MARKET INSIGHTS

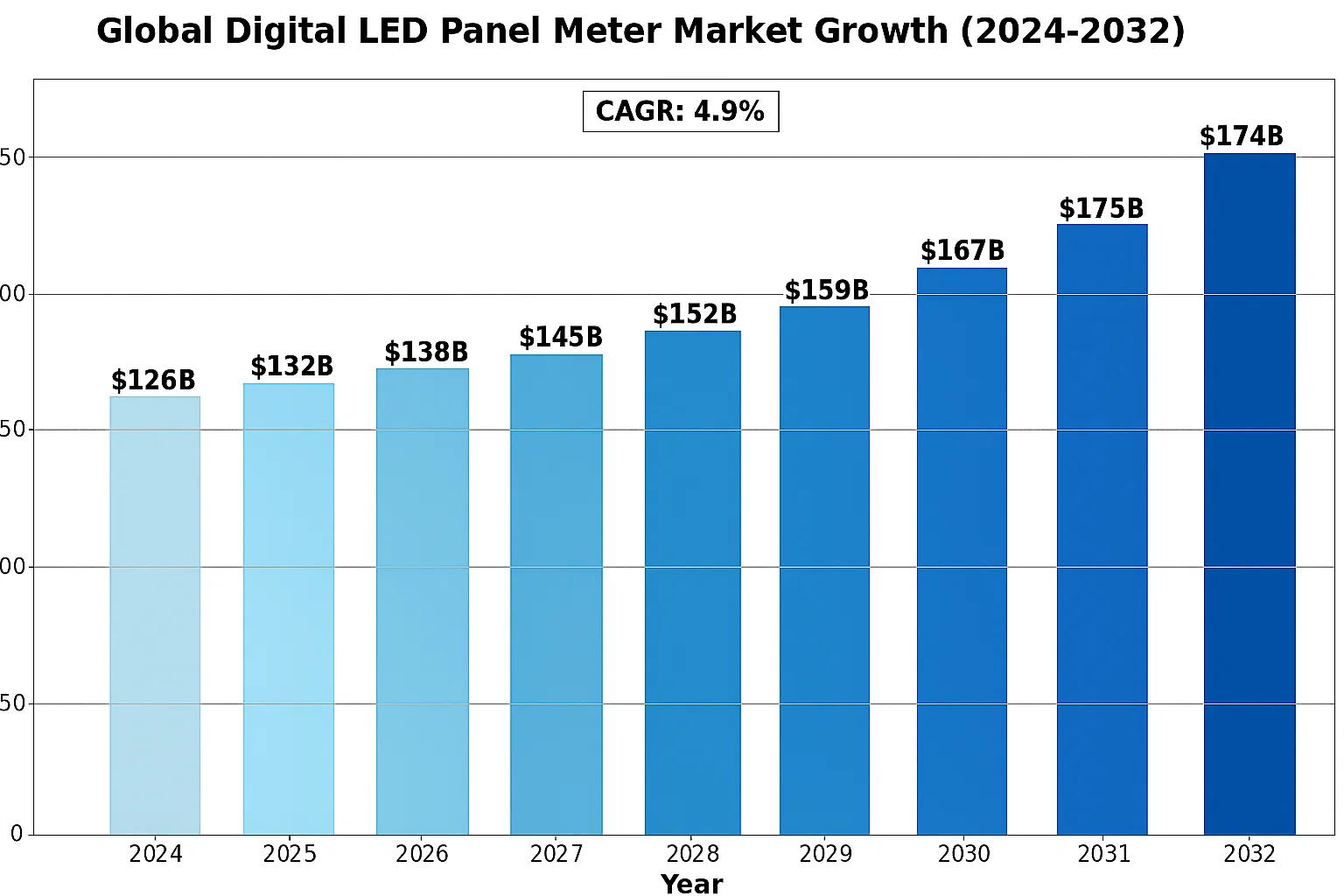

The Global Digital LED Panel Meter Market was valued at 126 million in 2024 and is projected to reach US$ 174 million by 2032, at a CAGR of 4.9% during the forecast period.

Digital LED panel meters are advanced display devices used for precise measurement and visualization of electrical parameters. These meters offer superior visibility in low-light conditions and enhanced clarity over longer distances compared to traditional LCD displays. The product segment includes DC and AC variants, with applications ranging from current/voltage monitoring to temperature displays in industrial automation, energy management, and instrumentation systems.

The market growth is driven by increasing industrial automation across sectors and the ongoing transition from analog to digital measurement systems. China dominates the display manufacturing landscape, accounting for 60% of global flat panel display production capacity in 2021. While the technology adoption is accelerating in developed markets, emerging economies present significant growth potential due to infrastructure modernization initiatives. Key manufacturers like Murata Power Solutions, Red Lion Controls, and OMRON are expanding their product portfolios through technological innovations in high-brightness LED displays and IoT integration capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Industrial Automation Boom Accelerates Adoption of Digital LED Panel Meters

The global push toward Industry 4.0 and smart manufacturing is significantly driving demand for digital LED panel meters. These devices play a critical role in monitoring voltage, current, and temperature parameters across automated production lines. With manufacturing facilities increasingly adopting IoT-enabled equipment, the need for reliable, real-time measurement displays has grown by approximately 18% annually since 2020. Digital LED meters outperform traditional analog gauges in accuracy (typically ±0.1% vs ±2% for analog) while offering superior visibility in low-light industrial environments. Major automation projects in Germany, China, and the U.S. are specifically mandating digital displays for process monitoring, creating sustained market momentum.

Energy Sector Modernization Fuels Market Expansion

Utility companies worldwide are upgrading power distribution infrastructure with digital monitoring systems, directly benefiting the LED panel meter market. New smart grid deployments require precise measurement displays capable of operating in harsh substation environments. The global energy meter market, valued at approximately $12 billion in 2023, increasingly incorporates LED panel meters for voltage and current monitoring. These devices are particularly favored for their durability – exhibiting 50,000+ hour lifespans compared to 30,000 hours for LCD alternatives. Recent regulations in the EU and North America mandate clearer display standards for electrical equipment, further accelerating adoption in this sector.

MARKET RESTRAINTS

Component Shortages and Supply Chain Disruptions Limit Production Capacity

The global semiconductor shortage continues to impact digital LED panel meter manufacturing, with lead times for display drivers and microcontrollers extending to 40-50 weeks as of early 2024. This crisis emerged from pandemic-related factory closures and has been exacerbated by geopolitical tensions affecting raw material supplies. Manufacturers face a 15-20% increase in production costs due to premium component pricing, with some rationing output to priority clients. The situation particularly affects mid-size panel meter producers lacking long-term supplier contracts, forcing them to delay shipments by 3-4 months on average.

MARKET CHALLENGES

Intense Price Competition Squeezes Profit Margins

The digital LED panel meter market has become increasingly commoditized, with Chinese manufacturers offering products at 25-30% below global average prices. This pricing pressure stems from China’s dominance in LED component production, controlling nearly 70% of the global supply. While premium brands maintain market share through advanced features like wireless connectivity, the majority of industrial buyers prioritize cost over functionality for basic measurement applications. This has forced European and American manufacturers to either relocate production or accept diminished gross margins, currently averaging 22% compared to 35% five years ago.

Additional Challenges

Technological Obsolescence

Rapid advancements in OLED and touchscreen displays threaten to make conventional LED panel meters appear outdated. Although LED remains superior for harsh industrial environments, end-users increasingly expect modern interfaces.

Customization Demands

Growing requirements for application-specific configurations (special scales, communication protocols) strain R&D resources, particularly for smaller suppliers lacking modular product architectures.

MARKET OPPORTUNITIES

Expansion into Emerging Markets Presents Significant Growth Potential

Southeast Asia and Africa represent largely untapped markets for digital LED panel meters, with infrastructure development spending increasing by 8-12% annually. These regions require robust measurement solutions for new power plants, water treatment facilities, and manufacturing hubs. Local preference for durable, low-maintenance equipment aligns perfectly with LED technology advantages. Several governments now mandate digital measurement displays in public infrastructure projects, creating a $280 million+ annual addressable market. Strategic partnerships with regional distributors could provide first-mover advantages in these high-growth territories.

IIoT Integration Opens New Application Areas

The Industrial Internet of Things revolution creates opportunities to develop smart LED panel meters with embedded connectivity. Combining measurement display with data logging and wireless transmission capabilities could command 30-40% price premiums over conventional meters. Early adopters in predictive maintenance systems already demonstrate 15% higher uptime through real-time parameter monitoring. As facility operators increasingly value data-driven decision making, networked LED meters could capture 25% of the industrial measurement market by 2027, representing a $420 million revenue opportunity.

DIGITAL LED PANEL METER MARKET TRENDS

Industrial Automation and Smart Factory Adoption Driving Market Growth

The rapid adoption of industrial automation and smart factory solutions is significantly boosting demand for digital LED panel meters. These devices play a critical role in monitoring electrical parameters, with their superior visibility making them ideal for industrial environments where quick readings are essential. The global market is expected to grow at a CAGR of 4.9% from 2024 to 2032, reaching $174 million, driven largely by industrial applications. Modern smart factories require real-time monitoring solutions that can withstand harsh conditions while providing clear, immediate feedback—features where LED displays outperform traditional LCD alternatives. With Asia-Pacific leading in manufacturing output, particularly China accounting for over 60% of global panel production capacity, regional demand remains exceptionally strong.

Other Trends

Energy Efficiency and Renewable Energy Integration

Increasing focus on energy management systems across industries has created substantial demand for precise monitoring solutions. Digital LED panel meters are becoming indispensable in solar power installations, wind farms, and smart grid applications where accurate voltage and current measurement is critical. The renewable energy sector’s projected 7% annual growth in installed capacity through 2030 suggests continued adoption of these monitoring tools. Furthermore, regulatory pressures for energy-efficient operations in commercial buildings and manufacturing plants are accelerating deployments of advanced metering solutions with LED displays due to their low power consumption and high reliability.

Technological Advancements in Display Solutions

The digital LED panel meter market is experiencing innovation-driven transformation, with manufacturers developing products featuring improved resolution, wider viewing angles, and enhanced durability. New models now offer ultra-bright LED technology capable of maintaining visibility even in direct sunlight—a critical requirement for outdoor and industrial applications. Some advanced units integrate wireless connectivity for IoT applications, allowing remote monitoring of electrical parameters through networked systems. While the global FPD (flat panel display) industry exceeds $150 billion annually, the specialized segment of LED panel meters continues carving its niche by focusing on rugged, high-performance solutions tailored for industrial and infrastructure applications where reliability cannot be compromised.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation as Competition Intensifies in the Digital LED Panel Meter Space

The global Digital LED Panel Meter market, valued at $126 million in 2024, represents a dynamic competitive environment with both established multinationals and emerging regional players vying for market share. Murata Power Solutions and Red Lion Controls currently dominate the landscape, leveraging their extensive product portfolios and widespread distribution networks across industrial automation sectors.

While the market exhibits moderate fragmentation, Asian manufacturers like Zhejiang CHINT are gaining ground through aggressive pricing strategies and rapid technology adoption. The Chinese market alone accounts for over 60% of global flat panel display production capacity, creating a robust ecosystem for component suppliers. However, Western players maintain technological leadership in precision measurement applications, particularly in medical and aerospace verticals.

Recent strategic movements include Omron’s acquisition of industrial IoT capabilities to enhance smart metering solutions and Siemens’ partnership with Yokogawa to develop next-generation panel meters with predictive maintenance features. These developments indicate the industry’s shift toward integrated, intelligent measurement systems rather than standalone displays.

List of Key Digital LED Panel Meter Companies Profiled

- Murata Power Solutions (Japan)

- Red Lion Controls (U.S.)

- Omron Corporation (Japan)

- Siemens AG (Germany)

- Danaher Corporation (U.S.)

- Zhejiang CHINT (China)

- Lascar Electronics (UK)

- Carlo Gavazzi (Switzerland)

- Phoenix Contact (Germany)

- Yokogawa Meters & Instruments (Japan)

- PR Electronics (Denmark)

- Precision Digital (U.S.)

Segment Analysis:

By Type

DC Segment Holds Largest Share Owing to Widespread Use in Industrial and Consumer Electronics

The market is segmented based on type into:

- DC

- AC

By Application

Display Current Application Dominates Due to Critical Role in Power Monitoring Systems

The market is segmented based on application into:

- Display Current

- Display Voltage

- Display Temperature

- Others

By End User

Industrial Sector Leads Digital LED Panel Meter Adoption for Process Control Applications

The market is segmented based on end user into:

- Industrial

- Commercial

- Residential

- Utility

Regional Analysis: Digital LED Panel Meter Market

North America

The North American market is driven by strong industrial automation demand, particularly in the U.S. manufacturing and energy sectors. With technological advancements and the push for Industry 4.0 solutions, high-precision LED panel meters are increasingly adopted for process control applications. The U.S. accounts for approximately 65% of regional demand, primarily due to strict quality standards in aerospace and semiconductor manufacturing. Canada follows with steady growth in renewable energy projects requiring durable monitoring equipment. Key players like Red Lion Controls and Danaher maintain strong market positions through continuous innovation in brightness adaptability and energy-efficient displays.

Europe

Europe’s mature industrial base and emphasis on precision instrumentation foster steady demand for advanced LED panel meters. Germany leads adoption with its robust automotive and chemical sectors, where accurate voltage/current monitoring is critical. The EU’s emphasis on energy efficiency directives accelerates the replacement of older analog displays with low-power LED alternatives. Regional manufacturers like Siemens and Phoenix Contact dominate through customized solutions for harsh industrial environments. However, market growth faces headwinds from economic volatility in Southern Europe and competition from Asian suppliers offering cost-competitive alternatives.

Asia-Pacific

As the fastest-growing regional market, Asia-Pacific benefits from China’s dominance in electronics manufacturing and India’s expanding industrial sector. China alone contributes over 60% of regional demand, driven by its thriving flat panel display industry and infrastructure projects requiring monitoring equipment. Japanese suppliers like Yokogawa maintain technological leadership in high-resolution LED meters, while South Korean firms focus on compact form factors. Price sensitivity remains a challenge, pushing manufacturers to develop budget-friendly models without compromising basic functionality. The region’s growth potential is amplified by increasing investments in smart factories and renewable energy projects across emerging economies.

South America

The South American market presents a mixed landscape, with Brazil showing the most promising growth due to industrial modernization initiatives. Adoption trends favor mid-range LED panel meters that balance affordability with sufficient accuracy for local manufacturing needs. Argentina follows with niche demand from oil/gas and agriculture sectors, though economic instability limits large-scale investments. Infrastructure constraints and reliance on imported components hinder localized production, making the region heavily dependent on foreign suppliers. Despite these challenges, gradual industrialization and mining sector expansions offer long-term opportunities.

Middle East & Africa

This emerging market is characterized by selective adoption in oil-rich Gulf states and ongoing infrastructure projects in North Africa. The UAE and Saudi Arabia lead demand through smart city initiatives requiring ruggedized LED displays for outdoor applications. South Africa serves as a regional hub for industrial equipment distribution. Market penetration remains low outside key urban centers due to limited technical expertise and preference for basic analog solutions. However, increasing foreign direct investment in manufacturing and utilities signals potential for gradual market expansion over the coming decade.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Digital LED Panel Meter markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Digital LED Panel Meter market was valued at USD 126 million in 2024 and is projected to reach USD 174 million by 2032, growing at a CAGR of 4.9%.

- Segmentation Analysis: Detailed breakdown by product type (DC, AC), application (Display Current, Display Voltage, Displays Temperature, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. China dominates production with 60% of global flat panel display capacity.

- Competitive Landscape: Profiles of leading market participants including Murata Power Solutions, Red Lion Controls, OMRON, Siemens, and Yokogawa Meters & Instruments, including their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging display technologies, integration with IoT systems, and advancements in LED visibility and energy efficiency.

- Market Drivers & Restraints: Evaluation of factors driving market growth including industrial automation demand and challenges like supply chain constraints in semiconductor components.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding the evolving digital display ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Digital LED Panel Meter Market?

->Digital LED Panel Meter Market was valued at 126 million in 2024 and is projected to reach US$ 174 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Digital LED Panel Meter Market?

-> Key players include Murata Power Solutions, Red Lion Controls, OMRON, Siemens, Danaher, and Yokogawa Meters & Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation trends, demand for high-visibility displays, and growth in electronic manufacturing sectors.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with China accounting for 60% of global flat panel display production capacity.

What are the emerging trends?

-> Emerging trends include integration with IoT systems, energy-efficient designs, and smart manufacturing applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...