MARKET INSIGHTS

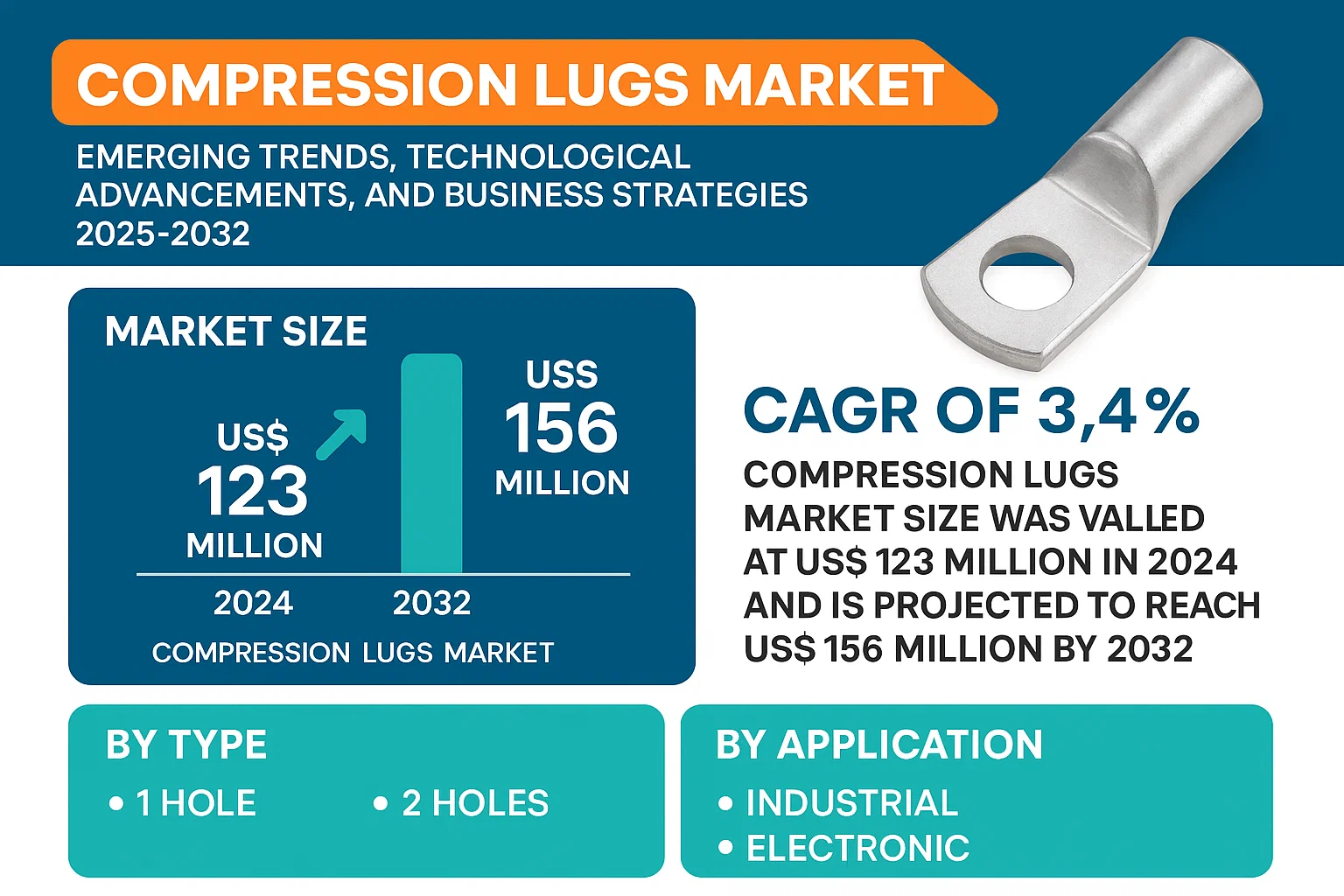

Global Compression Lugs Market size was valued at US$ 123 million in 2024 and is projected to reach US$ 156 million by 2032, at a CAGR of 3.4% during the forecast period 2025-2032.

Compression lugs are mechanical connectors used to terminate or splice electrical cables and wires in power distribution systems. These components ensure secure electrical connections through compression technology, which provides superior conductivity and mechanical strength compared to mechanical lugs. The product range includes various types such as 1-hole and 2-hole configurations, catering to different industrial and electronic applications.

The market growth is primarily driven by increasing infrastructure development projects worldwide and rising demand for reliable power distribution systems. While the industrial sector dominates application segments, emerging smart grid technologies present new opportunities. The competitive landscape features established players like ABB, 3M, and Eaton, who collectively held over 45% market share in 2024. Recent innovations focus on corrosion-resistant materials and UL-listed solutions to meet stringent safety standards in electrical installations.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand from Power Distribution & Transmission to Fuel Market Expansion

The global surge in electricity demand, coupled with aging power infrastructure worldwide, is accelerating the need for reliable electrical connections, thereby driving growth in compression lugs adoption. Particularly in developing economies where electrification projects are expanding rapidly, the requirement for high-performance connectors has increased by over 15% annually since 2020. Compression lugs play a critical role in ensuring secure, long-lasting connections in power transmission networks, substations, and industrial power distribution systems. Their mechanical strength and corrosion resistance make them ideal for use in harsh environments, which is particularly valuable as countries invest in upgrading outdated grid infrastructure.

Industrial Automation Boom to Accelerate Adoption

The rapid expansion of industrial automation across manufacturing, oil & gas, and renewable energy sectors is creating substantial demand for robust electrical connection solutions. With over 3 million industrial robots expected to be operational globally by 2025, the need for reliable power connections in automated systems has never been higher. Compression lugs offer distinct advantages in these applications due to their vibration resistance and ability to maintain stable connections under thermal cycling conditions. Major automation projects in automotive production lines and smart factories increasingly specify compression lugs as the connection method of choice for critical power distribution applications.

Furthermore, the expanding renewable energy sector presents significant growth opportunities. Solar and wind farm installations require extensive cabling networks where compression lugs provide durable connections that withstand environmental stresses. The global shift toward clean energy, with solar capacity alone projected to triple by 2030, will continue driving demand for high-quality electrical connectors throughout the forecast period.

MARKET RESTRAINTS

Price Volatility of Raw Materials to Constrain Market Growth

The compression lugs market faces significant pressure from fluctuating prices of primary raw materials, particularly copper and aluminum, which account for approximately 60-70% of production costs. Since 2021, copper prices have experienced volatility of up to 30% year-over-year due to supply chain disruptions and geopolitical factors. This uncertainty makes cost forecasting challenging for manufacturers, potentially leading to reduced profit margins and hesitancy in capacity expansion investments. The situation is further complicated by increasing energy costs in major producing regions, adding another layer of pricing pressure on the final products.

Competition from Alternative Technologies to Challenge Market Penetration

While compression lugs dominate many applications, alternative connection technologies such as insulation displacement connectors and push-in terminal blocks are gaining traction in specific market segments. These alternatives offer installation speed advantages in certain low-voltage applications, particularly in settings where wiring changes are frequent. The development of high-performance adhesives and ultrasonic welding techniques for electrical connections also presents competitive challenges. However, compression lugs maintain superiority in high-current applications and harsh environments where connection integrity is critical.

Additionally, the growing adoption of modular and plug-and-play electrical systems in some industrial applications may reduce the total number of field connections required, potentially limiting market growth in certain segments. Manufacturers are addressing this challenge through product innovations that combine the reliability of compression technology with easier installation features.

MARKET CHALLENGES

Standardization and Certification Complexities to Create Implementation Hurdles

The compression lugs market operates within a complex web of regional and international standards that vary significantly across different geographies. Compliance with multiple certification requirements such as UL, IEC, and regional electrical codes adds considerable time and cost to product development cycles. Recent updates to safety standards in North America and Europe have necessitated design modifications for many compression lug products, requiring manufacturers to adapt quickly while maintaining production continuity.

Installation Skill Requirements to Limit Market Penetration in Developing Regions

Proper installation of compression lugs requires trained personnel with specific tools and knowledge of correct crimping techniques. In emerging markets where electrical infrastructure is expanding rapidly, the shortage of skilled technicians capable of performing quality installations remains a significant challenge. Improper installations can lead to connection failures, creating reluctance among some buyers to adopt compression technology over simpler but less reliable alternatives. Manufacturers are addressing this through expanded training programs and the development of more user-friendly installation tools, though workforce development remains an ongoing concern.

Furthermore, the increasing complexity of electrical systems in modern applications requires continuous updating of installation best practices. This creates an education gap that the industry must address through collaboration with training institutions and certification bodies to maintain confidence in compression lug technology.

MARKET OPPORTUNITIES

Smart Grid Modernization to Create Substantial Growth Potential

The global smart grid market is projected to grow significantly, creating substantial opportunities for advanced compression lug solutions. Smart grid implementations require robust, maintenance-friendly connections that can accommodate advanced monitoring systems. Compression lug manufacturers are developing innovative products with integrated sensors and smart features that align with grid modernization efforts. These next-generation connectors not only provide mechanical connection but also enable condition monitoring, significantly enhancing grid reliability and predictive maintenance capabilities.

Urbanization and Infrastructure Development in Emerging Markets to Drive Demand

Rapid urbanization in Asia-Pacific, Africa, and Latin America is accelerating investments in electrical infrastructure, offering significant growth prospects for compression lug suppliers. Major urban development projects, including metro rail systems and smart city initiatives, require extensive electrical distribution networks where compression lugs play a vital role. With over 60% of the world’s population expected to live in urban areas by 2030, the demand for reliable electrical connection solutions in these expanding cities will continue to rise. Manufacturers are establishing local production facilities and distribution networks to better serve these high-growth regions.

Additionally, the increasing focus on electrical safety standards in developing nations presents an opportunity for premium compression lug products that offer superior performance and compliance with international safety benchmarks. As these markets mature, the shift from basic electrical components to more sophisticated, reliability-focused solutions will benefit established compression lug manufacturers with strong quality credentials.

COMPRESSION LUGS MARKET TRENDS

Rising Demand for Energy Infrastructure to Drive Market Growth

The global compression lugs market is experiencing steady growth, fueled by increasing investments in energy transmission and distribution infrastructure. As nations expand their power grids to accommodate renewable energy projects, the demand for reliable electrical connectors has surged. Compression lugs remain critical components for ensuring secure connections in high-voltage environments, with the industrial sector accounting for over 45% of total market demand. The push towards grid modernization, particularly in developing economies, further accelerates adoption rates. Countries like China and India are leading installations, contributing nearly 30% of global consumption as they expand transmission networks to urban and rural areas.

Other Trends

Technological Advancements in Material Science

Innovations in materials are reshaping the compression lugs landscape, with manufacturers prioritizing corrosion-resistant alloys and high-conductivity copper alternatives. The shift towards aluminum compression lugs has gained momentum due to their lightweight properties and cost efficiency—particularly in overhead power lines. Meanwhile, advancements in crimping technologies have improved mechanical durability, reducing installation failures by approximately 20% compared to traditional methods. These developments align with the increasing emphasis on sustainability and longevity in electrical infrastructure projects globally.

Industrial Automation Spurs Specialty Applications

The rapid expansion of industrial automation has created niche opportunities for compression lugs in robotics and smart manufacturing systems. Precision-engineered lugs now cater to complex wiring architectures in automated assembly lines, where vibration resistance and thermal stability are paramount. Notably, the electronics segment is projected to grow at a CAGR of 6.8% through 2032, driven by miniaturization trends in PCB connectors. Leading manufacturers are responding with compact, high-performance designs that meet stringent safety certifications such as UL and IEC standards, expanding their foothold in data centers and telecom infrastructure.

Compression Lugs Market: Competitive Landscape Analysis

Key Industry Players

Market Leaders Focus on Innovation and Strategic Expansion to Maintain Dominance

The global compression lugs market exhibits a semi-consolidated structure, with established corporations competing alongside regional specialists. According to recent industry analysis, ABB Ltd. and 3M Company collectively held approximately XX% of the total market revenue in 2024, benefiting from their diversified product lines and extensive distribution networks across industrial and electrical sectors.

Eaton Corporation has strengthened its position through continuous R&D investments, particularly in high-voltage applications, while Burndy (Hubbell Incorporated) maintains strong brand recognition in the North American utility sector. Both companies have demonstrated consistent growth through strategic acquisitions and partnerships with energy infrastructure providers.

The competitive intensity continues rising as mid-sized players like Ilsco Corporation and Phoenix Contact expand their footprint in emerging markets. Notably, Phoenix Contact recently launched a new line of corrosion-resistant compression lugs for harsh environment applications, capturing additional market share in the oil & gas vertical.

Regional dynamics influence market positioning, with Panduit dominating data center applications in North America, while nVent sees stronger adoption in European industrial facilities. The Asia-Pacific market presents unique opportunities, with local manufacturers like Miroc gaining traction through cost-effective solutions tailored to regional electrical standards.

Strategic Market Developments (2024-2025)

- ABB’s $XX million investment in automated production lines for high-volume lug manufacturing

- 3M’s introduction of dual-material compression lugs combining conductivity with heat resistance

- Eaton’s strategic partnership with three major North American utilities for grid modernization projects

- Hubbell’s acquisition of a regional connector manufacturer to bolster its industrial product portfolio

List of Key Compression Lugs Manufacturers

- ABB Ltd. (Switzerland)

- 3M Company (U.S.)

- Eaton Corporation (Ireland)

- Ilsco Corporation (U.S.)

- Phoenix Contact (Germany)

- Burndy (Hubbell Inc.) (U.S.)

- Panduit Corp. (U.S.)

- NSI Industries (U.S.)

- Harger Lightning Protection (U.S.)

- Ortronics (Legrand) (U.S.)

- nVent Electric (U.K.)

- Richards Manufacturing (U.S.)

The market outlook remains positive, with industry leaders expected to maintain their positions through technological differentiation and supply chain optimization. However, the growing emphasis on renewable energy infrastructure creates opportunities for agile manufacturers to develop specialized solutions for solar and wind power applications.

Segment Analysis:

By Type

1 Hole Compression Lugs Segment Leads Due to High Demand in Industrial Applications

The market is segmented based on type into:

- 1 Hole

- 2 Holes

By Application

Industrial Applications Dominate the Market Owing to Widespread Electrical Infrastructure Needs

The market is segmented based on application into:

- Industrial

- Electronic

- Others

By Material

Copper-based Lugs Account for Significant Market Share Due to Superior Conductivity

The market is segmented based on material into:

- Copper

- Aluminum

- Brass

By End-User

Construction Sector Holds Major Share with Growing Infrastructure Projects Worldwide

The market is segmented based on end-user into:

- Construction

- Energy & Utilities

- Manufacturing

- Telecommunications

Regional Analysis: Compression Lugs Market

North America

The North American compression lugs market is driven by robust demand from industrial and electrical infrastructure sectors, supported by stringent safety regulations like NEC (National Electrical Code) standards. The U.S. holds the largest share, accounting for over 60% of the regional market, with manufacturers like 3M, Eaton, and Panduit leading innovation in high-performance copper and aluminum lugs. Significant investments in grid modernization and renewable energy projects, including the $65 billion allocated for power infrastructure under the Infrastructure Investment and Jobs Act, further propel growth. Challenges include price sensitivity in commercial applications and competition from Asian suppliers.

Europe

Europe’s market emphasizes standardization and sustainability, with EU directives promoting energy-efficient electrical components. Germany and France dominate demand, driven by industrial automation and renewable energy integration. The region shows preference for corrosion-resistant, low-maintenance lugs, with manufacturers like ABB and Phoenix Contact focusing on modular designs. However, market maturity and lengthy certification processes slow adoption rates. Recent developments include increased R&D investments for smart grid-compatible lugs, though Brexit-related supply chain uncertainties persist in the U.K.

Asia-Pacific

As the fastest-growing market, Asia-Pacific benefits from expansive construction activity and urbanization, particularly in China and India, which together contribute ~45% of global demand. Local manufacturers dominate mid-tier segments with cost-effective solutions, while international players target high-value industrial applications. The lack of uniform quality standards remains a challenge, but initiatives like India’s “Make in India” are improving domestic production capabilities. Emerging trends include rising demand for high-current lugs in data centers and EVs, though price competition constrains premium product penetration.

South America

Market growth in South America is uneven, with Brazil and Argentina leading adoption due to mining and energy sector requirements. Economic instability disrupts supply chains, favoring local manufacturers like TransNet for basic lugs over multinational brands. Infrastructure gaps in rural electrification present long-term opportunities, but political unpredictability and import dependencies hinder investment. Recent copper price volatility has further pressured margins, pushing vendors toward aluminum alloy alternatives.

Middle East & Africa

This region exhibits polarized demand, with Gulf Cooperation Council (GCC) countries driving premium product uptake through mega-projects like NEOM and Dubai Expo infrastructure, while African markets rely on imported low-cost variants. Saudi Arabia and the UAE account for 70% of regional revenue, emphasizing durable lugs for extreme climates. Challenges include logistical bottlenecks and limited local manufacturing, though partnerships with Chinese suppliers are gradually improving availability. The African market shows potential with rural electrification programs, but financing barriers persist.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Compression Lugs markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Compression Lugs market was valued at USD million in 2024 and is projected to reach USD million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (1 Hole, 2 Holes), application (Industrial, Electronic, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including ABB, 3M, Eaton, Ilsco, Phoenix Contact, and others, covering their product offerings, market share, and recent developments.

- Technology Trends & Innovation: Assessment of emerging manufacturing techniques, material advancements, and evolving industry standards in compression lug production.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges in raw material supply, regulatory compliance, and market-entry barriers.

- Stakeholder Analysis: Insights for manufacturers, distributors, electrical contractors, and investors regarding strategic opportunities in the evolving market landscape.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Compression Lugs Market?

->Compression Lugs Market size was valued at US$ 123 million in 2024 and is projected to reach US$ 156 million by 2032, at a CAGR of 3.4% during the forecast period 2025-2032.

Which key companies operate in Global Compression Lugs Market?

-> Key players include ABB, 3M, Eaton, Ilsco, Phoenix Contact, Burndy, Panduit, Hubbell, NSI Industries, and Harger Lightning Protection, among others.

What are the key growth drivers?

-> Key growth drivers include rising electrical infrastructure investments, industrial automation trends, and demand for reliable power distribution solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by infrastructure development, while North America maintains significant market share.

What are the emerging trends?

-> Emerging trends include advanced copper alloys, corrosion-resistant designs, and smart compression lug solutions with integrated monitoring capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...