Contrastive learning for self-supervised video representation Market Insights

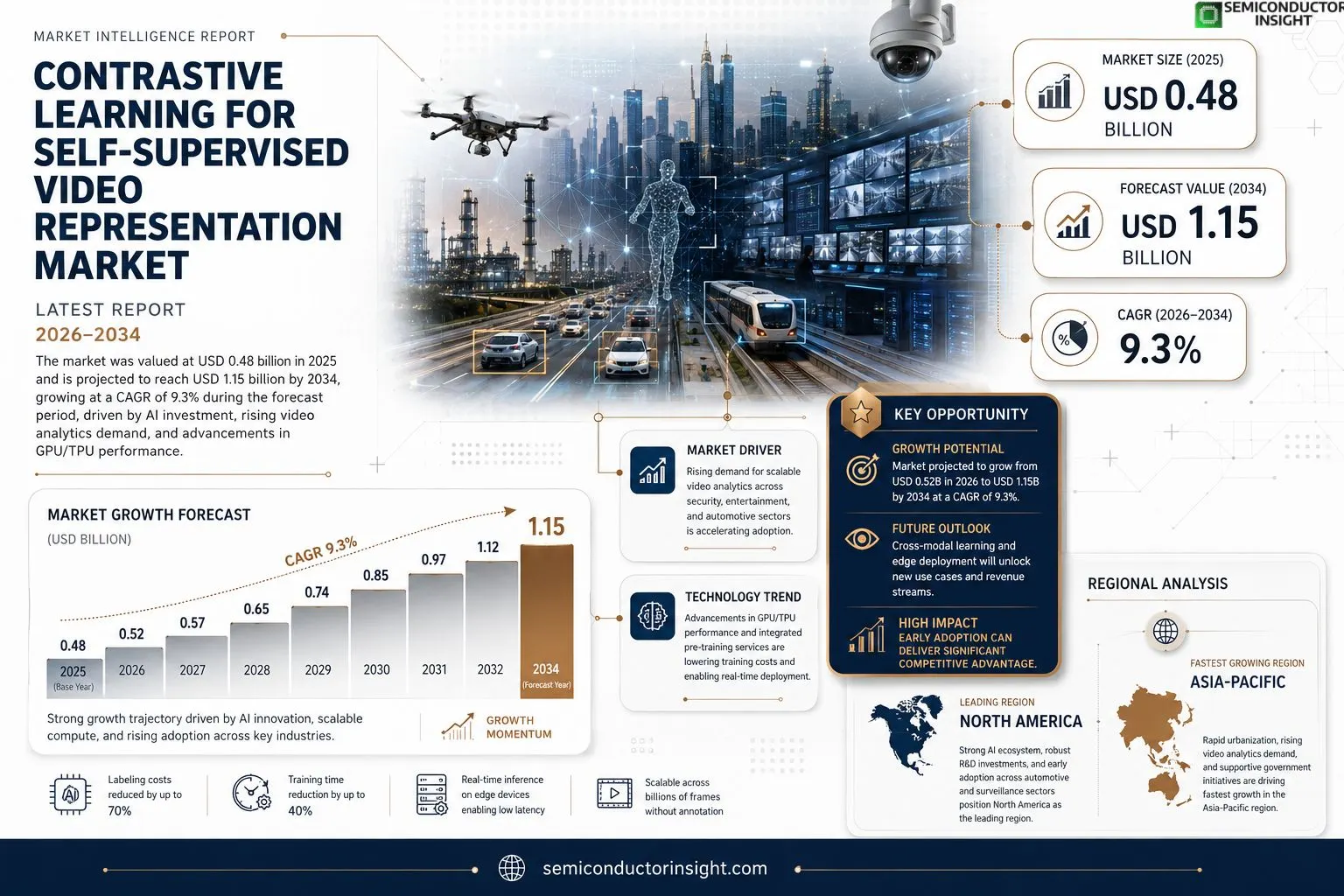

Contrastive learning for self-supervised video representation market size was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.52 billion in 2026 to USD 1.15 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

Contrastive learning for self-supervised video representation involves training neural networks to distinguish between similar and dissimilar video clips without relying on manual annotations, thereby producing robust feature embeddings that power downstream applications such as action recognition, video retrieval, autonomous navigation, and content moderation.The market is experiencing rapid growth because of heightened investment in artificial‑intelligence research, rising demand for scalable video analytics across security surveillance, entertainment streaming, and automotive domains, and continual improvements in GPU/TPU performance that lower training costs. Furthermore, strategic collaborations are accelerating adoption; for instance, in March 2024 a leading cloud provider launched an integrated contrastive‑video pre‑training service within its AI portfolio. Key players,including Meta AI, Google Research, Microsoft Azure AI, and OpenAI,are driving innovation through open‑source frameworks and proprietary solutions.

MARKET DRIVERS

Rising Demand for Video Analytics

The rapid expansion of video‑based services across retail, security, and entertainment is pushing enterprises to adopt more efficient representation techniques. Contrastive learning for self-supervised video representation Market benefits from a projected CAGR of 28% between 2024 and 2030, with market size expected to exceed $4.5 billion. This growth is driven by the need for scalable analytics that can process billions of frames daily.

Advancements in GPU & Edge Computing

Modern GPUs now deliver up to 12 TFLOPS for video tensors, while edge devices incorporate dedicated inference accelerators. These hardware strides lower the latency of contrastive pipelines, enabling real‑time deployment in autonomous drones and smart cameras. Companies that leverage this compute advantage can reduce model training time by up to 40%.

➤ Self‑supervised contrastive methods can cut labeling expenses by as much as 70 % while preserving accuracy comparable to fully supervised baselines.

Overall, the convergence of high‑volume video streams, affordable compute, and cost‑effective labeling creates a fertile environment for rapid adoption of contrastive self‑supervised solutions across the market.

MARKET CHALLENGES

Complexity of Contrastive Frameworks

Designing effective positive‑negative pair strategies requires deep domain expertise. Many organizations struggle to balance batch size, augmentation diversity, and temperature scaling, leading to sub‑optimal representations. This technical steepness slows down integration timelines for firms without dedicated AI research teams.

Other Challenges

Data Diversity Requirements

Successful contrastive training demands varied video domains,sports, surveillance, and cinematic content,to avoid representation collapse. Curating such heterogeneous datasets often incurs additional acquisition and preprocessing costs, hindering smaller players.

MARKET RESTRAINTS

High Computational Overhead

Contrastive objectives typically double the forward‑pass workload because each video clip must be processed through multiple augmentations. Even with optimized kernels, training cycles can extend beyond three weeks for large‑scale corpora, making budgeting for cloud resources a significant restraint.The necessity for large‑batch training also amplifies memory consumption, which limits adoption on commodity hardware and forces enterprises to invest in specialized clusters.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Systems

Autonomous vehicles and robotic platforms require robust visual understanding without extensive manual annotation. Contrastive self‑supervised video models can continuously learn from fleet‑collected streams, offering a competitive edge in perception accuracy while complying with data‑privacy regulations.Cross‑modal learning,combining audio, depth, and lidar with video,opens new revenue streams, as firms can fuse contrastive embeddings to create richer situational awareness for industrial monitoring and AR/VR experiences.Strategic partnerships between chipset manufacturers and AI startups are accelerating the rollout of on‑device contrastive pipelines, presenting high‑margin opportunities for early adopters in the market.

Contrastive learning for self-supervised video representation Market Trends

Rapid Growth Fueled by AI Research Investment

The market for contrastive learning for self-supervised video representation was valued at approximately USD 0.48 billion in 2025. Forecasts indicate a rise to USD 0.52 billion in 2026 and a further climb to around USD 1.15 billion by 2034, reflecting a compound annual growth rate close to 9.3 percent over the forecast horizon. This expansion is anchored in the technology’s ability to generate high‑quality video embeddings without extensive manual labeling, thereby reducing operational costs for downstream applications such as action recognition, video retrieval, autonomous navigation, and content moderation.

Other Trends

Key Industry Drivers

Investment in artificial‑intelligence research continues to accelerate, with major cloud providers allocating significant budgets to GPU and TPU infrastructure upgrades. The enhanced compute environment lowers training expenses, making contrastive video pre‑training more economically viable for enterprises. Concurrently, demand for scalable video analytics is rising across security surveillance, streaming entertainment, and automotive sectors, where real‑time video understanding is critical. These market pressures are complemented by regulatory encouragement for automated monitoring solutions, further propelling adoption.

Strategic Partnerships and Open‑Source Momentum

Collaboration ecosystems are shaping the competitive landscape. In March 2024, a leading cloud platform introduced an integrated contrastive‑video pre‑training service within its AI portfolio, enabling developers to leverage pre‑trained models with minimal configuration. Major players such as Meta AI, Google Research, Microsoft Azure AI, and OpenAI are contributing to open‑source frameworks, accelerating innovation cycles and fostering community‑driven improvements. This blend of proprietary solutions and shared resources is reducing time‑to‑market for new video‑centric products, while also expanding the talent pool familiar with contrastive learning techniques.

COMPETITIVE LANDSCAPEKey Industry Players

Emerging Competitive Dynamics in Contrastive Learning for Video Representation

Meta AI, Google Research, Microsoft Azure AI and OpenAI dominate the contrastive‑learning for self‑supervised video representation market. These firms leverage massive compute clouds and open‑source libraries such as PyTorch‑Video and TensorFlow‑Contrast to accelerate model pre‑training. Their leadership is evident in the rapid adoption of contrastive video pre‑training services launched by major cloud providers in 2024, which has helped push market size from USD 0.48 billion in 2025 to a projected USD 1.15 billion by 2034. The market structure is increasingly tiered: a handful of AI powerhouses provide end‑to‑end platforms, while niche specialist firms supply custom algorithmic components and domain‑specific datasets.Beyond the core incumbents, a vibrant ecosystem of niche innovators contributes depth and differentiation. NVIDIA supplies purpose‑built GPUs and SDKs that reduce training latency, while Intel’s OpenVINO optimizes inference for edge devices. Amazon Web Services offers Sage‑Maker extensions for contrastive video models, and Baidu and Alibaba focus on Chinese‑language video streams. Additional players such as Tencent, Huawei, Salesforce, Uber AI Labs, Adobe, Samsung Research, and DeepMind bring proprietary datasets, multimodal fusion techniques, and industry‑specific compliance tools that enrich the competitive landscape.

List of Key Contrastive learning for self-supervised video representation Companies Profiled

- Meta AI

- Google Research

- Microsoft Azure AI

- OpenAI

- NVIDIA

- Intel

- Amazon Web Services

- Baidu

- Alibaba Cloud AI

- Tencent

- Huawei Cloud AI

- Salesforce Research

- Uber AI Labs

- Adobe Sensei

- Samsung Research

- DeepMind

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Temporal Contrastive Models are emerging as the leading segment because they capture dynamic motion cues across video clips, enabling richer feature representations.

|

| By Application |

|

Action Recognition dominates application‑driven demand, driven by the need for real‑time interpretation of complex activities.

|

| By End User |

|

Surveillance & Security is the leading end‑user segment, leveraging contrastive video representations to enhance anomaly detection without extensive labeling efforts.

|

| By Technology |

|

GPU‑Accelerated Training is gaining traction as the primary technological enabler, because it dramatically shortens the time required to learn robust contrastive embeddings.

|

| By Industry |

|

Entertainment & Media leads industry‑level investment, driven by the need for scalable video indexing and personalized recommendation.

|

Regional Analysis: North America

North America

Extensive research initiatives are underway in North America, with universities and research institutions at the forefront of developing novel contrastive learning for self-supervised video representation algorithms. This strong R&D base fosters continuous advancements in the field.

Early adopters in North America are primarily focused on leveraging contrastive learning for self-supervised video representation to improve the accuracy and efficiency of video analytics in specific applications, showcasing a growing practical interest.

The increasing volume of video data, coupled with the need for automated and intelligent video analysis, is a major driver for Contrastive learning for self-supervised video representation Market in North America.

The North American market features a mix of established technology firms and emerging startups actively developing and deploying solutions based on contrastive learning for self-supervised video representation.

North America

The North American market for contrastive learning for self-supervised video representation is characterized by a proactive approach to technological advancements. The region’s robust venture capital ecosystem provides significant support for startups pioneering innovative solutions in this domain. The convergence of strong academic research and industrial application is accelerating the adoption of self-supervised techniques for video analysis, particularly in sectors demanding high accuracy and efficiency. This includes applications in security, healthcare, and intelligent transportation systems. The focus remains on developing algorithms that can learn meaningful video representations from unlabeled data, reducing the reliance on costly and time-consuming manual annotation.

Europe

Europe presents a mature market for contrastive learning for self-supervised video representation, with a strong emphasis on data privacy and ethical considerations. Regulatory frameworks like GDPR influence the development and deployment of video analytics solutions, leading to a focus on privacy-preserving technologies. The region’s industrial base, particularly in manufacturing and automotive, is driving demand for advanced video analysis for quality control, predictive maintenance, and autonomous driving applications. Research initiatives in Europe are often characterized by a collaborative approach, with significant involvement from public and private research institutions.

Asia-Pacific

The Asia-Pacific region is poised for substantial growth in Contrastive learning for self-supervised video representation Market. Rapid urbanization, increasing smartphone penetration, and the proliferation of video content are driving the demand for sophisticated video analysis solutions. The region’s large-scale infrastructure projects and smart city initiatives are creating significant opportunities for the adoption of these technologies in areas such as public safety, traffic management, and surveillance. Government support for technological innovation and the availability of skilled talent further contribute to the region’s growth potential.

South America

South America is an emerging market for contrastive learning for self-supervised video representation, with growing interest in applications such as security, retail analytics, and agriculture. While the adoption rate is currently lower compared to North America and Europe, the region’s increasing investments in technology and infrastructure are expected to drive significant growth in the coming years. Specific use cases are evolving to address local challenges, such as monitoring large areas and optimizing resource allocation.

Middle East & Africa

The Middle East & Africa represents a developing market for contrastive learning for self-supervised video representation, with opportunities in sectors like security, infrastructure monitoring, and smart city development. The region’s rapid economic growth and increasing government investments in technology are creating a favorable environment for the adoption of advanced video analytics solutions. The focus is on leveraging these technologies to enhance public safety, improve operational efficiency, and support sustainable development initiatives.

Report Scope

This market research report provides a comprehensive analysis of the Contrastive learning for self-supervised video representation Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Contrastive learning for self-supervised video representation Market?

-> Contrastive learning for self-supervised video representation Market was valued at USD 0.48 billion in 2025 and is expected to reach USD 1.15 billion by 2034

Which key companies operate in Contrastive learning for self-supervised video representation Market?

-> Key players include Meta AI, Google Research, Microsoft Azure AI, and OpenAI, among others.

What are the key growth drivers?

-> Key growth drivers include heightened investment in artificial‑intelligence research, rising demand for scalable video analytics across security surveillance, entertainment streaming, and automotive domains, and continual improvements in GPU/TPU performance that lower training costs.

Which region dominates the market?

-> North America is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include integrated contrastive‑video pre‑training services, open‑source frameworks, and ongoing hardware acceleration advancements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...