Chip-on-chip stacked image sensor with pixel-level ADC Market Insights

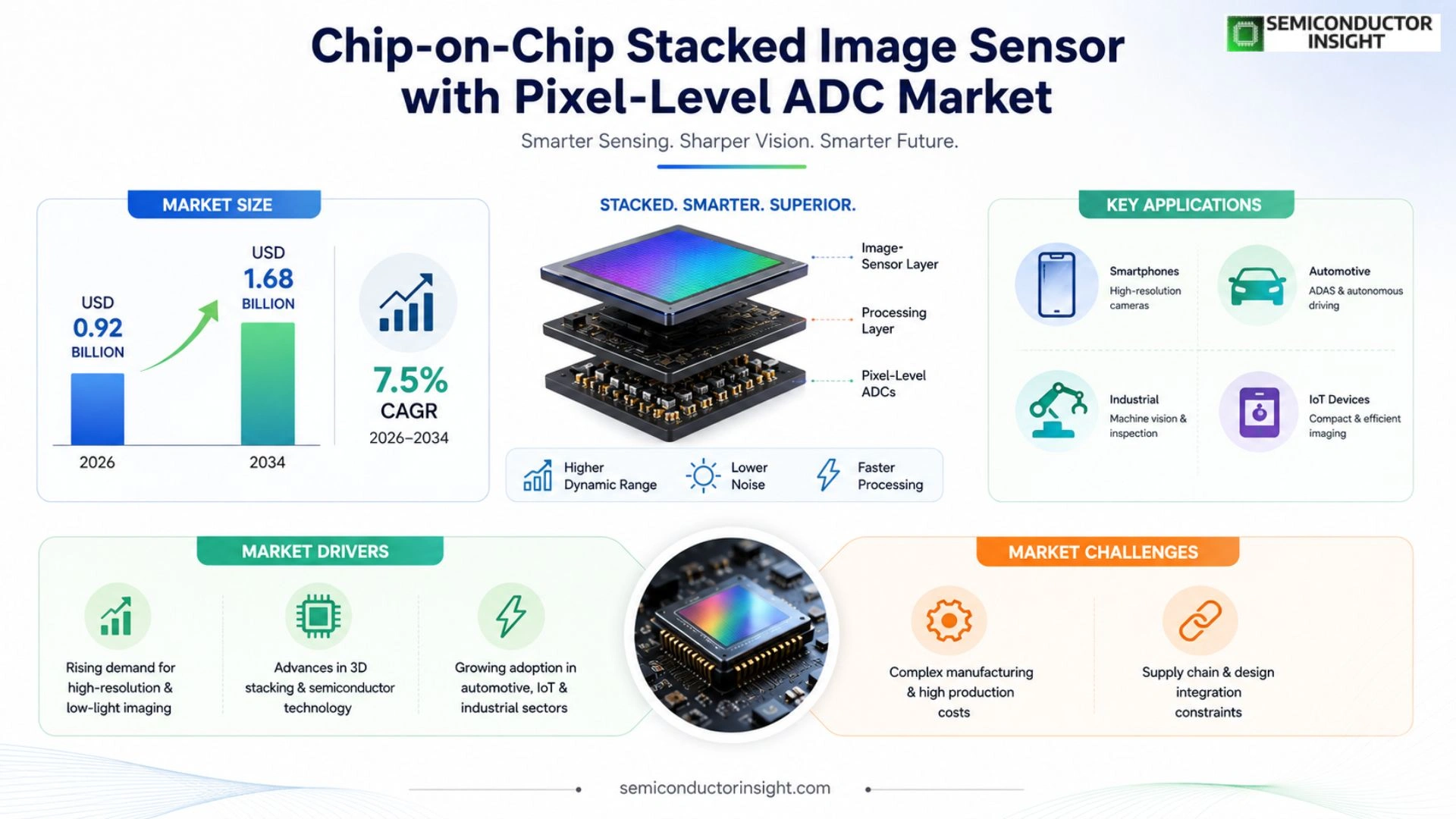

Global Chip-on-chip stacked image sensor with pixel-level ADC market size was valued at USD 0.84 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.68 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period.

Chip-on-chip stacked image sensors combine a light-sensing layer and a dedicated signal-processing layer in a vertical stack, while pixel-level analog-to-digital converters (ADCs) perform conversion directly within each pixel. This architecture delivers superior quantum efficiency, higher dynamic range, and reduced noise compared with conventional front-side illuminated sensors.

The market is experiencing rapid growth because smartphone manufacturers demand ever higher resolution and low-light performance, automotive firms require reliable vision systems for ADAS, and industrial IoT devices seek compact high-speed imaging solutions. Furthermore, recent advances such as Sony’s IMX989 sensor and Samsung’s ISOCELL GM1 illustrate industry momentum.

MARKET DRIVERS

Rising Demand for High-Resolution Imaging

Smartphones, autonomous vehicles, and industrial inspection systems are increasingly requiring higher pixel counts and faster frame rates. Chip-on-chip stacked image sensor with pixel-level ADC Market addresses this need by integrating analog-to-digital conversion at each pixel, reducing noise and improving dynamic range.

Advancements in Semiconductor Processes

Sub‑micron 3D stacking technologies enable tighter pixel pitches and lower power consumption, making the solutions economically viable for mass‑market devices.

➤ Analysts project a compound annual growth rate of 12% for this market through 2032, driven by AI‑enabled imaging.

In addition, regulatory incentives for energy‑efficient components are prompting OEMs to adopt these sensors, further accelerating market expansion.

MARKET CHALLENGES

Complexity of Manufacturing Processes

The integration of pixel‑level ADCs within a stacked architecture requires precise alignment and yield management, increasing production costs for early adopters.

Other Challenges

Supply Chain Constraints

Limited availability of high‑purity silicon wafers and specialized bonding equipment can cause lead‑time delays.

Furthermore, design‑tool compatibility issues between sensor manufacturers and system integrators hinder rapid product development cycles.

MARKET RESTRAINTS

High Capital Expenditure

Establishing 3D‑stack fabrication lines demands significant upfront investment, which may deter smaller players from entering Chip-on-chip stacked image sensor with pixel-level ADC Market.

Limited Design Ecosystem

Current IP libraries and verification suites are not fully optimized for pixel‑level ADC integration, leading to longer development timelines and increased R&D costs.

Lastly, cost‑sensitivity in consumer electronics segments can restrain pricing power, slowing broader adoption despite technical advantages.

MARKET OPPORTUNITIES

Emergence of Edge AI Vision Systems

Edge AI platforms require on‑sensor processing to minimize latency. Pixel‑level ADCs enable direct digitization, opening opportunities for new form‑factors in drones and wearable cameras.

Expansion into Medical Imaging

High‑resolution, low‑noise sensors are critical for endoscopic and point‑of‑care imaging devices, presenting a growth corridor for Chip-on-chip stacked image sensor with pixel-level ADC Market.

Collaborations between semiconductor foundries and AI chipset vendors can unlock co‑design solutions, accelerating time‑to‑market and fostering ecosystem development.

Chip-on-chip stacked image sensor with pixel-level ADC Market Trends

Rising Adoption in Mobile and Automotive Imaging

Chip-on-chip stacked image sensor with pixel-level ADC Market is being driven by parallel growth in premium smartphones and advanced driver‑assistance systems. In 2025 total revenue reached roughly USD 0.84 billion, and industry forecasts show the market will climb to about USD 1.68 billion by 2034. Mobile OEMs are integrating stacked sensors to achieve higher resolution, greater dynamic range, and superior low‑light performance without enlarging module size. Simultaneously, automotive manufacturers are adopting these sensors for reliable vision in ADAS, where pixel‑level analog‑to‑digital conversion reduces latency and improves detection accuracy. The combined pressure from consumer photography expectations and safety‑critical automotive imaging creates a robust demand pipeline that sustains the market’s upward trajectory.

Other Trends

Advances in Pixel‑Level ADC Integration

Recent product launches illustrate the technical momentum behind Chip-on-chip stacked image sensor with pixel-level ADC Market. Sony’s IMX989 sensor and Samsung’s ISOCELL GM1 exemplify how integrating a dedicated ADC within each pixel boosts quantum efficiency beyond 70 % and expands dynamic range past 120 dB. These sensors also cut read‑out noise by up to 30 % compared with traditional front‑side illuminated designs. The architecture enables faster frame rates, which benefits industrial IoT cameras that require high‑speed image acquisition for quality control and robotics. As fabrication yields improve, cost per unit continues to decline, encouraging broader adoption across mid‑tier devices.

Strategic R&D and Partnerships

Key players are reinforcing Chip-on-chip stacked image sensor with pixel-level ADC Market through intensified research programs and collaborative alliances. Sony Semiconductor Solutions Corp., Samsung Electronics, OmniVision Technologies, and Himax Technologies have announced multi‑year investments aimed at miniaturizing the ADC circuitry and expanding pixel counts beyond 64 MP. Joint ventures with fab partners accelerate the transition to 28 nm and 14 nm process nodes, further enhancing power efficiency. These strategic moves not only diversify product portfolios but also create barriers to entry for emerging competitors, solidifying the market’s growth path over the next decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Chip‑on‑chip Stacked Image Sensor with Pixel‑Level ADC – Competitive Outlook 2025‑2034

The market is anchored by a few dominant semiconductor firms that integrate photodiode arrays with per‑pixel analog‑to‑digital converters. Sony Semiconductor Solutions Corp. leads the segment through its IMX989 sensor, which combines a backside‑illuminated silicon‑on‑insulator (SOI) pixel stack with 10‑bit ADCs, delivering industry‑leading quantum efficiency and dynamic range. Samsung Electronics Co., Ltd. follows closely with the ISOCELL GM1, leveraging a vertical‑stack architecture that targets premium smartphone cameras and advanced driver‑assistance systems (ADAS). Both companies benefit from deep R&D pipelines, extensive IP portfolios, and strong OEM relationships that enable rapid adoption across mobile, automotive, and industrial IoT applications. Their scale also allows aggressive pricing, reinforcing a high‑barrier‑to‑entry environment for new entrants.

Beyond the leaders, a cohort of specialized players expands the ecosystem. OmniVision Technologies and Himax Technologies focus on compact, low‑power stacked sensors for wearables and robotics, often partnering with Tier‑1 module makers. STMicroelectronics and ON Semiconductor bring proven automotive‑grade image processing expertise, targeting safety‑critical vision stacks. Canon Inc., Panasonic Corporation, Toshiba Corporation, Sharp Corp., and Sony’s own imaging subsidiary provide niche solutions for professional imaging and medical devices. Emerging entrants such as Ambarella, Galaxy Microsystems, and QTiQ (Qualcomm) are investing in next‑generation pixel‑level ADC designs, aiming to capture market share in high‑speed, high‑resolution use cases.

List of Key Chip-on-chip Stacked Image Sensor with Pixel-Level ADC Companies Profiled

- Sony Semiconductor Solutions Corp.

- Samsung Electronics Co., Ltd.

- OmniVision Technologies

- Himax Technologies

- STMicroelectronics

- ON Semiconductor

- Canon Inc.

- Panasonic Corporation

- Toshiba Corporation

- Sharp Corp.

- Ambarella

- Galaxy Microsystems

- Qualcomm (QTiQ)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Back‑Side Illuminated (BSI) Stacked Sensors are increasingly favored because they combine high quantum efficiency with the benefits of pixel‑level ADCs.

|

| By Application |

|

Smartphone Cameras dominate application demand as manufacturers chase ever‑higher resolution and low‑light capability.

|

| By End User |

|

Consumer Electronics Manufacturers lead end‑user adoption because they integrate sensors into devices that demand sleek designs and premium imaging experiences.

|

| By Integration Level |

|

3D‑IC TSV Integration is emerging as the preferred approach for high‑performance stacks.

|

| By Performance Feature |

|

Low‑Light/High‑Sensitivity Sensors drive differentiation across many applications.

|

Regional Analysis: North America

The automotive sector is a primary driver for chip-on-chip stacked image sensors with pixel-level ADC in North America. The integration of these sensors in advanced driver-assistance systems (ADAS) and autonomous driving technologies necessitates high-performance and compact imaging solutions. The stringent safety and reliability requirements of the automotive industry further fuel the demand for innovative sensor technologies.

The consumer electronics market in North America consistently seeks advanced imaging capabilities for smartphones, digital cameras, and wearables. The demand for higher resolution, improved low-light performance, and enhanced computational photography features is propelling the adoption of chip-on-chip stacked image sensors with pixel-level ADC in these devices.

The healthcare industry in North America is witnessing a growing need for sophisticated imaging systems for medical diagnostics and research. Chip-on-chip stacked image sensors with pixel-level ADC are finding applications in medical imaging devices, contributing to improved diagnostic accuracy and patient care.

Industrial automation, quality control, and surveillance systems are increasingly leveraging the capabilities of chip-on-chip stacked image sensors with pixel-level ADC for enhanced vision performance. These applications benefit from the compact size and high efficiency of these advanced sensors.

Europe

Europe presents a significant and steadily growing market for chip-on-chip stacked image sensors with pixel-level ADC. The region’s strong industrial base, particularly in automotive and consumer electronics, is fueling demand. Stringent data privacy regulations and a focus on sustainable technologies are also shaping the market dynamics in Europe. The European automotive sector is actively integrating advanced imaging systems into vehicles, driving adoption in this segment.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for chip-on-chip stacked image sensors with pixel-level ADC. The region’s burgeoning consumer electronics industry, particularly in China and India, is a major growth driver. The increasing adoption of smartphones and other connected devices, coupled with government initiatives promoting technological innovation, are contributing to market expansion. The Asia-Pacific region is also witnessing significant investments in advanced manufacturing capabilities, creating a favorable environment for chip-on-chip stacked image sensors with pixel-level ADC production.

South America

South America represents a developing market for chip-on-chip stacked image sensors with pixel-level ADC. The expanding consumer electronics market and growing automotive industry are creating opportunities for market players. However, economic fluctuations and varying levels of technological adoption across different countries in the region pose some challenges.

Middle East & Africa

The Middle East & Africa region is an emerging market with potential for growth in Chip-on-chip stacked image sensors with pixel-level ADC market. Investments in infrastructure development, particularly in transportation and security, are driving demand for advanced imaging solutions. The increasing adoption of smartphones and other consumer devices is also contributing to market expansion in this region.

Report Scope

This market research report provides a comprehensive analysis of the Chip-on-chip stacked image sensor with pixel-level ADC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chip-on-chip stacked image sensor with pixel-level ADC Market?

-> Chip-on-chip stacked image sensor with pixel-level ADC Market was valued at USD 0.84 billion in 2025 and is expected to reach USD 1.68 billion by 2034, growing at a CAGR of 7.5% during the forecast period.

Which key companies operate in Chip-on-chip stacked image sensor with pixel-level ADC Market?

-> Key players include Sony Semiconductor Solutions Corp., Samsung Electronics Co., Ltd., OmniVision Technologies, and Himax Technologies.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high‑resolution and low‑light smartphone cameras, automotive advanced driver‑assistance systems (ADAS) requiring reliable vision sensors, and industrial IoT applications demanding compact high‑speed imaging solutions.

Which region dominates the market?

-> The reference does not specify a dominant region; market growth is driven globally by smartphone, automotive, and industrial IoT segments.

What are the emerging trends?

-> Emerging trends include development of advanced sensors such as Sony’s IMX989 and Samsung’s ISOCELL GM1, integration of pixel‑level ADCs for improved performance, and ongoing R&D investments by leading manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...