MARKET INSIGHTS

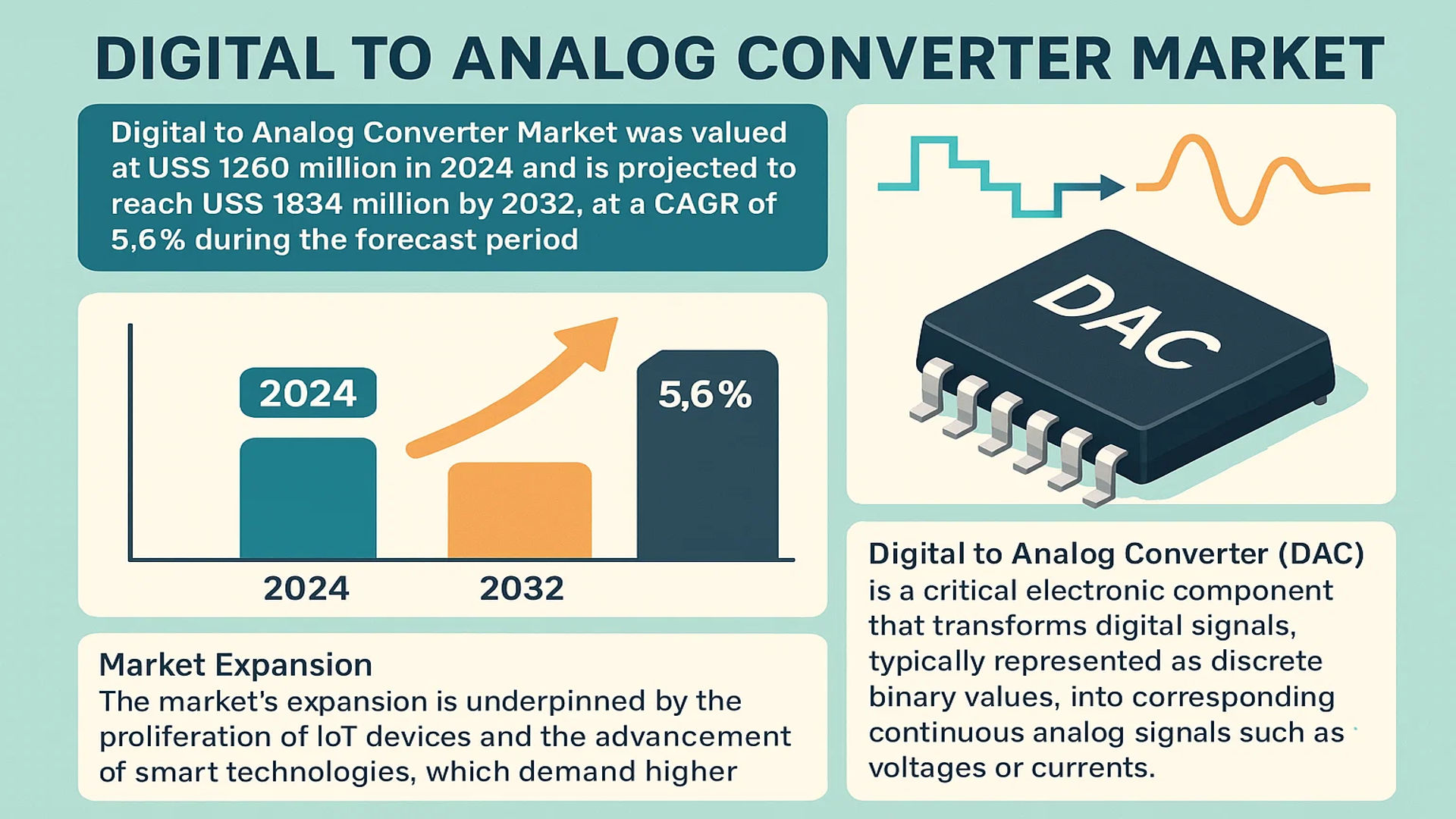

The global Digital to Analog Convertor Market was valued at 1260 million in 2024 and is projected to reach US$ 1834 million by 2032, at a CAGR of 5.6% during the forecast period.

A Digital to Analog Converter (DAC) is a critical electronic component that transforms digital signals, typically represented as discrete binary values, into corresponding continuous analog signals such as voltages or currents. These devices are fundamental for bridging the gap between the digital and physical worlds, enabling applications in high-fidelity audio systems, telecommunications infrastructure, industrial automation, and a vast array of consumer electronics.

The market’s expansion is underpinned by the proliferation of IoT devices and the advancement of smart technologies, which demand higher resolution and faster conversion speeds. Furthermore, the relentless upgrade cycle in consumer electronics, particularly the integration of premium audio features in smartphones and tablets, continues to stimulate demand. The industrial sector also represents a significant growth driver, as it increasingly relies on high-precision DACs for accurate process control and measurement. The market is highly concentrated, with the top four companies—ADI, TI, Microchip, and Renesas Electronics—collectively holding over 95% of the global market share.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT Devices and Smart Infrastructure to Accelerate Market Expansion

The exponential growth of Internet of Things (IoT) deployments across industrial, commercial, and residential sectors is significantly driving demand for digital-to-analog converters. IoT applications require precise signal conversion capabilities to interface between digital control systems and analog sensors/actuators. With over 30 billion active IoT devices projected globally by 2025, the need for high-performance DAC solutions continues to intensify. These converters enable critical functions in smart city infrastructure, industrial automation systems, and connected consumer devices, providing the essential bridge between digital processing units and analog world interfaces. The convergence of 5G connectivity with IoT ecosystems further amplifies this demand, particularly for DACs supporting higher sampling rates and improved signal integrity.

Advancements in Consumer Electronics and Audio Applications to Fuel Growth

The continuous evolution of consumer audio equipment and portable electronics represents a major growth driver for DAC market expansion. High-resolution audio formats and immersive sound experiences require sophisticated digital-to-analog conversion capabilities. The global consumer electronics market, valued at approximately $1 trillion annually, increasingly incorporates premium audio features across smartphones, tablets, wearables, and home entertainment systems. This trend drives demand for advanced DAC solutions that deliver superior signal-to-noise ratios, lower distortion, and enhanced power efficiency. Manufacturers are responding by developing integrated DAC solutions that support multiple audio formats while minimizing footprint and power consumption, enabling thinner device designs and longer battery life.

Furthermore, the gaming industry’s shift toward virtual reality and high-fidelity audio experiences creates additional demand for precision DAC components. These applications require ultra-low latency conversion and high dynamic range to maintain immersive user experiences.

➤ For instance, leading smartphone manufacturers now incorporate dedicated high-performance DAC chips to support lossless audio streaming and advanced noise cancellation features, driving premium segment growth.

The automotive sector’s integration of advanced infotainment and acoustic vehicle alerting systems further contributes to market expansion, with electric vehicle manufacturers particularly emphasizing premium audio experiences as differentiation factors.

Industrial Automation and Industry 4.0 Implementation to Drive Precision Demand

The global transition toward Industry 4.0 and smart manufacturing practices is creating substantial demand for high-precision digital-to-analog converters. Modern industrial automation systems require accurate control signals for motor drives, process control instrumentation, and robotic systems. DACs with 16-bit resolution or higher are increasingly necessary to achieve the precision required in advanced manufacturing environments. The industrial segment accounts for approximately 35% of total DAC market revenue, reflecting its critical role in automation infrastructure. As manufacturing facilities upgrade to smarter, more connected systems, the demand for robust DAC solutions that can operate reliably in harsh industrial environments continues to grow.

Moreover, the expansion of industrial IoT applications and predictive maintenance systems requires DAC components that can interface with various analog sensors while maintaining accuracy over extended temperature ranges and operational conditions.

MARKET RESTRAINTS

Technical Complexity and Design Integration Challenges to Hinder Market Penetration

While digital-to-analog converter technology continues advancing, implementation complexity remains a significant market restraint. Designing DAC systems requires sophisticated understanding of mixed-signal electronics, noise reduction techniques, and thermal management. System integrators often face challenges related to signal integrity, clock jitter, and electromagnetic interference when incorporating high-resolution DACs into complex electronic systems. These technical hurdles can prolong development cycles and increase overall system costs, particularly for applications requiring precision performance. The need for specialized engineering expertise creates additional barriers, as experienced mixed-signal design professionals remain scarce relative to market demand.

Additionally, achieving optimal performance often requires careful PCB layout considerations, specialized power supply designs, and advanced filtering components, adding complexity to end-product development.

Price Sensitivity in Consumer Markets to Limit Premium DAC Adoption

Intense cost pressure in consumer electronics and mass-market applications represents a considerable restraint for premium DAC solutions. While high-performance converters offer superior specifications, many price-sensitive market segments prioritize cost reduction over performance enhancement. This particularly affects consumer audio applications, where manufacturers often utilize integrated codec solutions rather than discrete high-performance DAC components to maintain competitive pricing. The consumer electronics segment typically operates with razor-thin margins, driving manufacturers to minimize bill-of-materials costs wherever possible. This economic reality limits adoption of advanced DAC solutions despite their technical advantages, particularly in entry-level and mid-range product categories.

Furthermore, the increasing integration of DAC functionality into system-on-chip designs reduces opportunities for discrete converter solutions in cost-sensitive applications.

MARKET CHALLENGES

Technological Obsolescence and Rapid Innovation Cycles to Challenge Market Stability

The DAC market faces continuous challenges from rapid technological evolution and shortening product life cycles. Converter specifications that represented state-of-the-art performance five years ago now qualify as standard requirements, forcing manufacturers to constantly innovate while maintaining competitive pricing. This rapid pace of technological advancement requires substantial ongoing research and development investment, particularly for companies competing in high-performance segments. The challenge is compounded by increasing integration trends, where DAC functionality becomes incorporated into larger semiconductor solutions, potentially reducing demand for discrete components. Manufacturers must balance performance improvements with cost considerations while anticipating future market requirements.

Other Challenges

Supply Chain Vulnerabilities

Global semiconductor supply chain disruptions continue to challenge DAC availability and pricing. Geopolitical factors, manufacturing capacity constraints, and material shortages create uncertainty in component availability, affecting production planning and time-to-market for end products requiring DAC solutions.

Standardization and Compatibility Issues

The absence of universal interface standards across applications creates integration challenges. Different industries utilize various communication protocols and interface requirements, forcing DAC manufacturers to maintain diverse product portfolios and increasing development complexity.

MARKET OPPORTUNITIES

Emerging Automotive Electronics and Electric Vehicle Systems to Create New Growth Avenues

The automotive industry’s transformation toward electrification and advanced driver assistance systems presents significant opportunities for DAC market expansion. Modern vehicles incorporate numerous electronic systems requiring precision analog outputs, including battery management systems, sensor interfaces, and advanced display technologies. The growing adoption of electric vehicles, which utilize approximately twice the semiconductor content of conventional vehicles, particularly benefits DAC manufacturers. These applications require robust converters capable of operating in automotive temperature ranges while meeting stringent reliability standards. The automotive DAC segment is projected to grow substantially as vehicle electrification accelerates and autonomous driving technologies advance.

Additionally, the integration of sophisticated audio systems and cabin experience technologies in premium vehicles drives demand for high-performance audio DAC solutions with multiple channels and advanced processing capabilities.

Medical Device Innovation and Healthcare Digitalization to Drive Precision Requirements

The healthcare sector’s ongoing digital transformation creates substantial opportunities for high-precision DAC applications. Medical imaging equipment, patient monitoring systems, and diagnostic instruments require exceptional signal accuracy and stability. The global medical devices market, growing consistently amid aging populations and increased health awareness, utilizes DAC components in various applications from ultrasound machines to laboratory analyzers. These applications often require specialized converters meeting medical safety standards and providing enhanced reliability. The trend toward portable and wearable medical devices further drives demand for low-power, small-form-factor DAC solutions that can maintain precision while operating on battery power.

Furthermore, telemedicine expansion and remote patient monitoring systems create additional opportunities for DAC integration into distributed healthcare infrastructure.

5G Infrastructure Deployment and Communications Equipment to Fuel Advanced DAC Demand

The global rollout of 5G networks and subsequent communication infrastructure upgrades represents a significant growth opportunity for high-speed DAC solutions. 5G systems require sophisticated signal processing capabilities, including advanced digital-to-analog conversion for both baseband and radio frequency applications. The massive multiple-input multiple-output technology fundamental to 5G performance utilizes numerous DAC channels simultaneously, driving demand for multi-channel converter solutions. Network equipment manufacturers require DAC components supporting higher sampling rates, improved linearity, and enhanced power efficiency to meet 5G performance specifications while controlling operational costs.

Additionally, the ongoing expansion of fiber optic networks and broadband infrastructure creates parallel opportunities for DAC applications in optical communication systems and network interface equipment.

DIGITAL TO ANALOG CONVERTOR MARKET TRENDS

Proliferation of IoT and Smart Infrastructure to Emerge as a Dominant Trend

The proliferation of Internet of Things (IoT) devices and the accelerated development of smart city infrastructure are fundamentally reshaping the demand landscape for Digital-to-Analog Converters (DACs). These applications necessitate DACs that are not only high-performance but also exceptionally power-efficient, driving innovation toward higher resolution and faster conversion speeds. For instance, the global number of connected IoT devices is projected to exceed 29 billion by 2027, creating an immense installed base requiring sophisticated signal conversion. This surge is directly fueling the development of advanced DAC architectures capable of handling complex data processing tasks in real-time within constrained power budgets. Furthermore, the integration of AI at the edge for predictive maintenance and data analytics in industrial IoT settings places additional performance demands on data conversion subsystems, making the role of the DAC more critical than ever.

Other Trends

Miniaturization and Higher Integration

A pronounced trend across the electronics industry, the relentless drive toward miniaturization, is profoundly impacting DAC design and packaging. Technological innovations are advancing system-in-package (SiP) and multi-chip module (MCM) techniques, enabling DACs to provide more channels and functionalities within increasingly confined spaces. This is particularly critical for portable consumer electronics and compact industrial sensors where board real estate is at a premium. The market is witnessing a shift toward highly integrated mixed-signal ICs that combine DACs with other functionalities like amplifiers and microcontrollers, reducing the overall component count and system footprint. This trend is a direct response to the demand for smaller, more powerful, and more energy-efficient end products.

Advancements in Next-Generation Communication and Automotive Systems

The global rollout of 5G infrastructure and the rapid development of autonomous driving technologies are creating a new frontier of requirements for DACs, emphasizing unparalleled real-time performance and reliability. In 5G massive MIMO (Multiple Input Multiple Output) base stations, high-speed, high-resolution DACs are essential for generating the complex waveforms required for beamforming and achieving higher data throughput. Similarly, in automotive applications, the evolution toward Level 3 and Level 4 autonomy is increasing the number of sensors per vehicle—LiDAR, radar, and high-resolution imaging systems all rely on precise analog signal generation for accurate environmental perception. This is promoting the research and development of new DAC architectures that offer stronger interference resistance, higher stability over wide temperature ranges, and lower latency to meet the stringent safety and performance standards of these advanced applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global Digital-to-Analog Converter (DAC) market exhibits a highly consolidated competitive structure, dominated by a handful of major semiconductor manufacturers. This consolidation is primarily because the market demands significant investment in research and development, advanced fabrication facilities, and extensive intellectual property portfolios. Analog Devices, Inc. (ADI) and Texas Instruments (TI) are the unequivocal leaders, collectively commanding a substantial portion of the global revenue share. Their dominance is anchored in decades of technological expertise, a vast and diverse product portfolio catering to nearly every application segment, and a robust global distribution and support network that serves customers from consumer electronics to aerospace.

Microchip Technology Inc. and Renesas Electronics Corporation also hold significant market positions. Their growth strategy often focuses on providing highly integrated solutions and microcontrollers with embedded DAC functionality, which is particularly appealing for space-constrained and cost-sensitive applications in the automotive and industrial sectors. Furthermore, these companies are aggressively expanding their manufacturing capacities and engaging in strategic acquisitions to bolster their analog semiconductor offerings, ensuring they remain competitive against the top players.

Additionally, these leading companies are continuously driving innovation through substantial R&D investments. Their initiatives are focused on developing next-generation DACs that offer higher resolution, lower power consumption, and enhanced integration to meet the evolving demands of 5G infrastructure, autonomous vehicles, and high-end audio equipment. Geographical expansion into high-growth regions, particularly Asia-Pacific, and a constant stream of new product launches are expected to be key strategies for these players to grow their market share over the forecast period.

Meanwhile, other notable players like STMicroelectronics and ROHM Semiconductor are strengthening their market presence. They compete effectively in niche segments and specific regional markets by focusing on specialized, high-performance DACs and forging strategic partnerships with key OEMs. Their efforts in developing energy-efficient and robust solutions for automotive and industrial applications are crucial for their sustained growth within this competitive landscape.

List of Key Digital-to-Analog Converter Companies Profiled

- Analog Devices, Inc. (ADI) (U.S.)

- Texas Instruments Incorporated (TI) (U.S.)

- Microchip Technology Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- ESS Technology, Inc. (U.S.)

- Nisshinbo Micro Devices Inc. (Japan)

- ROHM Semiconductor (Japan)

- STMicroelectronics (Switzerland)

Segment Analysis:

By Type

R-2R Ladder DACs Segment Dominates the Market Due to Superior Linearity and High-Resolution Performance

The market is segmented based on type into:

- R-2R Ladder DACs

- Sigma-Delta DACs

- Current-Steering DACs

- Multiplying DACs

- Others

By Application

Industrial Segment Leads Due to Critical Role in Automation, Process Control, and Precision Measurement Systems

The market is segmented based on application into:

- Industrial

- Communications

- Automotive

- Consumer Electronics

- Medical

- Others

By Resolution

High-Resolution DACs (16-bit and Above) Segment Gains Traction for Demanding Applications in Audio and Instrumentation

The market is segmented based on resolution into:

- 8-bit and Below

- 9-bit to 14-bit

- 15-bit to 18-bit

- 19-bit and Above

By Channel

Multi-Channel DACs Segment Expands with Growth in Multi-Sensor Systems and Complex Data Acquisition Setups

The market is segmented based on channel into:

- Single Channel

- Dual Channel

- Quad Channel

- Octal Channel and Above

Regional Analysis: Digital to Analog Converter Market

Asia-Pacific

The Asia-Pacific region dominates the global DAC market, accounting for approximately 45% of total consumption. This leadership position is driven by massive electronics manufacturing ecosystems in China, Japan, South Korea, and Taiwan, coupled with rapid industrialization across India and Southeast Asia. The region benefits from strong government support for semiconductor manufacturing initiatives, such as China’s “Made in China 2025” policy and India’s Semiconductor Mission with its $10 billion incentive package. While cost sensitivity remains a factor, there is growing demand for high-performance DACs in automotive electronics, industrial automation, and consumer devices. The proliferation of 5G infrastructure and IoT deployments further accelerates DAC adoption, though supply chain dependencies and intellectual property challenges persist.

North America

North America represents a technologically advanced DAC market characterized by high-value applications and innovation-driven demand. The region’s strong semiconductor design capabilities, particularly in the United States, drive development of precision DACs for aerospace, defense, and medical equipment applications. Major technology companies’ investments in data centers and cloud infrastructure—projected to exceed $50 billion annually—create substantial demand for high-speed data conversion solutions. While the market faces cost pressures and supply chain vulnerabilities, ongoing research in quantum computing and advanced communications ensures continued demand for cutting-edge DAC technologies with enhanced resolution and lower power consumption.

Europe

Europe maintains a robust DAC market focused on high-reliability applications and environmental compliance. Stringent EU regulations regarding electronic waste and energy efficiency drive innovation in low-power DAC designs, particularly for automotive and industrial applications. The region’s strong automotive industry, with its transition toward electric and autonomous vehicles, requires sophisticated DAC solutions for sensor systems and infotainment. European research initiatives like the Horizon Europe program foster development of advanced semiconductor technologies, though the market faces challenges from global competition and complex regulatory requirements. Germany, France, and the UK remain key markets, with growing demand from renewable energy and medical technology sectors.

South America

The South American DAC market is emerging, characterized by gradual technological adoption and infrastructure development. Brazil and Argentina represent the primary markets, driven by industrial automation investments and growing consumer electronics penetration. Economic volatility and import dependencies create challenges for consistent technology adoption, though local manufacturing initiatives are gaining traction. The region shows potential in agricultural technology and renewable energy applications, where precision DACs are increasingly required. While adoption of advanced DAC solutions lags behind other regions, increasing digitalization efforts and infrastructure projects suggest steady long-term growth opportunities.

Middle East & Africa

This region represents a developing DAC market with significant growth potential despite current limitations. Infrastructure development projects in Gulf Cooperation Council countries, particularly in smart city initiatives and telecommunications, drive demand for basic to mid-range DAC solutions. South Africa and Israel show more advanced adoption patterns due to their established technology sectors. The market faces challenges including limited local semiconductor manufacturing, reliance on imports, and budget constraints across many African nations. However, increasing investments in digital infrastructure and industrial automation, coupled with growing technology transfer partnerships, indicate promising long-term development for DAC applications in energy management, communications, and basic industrial systems.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Digital to Analog Converter (DAC) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Digital to Analog Converter Market?

-> Digital to Analog Convertor Market was valued at 1260 million in 2024 and is projected to reach US$ 1834 million by 2032, at a CAGR of 5.6% during the forecast period.

Which key companies operate in Global Digital to Analog Converter Market?

-> Key players include Analog Devices Inc. (ADI), Texas Instruments (TI), Microchip Technology, Renesas Electronics, ESS Technology, Nisshinbo Micro Devices, ROHM Semiconductor, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include proliferation of IoT devices, advancement of smart home and smart city projects, consumer electronics upgrade cycles, and increasing demand for high-precision DAC solutions in industrial automation.

Which region dominates the market?

-> Asia-Pacific is the largest market, accounting for approximately 45% of global market share, while North America and Europe collectively hold over 45% market share.

What are the emerging trends?

-> Emerging trends include higher integration, lower power consumption, smaller form factors, miniaturization packaging techniques, development of DACs with stronger interference resistance for 5G and autonomous driving applications, and energy-efficient DAC solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...