Market Insights

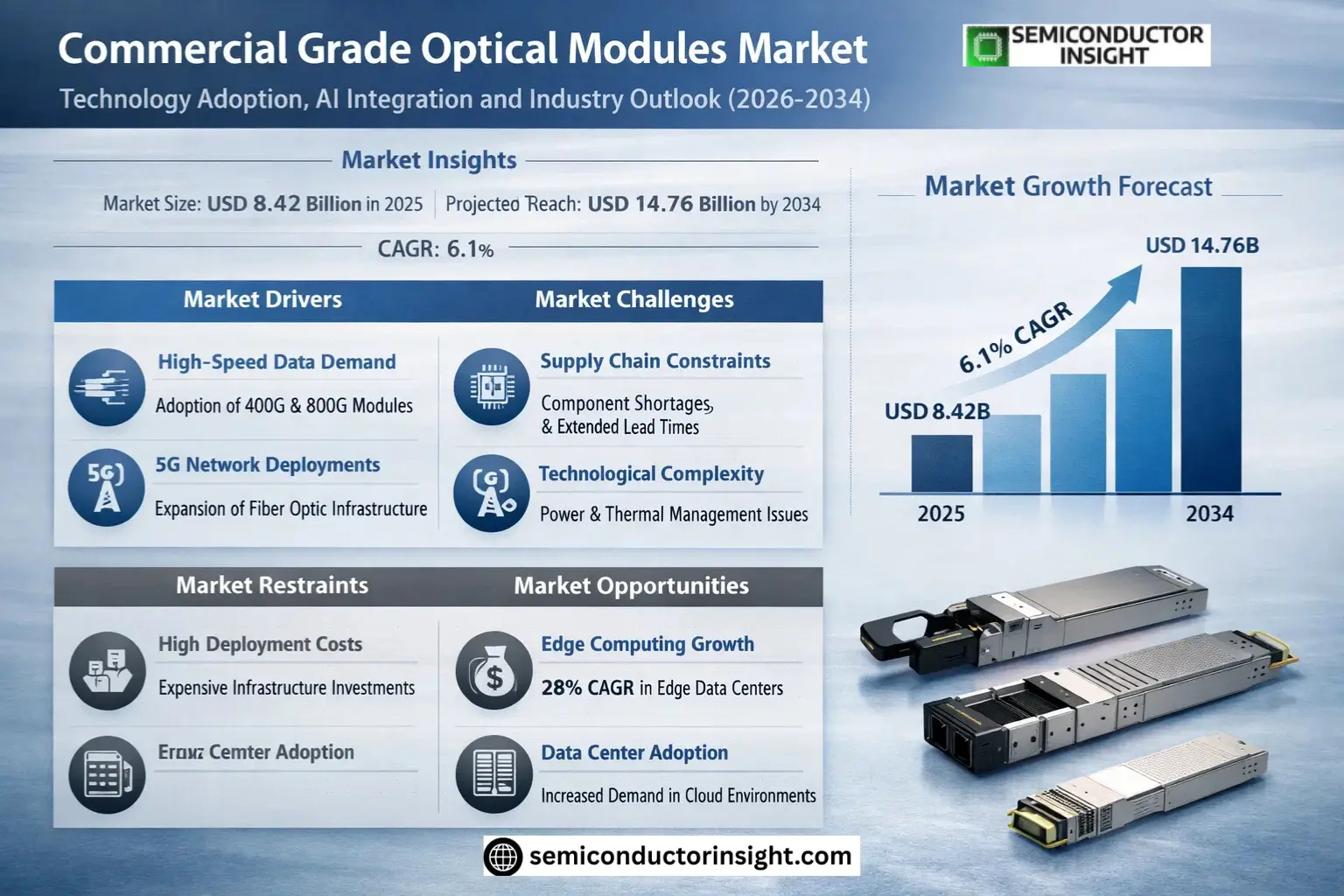

Global Commercial Grade Optical Modules Market size was valued at USD 8.42 billion in 2025. The market is projected to grow from USD 9.15 billion in 2026 to USD 14.76 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

Commercial Grade Optical Modules Market are designed for stable, controlled environments with temperature ranges between 0°C and 70°C, making them cost-effective solutions for applications not requiring extreme conditions. These modules facilitate high-speed data transmission in enterprise networks, data centers, and machine learning infrastructure, supporting technologies such as QSFP and OSFP form factors.

The market growth is driven by increasing demand for high-bandwidth connectivity, expansion of cloud computing services, and advancements in AI-driven networking solutions. Key players like Cisco, Juniper Networks, and Broadcom dominate the sector with innovative product portfolios and strategic collaborations aimed at enhancing data center efficiency.

MARKET DRIVERS

Increasing Demand for High-Speed Data Transmission

Commercial Grade Optical Modules Market is witnessing significant growth due to the rising need for high-bandwidth applications in data centers, telecom networks, and enterprise solutions. With data traffic expected to grow by 30% annually, optical modules are becoming essential for reliable, low-latency communication. The adoption of 400G and 800G modules is accelerating as cloud providers expand their infrastructure.

5G Network Deployments

Global 5G rollouts are driving demand for commercial grade optical modules to support fronthaul and backhaul networks. Telecom operators are investing heavily in fiber optic infrastructure, with optical module shipments projected to increase by 22% year-over-year through 2025. The shift towards Open RAN architectures further amplifies this demand.

Network modernization initiatives and the phasing out of copper-based systems are creating sustained growth opportunities for commercial grade optical modules across all regions.

MARKET CHALLENGES

Supply Chain Constraints

Commercial Grade Optical Modules Market faces persistent component shortages, particularly for critical semiconductors and photonic chips. Lead times have extended to 30+ weeks for certain high-speed modules, affecting deployment schedules. Manufacturers are reevaluating their supplier networks to mitigate these disruptions.

Other Challenges

Technological Complexity

Developing next-gen optical modules that meet commercial reliability standards while reducing power consumption remains a significant engineering challenge, with thermal management being a key constraint for 800G+ modules.

MARKET RESTRAINTS

High Initial Deployment Costs

The capital expenditure required for commercial grade optical network upgrades presents a barrier for small-to-medium enterprises. While total cost of ownership favors optical solutions, the upfront investment in compatible infrastructure deters some potential adopters, particularly in emerging markets.

MARKET OPPORTUNITIES

Edge Computing Expansion

The proliferation of edge data centers creates new demand for ruggedized commercial grade optical modules capable of operating in varied environmental conditions. Market analysts project the edge optical module segment to grow at 28% CAGR through 2027, with significant opportunities for vendors offering industrial temperature-range products.

Commercial Grade Optical Modules Market Trends

Growing Adoption in Data Center Applications

Commercial Grade Optical Modules Market is witnessing increased demand from data center applications due to rising cloud computing needs. These modules provide optimal performance in controlled environments between 0°C to 70°C, making them cost-effective solutions for enterprise data centers. Major cloud service providers are deploying commercial-grade modules for server-to-server and switch-to-switch connections.

Other Trends

QSFP Form Factor Dominance

QSFP modules continue to lead Commercial Grade Optical Modules Market, accounting for over 40% of shipments. Their compact size and high-density connectivity make them ideal for modern data center architectures. Manufacturers are developing QSFP-DD variants to support 400G Ethernet requirements while maintaining backward compatibility.

Asia-Pacific Market Expansion

China and Japan are becoming key growth markets for Commercial Grade Optical Modules, driven by rapid data center construction and 5G network deployments. Local manufacturers are gaining market share through competitive pricing and government support, though global brands like Cisco and Broadcom maintain strong positions in enterprise networks.

Supply Chain Diversification

Manufacturers are expanding production facilities across multiple regions to mitigate geopolitical risks. This trend is particularly evident among US-based Commercial Grade Optical Module suppliers establishing manufacturing partnerships in Southeast Asia and India.

Energy Efficiency Focus

The industry is prioritizing power-efficient designs as data centers implement sustainability initiatives. New Commercial Grade Optical Modules consume 15-20% less power than previous generations while maintaining thermal performance within the specified operating range.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance Shifts in Commercial Optical Module Sector

Commercial Grade Optical Modules Market is led by established networking giants Cisco and Juniper Networks, which together command over 30% market share through their comprehensive product portfolios and strong R&D capabilities. Intel and Broadcom follow closely, leveraging their semiconductor expertise to deliver high-performance optical solutions for data center and enterprise applications. The top five players collectively account for approximately 58% of global revenue, demonstrating moderate concentration in this USD X billion industry.

Emerging challengers like Eoptolink and Qsfptek are gaining traction through competitive pricing strategies in the Asia-Pacific region, while specialist manufacturers such as II-VI Incorporated and Molex focus on niche applications in machine learning environments. Chinese manufacturers including Huagong Tech and Accelink Technologies are rapidly expanding their global footprint through aggressive pricing and government-backed initiatives, particularly in the QSFP segment which shows the highest growth potential.

List of Key Commercial Grade Optical Modules Companies Profiled

- Cisco Systems

- Juniper Networks

- Intel Corporation

- NEC Corporation

- NVIDIA

- Molex LLC

- II-VI Incorporated

- E.C.I. Networks

- Broadcom Inc.

- Amphenol Corporation

- Huagong Tech

- Eoptolink Technology

- Accelink Technologies

- Qsfptek

- Finisar Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

QSFP Modules dominate due to:

|

| By Application |

|

Data Center Applications show strongest demand because:

|

| By End User |

|

Cloud Service Providers lead as end users due to:

|

| By Form Factor |

|

Hot-pluggable Modules see highest preference because:

|

| By Transmission Distance |

|

Short Reach Modules are most prevalent as:

|

Regional Analysis: Asia-Pacific Commercial Grade Optical Modules Market

Asia-Pacific: The Innovation Powerhouse

China’s Pearl River Delta hosts the world’s most concentrated optical module manufacturing base, with vertically integrated supply chains reducing production lead times by 30-40%. Japanese facilities specialize in ultra-low-loss optical components for premium modules.

National broadband initiatives across APAC governments actively subsidize optical network deployments. India’s PM-WANI program and China’s “East Data West Computing” project create sustained demand for commercial grade optical connectivity solutions.

Regional R&D centers lead in developing climate-resilient optical modules, crucial for tropical deployments. Modular designs from Singaporean engineers enable easier field maintenance in remote areas across archipelagic nations.

Price sensitivity drives localization strategies, with Indian and Vietnamese manufacturers gaining share in budget-conscious segments. Australia and New Zealand serve as premium technology testbeds for next-gen coherent optical modules.

North America

The North American Commercial Grade Optical Modules Market thrives on hyperscale datacenter demand and private 5G network deployments. U.S.-based cloud providers drive adoption of 400G ZR optics for DCI applications, while Canadian mining and energy sectors require ruggedized optical solutions. Silicon Valley remains the center for cutting-edge silicon photonics development, with several startups commercializing co-packaged optics solutions. The region’s focus on network security boosts demand for optical encryption modules in government and financial sectors.

Europe

Europe’s commercial optical modules market emphasizes energy efficiency and sustainability, with German manufacturers leading in low-power designs. The EU’s tough regulatory environment accelerates adoption of RoHS-compliant optical components. Key growth comes from smart city deployments across Scandinavia and industrial IoT networks in Germany’s manufacturing heartland. French and Italian telecom operators are early adopters of flex-grid optical modules for enhanced network flexibility.

Middle East & Africa

Gulf Cooperation Council nations drive optical module demand through massive smart city projects and subsea cable landing stations. UAE’s hyperscale datacenter boom creates opportunities for high-speed optical interconnects. African markets show growing appetite for affordable, solar-powered optical solutions for rural connectivity projects. South Africa serves as the regional hub for optical network equipment distribution and technical support.

South America

Brazil anchors South America’s commercial optical modules market with expanding fiber-to-the-home deployments. Chilean mining operations deploy rugged optical modules for harsh environment communications. The region shows strong preference for modular, upgradeable optical solutions that accommodate gradual infrastructure investments. Argentina’s research institutions collaborate with global vendors to adapt optical technologies for local network conditions.

Report Scope

This market research report provides a comprehensive analysis of the Commercial Grade Optical Modules Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of optical modules in powering advancements across industries such as enterprise networks, data centers, and machine learning.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (QSFP, OSFP, Others), application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, Latin America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies and evolving industry standards in commercial grade optical modules.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, and regulatory issues.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Commercial Grade Optical Modules Market?

-> Commercial Grade Optical Modules Market size was valued at USD 8.42 billion in 2025. The market is projected to grow from USD 9.15 billion in 2026 to USD 14.76 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

Which key companies operate in Commercial Grade Optical Modules Market?

-> Key players include Cisco, Juniper, Intel, NEC, NVIDIA, Molex, II-VI Incorporated, E.C.I. Networks, Broadcom, Amphenol, Huagong Tech, Eoptolink, Accelink Technologies, and Qsfptek.

What are the key growth drivers?

-> Key growth drivers include increasing demand for data center infrastructure, enterprise network expansions, and advancements in machine learning applications.

Which region dominates the market?

-> Asia is projected to be the fastest-growing market, with China reaching USD million by 2034, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include increasing adoption of QSFP modules, development of high-speed optical solutions, and expansion of 5G infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...