MARKET INSIGHTS

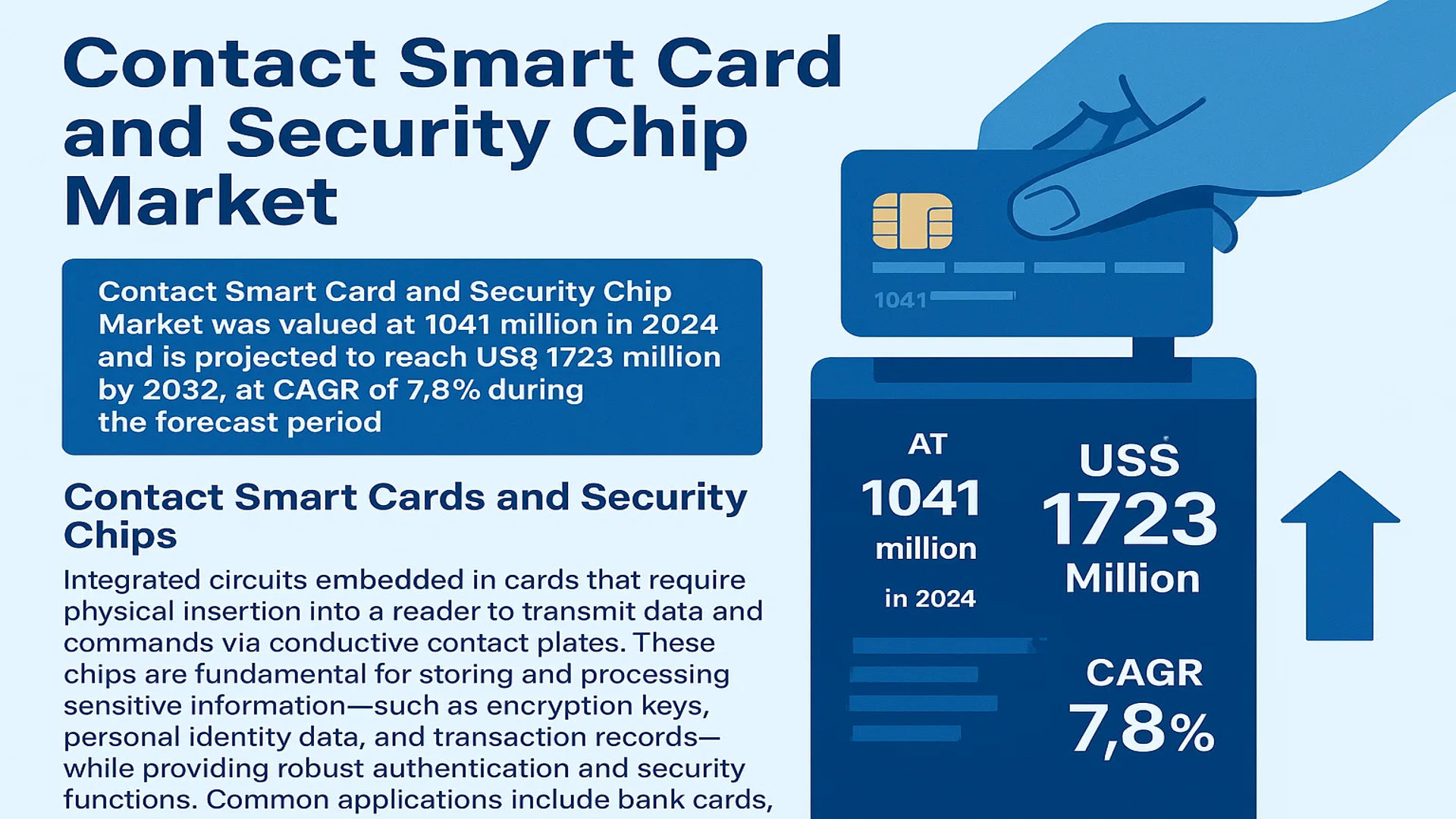

The global Contact Smart Card and Security Chip Market was valued at 1041 million in 2024 and is projected to reach US$ 1723 million by 2032, at a CAGR of 7.8% during the forecast period.

Contact smart cards and security chips are integrated circuits embedded in cards that require physical insertion into a reader to transmit data and commands via conductive contact plates. These chips are fundamental for storing and processing sensitive information—such as encryption keys, personal identity data, and transaction records—while providing robust authentication and security functions. Common applications include bank cards, electronic ID cards, transportation passes, and access control systems.

The market is experiencing steady growth driven by heightened global information security requirements and the ongoing adoption of EMV standards in the financial sector. While the rise of contactless technology presents competitive pressure in areas like payment and transit systems, contact-based solutions remain critical in applications demanding high-security assurance. Key players, including NXP Semiconductors, Infineon, and Samsung, collectively held over 45% of the market share in 2024, continuously innovating in chip design and multifunctional integration to meet evolving security and convenience demands.

MARKET DYNAMICS

MARKET DRIVERS

Global EMV Migration and Enhanced Payment Security Standards Accelerate Market Adoption

The global transition to EMV (Europay, Mastercard, Visa) chip technology represents one of the most significant drivers for contact smart card adoption. Financial institutions worldwide continue to phase out magnetic stripe cards in favor of more secure chip-based solutions, with over 90% of all card-present transactions globally now processed using EMV chip technology. This migration has dramatically reduced counterfeit fraud losses, which decreased by approximately 76% in regions that completed their EMV implementation. The ongoing requirement for stronger authentication protocols and the implementation of PSD2 regulations in Europe further compel financial institutions to upgrade their security infrastructure, creating sustained demand for contact smart cards with advanced security chips capable of handling cryptographic operations and secure element functionality.

Government Digital Identity Initiatives and National ID Programs Fuel Market Expansion

National digital identity programs represent a substantial growth driver, with governments worldwide implementing contact smart cards for citizen identification, healthcare, and social benefit distribution. Over 160 countries have now deployed or are planning electronic national ID systems incorporating contact smart card technology. These programs require high-security chips capable of storing biometric data, personal information, and supporting various government services. The integration of multiple applications onto a single card platform drives demand for microprocessor-based chips with enhanced memory capacity and advanced security features. The global electronic ID market is projected to grow at approximately 15% annually, directly contributing to the expansion of the contact smart card security chip market.

Rising Cybersecurity Threats and Financial Fraud Prevention Measures Drive Security Investments

Increasing sophistication in cyber attacks and financial fraud has created unprecedented demand for advanced security solutions. Financial institutions reported over 2.7 billion attempted fraudulent transactions in 2023, representing a 28% increase from the previous year. This escalation in threats drives investment in contact smart cards featuring security chips with enhanced encryption capabilities, secure key storage, and tamper-resistant designs. The banking sector alone accounts for approximately 42% of total contact smart card shipments, with continued growth expected as financial institutions implement multi-factor authentication and transaction verification systems. The constant evolution of security threats ensures ongoing research and development investments in chip security, maintaining market momentum.

Furthermore, regulatory requirements mandating stronger customer authentication protocols under frameworks such as Strong Customer Authentication (SCA) in Europe continue to drive replacement cycles and technology upgrades.

➤ For instance, recent mandates requiring dynamic data authentication for all payment transactions have accelerated the adoption of contact smart cards with cryptographic processors capable of generating unique transaction codes.

The convergence of these factors creates a robust growth environment, with financial institutions and government bodies prioritizing security enhancements that directly benefit contact smart card manufacturers and security chip providers.

MARKET CHALLENGES

Increasing Competition from Contactless Technology and Mobile Payment Solutions

The rapid adoption of contactless payment technology presents a significant challenge to traditional contact smart card growth. Contactless transactions have grown exponentially, representing over 55% of all face-to-face card payments in developed markets and showing a 30% year-over-year increase globally. Mobile wallet adoption continues to accelerate, with over 2.8 billion users worldwide preferring smartphone-based payment solutions over physical cards. This shift in consumer behavior pressures contact smart card manufacturers to demonstrate continued relevance and value proposition. While contact-based cards maintain advantages in high-security applications and certain markets, the convenience factor of contactless technology creates persistent competitive pressure that impacts market share and growth potential.

Other Challenges

Supply Chain Constraints and Semiconductor Shortages

Global semiconductor shortages continue to impact the smart card industry, with lead times for security chips extending to 26-32 weeks in 2024 compared to historical averages of 8-12 weeks. The specialized nature of security chip manufacturing, requiring certified fabrication facilities and stringent quality controls, exacerbates production challenges. These constraints affect manufacturers’ ability to meet demand fluctuations and maintain competitive pricing, particularly affecting smaller players without established supply chain relationships.

Rising Manufacturing and Certification Costs

Increasing complexity in security requirements drives higher development and certification costs. Achieving Common Criteria EAL 4+ certification or higher, now demanded by most financial and government clients, adds approximately 40-60% to development costs and extends time-to-market by 12-18 months. These rising barriers to entry concentrate market power among established players with sufficient resources to navigate the complex certification landscape, potentially limiting innovation and competition.

MARKET RESTRAINTS

High Implementation Costs and Infrastructure Requirements Limit Market Penetration

The substantial infrastructure investment required for contact smart card systems acts as a significant market restraint. Deploying contact-based smart card readers across merchant networks, government offices, and corporate environments requires considerable capital expenditure, with terminal costs ranging from $150-$400 per unit depending on functionality. This financial barrier particularly affects developing markets and small to medium-sized enterprises, where cost sensitivity is higher. The total cost of ownership for contact-based systems remains approximately 35-40% higher than magnetic stripe alternatives, creating resistance among price-sensitive market segments. While security benefits justify these costs for many applications, budget constraints continue to slow adoption rates in certain regions and vertical markets.

Technical Complexity and Interoperability Issues Hinder Seamless Integration

Technical challenges associated with contact smart card implementation present significant restraints to market growth. The requirement for physical contact creates mechanical wear issues, with typical contact smart cards rated for approximately 10,000 insertion cycles compared to virtually unlimited usage for contactless alternatives. Interoperability problems between different card readers and chip operating systems complicate large-scale deployments, particularly in cross-border applications. These technical complexities increase support costs and create user experience challenges that can deter adoption. Additionally, the physical interface limitations constrain design flexibility and form factor innovation, making contact-based solutions less adaptable to emerging applications compared to contactless alternatives.

Consumer Preference for Convenience and Speed Impacts Market Dynamics

Changing consumer preferences toward faster, more convenient payment methods restrain contact smart card growth in certain applications. Contactless transactions average 300-400 milliseconds compared to 2-3 seconds for contact-based EMV transactions, creating noticeable user experience differences. This speed advantage has driven contactless adoption across retail environments, transportation systems, and access control applications. While contact cards maintain advantages in high-value transactions and applications requiring enhanced security, the convenience factor increasingly influences purchasing decisions and technology specifications. This consumer-driven preference shift requires contact smart card manufacturers to continuously demonstrate superior security value to justify the additional processing time and physical interaction requirements.

MARKET OPPORTUNITIES

Emerging Applications in Healthcare and IoT Security Create New Growth Avenues

The expanding application of contact smart cards in healthcare systems presents substantial growth opportunities. Healthcare organizations increasingly adopt smart card technology for patient identification, electronic health records access, and prescription security. The global healthcare smart card market is projected to grow at 12.5% CAGR, driven by digital transformation initiatives and the need for secure patient data management. Contact-based solutions offer advantages in healthcare settings where reliability and security outweigh convenience considerations. Additionally, the integration of smart card technology into IoT security applications provides new opportunities, particularly in industrial control systems and critical infrastructure protection where physical connection requirements enhance security through air-gap protection.

Advanced Cryptographic Capabilities and Quantum-Resistant Security Development

The ongoing evolution of cryptographic threats creates opportunities for advanced security chip development. With quantum computing advancements threatening current encryption standards, demand is growing for quantum-resistant algorithms implemented in hardware security modules. Contact smart cards provide an ideal platform for deploying next-generation cryptographic solutions due to their physical security advantages and established infrastructure. Major financial institutions and government agencies are actively testing quantum-resistant algorithms, with planned implementations expected to drive card replacement cycles and technology upgrades. This technological evolution represents a significant opportunity for manufacturers developing chips capable of supporting advanced cryptographic operations while maintaining backward compatibility with existing systems.

Hybrid Card Solutions and Multi-Technology Integration

The development of hybrid cards combining contact and contactless functionality presents substantial market opportunities. These dual-interface cards account for approximately 38% of new card shipments and are growing at 20% annually. The ability to support both transaction methods allows organizations to maintain compatibility with existing infrastructure while offering contactless convenience where available. This approach particularly benefits markets undergoing gradual technology transition and applications requiring fallback options. The integration of additional technologies such as biometric sensors, display capabilities, and wireless charging further enhances value proposition and drives premium pricing opportunities. Manufacturers investing in multi-technology integration capabilities position themselves to capture value across multiple market segments and application scenarios.

CONTACT SMART CARD AND SECURITY CHIP MARKET TRENDS

Rising Demand for Enhanced Security and Multi-Functionality to Emerge as a Key Trend

The global contact smart card and security chip market is experiencing significant growth, primarily driven by escalating security requirements across financial, governmental, and corporate sectors. This demand is fueled by the increasing sophistication of cyber threats and the critical need to protect sensitive personal and financial data. The transition to EMV (Europay, Mastercard, and Visa) standards globally has been a major catalyst, with over 80% of all card-present transactions now utilizing chip technology for enhanced security. While contactless technology offers convenience, contact-based chips provide a robust, physically secure connection that is often preferred for high-value transactions and applications requiring stringent authentication, such as national ID programs and access control for secure facilities. The market is responding with chips that offer higher memory capacities, faster processing speeds, and advanced cryptographic capabilities, including support for elliptic curve cryptography (ECC) and post-quantum cryptography algorithms to future-proof security.

Other Trends

Convergence and Multi-Application Integration

A prominent trend is the move towards multi-application cards, where a single contact smart card consolidates several functions. This is particularly evident in government initiatives, where a national ID card can also serve as a health card, driver’s license, and public transportation pass. This convergence demands security chips with superior processing power and larger memory to handle multiple, isolated applications securely. The development of Java Card and MULTOS operating systems has been instrumental in this trend, enabling the deployment of various applications on a single secure platform. This not only enhances user convenience by reducing the number of cards carried but also drives higher-value chip sales, as these advanced, multi-functional chips command a premium price compared to standard single-application microcontrollers.

Technological Miniaturization and Advanced Manufacturing

The industry is witnessing continuous innovation in semiconductor manufacturing, leading to the production of more miniaturized, power-efficient, and cost-effective security chips. The adoption of finer process nodes, moving towards 40nm and below, allows for the integration of more complex security features and larger memory capacities within the same physical chip size. This miniaturization is crucial for applications in wearable technology and IoT devices, where space is at a premium. Furthermore, advancements in packaging, such as System-in-Package (SiP) and embedded silicon solutions, are enabling the integration of the security chip directly into devices like smartphones and passports, expanding the market beyond traditional plastic cards. These manufacturing advancements are simultaneously driving down costs per unit while increasing performance, making advanced security accessible for a broader range of applications and markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Security Enhancements to Maintain Market Position

The global contact smart card and security chip market features a semi-consolidated competitive structure, characterized by the presence of several established multinational corporations alongside emerging regional players. This dynamic is driven by continuous technological advancements and increasing security requirements across various sectors. NXP Semiconductors stands as a dominant force in this market, largely due to its extensive product portfolio, which includes highly secure microprocessor chips tailored for banking, government ID, and access control applications. The company’s robust global distribution network and significant investment in research and development further solidify its leadership, enabling it to capture a substantial market share, particularly in North America and Europe.

Infineon Technologies and Samsung are also major contenders, holding significant portions of the global market. Their growth is propelled by a strong focus on developing advanced security solutions, such as chips with enhanced encryption capabilities and tamper-resistant features. These companies benefit from longstanding relationships with key end-markets in the BFSI and government sectors, where security and reliability are paramount. Furthermore, their ongoing initiatives in product innovation, including the development of multi-application chips that support contact and dual-interface functionalities, are crucial for addressing evolving market demands.

Expansion strategies are equally important in this competitive environment. Companies are actively pursuing geographical growth, particularly in the Asia-Pacific region, which is experiencing rapid adoption of smart card technologies. New product launches that comply with the latest international security standards, such as Common Criteria and EMVCo, are frequent as firms strive to differentiate their offerings. These efforts are expected to significantly influence market shares over the coming years, as end-users increasingly prioritize vendors that can provide comprehensive, secure, and future-proof solutions.

Meanwhile, other significant players like STMicroelectronics and Shanghai Fudan Microelectronics Group Co., Ltd. are strengthening their positions through targeted investments in semiconductor manufacturing capabilities and strategic partnerships. By focusing on vertical integration and securing supply chains, these companies aim to enhance their product availability and reduce time-to-market for new innovations, ensuring they remain competitive in a market that values both security and efficiency.

List of Key Contact Smart Card and Security Chip Companies Profiled

- NXP Semiconductors (Netherlands)

- Infineon Technologies AG (Germany)

- Samsung (South Korea)

- STMicroelectronics (Switzerland)

- Shanghai Fudan Microelectronics Group Co., Ltd. (China)

- Unigroup Guoxin Microelectronics Co., Ltd. (China)

- HED (Germany)

- Microchip Technology Inc. (U.S.)

- Datang Telecom Technology Co.,Ltd. (China)

- Nations Technologies Inc. (China)

- Giantec Semiconductor Corporation (China)

Segment Analysis:

By Type

Microprocessor Chip Segment Dominates the Market Due to Superior Security and Processing Capabilities

The market is segmented based on type into:

- Memory Chip

- Microprocessor Chip

- RFID Chip

- Security Chip

- Others

By Application

BFSI Segment Leads Due to Mandatory EMV Migration and High Security Requirements

The market is segmented based on application into:

- BFSI

- Government & Public Utilities

- Transportation

- Others

Regional Analysis: Contact Smart Card and Security Chip Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global contact smart card and security chip market, accounting for the largest market share by both volume and revenue. This leadership is primarily driven by massive government-led digital identity initiatives and the rapid expansion of the banking sector. China’s national electronic ID card program, which has issued over 1 billion cards, represents one of the largest deployments of contact smart card technology globally. India’s Aadhaar project, with its linked banking and subsidy systems, further fuels demand for secure microprocessor chips. The region also benefits from being the manufacturing hub for major global players like Samsung and housing domestic powerhouses such as Shanghai Fudan Microelectronics. While cost sensitivity leads to a mix of memory and microprocessor chip adoption, there is a clear, accelerating trend towards higher-security chips to combat rising financial fraud and support integrated applications in public transit and healthcare.

North America

North America represents a mature yet steadily growing market, characterized by high-value, security-intensive applications. The region’s demand is heavily anchored in the BFSI sector, where the full migration to EMV chip technology has been a primary driver. The United States, in particular, accounts for a significant portion of the regional market due to strict payment security standards and the widespread use of credit and debit cards. Beyond finance, there is growing adoption in government sectors for secure access cards and in healthcare for patient ID and data security. The market is highly competitive, with leading technology firms like NXP Semiconductors and Microchip continuously innovating to offer chips with enhanced encryption and anti-tampering features. The focus is less on volume and more on advanced security, reliability, and compliance with stringent regulations, making it a high-revenue-per-unit market.

Europe

Europe is a highly regulated and innovation-driven market for contact smart cards. Stringent data protection laws, notably the General Data Protection Regulation (GDPR), mandate the highest levels of security for personal data, making embedded security chips indispensable. The region has been a long-time adopter of smart card technology, evident in its standardized chip-based payment systems and national e-ID programs in countries like Germany and France. The market is transitioning from single-application cards to multi-application chips that combine functions such as payment, public transportation, and digital signature. This push for multifunctionality, coupled with a strong focus on standardization and interoperability under frameworks like those from the European Telecommunications Standards Institute (ETSI), ensures sustained demand for advanced microprocessor chips from suppliers like Infineon and STMicroelectronics.

South America

The South American market for contact smart cards is in a developing phase, presenting both opportunities and challenges. Countries like Brazil and Argentina are gradually modernizing their financial and governmental systems, which creates a foundational demand for basic smart card solutions. The primary growth is observed in the banking sector’s shift towards EMV cards to reduce fraud. However, economic volatility often constrains large-scale public sector investments in sophisticated national ID or health card projects. Consequently, while the potential for growth is significant, the adoption of high-end security chips is slower compared to more developed regions. The market currently leans towards cost-effective solutions, but as economies stabilize and digital infrastructure improves, a shift towards more secure and integrated applications is anticipated.

Middle East & Africa

The Middle East and Africa region represents an emerging market with pockets of high growth potential, particularly in the Gulf Cooperation Council (GCC) countries. Nations like the UAE, Saudi Arabia, and Israel are investing heavily in smart government initiatives, digital ID programs, and modernized financial services, all of which require robust contact smart card solutions. These projects are often driven by national visions for economic diversification and digital transformation. In contrast, other parts of the region face challenges related to infrastructure development and funding, which slows widespread adoption. The market is characterized by a dual trajectory: advanced, security-focused deployments in wealthier nations and more gradual, foundational adoption in developing economies. The long-term outlook remains positive as urbanization and digitalization efforts continue to gain momentum.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Contact Smart Card and Security Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Contact Smart Card and Security Chip Market?

-> Contact Smart Card and Security Chip Market was valued at 1041 million in 2024 and is projected to reach US$ 1723 million by 2032, at a CAGR of 7.8% during the forecast period.

Which key companies operate in Global Contact Smart Card and Security Chip Market?

-> Key players include NXP Semiconductors, Infineon, Samsung, STMicroelectronics, Shanghai Fudan Microelectronics Group Co., Ltd., and Unigroup Guoxin Microelectronics Co., Ltd., among others.

What are the key growth drivers?

-> Key growth drivers include increasing global information security requirements, EMV standard adoption in banking, demand for secure payment authentication, and multifunctional integration in government ID programs.

Which region dominates the market?

-> North America holds the largest market share, accounting for over 35% of global demand in 2024, driven by financial sector adoption, while Asia-Pacific demonstrates the fastest growth rate.

What are the emerging trends?

-> Emerging trends include miniaturization of security chips, multifunctional card integration, enhanced cryptographic capabilities, and increased adoption in healthcare and transportation applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...