenue, with California and Texas driving demand through mandates for surge protection in photovoltaic systems. The Inflation Reduction Act’s $369 billion clean energy funding is accelerating utility-scale solar deployments, benefiting manufacturers like Eaton and Littelfuse. Canada shows slower growth due to prolonged certification processes but is adopting smart SPDs with IoT monitoring for critical infrastructure. Unlike Asia, North American buyers prioritize high-disruption-capacity devices, creating premium pricing opportunities.

Europe

Europe’s mature market focuses on technological differentiation and sustainability compliance. Germany and France lead demand, with IEC 61643-31 standards pushing for SPDs with lower carbon footprints. Solar-plus-storage systems in Nordic countries require specialized DC SPDs capable of handling bidirectional energy flows, with ABB and Siemens capturing 60% of this niche. Southern European nations show price sensitivity, favoring mid-tier Chinese imports despite EU anti-dumping measures. The region is pioneering integration of DC microgrid protections, creating opportunities for modular SPD solutions. However, complex certification requirements across EU member states remain a barrier for new entrants.

Middle East & Africa

The MEA region presents high-growth potential with 46% CAGR forecast for DC SPDs, though from a small base. GCC countries lead through mega solar projects like UAE’s Al Dhafra (2GW) and Saudi’s NEOM, demanding industrial-grade SPDs from Eaton and Schneider Electric. Africa’s off-grid solar boom drives demand for compact, cost-effective SPDs, with South Africa and Kenya adopting localized certification schemes. Political instability in some markets causes supply chain fragmentation, while the lack of standardized regulations results in widespread counterfeit products. Nevertheless, Middle Eastern sovereign wealth funds are increasingly mandating Tier-1 SPDs in infrastructure tenders.

South America

Brazil and Chile account for 70% of South America’s DC SPD market, powered by utility-scale solar auctions and net metering policies. The Brazilian Association of Technical Standards (ABNT) has accelerated adoption by aligning local SPD norms with international benchmarks. Argentina’s economic crisis has stalled projects, though industrial facilities continue importing SPDs for mission-critical operations. The region shows unique demand for lightning-prone area solutions, with Phoenix Contact and locally assembled products gaining traction. High import duties on finished goods have prompted Chinese vendors like Beny Electric to establish regional assembly units.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Direct Current Surge Protective Device (DC SPD) markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global DC SPD market was valued at US$ 863 million in 2024 and is projected to reach US$ 1.67 billion by 2032 at a CAGR of 8.7%.

- Segmentation Analysis: Detailed breakdown by product type (Type 1+2 and Type 2 SPDs), application (residential, commercial, industrial), and voltage range to identify high-growth segments. The Type 1+2 segment is expected to grow at 5.2% CAGR through 2032.

- Regional Outlook: Insights into market performance across North America (U.S. market valued at USD 89.2 million in 2024), Europe, Asia-Pacific (China projected at USD 112.4 million by 2032), Latin America, and Middle East & Africa.

- Competitive Landscape: Profiles of 16 key players including ABB, Eaton, Siemens, Schneider Electric (collectively holding 42% market share), covering product portfolios, R&D investments, and recent M&A activity.

- Technology Trends: Analysis of smart SPDs with IoT integration, advanced metal oxide varistor (MOV) technologies, and solutions for high-voltage DC applications up to 1500V.

- Market Drivers & Restraints: Evaluation of factors including solar energy adoption (global PV capacity reached 1.2 TW in 2024), EV charging infrastructure growth, versus challenges like raw material price volatility.

- Stakeholder Analysis: Strategic insights for solar project developers, electrical equipment manufacturers, and regulatory bodies on compliance with IEC 61643-31 and UL 1449 standards.

The research methodology incorporates primary interviews with 85 industry participants across the value chain, combined with data from regulatory bodies and verified market intelligence platforms.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Direct Current Surge Protective Device Market?

-> Direct Current Surge Protective Device Market size was valued at US$ 863 million in 2024 and is projected to reach US$ 1.67 billion by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Market leaders include ABB, Eaton, Siemens, Schneider Electric, GE, and Littelfuse, with the top 5 players holding 58% market share.

What are the key growth drivers?

-> Primary drivers are renewable energy expansion (global solar installations grew 35% YoY in 2023), EV infrastructure development, and stricter electrical safety regulations.

Which region dominates the market?

-> Asia-Pacific leads with 39% market share in 2024, while North America shows the fastest growth at 5.8% CAGR.

What are the emerging technology trends?

-> Emerging trends include IoT-enabled SPDs for predictive maintenance, hybrid protection technologies, and solutions for 1500V DC solar systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...