MARKET INSIGHTS

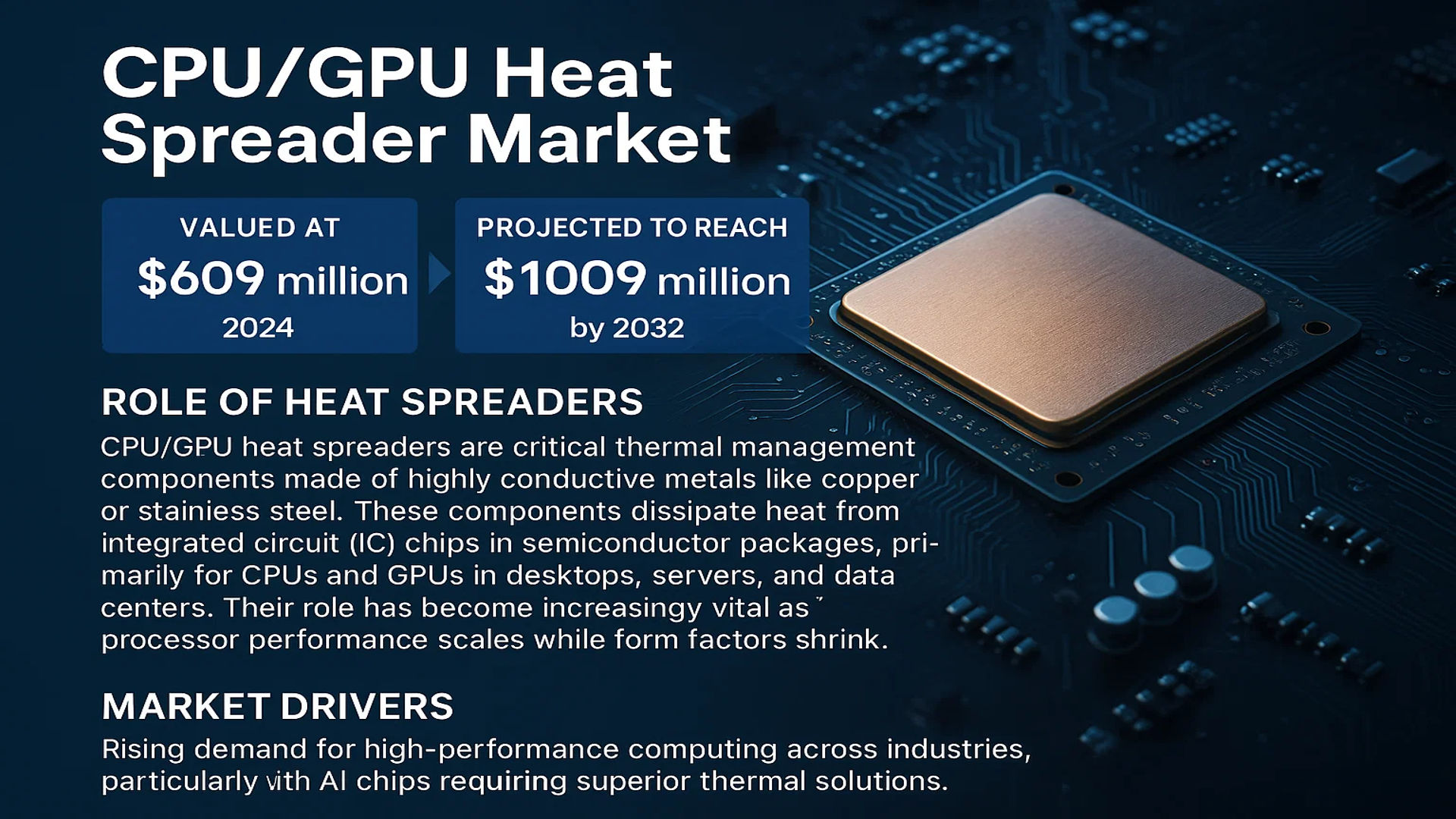

The global CPU/GPU Heat Spreader Market was valued at 609 million in 2024 and is projected to reach US$ 1009 million by 2032, at a CAGR of 7.1% during the forecast period.

CPU/GPU heat spreaders are critical thermal management components made of highly conductive metals like copper or stainless steel. These components efficiently dissipate heat from integrated circuit (IC) chips in semiconductor packages, primarily for CPUs and GPUs in desktops, servers, and data centers. Their role has become increasingly vital as processor performance scales while form factors shrink.

The market growth is driven by rising demand for high-performance computing across industries, particularly with AI chip advancements requiring superior thermal solutions. While copper remains dominant (89% market share in 2024), stainless steel variants are gaining traction due to higher durability in advanced packaging designs. Regionally, China Taiwan leads production with 57% market share, followed by Japan (16.7%) and the US (17.1%). Key players like Jentech Precision Industrial and Shinko collectively hold 91% market dominance, though competition is intensifying with new entrants.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Computing to Accelerate Heat Spreader Adoption

The global surge in high-performance computing (HPC) applications is driving substantial demand for advanced thermal management solutions. With data center workloads expected to grow at a compound annual growth rate exceeding 20% through 2030, the need for efficient CPU/GPU cooling has become critical. Heat spreaders have emerged as a fundamental component in modern computing architectures because they enable effective heat dissipation without relying solely on bulky cooling systems. The transition to smaller process nodes (5nm and below) has intensified thermal challenges, as chip densities continue increasing while physical dimensions shrink. This paradox is forcing engineers to innovate thermal solutions, with copper heat spreaders currently dominating 89% of the market due to their superior conductivity.

AI Chip Revolution Reshaping Material Preferences

Artificial intelligence processors are fundamentally altering heat spreader requirements, creating new growth avenues. The unique thermal profiles of AI accelerators have prompted a shift toward stainless steel heat spreaders, which offer higher hardness and better durability under continuous high-load operations. While copper currently maintains market dominance, emerging AI chip designs demand materials that can withstand higher pressure and maintain structural integrity across larger surface areas (up to 60mm x 60mm). This transition represents both a technical evolution and business opportunity, with stainless steel variants projected to capture over 25% of the thermal solution market for AI applications by 2027. The server/data center segment particularly benefits from these innovations, growing from 35% to an estimated 50% market share by 2032.

Miniaturization Trend in Electronics Strengthens Market Position

Consumer electronics’ relentless push toward thinner form factors amplifies the importance of compact thermal solutions. Contemporary all-in-one PCs and ultra-slim laptops increasingly integrate sophisticated heat spreaders as primary thermal management components. This trend aligns with the broader industry movement toward fanless designs in portable devices, where heat spreaders provide silent operation crucial for user experience. The proportion of heat spreaders sized above 35mm x 35mm has risen to 53% in 2024 and will likely reach 61% by 2032, reflecting both performance requirements and the space constraints of modern electronics. Taiwan’s manufacturing dominance (57% global share) positions it strategically to capitalize on these evolving demands through advanced production capabilities.

MARKET RESTRAINTS

Material Cost Volatility Disrupts Supply Chain Stability

The heat spreader industry faces significant pressure from fluctuating raw material prices, particularly for copper and specialty steel alloys. Global copper prices have demonstrated 20-30% annual volatility in recent years, directly impacting production costs for the 89% of heat spreaders using this material. Manufacturers struggle to maintain consistent pricing amidst these fluctuations, creating friction in long-term contract negotiations with OEMs. The situation worsens for emerging stainless steel variants, where specialized alloys command premiums up to 300% over standard grades. Smaller producers often lack the financial resilience to stockpile materials during price dips, placing them at a competitive disadvantage against established players who control 91% of the market.

Technical Barriers in Advanced Material Processing

Transitioning to next-generation heat spreader materials presents formidable technical obstacles. Stainless steel’s advantageous mechanical properties come with steep processing challenges – its hardness increases machining difficulty by approximately 40% compared to copper, while thermal conductivity drops nearly 90%. These physical realities force manufacturers to invest heavily in specialized equipment and process retooling. The technological divide leaves many mid-sized producers unable to compete in the premium segment, potentially consolidating market share among top-tier suppliers. Furthermore, precision requirements for larger form factors (above 60mm) exacerbate yield rate challenges, with rejection rates for complex geometries sometimes exceeding 15% in early production runs.

Geopolitical Factors Impacting Critical Material Access

Concentration of rare material sources creates supply chain vulnerabilities for heat spreader production. Certain alloying elements essential for high-performance variants originate from geopolitically sensitive regions, exposing manufacturers to trade restrictions and logistic disruptions. The industry’s heavy reliance on Taiwanese production (57% share) further compounds risk, as cross-strait tensions could potentially interrupt supply flows. These geopolitical complexities force companies to maintain costly inventory buffers and diversify supplier networks, adding 7-12% to operational expenses. Smaller players particularly feel this pressure, as they lack the scale to absorb these additional costs while remaining price competitive.

MARKET OPPORTUNITIES

Automotive Electronics Expansion Creates New Thermal Solution Demand

The automotive sector’s rapid electrification presents a substantial growth avenue for heat spreader technologies. Advanced driver assistance systems (ADAS) and autonomous driving platforms generate intense thermal loads that conventional cooling methods struggle to manage. Emerging vehicle architectures increasingly incorporate heat spreaders for domain controllers and AI processors, with the automotive SoC/FPGA segment projected to grow at 18% CAGR through 2030. The unique vibration and environmental requirements of automotive applications also drive innovation in material science, opening opportunities for specialized alloy development. This vertical’s rigorous qualification processes create barriers to entry that reward technically advanced suppliers with premium pricing power.

Advanced Packaging Innovations Requiring Custom Thermal Solutions

Cutting-edge chip packaging technologies like 3D IC and chiplets demand bespoke heat spreader configurations, creating value-added opportunities. These architectures introduce complex thermal management challenges as vertical stacking concentrates heat density beyond traditional two-dimensional patterns. Innovative heat spreader designs incorporating microfluidic channels or phase-change materials could capture this high-value segment. The market for specialized packaging thermal solutions is forecast to exceed $200 million annually by 2026, with gross margins 25-30% above standard products. Early movers in developing these solutions establish crucial intellectual property positions through patents on novel geometries and material combinations.

Emerging Economies Developing Domestic Supply Chains

Government initiatives in developing nations aim to reduce reliance on imported thermal solutions, creating partnership opportunities. China’s semiconductor self-sufficiency push has already boosted domestic heat spreader producers from 4.98% to an estimated 10.25% market share by 2032. Similar programs in India and Southeast Asia offer avenues for technology transfer and joint venture formations. These markets often prioritize cost-optimized solutions over maximum performance, enabling manufacturers to monetize mature production technologies while reserving advanced capacity for premium segments. The strategic value of local production is further enhanced by rising trade barriers and regional content requirements in government procurement.

MARKET CHALLENGES

Intellectual Property Protection in Rapidly Evolving Field

The heat spreader industry faces mounting intellectual property disputes as technological differentiation becomes critical. With gross margins under pressure from standard products, companies aggressively protect novel designs and processes. The surge in patent filings (over 300% increase since 2018) reflects both innovation and defensive posturing. Legal expenses now consume 5-7% of R&D budgets for major players, diverting resources from actual development. Smaller innovators risk being crowded out by larger competitors’ patent portfolios, potentially stifling diversity in solution approaches. International enforcement adds further complexity, as jurisdictional differences in IP protection create uneven playing fields.

Workforce Shortages in Precision Manufacturing

Specialized metalworking skills essential for heat spreader production face severe talent shortages globally. The industry requires technicians proficient in ultra-precision machining (tolerances under 10 microns) and exotic material handling, skills increasingly rare among younger workers. Training times for complex operations exceed eighteen months, creating bottlenecks in capacity expansion. This scarcity drives up labor costs by 12-15% annually in key manufacturing regions, disproportionately affecting smaller producers. Automation offers partial solutions, but the nuanced adjustments required for different materials and designs limit full robotic implementation, maintaining human expertise as a crucial differentiator.

Environmental Regulations Constraining Traditional Materials

Evolving environmental standards pressure manufacturers to reformulate proven heat spreader compositions. Restrictions on heavy metals and mining practices threaten supply stability for conventional copper alloys, while alternative materials often sacrifice performance. Compliance costs now account for 8-10% of production expenses, with new regulations frequently requiring complete process overhauls. The transition to greener alternatives also introduces technical uncertainty – bio-based thermal interface materials currently demonstrate 20-30% lower conductivity than metallic solutions. These constraints arrive amid growing customer demand for sustainable products, forcing manufacturers to balance ecological commitments with practical performance requirements.

CPU/GPU HEAT SPREADER MARKET TRENDS

Shift Toward High-Performance Computing Drives Heat Spreader Demand

The rapid evolution of high-performance computing (HPC) and artificial intelligence (AI) has intensified thermal management challenges, propelling demand for advanced CPU/GPU heat spreaders. With data centers handling larger workloads and AI chips requiring higher power densities, thermal dissipation has become a critical bottleneck. Heat spreaders, particularly those exceeding 35mm × 35mm in size, now account for 53% of the market, as modern processors incorporate more transistors and memory modules. This upward trend is expected to persist, with projections indicating that such large-sized spreaders will capture 61% of the market by 2032, reflecting the industry’s shift toward bulkier and more heat-intensive chip architectures.

Other Trends

Material Innovations: Transition from Copper to Stainless Steel

While copper has traditionally dominated the CPU/GPU heat spreader market—accounting for 89% of global production in 2024—manufacturers are increasingly turning toward stainless steel due to its superior durability and hardness. The emergence of AI and data center applications demands heat spreaders capable of withstanding prolonged high-temperature exposure without deformation. Stainless steel’s mechanical strength, coupled with its thermal conductivity properties, positions it as a key material for next-generation heat management. However, its adoption introduces manufacturing complexities, requiring precision machining techniques that may elevate production costs and widen the technological gap between market leaders and new entrants.

Data Center Expansion Fuels Long-Term Growth

The exponential growth of cloud computing and edge data centers is reshaping heat spreader applications. Server and data center CPU/GPU packages represented 35% of the market in 2024, but forecasts suggest this segment could match PC-based applications by 2032, reaching a 50% market share. Increasing 5G deployments and hyperscale data center constructions further amplify thermal management needs, with heat spreaders becoming indispensable for maintaining operational efficiency in compact, high-power-density environments.

Moreover, the rise of silicon photonics and 3D integrated circuits (3D-ICs) necessitates innovative heat dissipation strategies, compelling manufacturers to explore hybrid cooling solutions that integrate traditional spreaders with advanced thermal interface materials. As data traffic surges—driven by AI inference workloads and real-time analytics—heat spreader designs must evolve to address localized hotspots and ensure sustained performance in mission-critical infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Manufacturers Focus on Materials Innovation and Larger Form Factors to Gain Competitive Edge

The global CPU/GPU heat spreader market exhibits a semi-consolidated structure with notable dominance by Taiwanese and Japanese manufacturers, who collectively hold over 73% market share as of 2024. Jentech Precision Industrial and Shinko Electric Industries emerge as market leaders, owing to their vertically integrated manufacturing capabilities and strategic partnerships with major semiconductor foundries.

Chinese manufacturers are rapidly gaining traction in this space, with Shandong Ruisi Precision Industry and HongRiDa Electronics recording above-market growth rates exceeding 15% annually. Their competitive pricing strategies and government-supported R&D initiatives in advanced thermal materials pose a growing challenge to established players.

Material science breakthroughs represent the current competitive battleground, with companies like Honeywell Advanced Materials investing heavily in next-generation stainless steel alloys that combine superior thermal conductivity with structural rigidity. Meanwhile, traditional copper-based solutions from Fujikura and I-Chiun Precision Industry continue to dominate mainstream applications through continuous refinement of manufacturing processes.

The competitive intensity is further amplified by server/data center applications becoming the new growth frontier, accounting for 35% of 2024 demand and projected to reach 50% by 2032. Market leaders are responding with specialized product lines featuring enhanced thermal interfaces and improved mechanical stability for high-density computing environments.

List of Key CPU/GPU Heat Spreader Manufacturers

- Shinko Electric Industries Co., Ltd. (Japan)

- Fujikura Ltd. (Japan)

- Honeywell Advanced Materials (U.S.)

- Jentech Precision Industrial Co., Ltd. (Taiwan)

- I-Chiun Precision Industry Co., Ltd. (Taiwan)

- Favor Precision Technology Co., Ltd. (Taiwan)

- Niching Industrial Corporation (Taiwan)

- Fastrong Technologies Corp. (Taiwan)

- ECE (Excel Cell Electronic Co., Ltd.) (Taiwan)

- Shandong Ruisi Precision Industry Co., Ltd. (China)

- HongRiDa Electronics Co., Ltd. (China)

- TBT Co., Ltd (Korea)

Segment Analysis:

By Type

Copper Heat Spreaders Dominate Due to High Thermal Conductivity

The market is segmented based on material type into:

- Copper heat spreaders

- Standard copper alloys

- High-purity oxygen-free copper

- Stainless steel heat spreaders

- Austenitic grades

- Ferritic grades

- Aluminum heat spreaders

- Composite material heat spreaders

- Copper-graphite composites

- Metal matrix composites

- Diamond-based composites

- Others

By Size

Large-Sized Heat Spreaders Gain Traction with Increasing Chip Complexity

The market is segmented based on size into:

- Small-sized heat spreaders (below 35mm × 35mm)

- Medium-sized heat spreaders (35mm × 35mm to 50mm × 50mm)

- Large-sized heat spreaders (above 50mm × 50mm)

- Custom-sized heat spreaders

By Application

Server/Data Center Segment Experiences Rapid Growth Due to Cloud Computing Demand

The market is segmented based on application into:

- PC CPU/GPU packages

- Server/data center/AI chip packages

- Automotive SoC/FPGA packages

- Gaming consoles

- Consumer electronics

- Others

By Manufacturing Process

Precision Stamping Process Remains Widely Adopted for Cost-Effective Production

The market is segmented based on manufacturing process into:

- Precision stamping

- CNC machining

- Forging

- Additive manufacturing

- Others

Regional Analysis: CPU/GPU Heat Spreader Market

Asia-Pacific

The Asia-Pacific region dominates the global CPU/GPU heat spreader market, accounting for nearly 65% of production volume in 2022. Taiwan holds the lion’s share with major manufacturers like Jentech Precision Industrial and Favor Precision Technology operating in the region. This leadership position stems from Taiwan’s well-established semiconductor supply chain and proximity to key chip packaging facilities. China is emerging as a fast-growing player with companies like Shandong Ruisi Precision Industry expanding production capabilities to capitalize on domestic demand. The region benefits from strong government support for electronics manufacturing and continuous investments in AI and cloud infrastructure. However, rising labor costs and geopolitical tensions in the semiconductor supply chain pose challenges to sustained growth.

North America

North America represents the second-largest market, with the U.S. contributing about 17% of global heat spreader production. The region boasts advanced R&D capabilities, with companies like Honeywell Advanced Materials developing next-generation thermal solutions. Demand is primarily driven by expanding data center infrastructure and the gaming hardware sector. The U.S. Department of Defense’s increasing focus on advanced computing solutions for defense applications has created specialized requirements for ruggedized heat spreaders. Domestic manufacturers face pressure from lower-cost Asian producers but maintain competitiveness through innovation in materials science and patented manufacturing processes.

Europe

Europe’s market is characterized by steady demand from automotive electronics and industrial automation sectors. German engineering firms are pioneering heat spreader applications for automotive SoC packages, collaborating with leading automakers on thermal management solutions for electric vehicles. The region shows particular strength in high-performance computing applications, with academic institutions partnering with manufacturers on advanced cooling technologies. Strict EU environmental regulations are pushing manufacturers toward more sustainable production methods, including recycled copper usage. However, limited local production capacity means Europe remains dependent on imports for most standard heat spreader components.

South America

The South American market remains relatively small but shows potential for growth in consumer electronics applications. Brazil has emerged as a regional hub for final assembly operations, with some local manufacturers investing in basic heat spreader production lines. The market faces challenges from import restrictions and fluctuating currencies that impact components pricing. Growing gaming adoption and increasing internet penetration are driving demand for PC and console components, though most high-value manufacturing remains concentrated in other regions. Local players focus mainly on serving aftermarket and repair segments rather than OEM supply chains.

Middle East & Africa

This region represents an emerging opportunity as countries invest in digital infrastructure and data localization. The UAE and Saudi Arabia are establishing technology hubs that require server infrastructure, creating new demand for heat spreaders in data center applications. However, the market remains constrained by limited local manufacturing capabilities and reliance on imports. Some governments have introduced incentives to attract electronics manufacturers, which could potentially lead to future heat spreader production facilities. The market currently serves mainly through distribution channels from Asian manufacturers, with growth tied to broader technology adoption across the region.

Report Scope

This market research report provides a comprehensive analysis of the global CPU/GPU Heat Spreader market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global CPU/GPU Heat Spreader market was valued at USD 609 million in 2024 and is projected to reach USD 1009 million by 2032, growing at a CAGR of 7.1%.

- Segmentation Analysis: Detailed breakdown by product type (size above/below 35x35mm), material (copper, stainless steel), application (PC, server/data center, automotive, gaming), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Taiwan holding 57% production share in 2024.

- Competitive Landscape: Profiles of leading manufacturers like Shinko, Fujikura, Honeywell, and Jentech Precision, with top 5 players holding 91% market share in 2024.

- Technology Trends & Innovation: Assessment of material shifts from copper (89% share) to stainless steel, and increasing heat spreader sizes (53% above 35x35mm in 2024).

- Market Drivers & Restraints: Evaluation of factors like AI chip demand, server growth (projected 50% share by 2032), versus challenges in material processing and supply chain constraints.

- Stakeholder Analysis: Insights for thermal solution providers, semiconductor manufacturers, and investors regarding the evolving thermal management ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global CPU/GPU Heat Spreader Market?

-> CPU/GPU Heat Spreader Market was valued at 609 million in 2024 and is projected to reach US$ 1009 million by 2032, at a CAGR of 7.1% during the forecast period.

Which key companies operate in Global CPU/GPU Heat Spreader Market?

-> Key players include Shinko, Fujikura, Honeywell Advanced Materials, Jentech Precision Industrial, and I-Chiun, with top 5 holding 91% market share in 2024.

What are the key growth drivers?

-> Key growth drivers include AI chip adoption, server/data center expansion (35% share in 2024), and increasing thermal management requirements in advanced semiconductor packaging.

Which region dominates the market?

-> Taiwan is the dominant production region with 57% global share, followed by Japan (16.7%) and US (17.1%) in 2024.

What are the emerging trends?

-> Emerging trends include shift to stainless steel materials, larger heat spreader sizes (projected 61% above 35x35mm by 2032), and increasing server application share (50% by 2032).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...