MARKET INSIGHTS

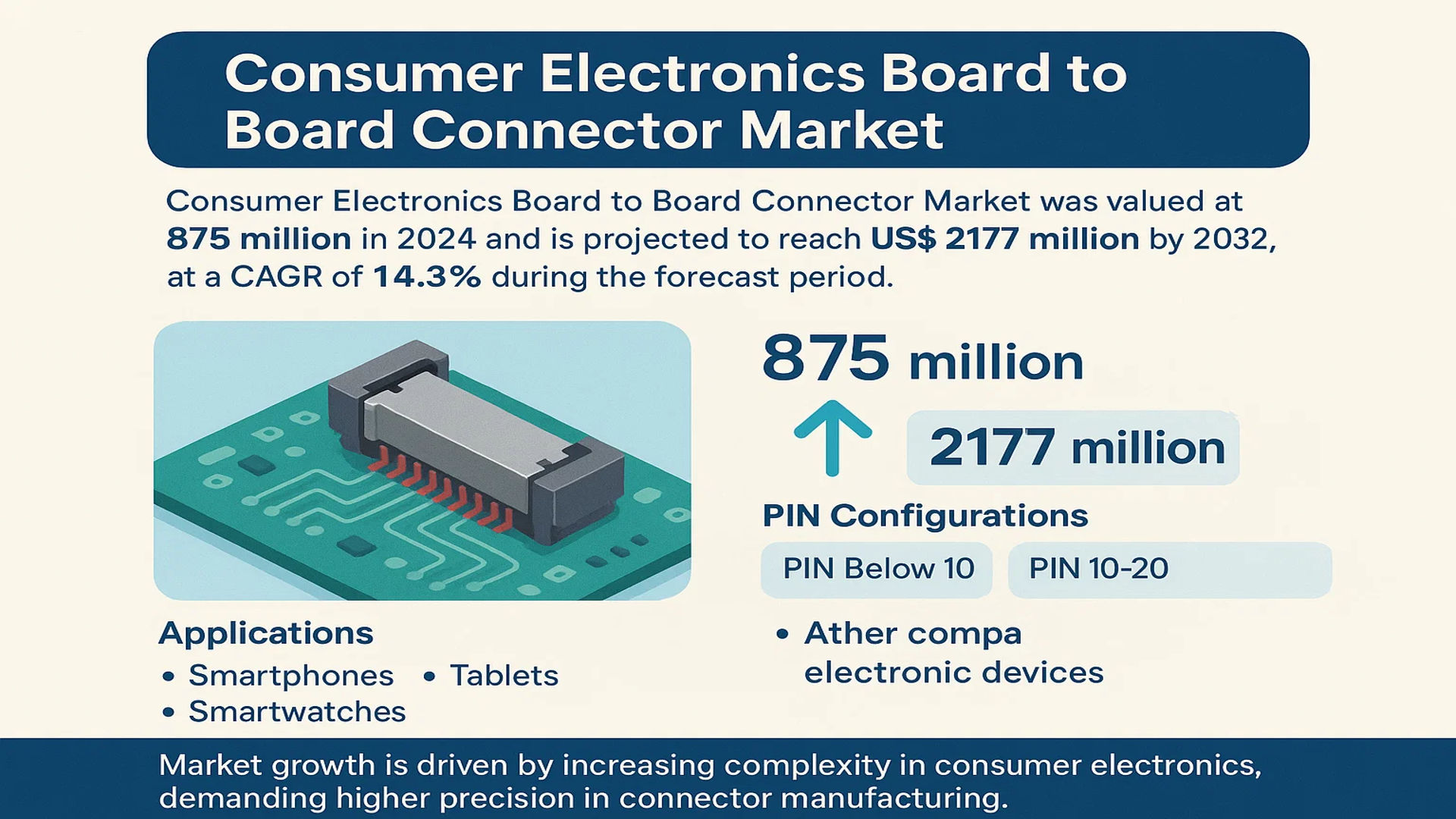

The global Consumer Electronics Board to Board Connector Market was valued at 875 million in 2024 and is projected to reach US$ 2177 million by 2032, at a CAGR of 14.3% during the forecast period.

Board-to-board connectors are critical components in electronic devices that enable signal and power transmission between printed circuit boards (PCBs). These connectors are categorized based on pin configurations, including PIN Below 10, PIN 10-20, and PIN Above 20 variants. They play a vital role in applications such as smartphones, tablets, smartwatches, and other compact electronic devices where space optimization and high-speed data transfer are essential.

The market growth is driven by increasing complexity in consumer electronics, demanding higher precision in connector manufacturing. Miniaturization trends and advancements in high-frequency signal transmission have elevated technical requirements for these components. Leading manufacturers like Molex, TE Connectivity, and Amphenol dominate this highly concentrated market, investing in R&D to meet evolving industry standards. The Asia-Pacific region holds the largest market share due to its robust electronics manufacturing ecosystem.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Complexity and Miniaturization of Consumer Electronics to Drive Market Growth

The global consumer electronics board to board connector market is experiencing robust growth driven by the increasing complexity and miniaturization of electronic devices. Modern smartphones now incorporate advanced features including 5G connectivity, augmented reality capabilities, and sophisticated camera systems requiring multiple board interconnections. This trend is driving demand for high-density board to board connectors that can handle high-frequency signals while maintaining electromagnetic compatibility. The average smartphone now contains approximately 15-20 board to board connectors, representing a significant increase from the 8-12 connectors found in devices from five years ago. This trend is particularly pronounced in premium devices, where the number of connectors can exceed 25 units per device. The market is further driven by the growing adoption of flexible printed circuit board connections in foldable devices and wearables, creating additional demand for specialized connector solutions.

Growing Demand for High-Speed Data Transmission and 5G Connectivity to Accelerate Market Expansion

The global market is experiencing significant growth driven by the increasing demand for high-speed data transmission capabilities required by advanced consumer electronics. The widespread adoption of 5G technology has created unprecedented requirements for connectors capable of handling data rates exceeding 10 Gbps while maintaining signal integrity. This has led to the development of advanced connector designs featuring improved impedance matching and reduced crosstalk. The market is further driven by the increasing adoption of high-resolution displays requiring high-speed video interfaces and the growing complexity of camera systems in mobile devices. These applications require connectors that can support multiple high-speed data channels simultaneously while maintaining minimal signal degradation.

Furthermore, the increasing integration of artificial intelligence processors and machine learning capabilities in consumer devices is creating additional requirements for high-speed interconnects that can handle the massive data transfer rates required by these applications.

➤ For instance, leading connector manufacturers have recently introduced new connector series specifically designed for high-speed applications, featuring improved signal integrity and reduced insertion loss.

Additionally, the market is benefiting from the growing adoption of IoT devices and smart home applications, which require reliable board to board connections for various sensor and communication modules.

Expansion of Wearable Technology and IoT Devices to Drive Market Growth

The wearable technology market is experiencing remarkable growth, creating substantial opportunities for board to board connector manufacturers. Smartwatches, fitness trackers, and other wearable devices require ultra-miniature connectors that can withstand daily wear and tear while maintaining reliable connections. These devices typically require connectors with pitches below 0.4mm and often incorporate waterproof and dustproof features. The market is further driven by the growing adoption of medical wearables and health monitoring devices, which require specialized connectors that can handle medical-grade requirements while maintaining small form factors. This trend is creating demand for connectors that can handle both power and data transmission in extremely constrained spaces.

Moreover, the increasing adoption of IoT devices across various consumer applications is creating additional demand for board to board connectors. These applications require connectors that can handle various environmental conditions while maintaining reliable connections.

Additionally, the growing adoption of augmented reality and virtual reality devices is creating new requirements for connectors that can handle high-speed data transmission while maintaining small form factors.

MARKET CHALLENGES

High Technical Requirements and Manufacturing Complexity to Challenge Market Growth

The consumer electronics board to board connector market faces significant challenges related to the high technical requirements and manufacturing complexity involved in producing these components. The market requires connectors that can handle increasingly higher data rates while maintaining signal integrity and electromagnetic compatibility. This requires advanced manufacturing processes involving precision stamping, injection molding, and plating processes that require substantial investment in specialized equipment and skilled personnel. The manufacturing of high-frequency connectors requires specialized materials and processes that can be challenging to scale for mass production while maintaining consistent quality. This is particularly challenging for connectors with pitches below 0.3mm, where manufacturing tolerances become extremely tight and require specialized manufacturing processes.

Other Challenges

Increasing Cost Pressures

The consumer electronics market is characterized by intense cost pressures, which creates challenges for connector manufacturers. Original equipment manufacturers are constantly seeking to reduce component costs while maintaining or improving performance. This creates significant challenges for connector manufacturers who need to invest in advanced manufacturing processes and materials while facing constant pressure to reduce prices. This challenge is particularly acute for high-performance connectors that require specialized materials and processes.

Supply Chain Complexity

The global supply chain for connector manufacturing involves multiple specialized processes and materials that can be challenging to manage. This complexity creates challenges related to material availability, quality control, and logistics. The recent global supply chain disruptions have highlighted the vulnerabilities in the connector supply chain and the challenges involved in maintaining consistent supply while managing multiple specialized processes and materials.

MARKET RESTRAINTS

Increasing Competition and Price Pressure to Deter Market Growth

The consumer electronics board to board connector market is facing significant restraints related to increasing competition and price pressure from original equipment manufacturers. The market is characterized by intense competition between established players and new entrants, leading to constant pressure to reduce prices while maintaining or improving performance. This creates challenges for manufacturers who need to invest in advanced manufacturing processes and materials while facing constant pressure to reduce prices. This restraint is particularly challenging for high-performance connectors that require specialized materials and processes that are more expensive to produce.

Additionally, the market is facing challenges related to the increasing complexity of connector designs and the need to support multiple applications and interfaces. This creates challenges related to inventory management and production planning, as manufacturers need to manage multiple connector variants with different specifications and requirements.

Furthermore, the market is facing challenges related to the increasing requirements for environmental compliance and sustainability, which require additional investment in materials and processes that meet these requirements.

MARKET OPPORTUNITIES

Emerging Applications in Automotive Electronics and Advanced Consumer Devices to Provide Profitable Opportunities

The market is experiencing significant opportunities from emerging applications in automotive electronics and advanced consumer devices. The automotive industry is increasingly incorporating advanced electronic systems requiring high-reliability board to board connectors that can handle harsh environmental conditions. This creates opportunities for connector manufacturers who can provide connectors that meet automotive-grade requirements while maintaining small form factors. The market is further driven by the growing adoption of advanced driver assistance systems and infotainment systems requiring high-speed data transmission capabilities.

Additionally, the market is benefiting from the growing adoption of advanced consumer devices incorporating artificial intelligence and machine learning capabilities, which require connectors that can handle high-speed data transmission while maintaining small form factors.

Furthermore, the market is experiencing opportunities from the growing adoption of advanced display technologies and camera systems in consumer devices, which require connectors that can handle high-speed video interfaces and power transmission.

CONSUMER ELECTRONICS BOARD TO BOARD CONNECTOR MARKET TRENDS

Miniaturization and High-Speed Data Transmission Driving Market Evolution

The relentless push towards miniaturization in consumer electronics is fundamentally reshaping the board-to-board connector landscape. As devices like smartphones, tablets, and wearables become thinner and more compact, the demand for connectors with a lower profile and finer pitch has surged dramatically. This trend necessitates advanced manufacturing techniques, particularly in precision mold design, to produce connectors that can reliably handle high-frequency signals while occupying minimal space. Concurrently, the exponential growth in data consumption requires connectors that support significantly higher data rates. The transition to 5G technology and the proliferation of high-definition multimedia content are compelling manufacturers to develop solutions that ensure electromagnetic compatibility and stable signal integrity at speeds exceeding 20 Gbps. This dual pressure for smaller form factors and superior performance represents a primary growth vector for the market.

Other Trends

Expansion in High-Pin-Count Applications

While miniaturization is critical, there is a parallel and significant trend towards the adoption of connectors with a higher number of pins, particularly those in the PIN Above 20 category. This growth is directly linked to the increasing functional complexity of modern devices. Advanced smartphones, for instance, now incorporate multiple cameras, sophisticated sensors, and powerful processors, all of which require a dense network of interconnections within a confined motherboard architecture. This complexity drives the consumption of high-pin-count board-to-board connectors, as they are essential for facilitating the necessary data and power pathways between various sub-assemblies and printed circuit boards (PCBs).

Consolidation and Technological Barriers Intensifying Market Concentration

The global market is characterized by a high degree of concentration among a limited number of established players, a situation exacerbated by significant technical and manufacturing barriers. The expertise required for precision engineering, mass production of micro-connectors, and ensuring consistent performance under high-frequency conditions creates a high entry threshold for new participants. This has led to a market where the top five companies collectively hold a substantial share of the global revenue. Furthermore, recent industry developments point towards increased collaborative research initiatives and strategic mergers and acquisitions as key players seek to pool R&D resources and expand their technological portfolios to maintain a competitive edge. This consolidation trend is expected to continue as the technological requirements become even more stringent.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Accelerate Innovation in Miniaturized Connector Solutions

The global consumer electronics board-to-board connector market features a competitive and technologically advanced landscape dominated by established players with strong R&D capabilities. With increasing demand for high-density, miniaturized connectivity solutions, companies are focusing on developing high-precision connectors that meet evolving industry standards. The market is moderately consolidated, with the top five players accounting for approximately 35-40% of the 2024 market share.

TE Connectivity and Molex currently lead the market, leveraging their extensive product portfolios and global distribution networks. These industry giants have maintained their positions through continuous innovation in micro-pitch connectors and strategic acquisitions. Meanwhile, Japanese manufacturers like JAE Electronics and Hirose Electric (HRS) are gaining traction through their expertise in ultra-fine pitch solutions popular in compact smart devices.

Emerging players from Asia, particularly Chinese manufacturers such as Sunway Communication and Acon, are challenging established brands with cost-competitive alternatives. However, their market penetration remains limited in high-end applications due to stricter quality requirements in premium consumer electronics segments. As the market grows at a robust 14.3% CAGR, competition is intensifying across all product categories.

List of Key Consumer Electronics Board-to-Board Connector Manufacturers

- TE Connectivity (Switzerland)

- Molex (U.S.)

- JAE Electronics (Japan)

- Hirose Electric (HRS) (Japan)

- Panasonic (Japan)

- Amphenol (U.S.)

- Kyocera (Japan)

- Sunway Communication (China)

- Acon (China)

- CSCONN (China)

Segment Analysis:

By Type

PIN 10-20 Segment Holds Significant Market Share Due to Widespread Use in Compact Electronics

The market is segmented based on type into:

- PIN Below 10

- PIN 10-20

- PIN Above 20

By Application

Smart Phone Application Leads the Market Owing to Rising Demand for High-Density Connectivity

The market is segmented based on application into:

- Smart Phone

- Tablet

- Smart Watch

- Others

By Connector Pitch Size

Fine Pitch Connectors Gaining Traction Due to Miniaturization Trends

The market is segmented based on connector pitch size into:

- Standard Pitch (Above 0.5mm)

- Fine Pitch (0.3mm – 0.5mm)

- Ultra Fine Pitch (Below 0.3mm)

By End-Use Industry

Consumer Electronics Dominates the Market

The market is segmented based on end-use industry into:

- Consumer Electronics

- Sub-segments: Smartphones, Wearables, Home Appliances

- Automotive Electronics

- Industrial Electronics

- Medical Electronics

Regional Analysis: Consumer Electronics Board to Board Connector Market

Asia-Pacific

The Asia-Pacific (APAC) region dominates the global board-to-board connector market, accounting for over 45% of the total revenue in 2024. This leadership position stems from China, Japan, and South Korea’s robust electronics manufacturing ecosystems, which collectively produce 70% of the world’s consumer electronics. The region benefits from concentrated R&D investments in miniaturized connector technologies, particularly for smartphones and wearables. However, intensifying competition among local manufacturers like Sunway Communication and YXT has led to price pressures, with average connector costs declining 8-12% annually since 2020. While high-speed 5G device adoption creates new opportunities, overcapacity in basic connector segments remains a challenge.

North America

North America maintains 25% market share primarily through premium connector solutions from Molex and TE Connectivity. The region specializes in high-density (>50 pin) and high-frequency (up to 20GHz) connectors for advanced applications like AR/VR headsets and foldable devices. Recent US legislation, including the CHIPS Act’s $52 billion semiconductor investment, indirectly supports connector innovation through improved PCB integration. Environmental regulations, particularly California’s Proposition 65, drive demand for lead-free and halogen-free connector designs. However, reliance on Asian component suppliers creates vulnerabilities, with 70-80% of base materials still imported from China.

Europe

European manufacturers focus on automotive-grade connectors, leveraging strict EU EMC Directive compliance requirements. Germany’s Bosch and Continental have expanded into consumer electronics connectors for smart home systems, capturing 18% of regional revenue. The market shows particular strength in ruggedized connectors for outdoor wearables and industrial-grade tablets. Brexit has complicated UK-based supply chains, with connector lead times extending 3-5 weeks longer than continental Europe. Sustainability initiatives push development of recyclable thermoplastic connectors, though adoption lags behind North America due to higher costs.

South America

Brazil represents 60% of regional demand, driven by local smartphone assembly plants from Samsung and Motorola. Economic instability has increased preference for refurbished devices, limiting growth in premium connector segments. Mexican maquiladoras serve as a bridge market, processing 35% of connectors ultimately destined for US customers. Local manufacturers struggle against Asian imports, with Chinese connectors priced 20-30% lower than domestic equivalents. Recent USMCA trade provisions have improved component traceability but haven’t significantly altered market dynamics.

Middle East & Africa

The MEA market shows promising 9.1% CAGR through 2032, albeit from a small base. Dubai’s Smart City initiatives drive demand for IoT device connectors, while South Africa serves as an assembly hub for entry-level smartphones. Political instability in key markets like Nigeria disrupts supply chains, with inventory turnover rates 40% slower than global averages. Gulf Cooperation Council countries increasingly serve as testing grounds for extreme-environment connectors, benefiting from year-round high-temperature conditions. Lack of local R&D capabilities forces reliance on European and Asian technical partnerships.

Report Scope

This market research report provides a comprehensive analysis of the Global Consumer Electronics Board to Board Connector Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 875 million in 2024 and is projected to reach USD 2,177 million by 2032, growing at a CAGR of 14.3%.

- Segmentation Analysis: Detailed breakdown by product type (PIN Below 10, PIN 10-20, PIN Above 20), application (Smartphone, Tablet, Smart Watch, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies, including high-frequency stable transmission, electromagnetic compatibility, and miniaturization trends.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges such as technical thresholds and supply chain constraints.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Consumer Electronics Board to Board Connector Market?

->Consumer Electronics Board to Board Connector Market was valued at 875 million in 2024 and is projected to reach US$ 2177 million by 2032, at a CAGR of 14.3% during the forecast period.

Which key companies operate in Global Consumer Electronics Board to Board Connector Market?

-> Key players include Molex, TE Connectivity, Amphenol, JAE, Panasonic, and Hirose Electric (HRS), among others.

What are the key growth drivers?

-> Key growth drivers include increasing complexity of consumer electronics, demand for miniaturization, and rising adoption of high-frequency connectors.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 45% of global revenue in 2024, driven by strong electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include high-density connectors, improved electromagnetic compatibility solutions, and advanced manufacturing techniques for precision components.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...