MARKET INSIGHTS

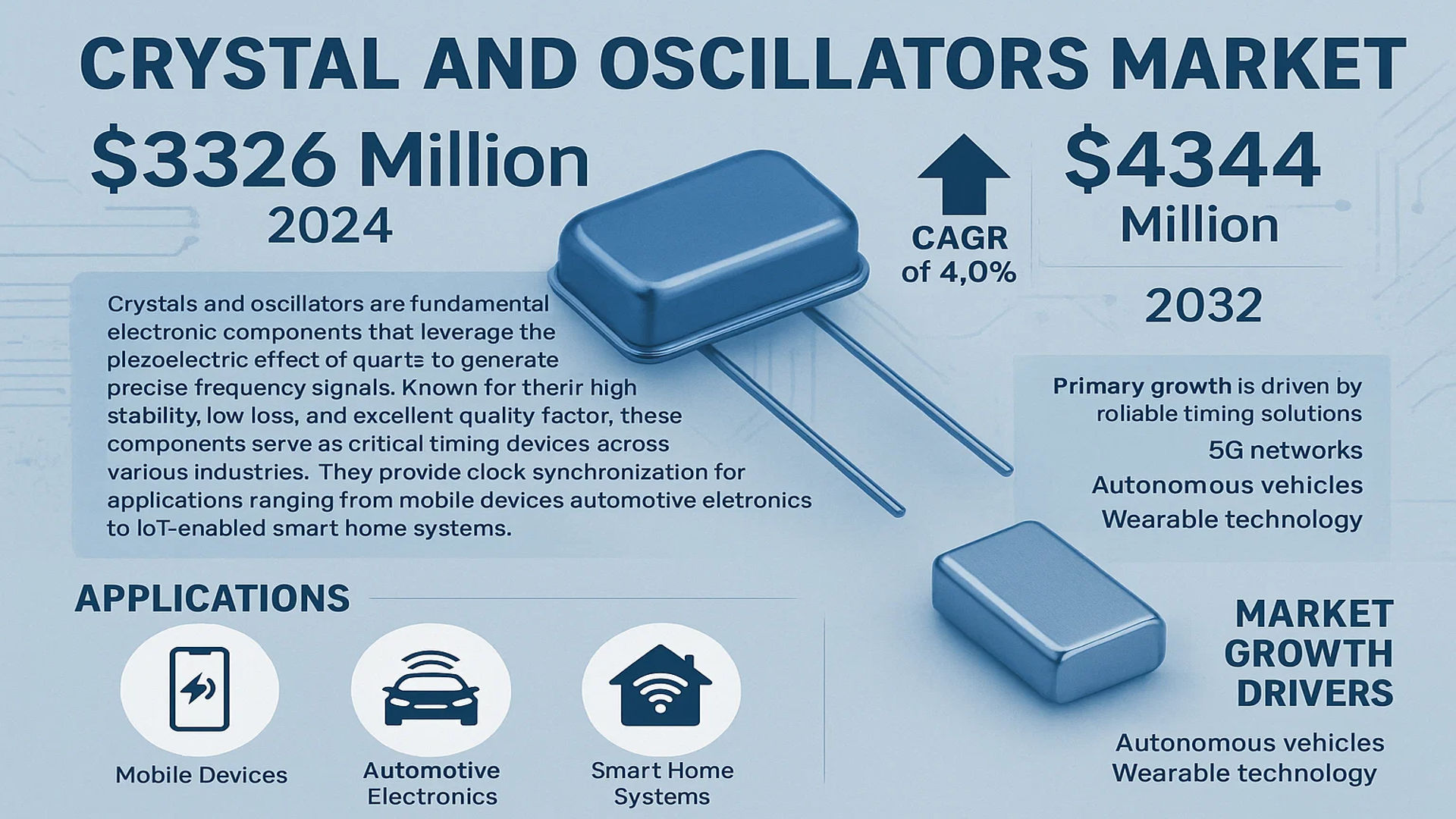

The global Crystal and Oscillators Market was valued at 3326 million in 2024 and is projected to reach US$ 4344 million by 2032, at a CAGR of 4.0% during the forecast period.

Crystals and oscillators are fundamental electronic components that leverage the piezoelectric effect of quartz to generate precise frequency signals. Known for their high stability, low loss, and excellent quality factor, these components serve as critical timing devices across various industries. They provide clock synchronization for applications ranging from mobile devices and automotive electronics to IoT-enabled smart home systems.

The market growth is driven by increasing demand for reliable timing solutions in 5G networks, autonomous vehicles, and wearable technology. Japan dominates production, accounting for 44% of the market share, while the top five manufacturers collectively hold 43% of the global market. Crystal units represent the largest product segment (53% share), with mobile terminals being the leading application (47% share). Recent technological advancements in MEMS-based oscillators and miniaturization trends are further shaping the industry landscape.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of 5G Networks and IoT to Fuel Demand for Crystal Oscillators

The global rollout of 5G infrastructure represents a significant growth driver for crystal oscillators, which are essential for frequency stability in wireless communication systems. As telecom operators continue deploying 5G base stations requiring precise timing solutions, demand for high-performance temperature-compensated crystal oscillators (TCXOs) and oven-controlled crystal oscillators (OCXOs) has surged. The Internet of Things (IoT) ecosystem, projected to exceed 30 billion connected devices by 2025, further amplifies this demand as wireless modules across smart factories, wearables, and smart meters all require timing components.

Automotive Electronics Revolution Creating New Growth Avenues

Modern vehicles now incorporate over 100 electronic control units (ECUs) that depend on quartz crystal timing devices for operation. The automotive crystal oscillator market is expanding rapidly due to rising ADAS penetration, in-vehicle networking systems, and electric vehicle production. With autonomous vehicle development accelerating, the requirement for ultra-high precision MEMS oscillators in LiDAR and V2X communication systems has increased substantially. Major manufacturers are introducing automotive-grade oscillators with AEC-Q200 compliance to meet stringent quality requirements.

Consumer Electronics Miniaturization Driving Innovation

The relentless push for smaller form factors in smartphones, wearables, and hearables has compelled oscillator manufacturers to develop innovative packaging solutions. Chip-scale packaging (CSP) and wafer-level packaging (WLP) technologies now enable crystal devices under 1.0mm footprint while maintaining frequency stability. With mobile manufacturers increasingly adopting these space-saving solutions for 5G smartphones and TWS earbuds, the miniaturized oscillator segment shows robust growth potential.

MARKET RESTRAINTS

Increasing Competition from MEMS Technology Poses Market Challenges

While quartz crystal oscillators dominate the timing solutions market, microelectromechanical systems (MEMS) oscillators are gaining share in cost-sensitive applications. MEMS devices offer advantages like smaller size, better shock resistance, and faster production scalability. Although quartz still maintains superior frequency stability for high-performance applications, the price gap continues to narrow, particularly in consumer electronics where 5-10ppm stability suffices. This competition forces quartz manufacturers to accelerate R&D investments to maintain technological leadership.

Supply Chain Vulnerabilities Impacting Market Stability

The crystal oscillator industry faces ongoing challenges from global supply chain disruptions affecting quartz crystal blanks and other raw materials. Geopolitical tensions have created availability issues for high-purity quartz, while pandemic-related factory closures caused production bottlenecks. These constraints come as demand surges across multiple end-use sectors, creating inventory shortages that some manufacturers estimate may persist through 2025. The situation has prompted companies to diversify supply sources and increase strategic inventory.

Stringent Quality Requirements Increasing Production Costs

Emerging applications in automotive, industrial, and medical fields require oscillators meeting increasingly rigorous quality standards. Compliance with specifications like AEC-Q200, ISO 13485, and MIL-PRF-55310 necessitates substantial investments in production equipment and quality control processes. The added certification and testing overheads, particularly for high-reliability applications, compress manufacturer margins. While these standards create market barriers, they also drive consolidation as only well-capitalized players can afford the necessary investments.

MARKET OPPORTUNITIES

Emerging AI and Edge Computing Applications Open New Markets

The proliferation of AI processing at the network edge creates fresh demand for ultra-stable timing solutions. AI accelerators and edge servers require precise clock synchronization across distributed systems, driving adoption of low-jitter oscillators. Manufacturers developing specialized timing ICs optimized for AI workloads can capture this high-value segment. With edge computing infrastructure investment projected to grow at double-digit rates through 2030, the opportunity for specialized timing solutions continues expanding.

Satellite Communications and Space Applications Present Growth Potential

The commercialization of low-earth orbit (LEO) satellite constellations has created demand for radiation-hardened crystal oscillators capable of withstanding space environments. With thousands of satellites planned for deployment this decade, aerospace-grade timing components represent a premium market segment. Developing space-qualified oscillators with extended temperature ranges and vibration resistance allows manufacturers to access this high-margin opportunity while diversifying from terrestrial applications.

Medical Electronics Innovation Drives Specialized Solutions

Advanced medical devices including patient monitors, imaging systems, and portable diagnostics increasingly incorporate high-reliability oscillators. The trend toward wireless and wearable medical technology creates opportunities for miniaturized timing solutions meeting medical safety standards. With the global medical electronics market continuing to expand, manufacturers offering biocompatible packaging and low-EMI oscillator designs can establish strong positions in this regulated but lucrative sector.

MARKET CHALLENGES

Manufacturing Complexity and Yield Issues Impacting Production Efficiency

Quartz crystal oscillator production involves intricate processes including wafer slicing, electrode deposition, and frequency adjustment that require specialized equipment and skilled technicians. Achieving consistent yields, especially for high-frequency devices above 100MHz, presents ongoing technical challenges. The industry faces pressure to improve manufacturing efficiencies as customers demand tighter tolerances and lower prices. Process automation investments are becoming essential but require significant capital that strains smaller manufacturers.

Technological Skills Gap in Precision Manufacturing

As oscillator technology advances, the industry encounters difficulties in maintaining sufficient technical expertise. The specialized knowledge required for quartz crystal processing, frequency tuning, and quality control takes years to develop. Many experienced professionals are retiring while educational institutions struggle to produce enough graduates with the exact skill sets needed. This talent shortage complicates expansion plans and slows innovation cycles at a time when market demands are accelerating.

Environmental Regulations Affecting Material Sourcing

Increasing environmental regulations governing mining and chemical processing impact the crystal oscillator supply chain. Restrictions on certain etching chemicals used in quartz processing require manufacturers to develop alternative production methods. Sustainable sourcing of raw materials while maintaining quality standards presents an ongoing challenge. The industry must balance ecological responsibilities with the need to deliver components meeting exacting technical specifications across diverse applications.

CRYSTAL AND OSCILLATORS MARKET TRENDS

5G and IoT Expansion Driving Demand for High-Precision Timing Solutions

The deployment of 5G networks and rapid growth of IoT applications are significantly boosting demand for precision timing components. Crystal oscillators, particularly temperature-compensated crystal oscillators (TCXOs) and oven-controlled crystal oscillators (OCXOs), are critical for maintaining synchronization in 5G base stations and telecom infrastructure. With global 5G subscriptions projected to surpass 3 billion by 2026, this sector alone accounts for approximately 32% of oscillator demand. Furthermore, the proliferation of IoT devices, expected to exceed 75 billion connections by 2025, continues to create sustained demand for compact, low-power timing solutions. Original equipment manufacturers are increasingly adopting MEMS-based oscillators for their superior stability and shock resistance in these applications.

Other Trends

Automotive Electronics Evolution

The advancement of autonomous driving systems and electric vehicle production is generating substantial growth in the automotive oscillator market. Modern vehicles contain over 50 timing components to support ADAS, infotainment systems, and vehicle-to-everything (V2X) communication. The push toward electric vehicles, with annual sales projected to reach 45 million units by 2030, requires even more sophisticated timing solutions for battery management and power electronics. Leading manufacturers are developing automotive-grade oscillators with AEC-Q200 certification to meet the stringent reliability and temperature stability requirements of the automotive sector, which now represents nearly 18% of total market demand.

Miniaturization and Power Efficiency Innovations

Industry-wide efforts to reduce component sizes while improving power efficiency continue to shape product development strategies. The trend toward smaller form factors is particularly evident in wearable devices and mobile terminals, where demand for 2016 and 2520 package sizes has grown by 25% year-over-year. Simultaneously, manufacturers are achieving significant breakthroughs in low-power oscillator designs, with some models now operating at under 1 mA current consumption. This aligns with the broader industry emphasis on energy-efficient electronics, as power consumption remains a critical selection criterion for about 65% of design engineers. Recent innovations include programmable oscillators that allow dynamic frequency adjustment to optimize power usage across different operational modes.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics Shaped by Technological Advancements and Regional Dominance

The global crystal and oscillators market is characterized by a mix of established players and emerging competitors, with Japanese manufacturers leading in terms of market share. Seiko Epson Corp dominates the space, accounting for approximately 12% of global revenue in 2024. The company’s success stems from its vertically integrated supply chain and precision manufacturing capabilities for crystal units used in wearables and IoT devices.

TXC Corporation and NDK follow closely, leveraging their strong foothold in Asia-Pacific markets—particularly in smartphone and automotive applications. These players are investing heavily in temperature-compensated crystal oscillators (TCXOs) to meet 5G infrastructure demands. Meanwhile, KCD and KDS are expanding their presence in Europe through partnerships with automotive Tier-1 suppliers.

North American players like Microchip and SiTime are differentiating themselves through MEMS-based timing solutions, which are gaining traction in aerospace and industrial applications. Recent acquisitions in this space indicate consolidation trends, with SiTime purchasing five smaller timing-component specialists since 2022 to expand its product portfolio.

Notably, Chinese manufacturers such as ZheJiang East Crystal are rapidly gaining market share in consumer electronics through cost-competitive offerings. However, quality perception challenges persist for these emerging players in high-reliability applications like medical devices and automotive systems.

List of Key Crystal and Oscillator Manufacturers

- Seiko Epson Corp (Japan)

- TXC Corporation (Taiwan)

- NDK (Japan)

- KCD (Japan)

- KDS (Japan)

- Microchip Technology Inc. (U.S.)

- SiTime Corporation (U.S.)

- Murata Manufacturing (Japan)

- Rakon Limited (New Zealand)

- ZheJiang East Crystal (China)

- Siward Crystal Technology (Taiwan)

- Hosonic Electronic (Taiwan)

Segment Analysis:

By Type

Crystal Units Segment Leads the Market Due to Their Wide Application in Electronic Devices

The market is segmented based on type into:

- Crystal Units

- Subtypes: AT-cut, BT-cut, SC-cut, and others

- Crystal Oscillators

- Subtypes: TCXO, VCXO, OCXO, and others

By Application

Mobile Terminal Segment Dominates Due to High Demand in Smartphones and Tablets

The market is segmented based on application into:

- Mobile Terminal

- Automotive Electronics

- Wearable Device

- Smart Home

- Internet of Things

- Others

By Frequency Range

Mid-Frequency Range (10-100 MHz) Sees Highest Adoption Across Industries

The market is segmented based on frequency range into:

- Low Frequency (Below 10 MHz)

- Mid Frequency (10-100 MHz)

- High Frequency (Above 100 MHz)

By Mounting Type

Surface Mount Technology Gains Traction for Miniaturization Advantages

The market is segmented based on mounting type into:

- Through-Hole Mounting

- Surface Mount Technology

Regional Analysis: Crystal and Oscillators Market

Asia-Pacific

Leading the global crystal and oscillators market, the Asia-Pacific region accounts for the highest production and consumption volumes, driven by Japan’s dominance (44% market share) and China’s massive electronics manufacturing ecosystem. Japan houses key players like Seiko Epson and NDK, leveraging decades of quartz crystal expertise. The proliferation of 5G networks, IoT devices, and automotive electronics in China and India is accelerating demand for precision timing components. While cost-sensitive segments still prioritize crystal units (53% of the market), OEMs are increasingly adopting MEMS oscillators for advanced applications like AI processors and autonomous vehicles. Regional growth is further fueled by government initiatives like China’s “Made in China 2025,” which prioritizes semiconductor self-sufficiency.

North America

North America’s market thrives on high-performance applications in aerospace, defense, and telecommunications, where stability and low phase noise are critical. The U.S. leads with innovations in MEMS-based oscillators, supported by companies like Microchip and SiTime. Demand is amplified by automotive ADAS systems and data center expansions, requiring ultra-precise clocking solutions. However, supply chain dependencies on Asian quartz crystal suppliers occasionally disrupt production. Regulatory standards, including MIL-PRF-55310 for military-grade components, shape product development, while R&D investments focus on reducing jitter and improving frequency stability for next-gen networks.

Europe

Europe’s market emphasizes quality and miniaturization, with Germany and France spearheading automotive and industrial IoT adoption. Automotive Tier-1 suppliers demand AEC-Q200 compliant oscillators for reliability in harsh environments. The region also sees growth in ultra-low-power devices for wearable health tech, where Swiss firms like Micro Crystal excel in micro-oscillator production. However, competition from Asian manufacturers and high production costs limit market expansion. EU policies promoting semiconductor resilience, such as the Chips Act, could bolster local sourcing of timing components in the medium term.

South America

A niche but growing market, South America’s demand centers on consumer electronics and automotive replacements, with Brazil as the primary hub. Local assembly of smartphones and IoT gadgets drives crystal unit imports, primarily from China. Economic volatility and import dependencies constrain investment in local production, though tax incentives in free trade zones are attracting minor assembly operations. The lack of advanced manufacturing infrastructure keeps the region reliant on low- to mid-range frequency components, with limited uptake of high-end oscillators.

Middle East & Africa

This emerging market is propelled by telecom infrastructure rollouts, particularly in GCC countries investing in 5G. The UAE and Saudi Arabia import oscillators for base stations and smart city projects, prioritizing temperature-stable components for desert climates. South Africa’s automotive sector shows potential, but political instability and currency risks deter major investments. While the region lacks local production, distributors are expanding inventories to serve growing demand from industrial automation and renewable energy projects.

Report Scope

This market research report provides a comprehensive analysis of the global Crystal and Oscillators market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Crystal and Oscillators market was valued at USD 3,326 million in 2024 and is projected to reach USD 4,344 million by 2032, growing at a CAGR of 4.0% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Crystal Units and Crystal Oscillators), application (Mobile Terminal, Automotive Electronics, Wearable Devices, etc.), and end-user industry to identify high-growth segments and investment opportunities. Crystal Units dominate with a 53% market share, while Mobile Terminal applications account for 47% of total demand.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Japan leads in production value with a 44% share of the global market, while Asia-Pacific shows the strongest growth potential.

- Competitive Landscape: Profiles of leading market participants including Seiko Epson Corp, TXC Corporation, NDK, KCD, and KDS, which collectively hold about 43% market share. The analysis covers their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in frequency control devices, miniaturization trends, and the impact of IoT and 5G network expansion on oscillator requirements.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for electronic devices, automotive electronics expansion, and 5G deployment, along with challenges like raw material price volatility and supply chain complexities.

- Stakeholder Analysis: Insights for component manufacturers, OEMs, system integrators, and investors regarding the evolving frequency components ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, manufacturer surveys, and analysis of verified market data to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Crystal and Oscillators Market?

-> Crystal and Oscillators Market was valued at 3326 million in 2024 and is projected to reach US$ 4344 million by 2032, at a CAGR of 4.0% during the forecast period.

Which key companies operate in Global Crystal and Oscillators Market?

-> Key players include Seiko Epson Corp, TXC Corporation, NDK, KCD, KDS, Microchip, SiTime, Murata Manufacturing, and other prominent manufacturers.

What are the key growth drivers?

-> Key growth drivers include expansion of 5G networks, increasing demand for IoT devices, growth in automotive electronics, and rising smartphone adoption.

Which region dominates the market?

-> Asia-Pacific is both the largest and fastest-growing region, with Japan accounting for 44% of global production value.

What are the emerging trends?

-> Emerging trends include miniaturization of components, MEMS-based oscillators, and increasing demand for high-frequency precision components in 5G applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...