CPCI Power Backplane Market Insights

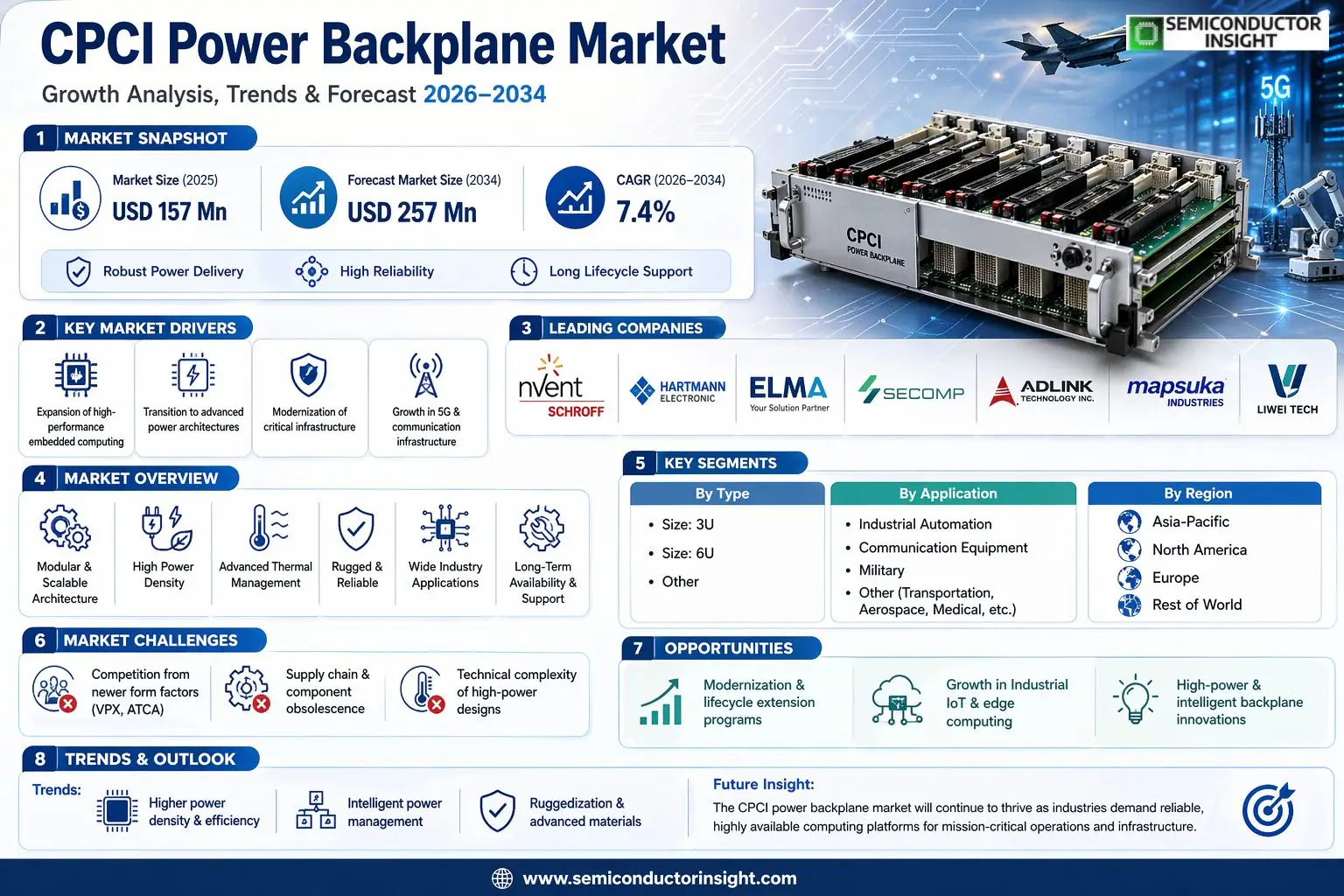

Global CPCI Power Backplane market size was valued at USD 157 million in 2025. The market is projected to grow from USD 168.6 million in 2026 to USD 257 million by 2034, exhibiting a CAGR of 7.4% during the forecast period.

A CPCI (CompactPCI) Power Backplane is a critical hardware component designed for the CompactPCI system architecture, primarily responsible for distributing power to various modules and components within the chassis. This backplane serves as the central nervous system for power delivery, ensuring stable and reliable operation across demanding applications. It is an indispensable part of systems used in sectors such as industrial automation, communication equipment, defense, transportation, and aerospace.

The market growth is driven by sustained demand from legacy industrial systems that rely on the robustness of the CompactPCI standard and ongoing modernization efforts within defense and communication infrastructure. However, the market faces challenges from newer form factors like VPX. Key players are focusing on innovation to enhance power density and reliability. For instance, companies like Elma Electronic and Adlink Tech continue to develop advanced backplane solutions that support higher current requirements and improved thermal management for next-generation applications in 5G networking and military upgrades.

MARKET DRIVERS

Expansion of High-Performance Embedded Computing

The primary driver for the CPCI Power Backplane Market is the robust demand for modular, high-availability computing in defense, telecommunications, and industrial automation. The CompactPCI (CPCI) standard offers superior reliability and efficient power distribution through its robust backplane architecture, which remains critical for systems requiring continuous operation. As embedded systems become more complex and power-hungry, the need for reliable CPCI power backplanes that can deliver stable, high-current power to multiple boards is intensifying.

Transition to Advanced Power Architectures

Technological evolution is propelling the CPCI Power Backplane Market forward, with a clear shift towards supporting newer, more efficient power standards and higher slot counts. Modern backplanes are being designed to accommodate advanced power management features, including intelligent power sequencing and hot-swap capabilities, which are essential for reducing system downtime in critical applications.

➤ The adaptability of the CPCI Power Backplane Market to hybrid systems, which combine legacy CompactPCI serial boards with newer PCI Express capabilities, ensures its sustained relevance in upgrading existing mission-critical infrastructure.

This enduring need for reliable, upgradeable embedded computing platforms continues to generate steady demand. The market benefits significantly from the long lifecycle and stringent certification requirements of sectors like aerospace and defense, where the proven performance of CPCI power backplanes is a major selection factor.

MARKET CHALLENGES

Competition from Newer Form Factors

A significant challenge for the CPCI Power Backplane Market is the competitive pressure from more modern embedded standards like VPX and AdvancedTCA. While CPCI offers proven reliability, newer architectures provide higher data throughput and denser processing capabilities, drawing design wins in next-generation systems. The CPCI market must continually demonstrate its superior value in ruggedness and long-term availability to maintain its niche.

Other Challenges

Supply Chain and Component Obsolescence

Sourcing long-lifecycle components compatible with the CPCI standard can be challenging, as semiconductor manufacturers often prioritize newer technologies. This can lead to extended lead times or necessary redesigns for the CPCI Power Backplane Market.

Technical Complexity of High-Power Designs

As board power requirements escalate, designing CPCI power backplanes that manage thermal dissipation, minimize voltage drop, and ensure signal integrity across all slots becomes increasingly complex and costly.

MARKET RESTRAINTS

Perception as a Legacy Technology

The most potent restraint on the CPCI Power Backplane Market is its perception as a mature or legacy solution. This can deter new system architects in fast-moving commercial sectors from specifying CPCI, opting instead for form factors perceived as more cutting-edge. This restraint limits market expansion primarily to established verticals with entrenched CPCI-based systems, slowing penetration into new application areas.

High Cost of Ruggedization

The very ruggedness that defines the CPCI Power Backplane Market for harsh environments also imposes cost restraints. The use of specialized materials, connectors, and extensive testing for shock, vibration, and extended temperature ranges results in a higher price point compared to commercial-grade backplanes, potentially limiting adoption in cost-sensitive projects.

MARKET OPPORTUNITIES

Modernization and Lifecycle Extension Programs

A key opportunity for the CPCI Power Backplane Market lies in the extensive installed base of legacy systems in military, transportation, and industrial control. There is a growing need for modern, drop-in replacement CPCI power backplanes that offer enhanced power delivery and monitoring while maintaining mechanical and electrical compatibility, allowing for system upgrades without costly full-platform replacements.

Growth in Industrial IoT and Edge Computing

The expansion of Industrial IoT (IIoT) and rugged edge computing creates a distinct opportunity. The reliability of the CPCI form factor is well-suited for harsh factory floor or remote field deployments. Manufacturers in the CPCI Power Backplane Market can capitalize on this by integrating features like enhanced power filtration for noisy electrical environments and support for Ethernet-based system management, aligning CPCI with modern industrial networking trends.

CPCI Power Backplane Market Trends

Advancements Towards High-Density and Power Efficiency

The primary trend shaping the CPCI power backplane market is the focused evolution towards higher power density and improved electrical efficiency. This shift is driven by the critical need for robust, intelligent power management within complex CompactPCI (CPCI) systems widely deployed across defense, aerospace, and industrial automation. The introduction of hybrid power architectures within advanced backplane designs now facilitates superior power delivery, enhanced thermal performance, and better management of peak loads. Market leaders are innovating to support modern processors and FPGAs that demand stable, precisely regulated high-current delivery, moving away from purely passive distribution to more integrated supervisory designs. This evolution directly addresses application demands for greater reliability and system longevity.

Other Trends

Consolidation and Vertical Integration Among Key Players

A significant market dynamic is the ongoing consolidation among system-level players and specialized manufacturers. Leading suppliers are vertically integrating to control more of the design, manufacturing, and testing chain for CPCI power backplanes to ensure stringent quality and performance standards. This trend, combined with strategic partnerships, is creating a more concentrated vendor landscape focused on providing full-system solutions rather than discrete components. Competition is shifting toward technical support, lifecycle management, and adherence to defense-grade specifications, as opposed to price alone.

Sustained Demand from Modernization of Critical Infrastructure

The enduring trend of upgrading legacy industrial control and defense systems continues to generate steady demand for CPCI power backplanes. As existing infrastructure undergoes modernization or replacement, the inherent ruggedness and modularity of the CPCI platform ensure its relevance. This drives consistent demand for 3U and 6U backplane variants. Additionally, new installations in sectors like advanced communication equipment and transportation systems are adopting enhanced CPCI power backplane solutions to ensure fail-safe operation and compliance with evolving safety and electromagnetic compatibility (EMC) standards.

Adoption of Advanced Materials for Reliability and Thermal Management

Manufacturers are increasingly utilizing advanced materials, such as specific laminates and conductive layers, to improve signal integrity and reduce power losses in CPCI power backplane designs. The push for higher operating temperatures requires better thermal management, achieved through materials with lower thermal resistance and optimized board layouts. This is particularly critical for high-reliability applications like aerospace, where failure is not an option. The trend underscores a market-wide emphasis on product ruggedization and design-for-environment philosophies, ensuring the CPCI power backplane remains the backbone of mission-critical systems.

COMPETITIVE LANDSCAPE

Key Industry Players

A High-Growth Niche Driven by Critical Infrastructure Demands

Global CPCI Power Backplane market, projected to grow from US$ 157 million in 2025 to US$ 257 million by 2034 at a CAGR of 7.4%, is characterized by a moderately concentrated competitive environment dominated by specialized industrial electronics suppliers. Global top five players commanded a significant collective revenue share in 2025, with nVent SCHROFF (nvent) often cited as a leading force. This leadership stems from comprehensive system solutions and a strong global footprint in enclosure and backplane technology, particularly for demanding applications in defense and industrial automation. The market structure requires players to offer not just components, but robust, high-reliability power distribution solutions that meet stringent standards for vibration, thermal management, and signal integrity, creating significant barriers to entry and favoring established engineering-centric firms.

Beyond the top-tier leaders, the landscape includes several other significant players carving out niches through application-specific expertise and regional strength. Companies like Elma Electronic and Hartmann Electronic have solidified reputations in Europe and North America for precision engineering in military and aerospace applications. Meanwhile, Asia-Pacific-based manufacturers, including ADLINK Technology, Secomp, and various Chinese firms like Shanghai Gaolin and Liwei Tech, are expanding their influence by catering to the region’s booming industrial automation and communication equipment sectors. These companies compete on reliability, customization capabilities, and cost-effectiveness, serving diverse verticals from transportation to medical imaging where the CompactPCI standard is employed for its ruggedness and modularity.

List of Key CPCI Power Backplane Companies Profiled

- nVent SCHROFF (nvent)

- Hartmann Electronic

- Elma Electronic

- Secomp S.p.A.

- ADLINK Technology Inc.

- Mapsuka Industries Co., Ltd.

- Horn Tech Industrial Corp.

- Liwei Tech Co., Ltd.

- Shanghai Gaolin Industrial Co., Ltd.

- Beijing Art Technology Development Co., Ltd.

- Shanxi Zhenghong Electronic Technology Co., Ltd.

- Beijing Yanxintong Science & Technology Co., Ltd.

- Xinhang Tianjin Technology Co., Ltd.

- PENTAIR Technical Solutions (Schroff)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

3U Size Backplanes represent the dominant product category due to their optimal balance between physical footprint and functional capacity. Their widespread adoption is driven by compatibility with a vast array of existing CompactPCI chassis and modules, making them the de-facto standard for many industrial and embedded systems. The form factor offers sufficient slot density for most applications while maintaining a compact profile that is crucial for space-constrained environments such as transportation and mobile platforms. Continuous design refinements in this segment focus on enhancing power delivery efficiency and thermal management to support newer, more power-hungry processor boards and I/O cards. |

| By Application |

|

Industrial Automation stands as the primary application segment, leveraging the CPCI architecture’s robustness for harsh manufacturing environments. The segment’s growth is underpinned by the critical need for reliable power distribution in programmable logic controllers, machine vision systems, and motion control racks where system uptime is paramount. Backplanes in this field are selected for their high mean time between failures, resistance to vibration and contaminants, and ability to facilitate modular system upgrades without major redesigns. This reliability directly translates to reduced production line downtime and supports the trend towards increasingly interconnected and smart factory infrastructures. |

| By End User |

|

Original Equipment Manufacturers (OEMs) constitute the leading end-user segment, as they integrate CPCI power backplanes directly into their final products such as industrial computers, test & measurement equipment, and specialized computing platforms. These users prioritize long-term supply stability, stringent quality certifications, and technical support from backplane suppliers to ensure the integrity of their own branded systems. The relationship is often collaborative, with OEMs working closely with manufacturers on custom specifications for pin assignments, power ratings, and connector types to meet unique application demands, thereby creating a strong dependency on reliable and technically proficient component partners. |

| By Power Rating |

|

High Power / High Current Backplanes are seeing increased demand, driven by the growing power requirements of advanced computing and processing cards used in data-intensive applications like signal processing and simulation. This segment is characterized by designs that incorporate heavier copper layers, enhanced thermal vias, and robust connector systems to manage increased electrical loads without overheating or voltage sag. The trend towards system consolidation, where multiple functions are housed in a single chassis, further amplifies the need for backplanes capable of cleanly delivering substantial power, making this a key area for technological innovation and supplier differentiation. |

| By System Criticality |

|

Mission-Critical Systems represent the most demanding and quality-focused segment, encompassing applications in defense, aerospace, and core network infrastructure where failure is not an option. Backplanes for these environments are subject to the most rigorous design, testing, and qualification processes, often requiring compliance with specific military or telecom standards. Key purchasing drivers include exceptional reliability, extended product lifecycles, traceability of components, and the ability to operate under extreme environmental stresses. This segment fosters long-term partnerships between users and a select group of specialized manufacturers known for their rigorous quality control and ability to support products over decades. |

Regional Analysis: Global CPCI Power Backplane Market

North America

The presence of leading defense primes and aerospace OEMs in North America creates a specialized, high-value segment for ruggedized CPCI Power Backplane Market solutions. These applications demand compliance with rigorous MIL-SPEC standards, driving innovation in vibration resistance, extended temperature ranges, and long lifecycle support not commonly required in commercial markets.

Aggressive 5G deployment and edge computing expansion across the region fuel demand for compact, high-efficiency power distribution within telecom enclosures. CPCI Power Backplane designs are critical for supporting the power-hungry processors and I/O cards in baseband units and network function virtualization hardware at the network edge.

North America hosts the corporate R&D centers and specialized engineering firms that drive architectural advancements in the CPCI Power Backplane Market. This ecosystem focuses on integrating intelligent power management, improving signal integrity at higher data rates, and developing novel cooling solutions for next-generation CompactPCI systems.

A well-established supply chain for advanced PCBs, connectors, and power components underpins regional manufacturing capability. Furthermore, active participation in industry consortia that define CPCI and related standards ensures North American designs often set de facto benchmarks for performance and interoperability in Global power backplane market.

Europe

Europe represents a sophisticated and stable market for CPCI Power Backplane solutions, characterized by strong demand from industrial automation, medical technology, and transportation sectors. The region’s emphasis on engineering precision, product longevity, and adherence to strict environmental and safety regulations shapes market requirements. German and French industrial equipment manufacturers, in particular, integrate these backplanes into sophisticated control and testing systems where reliability is paramount. The European space and defense industry also contributes to demand for radiation-tolerant and highly reliable designs. A trend towards modular and serviceable systems in industrial settings supports the continued use of CPCI architecture, ensuring a steady, quality-focused demand within the regional CPCI Power Backplane Market.

Asia-Pacific

The Asia-Pacific region is the fastest-evolving and most competitive arena in the CPCI Power Backplane Market, led by manufacturing powerhouses like China, Taiwan, South Korea, and Japan. Massive investments in industrial IoT, telecommunications infrastructure, and public transportation systems are key growth drivers. The region benefits from a vast electronics manufacturing ecosystem, which enables rapid prototyping and cost-effective production of backplane assemblies. However, the market is highly segmented, with demand ranging from low-cost, high-volume solutions for commercial applications to more specialized designs for robotics and precision instrumentation. Intense local competition fosters continuous innovation in miniaturization and power density, positioning Asia-Pacific as both a major consumer and a primary global manufacturing hub for power backplane components.

South America

The South American market for CPCI Power Backplane solutions is developing, with growth primarily linked to modernization projects in the industrial, energy, and telecommunications sectors. Countries like Brazil and Chile are focal points, where upgrades to national infrastructure and industrial automation initiatives create opportunities. The market is characterized by a preference for proven, reliable technologies that offer long-term stability over cutting-edge features, due to economic volatility and longer refresh cycles for capital equipment. Demand often stems from sectors such as oil & gas monitoring and public utility control systems, where robustness in challenging environmental conditions is a critical purchase factor for power backplane integration.

Middle East & Africa

The Middle East & Africa region presents a specialized niche within the CPCI Power Backplane Market. Demand is closely tied to large-scale infrastructure and defense projects, particularly in Gulf Cooperation Council (GCC) nations. The extreme environmental conditions,high temperatures and dust,necessitate the use of ruggedized and hardened electronic subsystems, where the reliability of the power delivery network is non-negotiable. Applications are found in oil & gas infrastructure monitoring, military communications, and airport operations systems. While the overall market volume is smaller compared to other regions, the requirements are highly specific, often demanding custom solutions with enhanced cooling and protection, leading to higher-value engagements for suppliers who can meet these stringent operational demands.

Report Scope

This market research report provides a comprehensive analysis of the CPCI Power Backplane Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CPCI Power Backplane Market?

-> Global CPCI Power Backplane Market was valued at USD 157 million in 2025 and is projected to reach USD 257 million by 2034, at a CAGR of 7.4% during the forecast period.

What is CPCI Power Backplane?

-> CPCI power backplane refers to the power distribution backplane used in CompactPCI (CPCI) system. It is a hardware component designed for CompactPCI system, used to distribute power to various modules and components in the system.

Which are the key applications of CPCI Power Backplane?

-> Key applications include Industrial Automation, Communication Equipment, Military, and other fields such as transportation and aerospace.

Which are the key companies in the CPCI Power Backplane market?

-> Key players include Nvent, Hartmann Electronic, Elma Electronic, Secomp, Adlink Tech, Mapsuka Industries, Horn Tech, Liwei Tech, Shanghai Gaolin, and Beijing Art Technology Development, among others.

How is the market segmented by product type?

-> The market is segmented by type, including Size: 3U, Size: 6U, and Other form factors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...