Market Insights

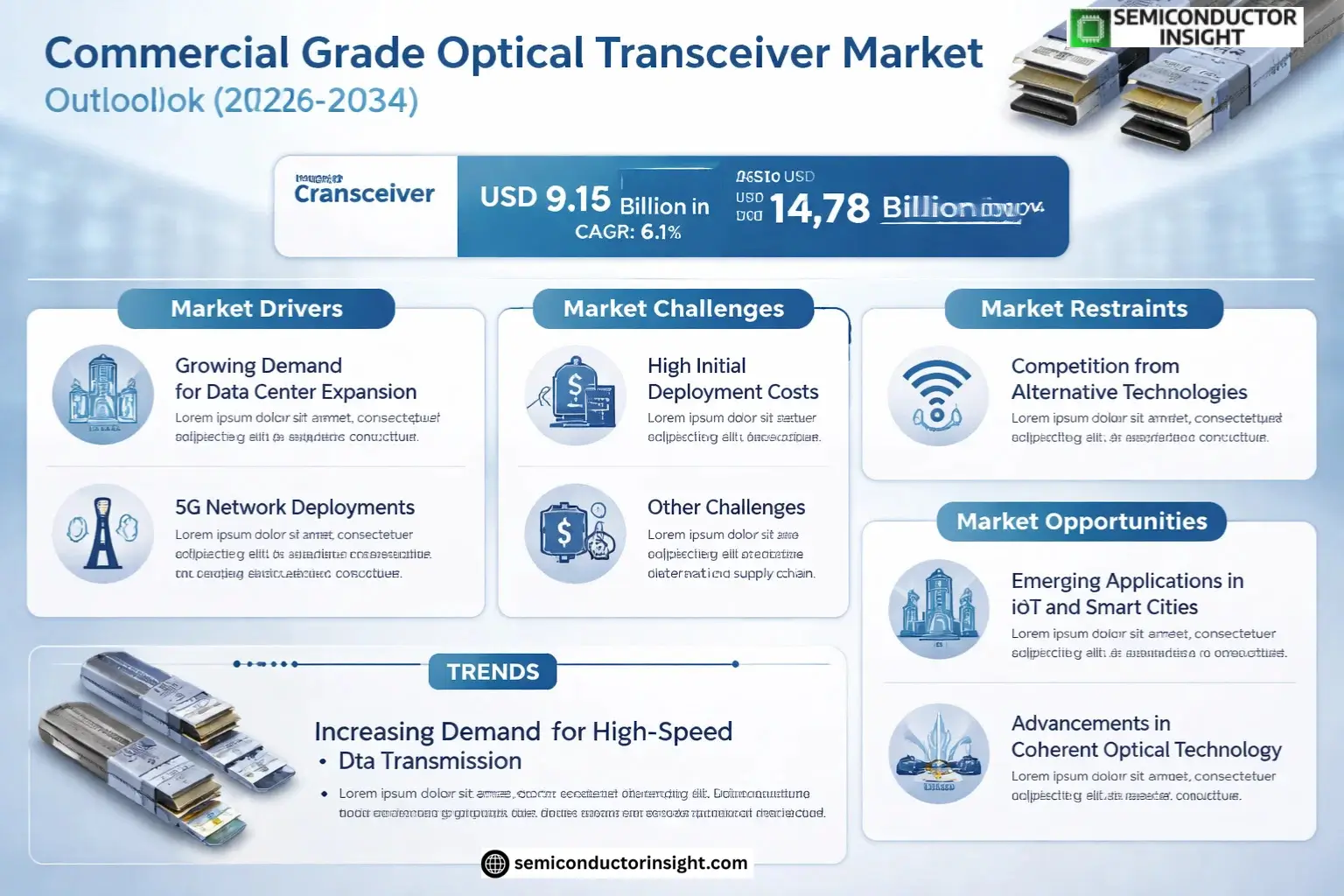

Global Commercial Grade Optical Transceiver Market size was valued at USD 8.42 billion in 2025. The market is projected to grow from USD 9.15 billion in 2026 to USD 14.78 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

Commercial grade optical transceivers are critical components in high-speed data communication networks, converting electrical signals into optical signals and vice versa. These devices support various form factors such as QSFP, OSFP, and others, catering to applications like enterprise networks, data centers, and machine learning infrastructure.

The market growth is driven by increasing demand for high-bandwidth connectivity, expansion of cloud computing services, and rapid deployment of 5G networks globally. Key players such as Cisco, Juniper Networks, and Broadcom dominate the market with advanced product portfolios. For instance, in early 2024, Broadcom introduced its latest 800G optical transceiver series to meet escalating data center demands.

MARKET DRIVERS

Growing Demand for Data Center Expansion

Commercial Grade Optical Transceiver Market is experiencing significant growth due to increasing demand from data centers. With enterprises adopting cloud computing and virtualization technologies, the need for high-speed data transmission through optical transceivers has surged by approximately 22% annually.

5G Network Deployments

The rollout of 5G networks worldwide is accelerating demand for commercial grade optical transceivers. These components are critical for backhaul and fronthaul applications, with the telecom sector accounting for nearly 35% of total market demand.

Fiber optic infrastructure upgrades across commercial enterprises continue to drive adoption of advanced optical transceiver solutions.

MARKET CHALLENGES

High Initial Deployment Costs

While commercial grade optical transceivers offer superior performance, their deployment requires significant upfront investment in compatible networking equipment. Many small and medium enterprises face budgetary constraints when upgrading to optical solutions.

Other Challenges

Technological Complexity

Integration of optical transceivers with existing network infrastructure often requires specialized expertise, creating barriers for some organizations.

Supply Chain Disruptions

Recent semiconductor shortages have affected production and delivery timelines for commercial grade optical transceiver components.

MARKET RESTRAINTS

Competition from Alternative Technologies

While commercial grade optical transceivers dominate high-speed applications, emerging wireless technologies pose potential competition. Some enterprises are adopting millimeter-wave solutions for short-range applications, impacting optical transceiver adoption in certain segments.

MARKET OPPORTUNITIES

Emerging Applications in IoT and Smart Cities

Commercial Grade Optical Transceiver Market stands to benefit from growing IoT deployments and smart city initiatives. These applications require reliable, high-bandwidth connectivity, with optical solutions being preferred for backbone infrastructure. The industrial sector is expected to account for 25% of market growth by 2025.

Advancements in Coherent Optical Technology

Recent breakthroughs in coherent optical transceiver technology are creating new opportunities in long-haul communications. These high-performance solutions offer improved signal integrity and greater transmission distances, opening new commercial applications.

Commercial Grade Optical Transceiver Market Trends

Increasing Demand for High-Speed Data Transmission

Commercial Grade Optical Transceiver Market is experiencing significant growth due to escalating demand for high-bandwidth applications. Data centers and enterprise networks are rapidly adopting QSFP and OSFP form factors to support 400G and beyond Ethernet standards. Network infrastructure upgrades across North America and Asia-Pacific regions are driving this trend, with major cloud service providers leading the transition to higher-speed optical connectivity solutions.

Other Trends

Adoption in Emerging Technologies

Commercial Grade Optical Transceivers are becoming integral to AI/ML infrastructure and 5G backhaul networks. The machine learning segment shows particularly strong growth potential as hyperscalers optimize data center interconnects for distributed computing workloads. Manufacturers are developing low-latency variants to meet the stringent requirements of real-time analytics applications.

Supply Chain Diversification Strategies

Leading vendors like Cisco and Broadcom are restructuring their manufacturing footprints to mitigate geopolitical risks. The market has seen increased investment in alternative production facilities across Southeast Asia and North America, with particular focus on securing supplies of critical optical components. This transition is expected to continue as companies implement dual-sourcing strategies for Commercial Grade Optical Transceivers.

Energy Efficiency Innovations

New product developments emphasize power reduction in Commercial Grade Optical Transceivers, with industry leaders targeting 30% lower power consumption for next-generation modules. Regenerative designs and advanced thermal management solutions are emerging as key competitive differentiators, particularly for data center applications where operating costs are a major consideration.

Regional Market Developments

China’s domestic Commercial Grade Optical Transceiver manufacturers continue to gain market share through aggressive pricing and government-supported R&D initiatives. Meanwhile, U.S. and European vendors are focusing on high-performance niches, particularly for defense and telecom applications requiring hardened components with extended temperature ranges.

COMPETITIVE LANDSCAPE

Key Industry Players

Dominance of Networking Giants in Optical Transceiver Market

Cisco Systems and Juniper Networks collectively command over 35% of the Commercial Grade Optical Transceiver Market, leveraging their vertically integrated supply chains and dominance in enterprise networking equipment. The market exhibits an oligopolistic structure where the top five players Cisco, Juniper, Intel, Broadcom, and II-VI Incorporated control approximately 58% of global revenue, as of 2025 market data. These leaders are aggressively expanding their QSFP and OSFP product portfolios to capitalize on data center upgrades and 5G backhaul deployments.

Niche players like Eoptolink and Accelink Technologies are gaining traction through specialized 400G/800G transceivers for hyperscale data centers, while Chinese manufacturers Huagong Tech and Qsfptek are expanding their global footprint with cost-competitive solutions. The competitive intensity is increasing as traditional component suppliers like Molex and Amphenol innovate in copper-interconnect alternatives, challenging the dominance of pure-play optical transceiver vendors.

List of Key Commercial Grade Optical Transceiver Companies Profiled

- Cisco Systems

- Juniper Networks

- Intel Corporation

- NEC Corporation

- NVIDIA

- Molex

- II-VI Incorporated

- E.C.I. Networks

- Broadcom

- Amphenol Corporation

- Huagong Tech

- Eoptolink Technology

- Accelink Technologies

- Qsfptek

- Infinera Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

QSFP maintains technology leadership with:

|

| By Application |

|

Data Center applications show strongest momentum:

|

| By End User |

|

Cloud Service Providers demonstrate strongest adoption patterns:

|

| By Data Rate |

|

400G+ emerges as the technology frontier:

|

| By Form Factor |

|

QSFP/QSFP+ maintains industry preference:

|

Regional Analysis: Asia-Pacific Commercial Grade Optical Transceiver Market

China

China has developed a comprehensive optical transceiver manufacturing ecosystem with clusters in Shenzhen and Wuhan. Local firms have achieved significant technological advancements in commercial-grade components.

The “Digital China” strategy and Made in China 2025 policy prioritize domestic optical communication equipment production, providing subsidies and tax incentives for commercial-grade transceiver development.

China’s rapid 5G rollout creates substantial demand for commercial-grade optical transceivers in fronthaul and backhaul networks, with base station installations exceeding other Asia-Pacific countries combined.

Chinese telecom operators are implementing AI-driven network optimization tools that require high-performance optical transceivers to handle increased data processing demands in commercial applications.

Japan & South Korea

Japan and South Korea maintain sophisticated commercial optical transceiver markets focused on quality and reliability. Japanese manufacturers lead in high-end commercial-grade components for enterprise networks, while Korean firms excel in compact transceiver designs for data center applications. Both countries invest heavily in AI-enabled network infrastructure that drives demand for next-generation optical communication solutions. Commercial Grade Optical Transceiver Market benefits from strong R&D capabilities and collaborations between telecom operators and equipment manufacturers.

India

India represents the fastest-growing Commercial Grade Optical Transceiver Market in Asia-Pacific, driven by digital transformation across industries and expanding data center capabilities. The government’s Smart Cities Mission necessitates advanced optical communication infrastructure. Indian telecom operators are upgrading networks to support increasing data traffic, creating opportunities for commercial-grade transceiver suppliers. Local manufacturing initiatives aim to reduce import dependence for optical communication components.

Southeast Asia

The Southeast Asian Commercial Grade Optical Transceiver Market shows strong growth potential with increasing submarine cable deployments and hyperscale data center construction. Thailand, Singapore, and Malaysia lead regional adoption as digital economies expand. Commercial applications in banking, e-commerce, and Industry 4.0 drive demand for reliable optical communication solutions. Regional governments support infrastructure projects that require high-performance optical transceivers for commercial network implementations.

Australia & New Zealand

Australia and New Zealand maintain mature Commercial Grade Optical Transceiver Markets with emphasis on network reliability and security. The countries’ remote locations necessitate robust optical communication infrastructure for commercial connectivity. Growing investments in smart grid technologies and renewable energy projects create specialized demands for industrial-grade optical transceiver solutions. Data center expansions in Sydney and Auckland fuel commercial-grade component procurement.

Report Scope

This market research report provides a comprehensive analysis of the Commercial Grade Optical Transceiver Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of optical transceivers in powering advancements across industries such as enterprise networks, data centers, machine learning, and telecommunications.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (QSFP, OSFP, Others), application (Enterprise Networks, Data Center, Machine Learning), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, optical transceiver design trends, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Commercial Grade Optical Transceiver Market?

-> Commercial Grade Optical Transceiver Market size was valued at USD 8.42 billion in 2025. The market is projected to grow from USD 9.15 billion in 2026 to USD 14.78 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

What is the expected CAGR of the Commercial Grade Optical Transceiver Market?

-> The market is expected to grow at a CAGR of % during the forecast period 2025-2034.

Which key companies operate in Commercial Grade Optical Transceiver Market?

-> Key players include Cisco, Juniper, Intel, NEC, NVIDIA, Molex, II-VI Incorporated, E.C.I. Networks, Broadcom, Amphenol, Huagong Tech, Eoptolink, Accelink Technologies, and Qsfptek.

Which product segment leads the market?

-> The QSFP segment is projected to reach USD million by 2034, representing significant market growth.

Which region dominates the market?

-> The U.S. market is estimated at USD million in 2025, while China is expected to reach USD million during the forecast period.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...