MARKET INSIGHTS

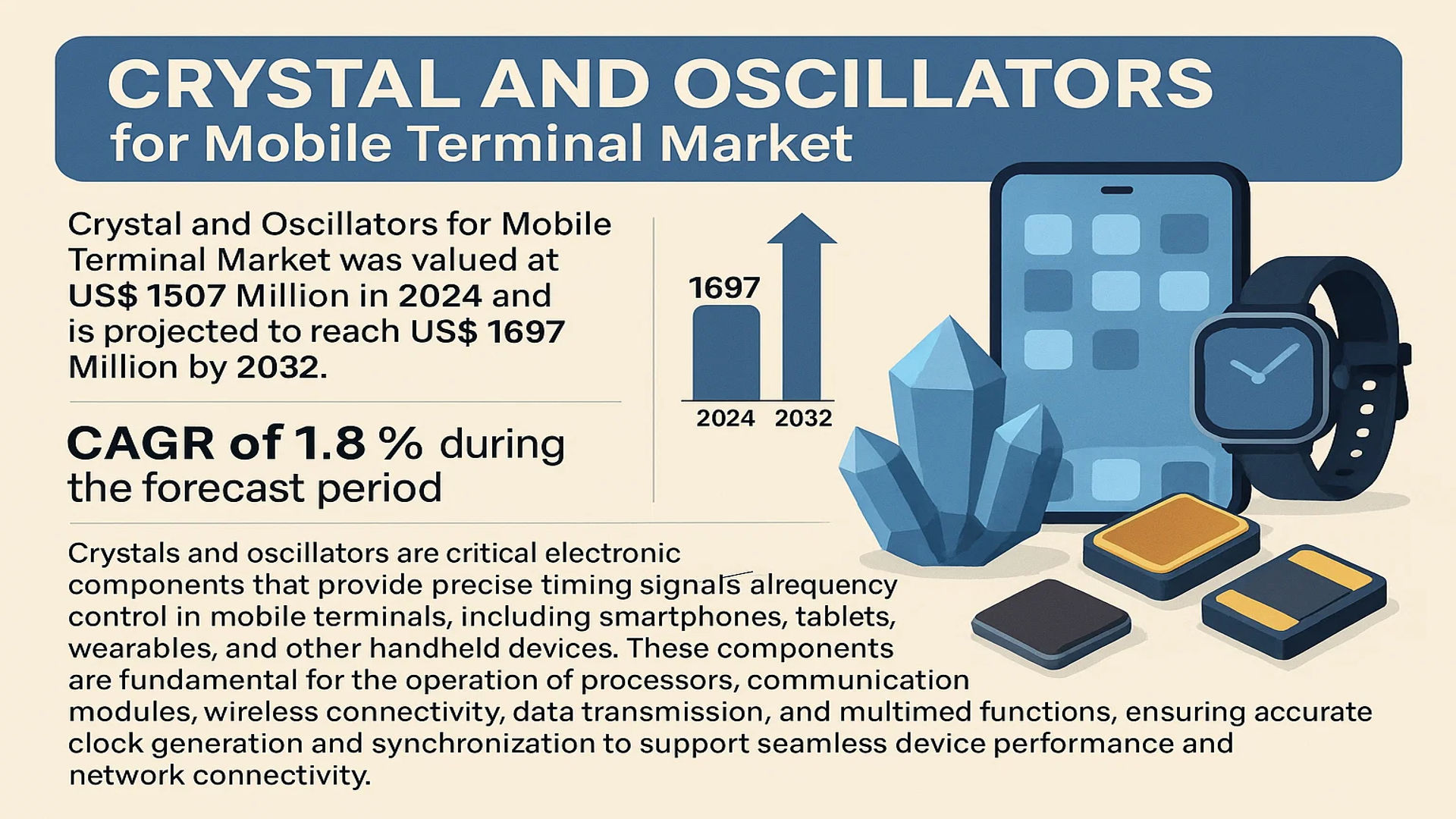

The global Crystal and Oscillators for Mobile Terminal Market was valued at 1507 million in 2024 and is projected to reach US$ 1697 million by 2032, at a CAGR of 1.8% during the forecast period.

Crystals and oscillators are critical electronic components that provide precise timing signals and frequency control in mobile terminals, including smartphones, tablets, wearables, and other handheld devices. These components are fundamental for the operation of processors, communication modules, wireless connectivity, data transmission, and multimedia functions, ensuring accurate clock generation and synchronization to support seamless device performance and network connectivity.

The market is experiencing steady growth driven by the continuous innovation in mobile technologies, particularly the global rollout of 5G infrastructure and the proliferation of IoT devices. However, the market faces challenges such as the need for high frequency stability under varying environmental conditions and managing electromagnetic interference. Key players like Murata Manufacturing, Seiko Epson Corp, and NDK dominate the market, focusing on developing miniature, low-power components to meet the demands of increasingly compact and power-efficient mobile devices.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated 5G Deployment and Mobile Device Proliferation to Drive Market Growth

The global rollout of 5G networks represents a fundamental driver for crystal and oscillator demand in mobile terminals. With over 2.1 billion 5G subscriptions projected worldwide by 2025, mobile device manufacturers require increasingly sophisticated timing components to support higher frequency bands, reduced latency, and enhanced data throughput. These components must maintain exceptional frequency stability—typically within ±5 ppm—while operating across temperature ranges from -40°C to 85°C. The transition to 5G-Advanced and future 6G standards further intensifies requirements for ultra-low jitter performance below 100 femtoseconds, driving innovation in temperature-compensated crystal oscillators (TCXOs) and oven-controlled crystal oscillators (OCXOs). This technological evolution directly correlates with the projected market expansion from $1507 million in 2024 to $1697 million by 2032.

Expansion of IoT and Wearable Ecosystems to Boost Component Demand

The proliferation of IoT-connected devices and wearable technology substantially contributes to market growth. With the global wearable device market exceeding 650 million units annually, crystals and oscillators must meet increasingly stringent power consumption requirements while maintaining frequency accuracy. Modern wearable applications demand current consumption below 1.5 μA in standby mode while supporting multiple wireless protocols including Bluetooth Low Energy, Wi-Fi 6, and cellular IoT. This power efficiency imperative drives adoption of MEMS-based oscillators and ultra-miniaturized crystal units with footprints below 1.6 × 1.2 mm. The convergence of health monitoring, navigation, and communication functionalities in single devices further necessitates components capable of supporting multiple frequency outputs with minimal phase noise.

Advanced Multimedia and Computing Capabilities to Stimulate Technical Innovation

Rising consumer expectations for multimedia performance drive substantial innovation in timing components. Mobile devices now incorporate high-refresh-rate displays (up to 120Hz), multi-camera arrays with computational photography, and immersive audio processing—all requiring precise synchronization and clock distribution. These applications demand jitter performance below 0.5 picoseconds root mean square and phase noise better than -150 dBc/Hz at 1 MHz offset. Furthermore, the integration of artificial intelligence processors operating at frequencies exceeding 2 GHz necessitates crystals and oscillators with improved frequency stability and lower aging characteristics. The automotive sector’s adoption of mobile-derived technologies for infotainment and advanced driver assistance systems creates additional growth avenues, particularly for components meeting AEC-Q200 reliability standards.

MARKET CHALLENGES

Frequency Stability and Environmental Compensation Challenges in Miniaturized Designs

Maintaining frequency stability presents significant technical challenges as mobile terminals become increasingly compact and multifunctional. Component miniaturization exacerbates temperature sensitivity, with frequency variations potentially reaching ±20 ppm across operational temperature ranges without adequate compensation. Modern smartphones may experience internal temperature fluctuations exceeding 60°C during intensive processing tasks, requiring advanced compensation techniques that add complexity and cost. The industry response has been development of digitally compensated oscillators (DCXOs) with accuracy within ±0.1 ppm, but these solutions increase power consumption and component footprint. Additionally, mechanical stress from device assembly and everyday usage can induce frequency shifts up to ±3 ppm, necessitating robust packaging designs and manufacturing controls.

Other Challenges

Electromagnetic Interference Management

Increasing component density in mobile devices creates electromagnetic compatibility challenges that affect oscillator performance. RF transmitters operating at power levels up to 23 dBm can induce frequency pulling effects up to ±10 ppm in nearby timing components. Modern designs require sophisticated shielding techniques, ground plane isolation, and frequency planning that add engineering complexity and material costs. The proximity of multiple oscillators operating at different frequencies—typically between 32 kHz and 40 MHz for various functions—creates beat frequency interference that can degrade signal integrity and increase bit error rates in high-speed data interfaces.

Supply Chain and Manufacturing Constraints

Global supply chain vulnerabilities present ongoing challenges for crystal and oscillator availability. The industry experienced component lead times extending to 52 weeks during recent disruptions, particularly for specialized products requiring rare materials or proprietary processes. Manufacturing yield issues for frequency-critical components remain problematic, with initial production yields for high-frequency crystals sometimes below 60% due to the precise mechanical tolerances required. These challenges are compounded by increasing material costs for premium quartz substrates and specialized packaging materials, with raw material price fluctuations of 15-20% annually affecting overall component pricing.

MARKET RESTRAINTS

Cost Pressure and Value Engineering Limitations to Constrain Premium Component Adoption

Intense cost competition in the mobile terminal market creates significant restraints for premium timing components. Device manufacturers typically allocate less than 0.3% of total bill of materials costs to timing solutions, creating pressure for component suppliers to reduce prices annually by 5-8% while improving performance. This economic reality limits adoption of advanced technologies like MEMS oscillators with integrated power management, which may cost 300% more than basic crystal units. Value engineering initiatives often prioritize cost reduction over performance optimization, particularly in mid-range and entry-level devices representing over 65% of global shipments. The resulting specification compromises can lead to reduced frequency stability, higher jitter, and increased power consumption—trade-offs that become increasingly problematic as wireless standards evolve toward more stringent requirements.

Technical Standardization and Compatibility Issues to Hinder Market Expansion

The proliferation of wireless standards and frequency bands creates compatibility challenges that restrain market growth. Mobile terminals must now support up to 30 different frequency bands for global roaming, each requiring precise frequency references with specific stability characteristics. This multiplicity of requirements complicates component selection and increases inventory costs for device manufacturers. Furthermore, the lack of standardization across emerging technologies like 5G millimeter-wave applications creates uncertainty in component specifications, with different chipset providers recommending conflicting oscillator parameters. These compatibility issues become particularly acute in multi-chipset designs where timing components must interface with baseband processors, application processors, and connectivity chips from different suppliers, each with unique interface requirements and performance expectations.

Technological Obsolescence and Design Cycle Constraints to Limit Innovation Adoption

Rapid technological evolution creates obsolescence risks that restrain investment in advanced timing solutions. The average mobile device design cycle has compressed to under nine months, while qualifying new timing components typically requires 6-12 months of reliability testing and compatibility verification. This mismatch creates reluctance to adopt innovative technologies that might not demonstrate sufficient field reliability within project timelines. Additionally, the industry’s transition toward system-on-chip designs with integrated clocking solutions threatens traditional discrete component markets, with some advanced processors incorporating clock generation that reduces external component counts by up to 40%. While these integrated solutions rarely match the performance of discrete high-quality oscillators, their cost and space advantages create significant competitive pressure on standalone timing component suppliers.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and Industrial IoT to Create New Growth Vectors

The expansion of mobile-derived technologies into automotive and industrial applications represents significant growth opportunities. The automotive sector’s adoption of 5G-based vehicle-to-everything (V2X) communication requires timing components with automotive-grade reliability (-40°C to 125°C operating range) and exceptional frequency stability (±2.5 ppm). This market segment is projected to require over 200 million high-reliability oscillators annually by 2026. Industrial IoT applications present additional opportunities, particularly for components supporting Time-Sensitive Networking (TSN) with synchronization accuracy below 100 nanoseconds. These applications demand features not typically required in consumer mobile devices, including extended temperature operation, enhanced shock and vibration resistance, and longevity guarantees exceeding 10 years—specifications that command premium pricing and improve profit margins for component manufacturers.

Advanced Packaging and Integration Technologies to Enable Performance Breakthroughs

Innovations in packaging and integration create opportunities for performance enhancement and value creation. wafer-level packaging techniques enable oscillator footprints below 1.0 × 0.8 mm while improving resistance to mechanical stress and temperature variations. The integration of multiple crystal frequencies in single packages—particularly combinations of 32.768 kHz real-time clock crystals with higher-frequency main oscillators—reduces component count and board space requirements. These integrated solutions typically command 25-40% price premiums over discrete components while providing system-level benefits including reduced power consumption and improved reliability. Furthermore, the development of oven-controlled MEMS oscillators (OCMOs) combines the stability of traditional oven-controlled oscillators with the miniaturization and reliability advantages of MEMS technology, creating new opportunities in high-end mobile applications requiring exceptional frequency stability.

Strategic Partnerships and Vertical Integration to Enhance Market Position

Consolidation and partnership activities within the supply chain create opportunities for market expansion and technology advancement. Leading mobile chipset providers increasingly seek strategic partnerships with timing component suppliers to optimize system-level performance and reduce compatibility issues. These collaborations often involve joint development of customized solutions with specifications tailored to specific platform requirements, creating dedicated revenue streams and barriers to competition. Vertical integration opportunities exist through acquisitions of specialized design houses or manufacturing facilities, particularly those with expertise in advanced materials or proprietary compensation techniques. The ongoing transition toward 5G-Advanced and preliminary 6G research initiatives further stimulates investment in next-generation timing technologies, with several major industry players increasing research and development budgets by 15-20% annually to maintain technological leadership.

CRYSTAL AND OSCILLATORS FOR MOBILE TERMINAL MARKET TRENDS

5G Network Deployment and IoT Integration Driving Component Demand

The global rollout of 5G networks represents the most significant catalyst for the crystal and oscillators market in mobile terminals. These components are fundamental to maintaining the precise frequency stability and low phase noise required for 5G’s high-speed data transmission and massive device connectivity. With over 1.9 billion 5G subscriptions projected globally by the end of 2024, the demand for advanced timing solutions has surged correspondingly. Furthermore, the proliferation of Internet of Things (IoT) devices within the mobile ecosystem, including wearables and smart sensors, necessitates oscillators that can operate efficiently across diverse frequency bands and environmental conditions. This trend is pushing manufacturers to develop components that not only meet the rigorous performance standards of 5G but also support the power efficiency and miniaturization requirements essential for next-generation IoT applications.

Other Trends

Miniaturization and Component Integration

The relentless drive towards thinner, lighter, and more powerful mobile devices is compelling a shift towards increasingly miniature crystal and oscillator packages. Surface-mount device (SMD) packages, particularly those in the 2016 and 1612 sizes, are becoming the industry standard to conserve valuable PCB real estate. This miniaturization is paralleled by a trend towards higher integration, where multiple timing functions are consolidated into a single, compact module. This approach simplifies device architecture, improves reliability by reducing the number of discrete components, and enhances overall performance. However, achieving this without compromising on critical parameters like frequency stability or increasing power consumption remains a primary engineering focus for leading suppliers.

Advancements in Power Efficiency and Thermal Management

As mobile terminals incorporate more sophisticated features—from high-refresh-rate displays to always-on AI assistants—power management has become paramount. Modern crystals and oscillators are being engineered with ultra-low power consumption profiles, often operating at less than 1.5mA in active mode and featuring advanced standby or power-down modes that draw minimal current. This is crucial for extending battery life in energy-intensive 5G devices. Concurrently, effective thermal management is a growing concern. Components must maintain frequency stability across a wide temperature range, typically -40°C to +85°C, without performance degradation. Innovations in materials and packaging are continuously improving the thermal performance of these components, ensuring reliable operation even under the thermal loads generated by powerful mobile processors and RF front-ends.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Miniaturization Drive Strategic Positioning

The global crystal and oscillators market for mobile terminals is characterized by a highly competitive and fragmented landscape, dominated by established Japanese and Taiwanese manufacturers alongside emerging Chinese players. Intense competition stems from the critical need for components that offer superior frequency stability, minimal jitter, and ultra-low power consumption, all while adhering to the relentless trend of device miniaturization. Murata Manufacturing and NDK (Nihon Dempa Kogyo Co., Ltd.) are consistently recognized as market leaders, holding significant revenue shares due to their extensive product portfolios, strong R&D capabilities, and deep-rooted relationships with top-tier smartphone OEMs like Apple and Samsung.

Seiko Epson Corp and TXC Corporation also command considerable market presence, leveraging their expertise in quartz crystal technology to produce highly reliable and compact components essential for 5G modules and advanced connectivity features. Their growth is heavily attributed to continuous innovation in temperature-compensated crystal oscillators (TCXOs) and oven-controlled crystal oscillators (OCXOs), which are vital for maintaining signal integrity in complex mobile environments.

Furthermore, these leading companies are aggressively pursuing growth through strategic expansions in manufacturing capacity, particularly in Southeast Asia, to optimize supply chains and reduce costs. New product launches focusing on MHz-range crystals for main processors and kHz-range tuning fork crystals for real-time clocks are expected to further solidify their market positions throughout the forecast period.

Meanwhile, companies like SiTime are disrupting the traditional market with MEMS-based oscillators, which offer advantages in shock resistance, miniaturization, and programmability. This technological shift is pushing incumbent quartz-based manufacturers to accelerate their own innovation cycles. Similarly, Rakon is strengthening its foothold through significant investments in R&D for timing solutions tailored for precise positioning in mobile devices, ensuring continued dynamism within the competitive landscape.

List of Key Crystal and Oscillator Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- NDK (Nihon Dempa Kogyo Co., Ltd.) (Japan)

- Seiko Epson Corporation (Japan)

- TXC Corporation (Taiwan)

- SiTime Corporation (U.S.)

- Rakon Limited (New Zealand)

- Microchip Technology Inc. (U.S.)

- Kyocera Corporation (Japan)

- Daishinku Corp. (KDS) (Japan)

Segment Analysis:

By Type

Crystal Oscillators Segment Leads Due to Superior Frequency Stability and Integration in Advanced Mobile Devices

The market is segmented based on type into:

- Crystal Units

- Subtypes: Quartz Crystal Units, MEMS Crystal Units, and others

- Crystal Oscillators

- Subtypes: Temperature-Compensated Crystal Oscillators (TCXO), Oven-Controlled Crystal Oscillators (OCXO), Voltage-Controlled Crystal Oscillators (VCXO), and others

By Application

Smart Phone Segment Dominates Owing to Massive Global Production Volumes and Continuous Technological Upgrades

The market is segmented based on application into:

- 5G Base Station

- Smart Phone

- Data Center

- Others (including wearables, tablets, and IoT devices)

By Frequency Range

High-Frequency Components Gain Traction to Support 5G mmWave and High-Speed Data Processing Requirements

The market is segmented based on frequency range into:

- Low Frequency (Below 50 MHz)

- Medium Frequency (50 MHz to 200 MHz)

- High Frequency (Above 200 MHz)

By Package Type

Surface-Mount Device (SMD) Packages Prevail Due to Demands for Miniaturization and Automated Assembly

The market is segmented based on package type into:

- Surface-Mount Device (SMD)

- Through-Hole

- Chip-Scale Package (CSP)

Regional Analysis: Crystal and Oscillators for Mobile Terminal Market

Asia-Pacific

Asia-Pacific dominates the global crystal and oscillators market for mobile terminals, accounting for over 65% of the total market volume. This leadership is driven by the region’s status as the global manufacturing hub for smartphones and consumer electronics, with China alone producing approximately 70% of the world’s mobile devices. The relentless pace of 5G network deployment, particularly in China, South Korea, and Japan, fuels demand for advanced timing components that support higher frequencies and lower jitter. Furthermore, the region’s thriving ecosystem of local component manufacturers, such as TXC Corporation, NDK, and Hosonic Electronic, provides a competitive and cost-effective supply chain. However, intense price competition and the need for continuous miniaturization to accommodate ultra-thin device designs present ongoing challenges for manufacturers operating in this region.

North America

The North American market is characterized by high-value, innovation-driven demand, particularly from leading smartphone brands and telecommunications infrastructure providers. The region’s focus on next-generation technologies, including 5G mmWave applications, IoT integration, and advanced wearable devices, necessitates crystals and oscillators with exceptional frequency stability and low phase noise. The United States, with its robust semiconductor and telecommunications industries, is the primary contributor to regional growth. Companies like Microchip Technology and SiTime Corp. are at the forefront, developing MEMS-based oscillators that offer superior performance and resilience against environmental factors. Stringent quality requirements and a strong emphasis on intellectual property and supply chain security are key defining features of this market.

Europe

Europe’s market is propelled by a strong automotive and industrial IoT sector, which increasingly integrates mobile terminal technologies. The region exhibits a steady demand for high-reliability components that can operate effectively in a wide temperature range and under strict electromagnetic compatibility (EMC) regulations mandated by the EU. Germany, the UK, and France are the largest markets, hosting major R&D centers for mobile communications and automotive electronics. European demand is shifting towards more energy-efficient and environmentally compliant components, aligning with the region’s broader sustainability goals. While the volume may be lower than in Asia-Pacific, the focus on premium, high-performance applications ensures a stable and valuable market segment.

South America

The South American market is in a growth phase, primarily driven by increasing smartphone penetration and gradual infrastructure modernization in countries like Brazil and Argentina. Economic fluctuations and currency volatility can impact the cost of imported electronic components, making local assembly and price-sensitive designs more prevalent. The demand is largely for mid-range to entry-level mobile devices, which influences the specifications and cost points of the crystals and oscillators sourced. While the adoption of the latest 5G technology is slower compared to other regions, the ongoing expansion of 4G LTE networks continues to generate consistent demand for essential timing components.

Middle East & Africa

This region represents an emerging market with significant long-term potential, driven by rapid urbanization, growing investments in telecommunications infrastructure, and rising disposable incomes. Countries like Israel, Turkey, Saudi Arabia, and the UAE are leading the adoption of advanced mobile technologies. The market demand is bifurcated: a premium segment for high-end devices in urban centers and a volume-driven segment for affordable smartphones in developing areas. Challenges include navigating diverse regulatory landscapes and managing logistics for component distribution. Nonetheless, the ongoing digital transformation across the region is expected to steadily increase the consumption of crystals and oscillators for mobile terminals in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Crystal and Oscillators for Mobile Terminal markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Crystal and Oscillators for Mobile Terminal Market?

-> Crystal and Oscillators for Mobile Terminal Market was valued at 1507 million in 2024 and is projected to reach US$ 1697 million by 2032, at a CAGR of 1.8% during the forecast period.

Which key companies operate in Global Crystal and Oscillators for Mobile Terminal Market?

-> Key players include Seiko Epson Corp, TXC Corporation, NDK, Murata Manufacturing, and Microchip, among others.

What are the key growth drivers?

-> Key growth drivers include 5G deployment, mobile device innovation, wireless connectivity expansion, and increasing demand for power-efficient components.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 65% of global production and consumption, driven by major manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of components, ultra-low power oscillators, temperature-compensated crystal oscillators (TCXOs), and integration with IoT and AI functionalities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...