MARKET INSIGHTS

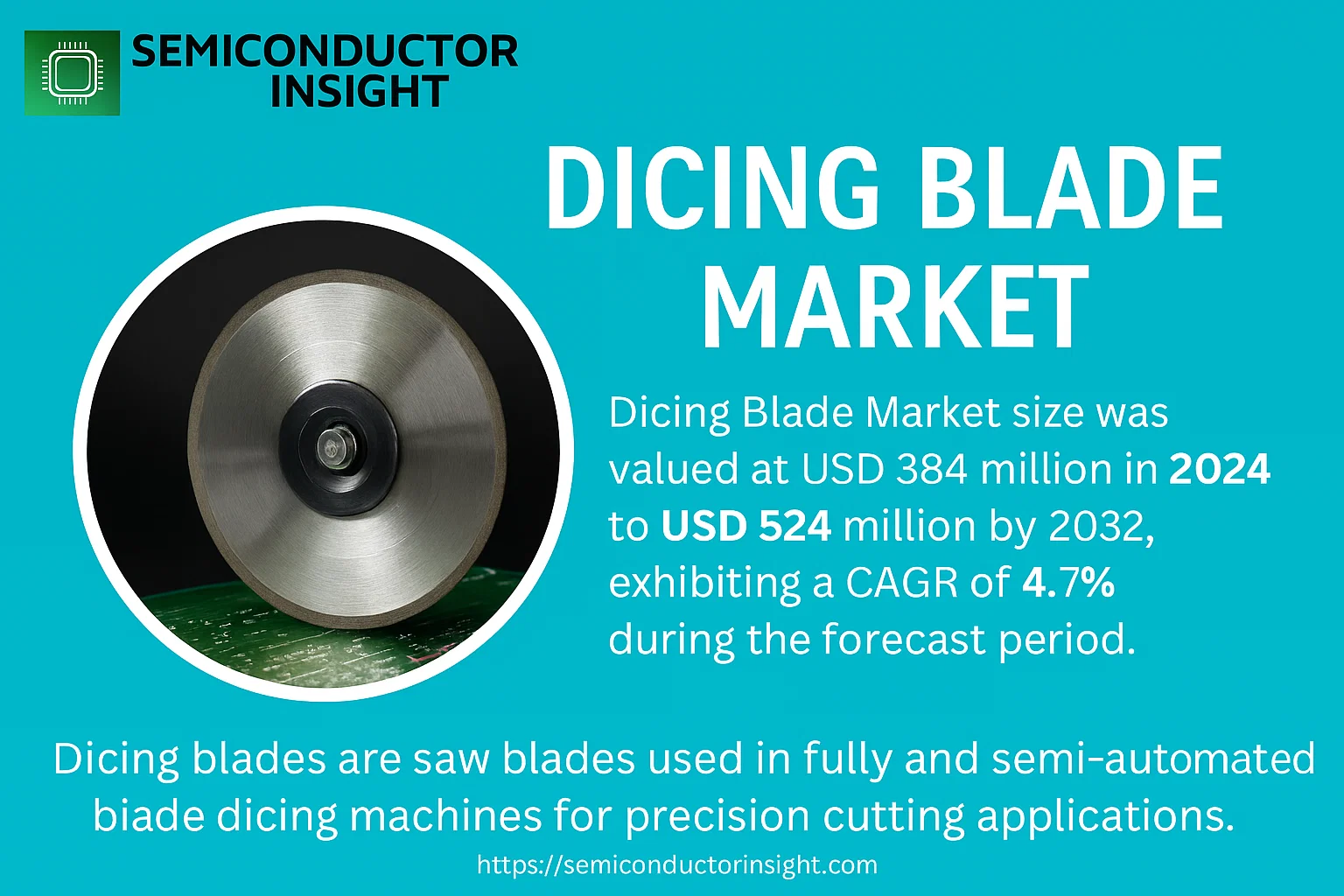

Global Dicing Blade Market size was valued at USD 384 million in 2024 to USD 524 million by 2032, exhibiting a CAGR of 4.7% during the forecast period.

Dicing blades are saw blades used in fully and semi-automated blade dicing machines for precision cutting applications. These expendable tools are specifically designed to groove, cut, and dice various materials including silicon wafers, compound semiconductors, glass substrates, ceramics, crystals, and other advanced materials requiring high-precision cut edges. The selection of appropriate dicing blades is crucial for achieving optimal sawing quality with minimal chipping and maximum yield.

The market is experiencing steady growth driven by increasing demand from the semiconductor industry and expanding electronics manufacturing sector. Key growth factors include rising adoption of advanced packaging technologies, growing production of micro-electromechanical systems (MEMS), and expanding applications in LED manufacturing. However, the market faces challenges such as intense price competition and the emergence of alternative dicing technologies like laser dicing. The Asia-Pacific region dominates the global market with approximately 72% share due to concentrated semiconductor manufacturing activities in countries like China, Taiwan, South Korea, and Japan. DISCO Corporation, K&S, TOKYO SEIMITSU, KODI, and Kinik Company represent the leading players collectively holding over 80% market share through their extensive product portfolios and technological expertise.

MARKET DRIVERS

Proliferation of Miniaturized Electronics

The relentless demand for smaller, more powerful electronic devices is a primary driver for the dicing blade market. The manufacturing of semiconductors for smartphones, wearables, and IoT devices requires ultra-precise dicing of silicon wafers into increasingly smaller and thinner dies. This trend fuels the need for advanced dicing blades capable of achieving higher accuracy and minimal chipping to maintain high device yields.

Expansion of the Automotive Electronics Sector

The automotive industry’s rapid transition towards electrification and advanced driver-assistance systems (ADAS) has significantly increased the consumption of power semiconductors and sensors. These components rely on robust dicing processes. The market is experiencing growth driven by the requirement for dicing blades that can handle new, tougher substrate materials like silicon carbide (SiC) and gallium nitride (GaN).

➤ Global market for dicing blades is projected to grow at a compound annual growth rate of approximately 6.5% over the next five years, largely propelled by these technological advancements.

Furthermore, investments in advanced packaging technologies, such as fan-out wafer-level packaging (FO-WLP) and 2.5D/3D IC integration, necessitate specialized dicing solutions for intricate singulation processes, creating sustained demand for high-performance blades.

MARKET CHALLENGES

High Precision and Quality Demands

One of the most significant challenges in the dicing blade market is meeting the extremely tight tolerances required for modern semiconductor fabrication. Any imperfection, such as micro-cracks or excessive chipping, can lead to catastrophic failure of the final electronic component. Manufacturers face constant pressure to produce blades that deliver exceptional consistency and durability across high-volume production runs.

Other Challenges

Rapid Technological Obsolescence

The fast-paced evolution of semiconductor materials and packaging designs means that dicing blade technologies can become outdated quickly. Manufacturers must invest heavily in research and development to keep pace with new substrate materials and cutting requirements, which is a significant financial and operational challenge.

Cost Sensitivity in Manufacturing

While performance is critical, there is intense pressure to control costs in the highly competitive semiconductor supply chain. Balancing the use of expensive, high-quality abrasives like diamond with the need for competitive pricing is a persistent challenge for dicing blade suppliers.

MARKET RESTRAINTS

High Cost of Advanced Dicing Technologies

The development and production of dicing blades for advanced applications, particularly those involving diamond abrasives and specialized bond systems, involve substantial costs. This high cost can be a barrier to adoption for smaller fabrication facilities or for applications where cost-effectiveness is a primary concern, potentially restraining market growth in certain segments.

Competition from Alternative Singulation Methods

The dicing blade market faces competition from laser-based dicing and plasma dicing technologies. These alternative methods offer advantages like non-contact processing and the ability to create very narrow streets, which can be a restraint on the growth of mechanical blade dicing for specific, high-end applications.

MARKET OPPORTUNITIES

Growth in Wide Bandgap Semiconductor Production

The escalating adoption of SiC and GaN semiconductors for electric vehicles, renewable energy systems, and 5G infrastructure presents a major growth avenue. These hard, brittle materials require specialized dicing blades, creating a lucrative niche market for manufacturers who can develop blades that minimize subsurface damage and increase throughput.

Emerging Applications in MEMS and Sensors

The expanding market for Micro-Electro-Mechanical Systems (MEMS) and various sensors used in consumer electronics, medical devices, and industrial automation requires delicate dicing processes. This creates opportunities for ultra-thin dicing blades and customized solutions tailored to the fragile nature of these devices, driving innovation and specialization within the market.

Dicing Blade Market Trends

Sustained Market Expansion Driven by Semiconductor Demand

Global Dicing Blade Market is on a trajectory of steady growth, valued at USD 384 million in 2024 and projected to reach USD 524 million by 2032, achieving a Compound Annual Growth Rate (CAGR) of 4.7%. This expansion is predominantly fueled by the relentless demand from the global semiconductor industry. Dicing blades, which are saw blades for fully and semi-automated dicing machines, are critical expendable tools for grooving, cutting, and dicing silicon wafers, compound semiconductors, glass, and ceramics. The selection of the appropriate dicing blade is a prerequisite for achieving high-precision cut edges and superior sawing quality, directly impacting manufacturing yields in electronics production.

Other Trends

Asia-Pacific Regional Dominance

The geographical distribution of the market highlights a pronounced concentration of demand and manufacturing in the Asia-Pacific region, which commands a dominant share of approximately 72% of the global market. This hegemony is attributable to the region’s status as the global hub for semiconductor fabrication and electronics manufacturing. North America and Europe follow distantly, with shares of 14% and 13% respectively, supported by their own advanced technology sectors and research institutions. The market’s growth is therefore intrinsically linked to the capital expenditure cycles and technological advancements within the semiconductor industries of these key regions.

Consolidated Competitive Landscape and Product Segmentation

The competitive environment is characterized by a high degree of consolidation, with the top five players, including DISCO Corporation, K&S, and TOKYO SEIMITSU, collectively holding over 80% of the market share. This concentration underscores the significant barriers to entry, driven by the need for advanced material science expertise and precision engineering capabilities. The market is segmented by product type, primarily into Hubless Blades and Hub Blades, each catering to specific dicing applications and machine requirements. By application, the market is divided between Wafer dicing and Substrate dicing, with the former being the largest segment due to the volume of silicon wafer processing for integrated circuits. The ongoing miniaturization of electronic components continues to drive innovation in blade technology, focusing on thinner, more durable blades capable of producing cleaner cuts with minimal material loss.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominated by a Handful of Established Leaders

Global Dicing Blade Market is highly concentrated, with the top five players collectively holding a dominant share exceeding 80% of the market. This structure is characterized by the significant market leadership of Japanese manufacturers who possess advanced technological expertise in precision machining and abrasives technology. DISCO Corporation stands as the clear global leader, renowned for its high-precision dicing saws and blades that set the industry standard for quality and performance in semiconductor and electronics manufacturing. The market’s high concentration is reinforced by substantial barriers to entry, including the need for specialized R&D, sophisticated manufacturing capabilities, and established, trusted relationships with major semiconductor fabricators who require ultra-reliable, high-yield consumables. This dominance is further solidified by the critical nature of dicing blades in the production process, where blade performance directly impacts yield, throughput, and ultimately, profitability.

Beyond the dominant leaders, a tier of specialized and regional players competes in specific niches or application segments. These companies often focus on offering cost-effective alternatives, specialized blades for novel materials like compound semiconductors or advanced ceramics, or cater to regional markets with strong local supply chains. Companies such as Kinik Company and Asahi Diamond Industrial leverage their deep experience in abrasive technologies to serve demanding applications. Other significant participants have carved out positions by providing compatible blades for a range of dicing equipment or by serving emerging manufacturing hubs. Competition in this segment is intense, driven by technical performance, price, and the ability to provide consistent quality and responsive customer support, particularly for manufacturers outside the largest global foundries.

List of Key Dicing Blade Companies Profiled

- DISCO Corporation

- Kulicke & Soffa (K&S)

- TOKYO SEIMITSU (ACCRETECH)

- KODI

- Kinik Company

- Asahi Diamond Industrial Co., Ltd.

- ADT (GL Tech)

- YMB Co., LTD

- UKAM Industrial Superhard Tools

- Ceiba Technologies

- Shanghai Sinyang Semiconductor Materials Co., Ltd.

- Norton Saint-Gobain Abrasives

- EHWA Diamond Industrial Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hubless Blades represent the leading segment, primarily due to their superior design flexibility and precise cutting capabilities for intricate semiconductor dicing applications. The absence of a central hub minimizes vibration and allows for thinner blade profiles, which is critical for achieving the fine cut widths and minimal kerf loss demanded by advanced microelectronics manufacturing. This segment’s growth is further propelled by the increasing miniaturization of electronic components and the high-volume production of memory chips and processors. |

| By Application |

|

Wafer Dicing is the dominant application segment, driven by the immense and continuously expanding global semiconductor industry. The relentless demand for smaller, more powerful integrated circuits necessitates highly precise dicing processes to separate individual die from silicon wafers without causing micro-cracks or chipping. The critical nature of this application for the production of virtually all modern electronics solidifies its leading position, with innovation focused on handling ultra-thin wafers and new semiconductor materials like gallium nitride and silicon carbide. |

| By End User |

|

Semiconductor Foundries constitute the primary end-user segment, as they are at the forefront of high-volume wafer production for a diverse range of fabless semiconductor companies. Their need for consistent, high-quality dicing blades that ensure maximum yield and throughput from expensive silicon wafers makes them the most demanding and significant consumers. The technological race to smaller process nodes and the adoption of advanced packaging techniques continuously influence blade specifications and performance requirements within this segment. |

| By Material Processed |

|

Silicon remains the leading material segment due to its foundational role in the global electronics supply chain. The vast majority of dicing blades are engineered and optimized specifically for cutting monocrystalline and polycrystalline silicon wafers. However, the segment for Compound Semiconductors is showing exceptionally strong growth momentum, driven by the adoption of wide-bandgap materials like silicon carbide and gallium nitride in power electronics, radio-frequency devices, and optoelectronics, which present unique and more challenging dicing requirements. |

| By Blade Diameter |

|

2 to 4 inches is the most prevalent blade diameter segment, as it aligns with the standard sizes used for dicing the majority of semiconductor wafers in high-volume manufacturing environments. This size offers an optimal balance between cutting stability, blade life, and the ability to achieve the necessary depth of cut for standard wafer thicknesses. The trend towards larger diameter wafers, such as 300mm, supports the sustained demand for blades within this range, although specialized applications are fostering growth in both smaller and larger diameter segments for specific materials and thicknesses. |

Regional Analysis: Dicing Blade Market

The concentration of leading semiconductor foundries and Integrated Device Manufacturers (IDMs) in the region creates immense, consistent demand for ultra-precise dicing blades. This ecosystem drives the need for blades capable of handling newer, thinner, and more complex wafer materials for advanced logic and memory chips.

As the global center for assembling smartphones, laptops, and wearables, the region requires vast quantities of diced semiconductor components. This fuels the market for dicing blades optimized for high-volume production while maintaining the strict quality standards demanded by major electronics brands.

A dense network of local dicing blade manufacturers and material science researchers promotes rapid adoption of new technologies like diamond-like carbon coatings and resin bond systems. This localized expertise allows for quick customization and technical support, enhancing the region’s competitive advantage.

National initiatives aimed at achieving technological self-sufficiency and securing the semiconductor supply chain are leading to massive investments in new fabrication facilities. This long-term strategic focus ensures a robust and growing pipeline of demand for dicing blades and associated equipment.

North America

The North American dicing blade market is characterized by high-value, technologically advanced demand, primarily driven by the United States. The region hosts several key semiconductor companies, defense contractors, and R&D centers that require dicing blades for cutting-edge applications. These include specialized compound semiconductors for aerospace, defense systems, and high-performance computing. The market demand is less about volume and more about precision, reliability, and the ability to dice novel materials like gallium nitride (GaN) and silicon carbide (SiC). Stringent quality control requirements and a focus on developing next-generation chip technologies ensure a steady market for premium, high-performance dicing blades from specialized suppliers.

Europe

Europe maintains a significant and stable position in the dicing blade market, supported by its strong automotive, industrial, and research sectors. Germany, in particular, is a key consumer due to its robust automotive industry’s shift towards electric vehicles and advanced driver-assistance systems (ADAS), which rely on power semiconductors that require precise dicing. The presence of major research institutions and equipment manufacturers, such as those for MEMS (Micro-Electro-Mechanical Systems) sensors, also generates demand for specialized dicing solutions. The European market emphasizes precision engineering, durability, and meeting strict environmental and manufacturing standards, influencing the types of dicing blades favored by regional manufacturers.

South America

The dicing blade market in South America is a developing segment with growth potential linked to the gradual expansion of its local electronics manufacturing and industrial base. Brazil is the most prominent market, with demand primarily driven by the automotive and consumer electronics assembly sectors. However, the region’s semiconductor production capability is limited, making it largely a net importer of finished semiconductor components and the dicing blades used in their production. Market growth is influenced by regional economic stability and government policies aimed at fostering local industrial development, which could slowly increase the need for manufacturing consumables like dicing blades over the long term.

Middle East & Africa

The Middle East & Africa region represents a smaller, niche market for dicing blades. Demand is primarily concentrated in a few countries with strategic diversification initiatives, such as those in the Gulf Cooperation Council (GCC), which are investing in technology and manufacturing sectors beyond oil and gas. This includes nascent electronics assembly and research facilities. The African market is minimal, with very limited local semiconductor manufacturing. Overall, consumption in this region is project-based and heavily reliant on imports, with potential for slow growth tied to long-term economic diversification plans and infrastructure development.

Report Scope

This market research report provides a comprehensive analysis of the Global Dicing Blade Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Dicing Blade Market?

-> Global Dicing Blade Market was valued at USD 384 million in 2024 and is projected to reach USD 524 million by 2032, growing at a CAGR of 4.7% during the forecast period.

Which key companies operate in Dicing Blade Market?

-> Key players include DISCO Corporation, K&S, TOKYO SEIMITSU, KODI, and Kinik Company, among others. The top five players hold a share of over 80%.

What are the key growth drivers?

-> Key growth drivers include the expansion of the semiconductor industry, rising demand for high-precision cutting tools for materials like silicon and ceramics, and technological advancements in automated dicing machines.

Which region dominates the market?

-> Asia-Pacific is the largest market, holding a share of about 72%, followed by North America and Europe with shares of approximately 14% and 13%, respectively.

What are the emerging trends?

-> Emerging trends include the development of advanced dicing blades for new semiconductor materials, the integration of precision engineering for finer cuts, and a focus on blades that offer longer lifespan and higher efficiency in production processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...