Chip-scale LIDAR with optical phased array solid-state beam steering Market Insights

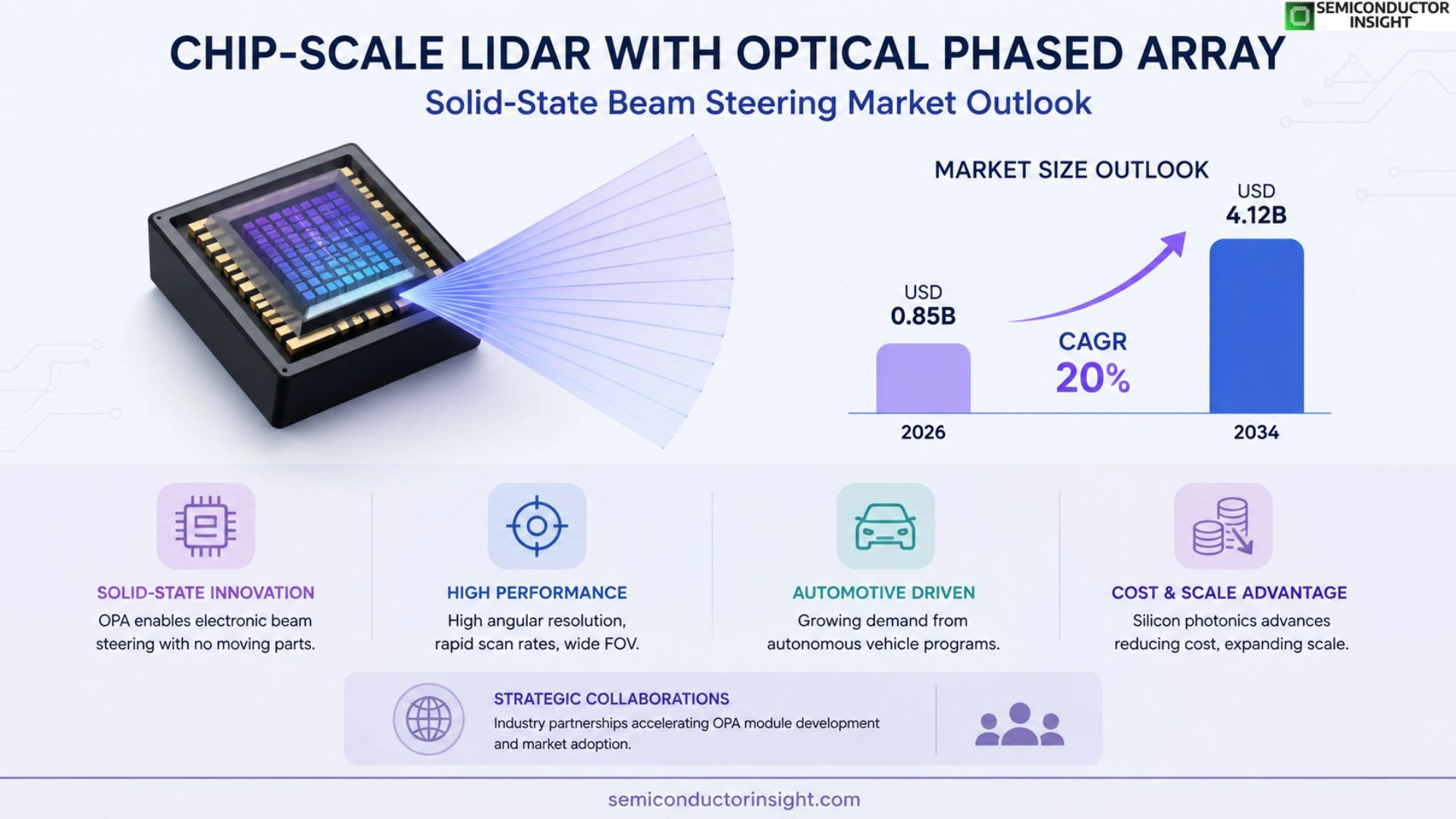

Chip-scale LIDAR with optical phased array solid-state beam steering market size was valued at USD 0.78 billion in 2025. The market is projected to grow from USD 0‑85 billion in 2026 to USD 4‑12 billion by 2034, exhibiting a CAGR of 20% during the forecast period.

Chip‑scale LiDAR equipped with an optical phased array (OPA) enables solid‑state beam steering without moving parts, leveraging photonic integrated circuits that emit thousands of coherent light beams across a wide field‑of‑view.

This technology delivers high angular resolution and rapid scan rates while maintaining a compact footprint suitable for automotive and robotics platforms.

The market is experiencing rapid growth because automotive manufacturers are accelerating autonomous‑vehicle programs that demand reliable, low‑cost perception sensors.

Furthermore, advances in silicon photonics have reduced production costs, while strategic collaborations,such as Intel’s partnership with Mobileye on OPA modules announced in early 2024,are expanding deployment opportunities.

Key players including Velodyne LiDAR Inc., Luminar Technologies, AEye Inc., Innoviz Technologies and Quanergy Systems are actively expanding their portfolios through new product launches and joint development agreements.

MARKET DRIVERS

Rising Demand in Autonomous Vehicles

Chip-scale LIDAR with optical phased array solid-state beam steering Market is being propelled by the rapid expansion of autonomous vehicle platforms, where manufacturers require compact, low‑power, and high‑resolution sensing solutions. Recent production forecasts indicate that more than 1.2 million autonomous‑ready vehicles will be equipped with chip‑scale LIDAR units by 2026, reflecting a significant shift from traditional mechanical scanners.

Advancements in Semiconductor Manufacturing

Innovations in silicon photonics and wafer‑scale integration have lowered the cost per unit of chip‑scale LIDAR devices, enabling manufacturers to target mass‑market pricing thresholds under $150. These manufacturing breakthroughs also improve yield rates to above 92%, enhancing the overall economic viability of the technology.

➤ Over 70% of new LIDAR deployments in 2024 are chip‑scale devices, underscoring the pace of adoption.

In parallel, the rise of advanced driver‑assistance systems (ADAS) in mid‑range vehicles is creating a broader consumer base, further accelerating market penetration and encouraging investment in R&D for higher frame‑rate optical phased arrays.

MARKET CHALLENGES

Technical Integration Complexities

Integrating chip‑scale LIDAR with existing vehicle electronics demands precise thermal management and firmware harmonization. The high‑frequency steering of optical phased arrays can introduce electromagnetic interference, requiring sophisticated shielding solutions that increase system complexity.

Other Challenges

Cost Sensitivity

Despite declining wafer costs, the overall bill of materials remains sensitive to fluctuations in semiconductor supply chains. Manufacturers must balance price pressures with performance targets to remain competitive in tier‑1 supplier contracts.

The limited availability of qualified foundries capable of high‑volume photonic integration adds another layer of risk, potentially delaying product roll‑outs and affecting time‑to‑market strategies.

MARKET RESTRAINTS

Regulatory Hurdles in Global Markets

Regulatory frameworks for automotive LIDAR vary widely across regions, with Europe enforcing stricter functional safety standards (ISO 26262) than North America. These divergent requirements compel OEMs to pursue multiple certification pathways, inflating development costs and extending product launch timelines.

MARKET OPPORTUNITIES

Emerging Applications in UAVs and Robotics

The lightweight nature of chip‑scale LIDAR makes it ideal for unmanned aerial vehicles (UAVs) and collaborative robots, where payload constraints are critical. Forecasts suggest a 35% CAGR for LIDAR‑enabled UAV platforms between 2024 and 2029, driven by demand for real‑time 3‑D mapping in logistics and inspection.

Additionally, the consumer electronics sector is exploring integration of optical phased arrays for augmented reality (AR) headsets, presenting a new revenue stream that could double the addressable market size within the next five years.

Chip-scale LIDAR with optical phased array solid-state beam steering Market Trends

Accelerating Adoption in Autonomous Vehicles

Chip-scale LIDAR with optical phased array solid-state beam steering Market is experiencing a pronounced shift as original equipment manufacturers integrate advanced perception sensors into next‑generation driver‑assist and autonomous platforms. The optical phased array architecture eliminates moving parts, delivering rapid scan rates and high angular resolution while preserving a compact footprint ideal for vehicle integration. Automotive OEMs are scaling pilot programs to validate sensor suites that meet stringent safety standards, creating a clear pathway for volume production. This momentum is reinforced by regulatory trends that encourage higher levels of automation, prompting suppliers to align road‑map timelines with automaker expectations.

Other Trends

Cost Reduction through Silicon Photonics

Recent breakthroughs in silicon photonic manufacturing have lowered wafer‑level costs, enabling Chip-scale LIDAR solutions to approach price points compatible with mass‑market vehicles. The transition from discrete components to photonic integrated circuits reduces assembly complexity and enhances yield consistency. As a result, suppliers can offer solid‑state beam steering modules that balance performance with affordability, addressing one of the primary barriers to widespread adoption in both automotive and robotics sectors.

Strategic Partnerships Driving Ecosystem Growth

Collaborations between semiconductor foundries, sensor specialists, and automotive technology firms are accelerating product commercialization. Notable examples include joint development agreements that combine expertise in OPA module design with vehicle‑level integration, yielding reference platforms that demonstrate real‑world reliability. These alliances also facilitate shared roadmaps for software and hardware co‑design, ensuring that firmware updates, calibration tools, and safety certifications evolve in tandem with hardware releases. The cumulative effect is a more resilient supply chain and a faster feedback loop between end‑users and manufacturers, reinforcing confidence in the technology’s long‑term viability.

COMPETITIVE LANDSCAPE

Key Industry Players

Chip‑scale LIDAR with Optical Phased Array Solid‑State Beam Steering Market Overview

The market is currently anchored by a handful of large‑scale manufacturers that have transitioned optical‑phased‑array (OPA) technology from research labs to production lines. Velodyne LiDAR Inc., leveraging its acquisition of OPA assets and a strategic partnership with Intel’s Mobileye division, dominates the high‑volume automotive segment by offering a cost‑effective, wafer‑scale solution that meets the 20 % CAGR target. Intel’s in‑house silicon‑photonic foundry complements Velodyne’s supply chain, creating a de‑facto tier‑one ecosystem that attracts OEMs seeking standardized integration. This concentration of capability establishes a clear market hierarchy where a few well‑capitalized firms control the bulk of revenue while smaller innovators focus on niche verticals such as robotics and UAVs.

Beyond the tier‑one leaders, a vibrant cohort of specialized players enriches the competitive landscape. Luminar Technologies and AEye Inc. advance hybrid OPA‑MEMS designs that improve range‑resolution trade‑offs for Level‑3+ autonomous driving. Innoviz Technologies and Quanergy Systems accelerate time‑to‑market through joint‑development agreements with Tier‑2 automotive suppliers. European entrants including Valeo, LeddarTech, and Continental tighten the supply chain for automotive manufacturers by integrating OPA modules into existing radar‑fusion architectures. Asian firms such as Sony and NXP contribute silicon‑photonic IP, while startups like Ouster, RoboSense, and LeddarTech pursue bespoke form‑factors for robotics, industrial automation, and indoor navigation, ensuring a diversified pipeline of innovation.

List of Key Chip-scale LIDAR with Optical Phased Array Companies Profiled

- Velodyne LiDAR Inc.

- Luminar Technologies

- AEye Inc.

- Innoviz Technologies

- Quanergy Systems

- Valeo

- LeddarTech

- Continental AG

- Ouster

- RoboSense

- Sony Semiconductor

- NXP Semiconductors

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

OPA‑based solid‑state is emerging as the dominant type because it eliminates moving parts, delivering higher reliability and faster scan cycles. – Enables ultra‑compact modules that integrate directly onto silicon photonic chips. – Provides consistent beam quality across a wide field‑of‑view, essential for safety‑critical perception. – Attracts automotive OEMs seeking long‑term cost reductions through scalable wafer‑level manufacturing. |

| By Application |

|

Autonomous driving drives the most compelling use case, demanding precise 3‑D mapping at high refresh rates. – Chip‑scale OPA LIDAR offers a low‑profile sensor that fits within vehicle design constraints. – The solid‑state nature aligns with automotive reliability standards and reduces maintenance concerns. – Enables seamless fusion with camera and radar data streams for robust perception. |

| By End User |

|

Automotive OEMs are the primary end‑users, integrating chip‑scale OPA LIDAR into next‑generation vehicle platforms. – They value the technology’s ability to meet stringent safety and durability requirements. – Preference for vendors that can provide co‑development support and long‑term supply assurance. – The trend toward fleet‑wide autonomous solutions amplifies demand for standardized, high‑volume sensor modules. |

| By Beam Steering Mechanism |

|

Optical phased array remains the core steering method, offering precise angular control without mechanical wear. – Supports rapid beam re‑direction essential for high‑speed vehicle scenarios. – Benefits from advances in silicon photonics that simplify integration with existing semiconductor processes. – Positions vendors to differentiate on performance rather than on moving‑part reliability. |

| By Market Deployment Stage |

|

Full‑scale production is accelerating as manufacturers lock in supply chains and design‑for‑manufacturability. – Companies are transitioning from prototype validation to volume‑ready modules. – The shift reflects confidence in cost‑effective silicon photonic fabrication. – Drives ecosystem growth as system integrators plan for large‑lot deployments in upcoming vehicle generations. |

Regional Analysis: North America

North America

The automotive industry is the primary consumer of chip-scale LIDAR technology in North America, driven by the escalating need for enhanced safety features and the pursuit of autonomous driving capabilities. OEMs are actively incorporating these sensors to improve object detection, lane keeping, and adaptive cruise control.

Government funding and regulatory support play a crucial role in accelerating the adoption of chip-scale LIDAR. Initiatives promoting autonomous vehicle development and road safety are creating a favorable environment for market expansion.

Significant R&D investments in North America are driving technological advancements in chip-scale LIDAR, leading to improved performance, reduced costs, and enhanced miniaturization. Collaboration between academic institutions and industry players is fostering innovation.

North America hosts a strong ecosystem of chip-scale LIDAR technology providers, ranging from established players to emerging startups, contributing to a competitive and innovative market landscape.

Europe

Europe’s market for Chip-scale LIDAR with optical phased array solid-state beam steering is experiencing steady growth, propelled by stringent automotive safety regulations and a growing emphasis on intelligent transportation systems. The region’s automotive sector is actively integrating advanced driver-assistance systems (ADAS) and autonomous driving features, creating demand for compact and cost-effective LIDAR solutions. Government initiatives promoting sustainable mobility and road safety are further supporting market expansion. Concerns regarding data privacy and cybersecurity are influencing the design and deployment of LIDAR systems in Europe. The focus on fuel efficiency and electric vehicles is also driving innovation in LIDAR technology to reduce system weight and power consumption.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for Chip-scale LIDAR with optical phased array solid-state beam steering. The region’s burgeoning automotive industry, particularly in China and Japan, is a major driver of demand. Rapid urbanization, increasing disposable incomes, and a growing awareness of road safety are contributing to market expansion. Government support for the development of autonomous driving technologies and smart cities is also fueling growth. The presence of a large number of electronics manufacturers in Asia-Pacific provides a strong foundation for the production of chip-scale LIDAR systems. Intense competition among regional players is leading to cost reductions and technological advancements.

South America

South America represents a nascent market for Chip-scale LIDAR with optical phased array solid-state beam steering, with growth potential linked to the development of the automotive and public transportation sectors. Increasing investments in infrastructure projects and a growing demand for enhanced safety features in vehicles are expected to drive adoption. The region’s automotive industry is gradually incorporating ADAS technologies, creating initial demand for LIDAR sensors. Government regulations and initiatives promoting road safety and sustainable transportation are also contributing to market growth. However, the relatively lower purchasing power and the presence of a fragmented automotive market pose challenges to rapid market expansion.

Middle East & Africa

The Middle East & Africa region presents a long-term growth opportunity for Chip-scale LIDAR with optical phased array solid-state beam steering, driven by increasing investments in infrastructure development and the growing adoption of advanced automotive technologies. Rising disposable incomes and a growing emphasis on safety are expected to fuel demand for ADAS and autonomous driving features. Government initiatives promoting smart cities and intelligent transportation systems are also contributing to market expansion. The region’s automotive market is undergoing rapid transformation, with increasing demand for connectivity and driver-assistance technologies. However, the region’s challenging economic conditions and geopolitical uncertainties pose potential risks to market growth.

Report Scope

This market research report provides a comprehensive analysis of the Chip-scale LIDAR with optical phased array solid-state beam steering Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chip-scale LIDAR with optical phased array solid-state beam steering Market?

-> Chip-scale LIDAR with optical phased array solid-state beam steering Market was valued at USD 0.78 billion in 2025 and is expected to reach USD 4.12 billion by 2034.

Which key companies operate in Chip-scale LIDAR with optical phased array solid-state beam steering Market?

-> Key players include Velodyne LiDAR Inc., Luminar Technologies, AEye Inc., Innoviz Technologies and Quanergy Systems, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of autonomous‑vehicle programs, demand for low‑cost high‑resolution perception sensors, advances in silicon photonics reducing production costs, and strategic collaborations such as Intel’s partnership with Mobileye on OPA modules.

Which region dominates the market?

-> The reference does not specify a single dominant region; market activity is global with significant contributions from North America and Asia‑Pacific.

What are the emerging trends?

-> Emerging trends include solid‑state OPA‑based beam steering, integration of photonic integrated circuits for higher angular resolution, rapid scan rates for real‑time sensing, and expanding applications in automotive and robotics platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...