CMOS comparator with body-driven input for low voltage Market Insights

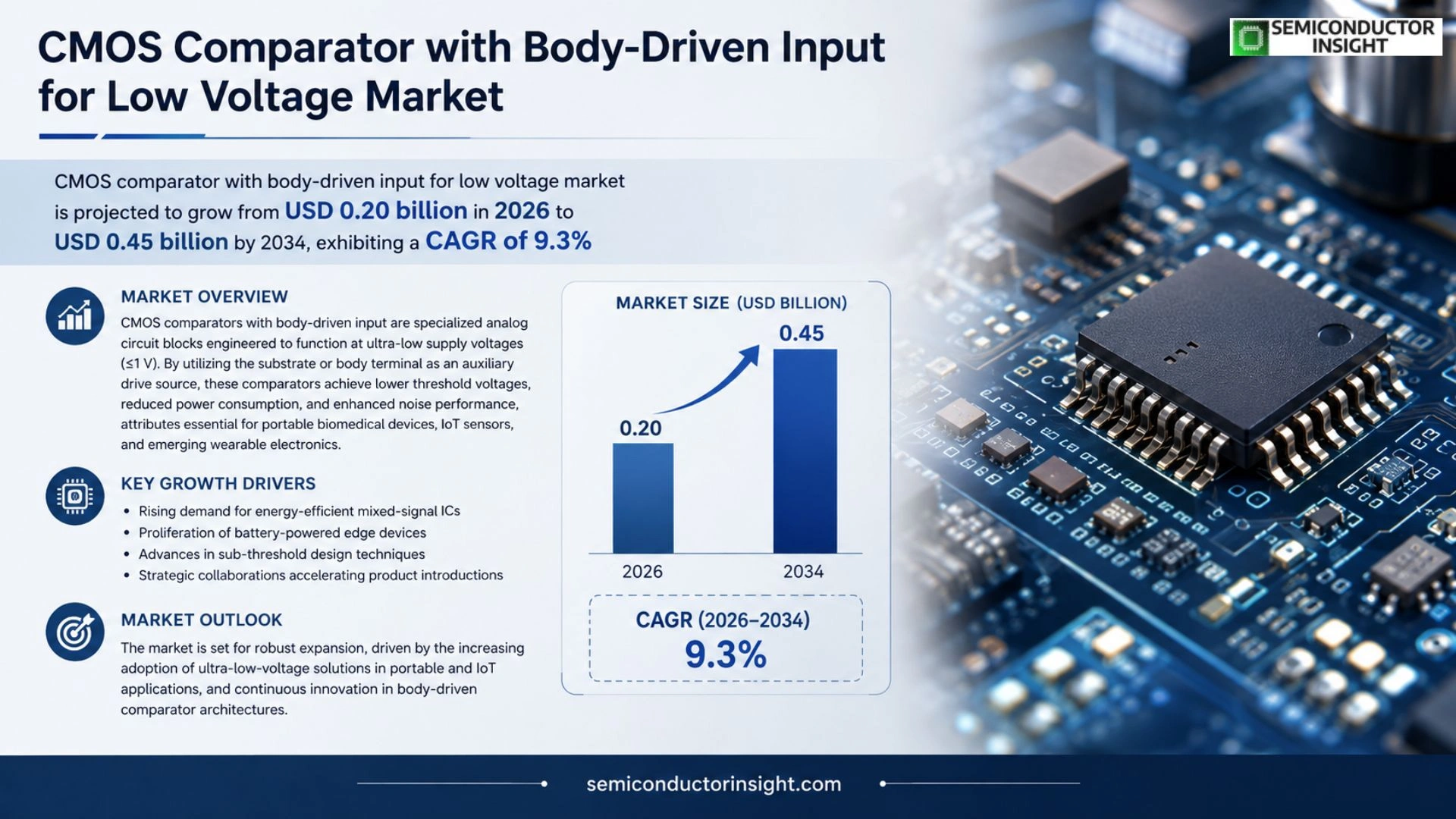

Global CMOS comparator with body-driven input for low voltage market size was valued at USD 0.18 billion in 2025. The market is projected to grow from USD 0.20 billion in 2026 to USD 0.45 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

CMOS comparators with body‑driven input are specialized analog circuit blocks engineered to function at ultra‑low supply voltages (≤1 V). By utilizing the substrate or body terminal as an auxiliary drive source, these comparators achieve lower threshold voltages, reduced power consumption, and enhanced noise performance,attributes essential for portable biomedical devices, IoT sensors, and emerging wearable electronics.

The market is experiencing rapid growth due to several factors, including heightened demand for energy‑efficient mixed‑signal ICs, proliferation of battery‑powered edge devices, and advances in sub‑threshold design techniques. Furthermore, strategic collaborations among semiconductor foundries and IP vendors are accelerating product introductions. Key players such as Texas Instruments, Analog Devices, ON Semiconductor, and STMicroelectronics are expanding their portfolios with body‑driven comparator IP blocks.

MARKET DRIVERS

Increasing Demand for Energy‑Efficient IoT Devices

The rise of battery‑powered Internet‑of‑Things (IoT) sensors is pushing designers toward components that operate reliably at sub‑1 V supply levels. A CMOS comparator with body‑driven input for low voltage Market offers the ultra‑low power consumption and fast decision speed required for such applications, making it a core enabler of the next‑generation edge ecosystem.

Advancements in Low‑Voltage Process Technologies

Modern 28 nm and 65 nm CMOS processes provide higher transistor densities while maintaining threshold voltages that support body‑driven operation. These process improvements reduce die size and cost, encouraging OEMs to adopt the specialized comparator in portable medical and wearable platforms.

➤ “Designers can achieve sub‑nanowatt standby power without compromising speed, a combination that was previously unattainable.”

Regulatory pressures for lower power consumption and longer device lifecycles further reinforce market adoption, as manufacturers seek solutions that meet both performance and sustainability targets.

MARKET CHALLENGES

Complex Integration with Mixed‑Signal Architectures

Integrating a CMOS comparator with body‑driven input for low voltage Market into heterogeneous SoCs requires careful matching of bias networks and careful layout to avoid substrate noise coupling. This complexity can increase design verification time and cost.

Other Challenges

Limited Design Expertise

Many analog design teams lack hands‑on experience with body‑driven techniques, leading to a steeper learning curve and potential under‑utilization of the comparator’s capabilities.

MARKET RESTRAINTS

Stringent Performance Verification Requirements

Certification bodies often require exhaustive testing of low‑voltage comparator performance across temperature and process corners. The need for extensive validation can delay product launches and raise non‑recurring engineering expenses.

Additionally, the limited availability of calibrated reference models for body‑driven inputs can hinder rapid simulation, forcing designers to rely on time‑consuming silicon iterations.

MARKET OPPORTUNITIES

Emerging Wearable Health Monitoring Segment

Wearable devices that continuously monitor physiological signals require ultra‑low power front‑end comparators. The specialized comparator’s ability to function at sub‑0.5 V makes it ideally suited for next‑generation health trackers, opening a sizable growth avenue.

Furthermore, expanding 5G edge computing nodes, which operate on constrained power budgets, present an untapped market where the comparator’s fast response combined with minimal energy draw can provide a competitive edge.

CMOS comparator with body-driven input for low voltage Market Trends

Rising Demand for Ultra‑Low‑Voltage Solutions

CMOS comparator with body-driven input for low voltage is being reshaped by a surge in battery‑operated edge devices. Designers increasingly target supply voltages at or below 1 V to extend runtimes in wearable health monitors, IoT sensors, and portable diagnostic equipment. By leveraging the substrate as a drive source, these comparators achieve threshold voltages well under 200 mV, which directly reduces static power draw. As a result, system‑level power budgets improve by 30 % or more, enabling longer operation without compromising signal integrity. The trend is supported by a growing ecosystem of low‑voltage analog IP, standardized design kits, and foundry processes optimized for sub‑threshold operation.

Other Trends

Energy‑Efficient Mixed‑Signal Integration

Manufacturers are integrating body‑driven comparators into mixed‑signal ASICs to consolidate functionality and lower board‑level component count. This integration reduces parasitic inductances and improves noise margins, which is critical for biomedical signal acquisition where millivolt‑level precision is required. Recent product releases from leading vendors illustrate a shift toward modular IP blocks that can be instantiated alongside low‑power ADCs and digital controllers, delivering a cohesive ultra‑low‑power front‑end. The approach also shortens time‑to‑market, as designers reuse validated blocks rather than developing custom comparator stages from scratch.

Strategic Partnerships Driving Innovation

Collaboration between semiconductor foundries and analog IP specialists is accelerating the availability of body‑driven comparator solutions. Joint development programs focus on optimizing transistor sizing, body‑bias schemes, and layout techniques to meet stringent power‑performance targets. These partnerships have resulted in a broadened portfolio that addresses diverse application segments, from implantable medical devices to autonomous sensor networks. By sharing simulation models and silicon validation data, partners reduce risk and enable faster adoption of ultra‑low‑voltage architectures across the industry.

COMPETITIVE LANDSCAPE

Key Industry Players

CMOS Comparator with Body‑Driven Input Market Overview

CMOS comparator market for body‑driven input at ultra‑low supply voltages is dominated by a handful of large analog powerhouses that have integrated the technology into their mixed‑signal portfolios. Texas Instruments, Analog Devices, ON Semiconductor, and STMicroelectronics lead the segment, each offering product families that target battery‑operated IoT sensors, portable biomedical instrumentation, and wearable electronics. Their extensive design‑win programs, global distribution networks, and deep wafer‑fab partnerships enable rapid deployment of sub‑threshold comparator IP, reinforcing a market structure where a few tier‑1 players capture the majority of revenue while licensing IP to fabless designers. The market’s valuation of USD 0.18 billion in 2025 and projected CAGR of 9.3 % through 2034 reflect the strong demand for energy‑efficient analog building blocks in emerging low‑power ecosystems.

Beyond the tier‑1 leaders, a diverse set of niche and regionally focused firms contributes specialized expertise and alternative architectures. Companies such as NXP Semiconductors, Infineon Technologies, Microchip Technology, Renesas Electronics, Rohm Semiconductor, Skyworks Solutions, Dialog Semiconductor (now part of Renesas), Cypress Semiconductor (now Infineon), and Maxim Integrated are expanding their offering with body‑driven comparator IP or reference designs. These participants often leverage strategic collaborations with foundries or focus on vertical markets like automotive sensor arrays, industrial IoT, and medical wearables, adding depth and competitive pressure that fosters innovation across the value chain.

List of Key CMOS Comparator Companies Profiled

- Texas Instruments

- Analog Devices

- ON Semiconductor

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies

- Microchip Technology

- Renesas Electronics

- Rohm Semiconductor

- Skyworks Solutions

- Dialog Semiconductor

- Maxim Integrated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Body‑Driven Architecture

|

| By Application |

|

Energy‑Sensitive Applications

|

| By End User |

|

Design‑Centric End Users

|

| By Voltage Range |

|

Sub‑Threshold Focus

|

| By Integration Mode |

|

IP‑Core Dominance

|

Regional Analysis: CMOS comparator with body-driven input for low voltage Market

North America

The push for ultra‑low power consumption in automotive safety modules and wearable health monitors fuels demand for CMOS comparator with body‑driven input for low voltage designs, especially where battery life and miniaturisation are critical.

Energy‑efficiency standards across North America push OEMs toward components that minimise quiescent current, indirectly promoting adoption of body‑driven input comparator architectures.

Established analog giants and emerging fabless innovators compete on integration density and voltage headroom, with partnerships accelerating technology transfer and market penetration.

Advances in finFET and FD‑SOI processes enable finer control of body bias, enhancing comparator performance at sub‑1 V supply levels.

Europe

Europe’s market for CMOS comparator with body‑driven input for low voltage is shaped by strong automotive engineering clusters in Germany and France. OEMs seek components that meet stringent emission‑reduction targets while maintaining high safety margins, prompting adoption of low‑voltage analog blocks. Collaborative research programmes funded by the EU foster cross‑border innovation, particularly in mixed‑signal ASICs for smart infrastructure. Though supply‑chain consolidation poses challenges, the region’s focus on sustainability and precision engineering sustains a positive outlook through the forecast horizon.

Asia‑Pacific

Asia‑Pacific demonstrates rapid uptake of CMOS comparator with body‑driven input for low voltage technology, driven largely by China, Japan, and South Korea’s expanding consumer electronics and automotive sectors. Cost‑competitiveness combined with aggressive scaling of foundry capabilities enables manufacturers to embed low‑voltage comparators into mass‑market devices such as smartphones and electric‑vehicle control units. Government incentives for low‑energy electronics further accelerate market momentum, while rising expertise in advanced packaging supports higher integration levels.

South America

South America’s growth in CMOS comparator with body‑driven input for low voltage arena remains nascent but promising, anchored by Brazil’s expanding automotive assembly plants and Argentina’s IoT pilot projects. Market entry is facilitated by partnerships with North American foundries, allowing local designers to access cutting‑edge analog IP. While economic volatility tempers investment, the region’s increasing focus on renewable energy systems and low‑power sensor networks creates a niche demand for ultra‑efficient comparator solutions.

Middle East & Africa

In the Middle East & Africa, adoption of CMOS comparator with body‑driven input for low voltage is primarily propelled by infrastructure monitoring and smart‑grid initiatives. UAE and South Africa lead with pilot deployments that leverage low‑power analog front‑ends for grid resilience and environmental sensing. Limited local fabrication capacity means reliance on imports, yet strategic import agreements and emerging design houses are laying the groundwork for broader market participation over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the CMOS comparator with body-driven input for low voltage Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

-

Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, …

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CMOS comparator with body-driven input for low voltage Market?

-> CMOS comparator with body-driven input for low voltage market is projected to grow from USD 0.20 billion in 2026 to USD 0.45 billion by 2034

Which key companies operate in CMOS comparator with body-driven input for low voltage Market?

-> Key players include Texas Instruments, Analog Devices, ON Semiconductor, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy‑efficient mixed‑signal ICs, proliferation of battery‑powered edge devices, advances in sub‑threshold design techniques, and strategic collaborations between semiconductor foundries and IP vendors.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains the dominant market in terms of revenue share.

What are the emerging trends?

-> Emerging trends include integration of body‑driven comparators in biomedical wearables, IoT sensor modules, low‑power AI edge processors, and the development of standardized IP blocks for sub‑threshold operation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...