MARKET INSIGHTS

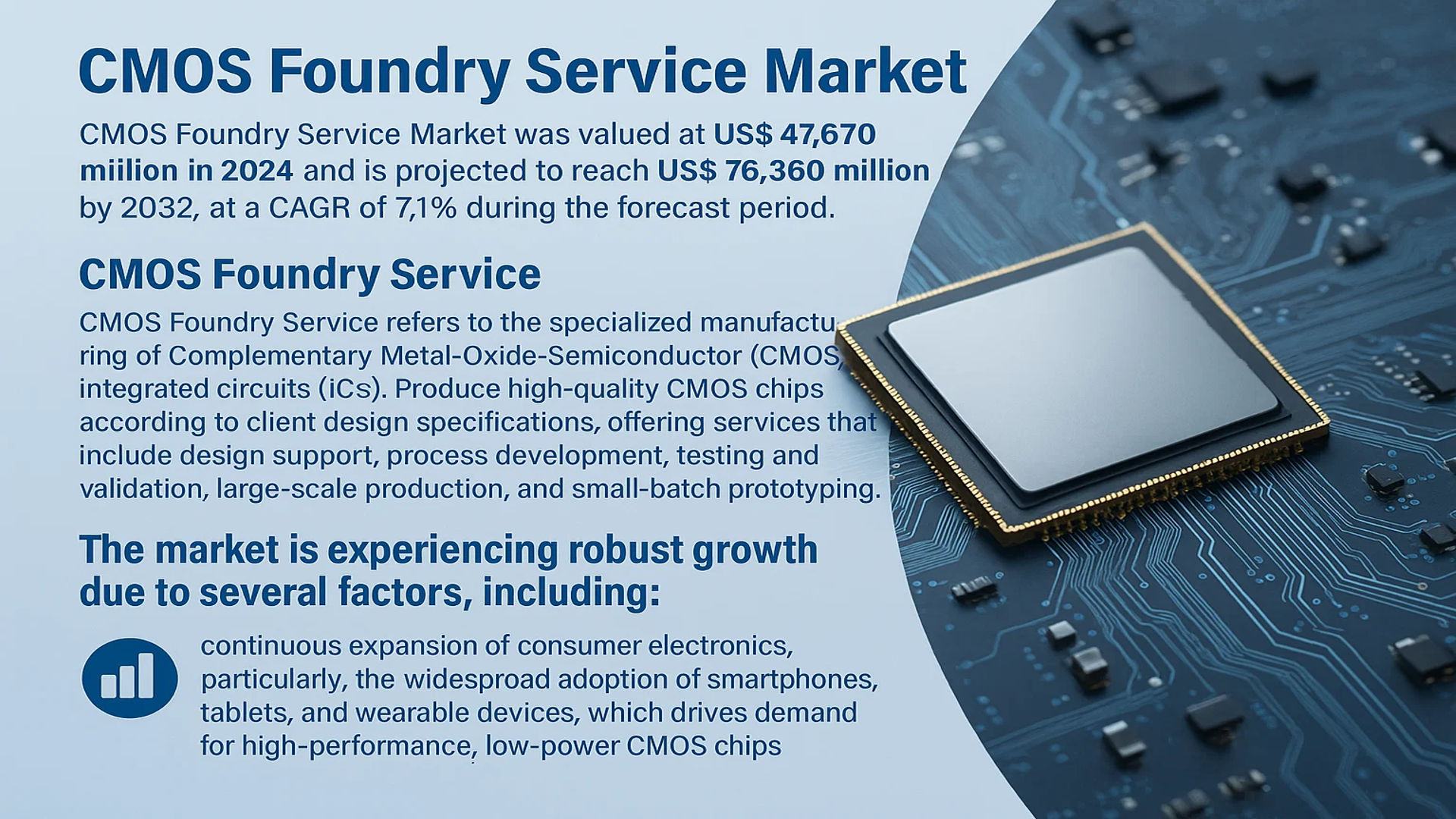

The global CMOS Foundry Service Market was valued at 47670 million in 2024 and is projected to reach US$ 76360 million by 2032, at a CAGR of 7.1% during the forecast period.

CMOS Foundry Service refers to the specialized manufacturing of Complementary Metal-Oxide-Semiconductor (CMOS) integrated circuits (ICs). These services are provided by professional semiconductor manufacturing companies that possess advanced manufacturing facilities and process technologies. They produce high-quality CMOS chips according to client design specifications, offering services that include design support, process development, testing and validation, large-scale production, and small-batch prototyping.

The market is experiencing robust growth due to several factors, including the continuous expansion of consumer electronics, particularly the widespread adoption of smartphones, tablets, and wearable devices, which drives demand for high-performance, low-power CMOS chips. Furthermore, the rapid development of automotive electronics, especially the rise of electric vehicles and autonomous driving technologies, increases the need for highly reliable CMOS chips. Additionally, the extensive application of emerging technologies such as 5G communication, the Internet of Things (IoT), and artificial intelligence (AI) further expands market demand. The expansion of data centers and cloud computing also fuels the need for high-performance computing chips, most of which are manufactured using CMOS processes. Key players such as TSMC, Samsung, and GlobalFoundries operate in the market with extensive portfolios and advanced technological capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of AI and High-Performance Computing to Accelerate Demand for Advanced Nodes

The exponential growth in artificial intelligence and high-performance computing applications is significantly driving the CMOS foundry service market. AI workloads, including machine learning training and inference, require immense computational power delivered by advanced semiconductor nodes. The demand for AI chips is projected to grow at a compound annual growth rate exceeding 35% through 2030, creating substantial pressure on foundries to deliver cutting-edge manufacturing capabilities. Major technology companies are investing billions in developing specialized AI accelerators, most of which utilize the latest CMOS processes for optimal performance and power efficiency. This trend is particularly evident in data center applications, where energy efficiency directly impacts operational costs and environmental sustainability. Foundries capable of producing at 5nm and below are experiencing unprecedented demand from both established semiconductor companies and emerging AI chip designers seeking to capitalize on this technological revolution.

5G Deployment and IoT Expansion to Fuel Semiconductor Manufacturing Requirements

The global rollout of 5G networks and the rapid expansion of Internet of Things devices are creating sustained demand for CMOS foundry services. 5G infrastructure requires sophisticated RF CMOS chips capable of handling higher frequency bands while maintaining signal integrity and power efficiency. The number of 5G connections worldwide is expected to reach 3.5 billion by 2026, driving continuous investment in network infrastructure and compatible devices. Simultaneously, IoT adoption continues to accelerate across industrial, consumer, and automotive applications, with projections indicating over 30 billion connected devices by 2025. These applications demand a diverse range of semiconductor solutions, from ultra-low-power chips for sensors to high-reliability components for industrial automation. Foundries are responding by developing specialized process technologies optimized for RF performance, low power consumption, and mixed-signal integration to address these expanding market segments.

Automotive Electronics Transformation to Drive Foundry Service Growth

The automotive industry’s transformation toward electrification and autonomous driving is generating substantial demand for specialized CMOS foundry services. Modern vehicles incorporate hundreds of semiconductors, with electric vehicles requiring approximately double the semiconductor content of traditional internal combustion vehicles. The automotive semiconductor market is projected to grow to over $80 billion by 2028, driven by advanced driver assistance systems, infotainment, and powertrain electronics. These applications require chips that meet stringent automotive-grade qualifications for reliability, temperature tolerance, and longevity. Foundries are investing in specialized automotive processes and expanding capacity to accommodate the automotive industry’s unique requirements. The shift toward software-defined vehicles and increasing electronic content per vehicle ensures sustained growth for foundries serving this sector, particularly those offering robust processes qualified for automotive applications.

MARKET CHALLENGES

Extreme Capital Intensity and Rising Manufacturing Costs to Constrain Market Expansion

The CMOS foundry industry faces significant challenges related to extreme capital expenditure requirements and escalating manufacturing costs. Establishing a state-of-the-art semiconductor fabrication facility now costs between $15 billion and $20 billion for advanced nodes, creating substantial barriers to entry and expansion. The cost per wafer has increased dramatically at each new process node, with 3nm wafer costs approximately 50% higher than 5nm processes. This financial burden is compounded by the need for continuous research and development investment to maintain technological competitiveness. Smaller foundries and new market entrants struggle to secure the necessary funding for capacity expansion and technology development, potentially limiting market diversity and innovation. The industry’s capital-intensive nature also makes it vulnerable to economic cycles and investment fluctuations, creating challenges for long-term planning and sustainable growth.

Other Challenges

Geopolitical Tensions and Supply Chain Fragmentation

Increasing geopolitical tensions and trade restrictions are creating significant challenges for the global CMOS foundry ecosystem. Export controls on advanced semiconductor manufacturing equipment and technologies are disrupting established supply chains and forcing foundries to navigate complex regulatory environments. The industry’s global nature means that restrictions in one region can impact production capabilities worldwide, potentially leading to capacity constraints and technology access limitations. Companies are facing increased compliance costs and operational complexity as they attempt to maintain multinational operations while adhering to evolving trade regulations and national security considerations.

Technical Complexity and Yield Management

The increasing technical complexity of advanced CMOS processes presents substantial manufacturing challenges. As feature sizes approach physical limits, phenomena such as quantum effects and atomic-scale variations become significant factors affecting yield and performance. Maintaining acceptable yields at 5nm and below requires sophisticated process control and extensive engineering expertise. The transition to new transistor architectures, including gate-all-around structures, introduces additional manufacturing complexities and potential yield challenges. Foundries must continuously invest in advanced metrology, process control systems, and engineering talent to address these technical hurdles while maintaining competitive production costs and delivery schedules.

MARKET RESTRAINTS

Cyclical Nature of Semiconductor Industry to Impact Foundry Utilization Rates

The semiconductor industry’s inherent cyclicality presents a significant restraint for CMOS foundry services. Historical patterns show that the industry experiences periods of oversupply followed by shortages, creating challenges for capacity planning and investment recovery. During downturn phases, foundry utilization rates can drop below 70%, impacting profitability and return on investment for recent capital expenditures. The memory of recent semiconductor shortages has prompted aggressive capacity expansion, which could lead to oversupply conditions in the medium term. This cyclical pattern makes it difficult for foundries to maintain consistent financial performance and justify continuous investment in next-generation technologies. The industry’s dependence on end-market demand from consumer electronics, which accounts for approximately 50% of semiconductor consumption, further exacerbates this cyclicality as consumer spending patterns fluctuate with economic conditions.

Intellectual Property Protection and Design Security Concerns to Limit Collaboration

Intellectual property protection and design security concerns represent significant restraints in the CMOS foundry ecosystem. As semiconductor designs become more complex and valuable, companies are increasingly cautious about sharing sensitive design information with external foundries. The potential for intellectual property theft or unauthorized replication creates barriers to broader adoption of foundry services, particularly for companies developing proprietary technologies. This concern is especially pronounced in military, aerospace, and automotive applications where security and reliability are paramount. Foundries must invest substantial resources in establishing robust security protocols, certification processes, and legal frameworks to address these concerns. However, the perception of risk remains a restraining factor for some potential customers, particularly those with highly sensitive or proprietary designs.

Environmental Regulations and Sustainability Requirements to Increase Operational Costs

Increasing environmental regulations and sustainability requirements are creating additional restraints for CMOS foundry operations. Semiconductor manufacturing is energy and water intensive, with advanced fabs consuming enough electricity to power small cities. Environmental regulations governing chemical usage, wastewater treatment, and greenhouse gas emissions are becoming more stringent worldwide. Compliance with these regulations requires significant capital investment in pollution control equipment, monitoring systems, and process modifications. The industry’s carbon footprint and water usage are facing increased scrutiny from regulators, investors, and customers. Meeting sustainability targets while maintaining competitive manufacturing costs presents a complex challenge, particularly for older facilities that may require substantial upgrades to meet modern environmental standards. These requirements add to the already substantial operational costs and may limit expansion plans in regions with particularly stringent environmental regulations.

MARKET OPPORTUNITIES

Emerging Applications in Quantum Computing and Neuromorphic Chips to Create New Revenue Streams

Emerging applications in quantum computing and neuromorphic chips present significant growth opportunities for CMOS foundry services. While still in early development stages, quantum computing requires sophisticated classical control systems manufactured using advanced CMOS processes. The quantum computing market is projected to grow exponentially as the technology matures, creating demand for specialized semiconductor manufacturing capabilities. Similarly, neuromorphic computing, which aims to mimic biological neural networks, requires novel chip architectures that can benefit from CMOS foundry expertise in heterogeneous integration and advanced packaging. These emerging fields represent potential markets worth billions of dollars as they transition from research to commercialization. Foundries that can develop processes optimized for these applications and establish early partnerships with research institutions and startups may capture substantial value in these nascent but high-potential markets.

Specialized Process Development for Edge Computing and Ultra-Low-Power Applications

The growth of edge computing and ultra-low-power applications creates substantial opportunities for foundries to develop specialized process technologies. Edge devices require chips that balance performance with extremely low power consumption, often operating on battery power or energy harvesting. The edge computing market is expected to grow at a compound annual growth rate exceeding 20% as more processing moves closer to data sources. This trend drives demand for processes optimized for low leakage, wide voltage operation, and mixed-signal integration. Foundries can differentiate themselves by offering processes specifically tailored for these applications, including technologies that enable near-threshold operation and improved power management capabilities. The proliferation of wearable devices, smart sensors, and always-on applications ensures sustained demand for these specialized processes, creating opportunities for foundries to develop niche expertise and capture value in these growing market segments.

Advanced Packaging and Heterogeneous Integration to Enable New Business Models

Advanced packaging and heterogeneous integration technologies present significant opportunities for CMOS foundries to expand their service offerings and capture additional value. As Moore’s Law scaling becomes more challenging, system performance improvements increasingly come from packaging innovations rather than transistor scaling. The advanced packaging market is growing at approximately 8% annually, driven by demand for improved performance, power efficiency, and form factor reduction. Foundries that develop expertise in 2.5D and 3D integration, silicon interposers, and chiplet architectures can offer more complete solutions to their customers. This trend enables foundries to move beyond traditional manufacturing services and provide value through system-level optimization and integration. The emergence of chiplet-based designs particularly benefits foundries with strong packaging capabilities, as it allows them to participate in value creation beyond the die level and establish stronger customer relationships through comprehensive solution offerings.

CMOS FOUNDRY SERVICE MARKET TRENDS

Advanced Process Node Evolution to Emerge as a Dominant Trend

The relentless pursuit of smaller process nodes continues to be the primary driver of innovation and investment within the CMOS foundry service market. While the 5-nanometer (nm) node has become the mainstream for high-performance computing and premium smartphones, the industry is rapidly progressing towards 3nm and even 2nm production. This evolution is critical because it directly enables higher transistor density, significantly improved performance, and reduced power consumption—key requirements for next-generation technologies. Leading foundries have committed over $200 billion in capital expenditure between 2021 and 2023 to develop and scale these advanced nodes. The transition to more complex extreme ultraviolet (EUV) lithography, which is essential for patterning at these scales, represents a monumental technical and financial hurdle. However, the payoff is substantial, as these advanced nodes are fundamental to powering artificial intelligence accelerators, advanced 5G modems, and the increasing computational needs of autonomous vehicles.

Other Trends

Rise of Specialized and Heterogeneous Integration

While the race to the smallest node captures headlines, a parallel and equally significant trend is the growing demand for specialized process technologies and advanced packaging solutions. Not all applications require or can afford the premium cost of the latest node. This has led foundries to develop a rich portfolio of specialty technologies, including RF-SOI for 5G/6G mmWave applications, high-voltage CMOS for automotive power management, and embedded non-volatile memory (eNVM) for microcontrollers in IoT devices. Furthermore, heterogeneous integration through advanced packaging techniques like 2.5D/3D IC, chip-on-wafer-on-substrate (CoWoS), and integrated fan-out (InFO) allows for the combination of multiple dies, often manufactured on different process nodes, into a single package. This approach optimizes performance, cost, and form factor, creating system-in-package (SiP) solutions that are crucial for space-constrained devices like wearables and smartphones.

Geopolitical Reshoring and Supply Chain Diversification

Geopolitical tensions and recent supply chain disruptions have catalyzed a strategic shift towards regionalizing semiconductor manufacturing capabilities. Governments worldwide are implementing substantial subsidies and policies, such as the US CHIPS and Science Act which allocates over $52 billion, and the European Chips Act, to bolster domestic foundry capacity and reduce reliance on a concentrated geographic supply base. This trend is not about decoupling but rather de-risking and diversifying the supply chain. It is driving significant investments in new fabrication facilities (fabs) across North America, Europe, and Japan. While this builds resilience, it also introduces challenges, including higher operational costs in these regions and a protracted timeline to establish a mature and competitive ecosystem comparable to established clusters in Asia. This strategic imperative ensures a more stable and secure supply of critical semiconductors for automotive, industrial, and defense applications.

Surging Demand from Automotive and AI Sectors

The automotive industry’s transformation into a technology-driven sector is creating an unprecedented demand for semiconductors. The average modern vehicle now incorporates over 1,400 chips, a number that is soaring with the adoption of electric vehicles, advanced driver-assistance systems (ADAS), and enhanced in-vehicle infotainment. These applications require chips built on robust, reliable, and often specialized CMOS processes capable of withstanding harsh automotive environments. Concurrently, the explosive growth of artificial intelligence, both in data centers and at the edge, is fueling demand for high-performance computing (HPC) chips. AI training and inference workloads necessitate immense processing power, which is primarily delivered by GPUs and ASICs manufactured on the most advanced CMOS nodes available. The convergence of these two powerful demand drivers is ensuring long-term, sustained growth for foundry services capable of meeting these stringent and high-volume requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global CMOS Foundry Service market is highly concentrated, dominated by a few major players while featuring numerous specialized foundries catering to niche applications. Taiwan Semiconductor Manufacturing Company (TSMC) stands as the undisputed market leader, commanding a significant share estimated at over 55% of the global pure-play foundry revenue in 2024. This dominance is primarily attributed to its technological leadership in advanced process nodes, including its mass production of 3nm technology and ongoing development of 2nm processes, coupled with its immense production capacity and diverse client base spanning Apple, NVIDIA, and Qualcomm.

Samsung Foundry and GlobalFoundries also hold substantial market shares, positioning themselves as key competitors. Samsung leverages its integrated device manufacturing (IDM) background and investment in cutting-edge EUV lithography to compete directly with TSMC in the advanced node race. Meanwhile, GlobalFoundries has strategically pivoted to focus on specialized technologies, such as RF-SOI and FD-SOI, carving out a strong position in markets like automotive and IoT where these technologies are critical.

p>Additionally, these leading companies are aggressively pursuing growth through massive capital expenditure initiatives and geographical expansions. For instance, TSMC is constructing new fabs in Arizona, USA, and Kumamoto, Japan, to address the global trend of supply chain regionalization. Similarly, Samsung is expanding its Pyeongtaek campus in South Korea. These moves are expected to further solidify their market positions over the forecast period.

Meanwhile, other significant players like United Microelectronics Corporation (UMC) and Semiconductor Manufacturing International Corporation (SMIC) are strengthening their presence by focusing on mature and specialty nodes, which remain in high demand for a wide array of applications beyond leading-edge logic. Companies such as STMicroelectronics and Tower Semiconductor (now part of Intel) are deepening their expertise in analog, mixed-signal, and power management ICs, ensuring continued growth through technological specialization and strategic partnerships in the competitive landscape.

List of Key CMOS Foundry Service Companies Profiled

- Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan)

- Samsung Foundry (South Korea)

- GlobalFoundries Inc. (U.S.)

- United Microelectronics Corporation (UMC) (Taiwan)

- Semiconductor Manufacturing International Corporation (SMIC) (China)

- Tower Semiconductor Ltd. (Israel)

- STMicroelectronics N.V. (Switzerland)

- SK hynix system ic (South Korea)

- Vanguard International Semiconductor Corporation (Taiwan)

- X-FAB Silicon Foundries SE (Germany)

- DB HiTek Co., Ltd. (South Korea)

- Shanghai Huahong Group (China)

- SilTerra Malaysia Sdn. Bhd. (Malaysia)

- Powerchip Semiconductor Manufacturing Corporation (PSMC) (Taiwan)

- Nexchip Semiconductor Corporation (China)

- Intel Foundry Services (U.S.)

Segment Analysis:

By Business Model

Pure Play Model Dominates Due to Specialized Manufacturing Focus and Technological Agility

The market is segmented based on business model into:

- Pure Play Model

- Subtypes: Advanced Node Foundries (e.g., sub-10nm), Mature Node Foundries (e.g., 28nm and above), Specialty Technology Foundries

- IDM (Integrated Device Manufacturer) Model

- Subtypes: Captive Foundry Services, Merchant Foundry Services

By Process Node

Advanced Nodes (sub-10nm) Segment Leads Due to Demand for High-Performance Computing and AI Chips

The market is segmented based on process node technology into:

- Advanced Nodes (sub-10nm)

- Subtypes: 7nm, 5nm, 3nm, and below

- Mainstream Nodes (10nm – 28nm)

- Mature Nodes (above 28nm)

- Subtypes: 40nm, 65nm, 90nm, 130nm, and above

- Specialty Technologies

- Subtypes: RF CMOS, High-Voltage CMOS, Embedded Non-Volatile Memory, BCD, SOI

By Application

Consumer Electronics Segment Leads Due to Proliferation of Smart Devices and IoT

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Smartphones, Tablets, Wearables, Home Appliances

- Automotive Electronics

- Subtypes: ADAS, Infotainment, Powertrain, Body Electronics

- Telecommunications

- Subtypes: 5G Infrastructure, Networking Equipment, Baseband Processors

- Industrial Control

- Medical Equipment

- Aerospace and Defense

- Others

By Wafer Size

300mm Wafer Segment Dominates Due to Superior Cost Efficiency and High-Volume Manufacturing

The market is segmented based on wafer size into:

- 300mm Wafers

- 200mm Wafers

- 150mm and below Wafers

Regional Analysis: CMOS Foundry Service Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the CMOS foundry service market, accounting for the largest market share by revenue and production volume. This dominance is primarily driven by Taiwan, South Korea, and China, which host the world’s leading pure-play foundries. Taiwan Semiconductor Manufacturing Company (TSMC), the market leader with over 60% global share, is aggressively expanding its advanced node capacity, including its 3nm and upcoming 2nm processes, to meet insatiable demand from fabless companies worldwide. Samsung Foundry in South Korea is a key competitor, also investing heavily in cutting-edge technologies. China’s Semiconductor Manufacturing International Corporation (SMIC) is rapidly scaling its mature and mid-range node capacity, supported by significant government initiatives aimed at achieving semiconductor self-sufficiency. The region benefits from a mature ecosystem of design houses, material suppliers, and packaging and testing services, creating a powerful and integrated supply chain. Demand is fueled by the massive local consumer electronics manufacturing base and the growing adoption of AI, 5G, and automotive electronics across the region.

North America

North America’s market is characterized by high-value, advanced research and development and a strong presence of fabless semiconductor companies and Integrated Device Manufacturers (IDMs). The United States government, through the CHIPS and Science Act which allocates $52.7 billion in funding and incentives, is actively encouraging the onshoring of advanced semiconductor manufacturing to bolster national security and supply chain resilience. Intel Corporation, traditionally an IDM, has launched Intel Foundry Services (IFS) to compete directly with pure-play foundries and is making monumental investments, including over $20 billion for new fabs in Arizona and Ohio, to establish a leading-edge manufacturing presence. GlobalFoundries, while focusing on specialized processes on mature nodes, is a significant player with major facilities in the U.S. The region’s demand is heavily driven by the need for high-performance computing chips for data centers, AI accelerators, and advanced automotive applications from its world-leading technology and automotive industries.

Europe

The European market is strategically focused on developing a more resilient and sovereign semiconductor ecosystem, as outlined in the ambitious EU Chips Act which aims to mobilize €43 billion in investments. The region’s strength lies not in competing at the most advanced process nodes but in dominating specialized technologies. STMicroelectronics and Infineon are leaders in producing highly reliable chips for the automotive and industrial sectors, utilizing technologies like BCD, FD-SOI, and power management ICs. These companies often operate on an IDM model but also utilize foundry services. The region is actively building capacity for these essential chips to reduce dependency on external supply chains. Furthermore, Europe hosts key R&D centers for advanced packaging and materials science, positioning it as an innovation hub for next-generation semiconductor technologies that complement leading-edge logic manufacturing.

Middle East & Africa

The market in the Middle East & Africa is nascent but shows strategic long-term potential, primarily through significant sovereign investment vehicles. The region is not currently a volume manufacturer but is making calculated entries into the semiconductor space. The most prominent development is the acquisition of a controlling stake in GlobalFoundries by Mubadala Investment Company of the UAE, giving the region a substantial indirect foothold in the global foundry business. Countries like Saudi Arabia and Israel are also exploring investments in semiconductor design and potentially specialty fabrication as part of broader economic diversification plans. While the region lacks the established ecosystem and volume demand of Asia, its financial capacity and strategic intent to move into high-tech industries signal a growing, albeit niche, role in the global CMOS foundry landscape focused on investment and ownership rather than direct operational control.

South America

South America represents a minor and underdeveloped region in the global CMOS foundry service market. The region has limited domestic semiconductor manufacturing infrastructure and is almost entirely reliant on imports to meet its electronics production needs. Economic volatility, inconsistent government support for high-tech industries, and a lack of a robust local supply chain have historically hindered any significant development. Brazil has seen intermittent efforts to establish a local chip industry, but these have faced challenges in achieving scale and competitiveness. The market is primarily driven by consumption in end-user industries like consumer electronics and automotive, with all required chips sourced from foundries in Asia, North America, and Europe. For the foreseeable future, South America’s role is expected to remain that of a consumer rather than a producer in the global CMOS foundry ecosystem.

Report Scope

This market research report provides a comprehensive analysis of the global CMOS Foundry Service market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by business model (Pure Play vs. IDM), application, and technology node to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, advanced semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for fabless semiconductor companies, integrated device manufacturers (IDMs), system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global CMOS Foundry Service Market?

-> CMOS Foundry Service Market was valued at 47670 million in 2024 and is projected to reach US$ 76360 million by 2032, at a CAGR of 7.1% during the forecast period.

Which key companies operate in Global CMOS Foundry Service Market?

-> Key players include TSMC, Samsung Foundry, GlobalFoundries, UMC, SMIC, Tower Semiconductor, STMicroelectronics, and Intel Foundry Services, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for consumer electronics, automotive electrification, 5G deployment, AI acceleration, and cloud computing expansion.

Which region dominates the market?

-> Asia-Pacific dominates the market, holding over 75% of global foundry capacity, with Taiwan, South Korea, and China as major manufacturing hubs.

What are the emerging trends?

-> Emerging trends include transition to sub-3nm nodes, development of specialized processes (RF, HV, BCD), advanced packaging (3D IC, chiplets), and geographic diversification of manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...