MARKET INSIGHTS

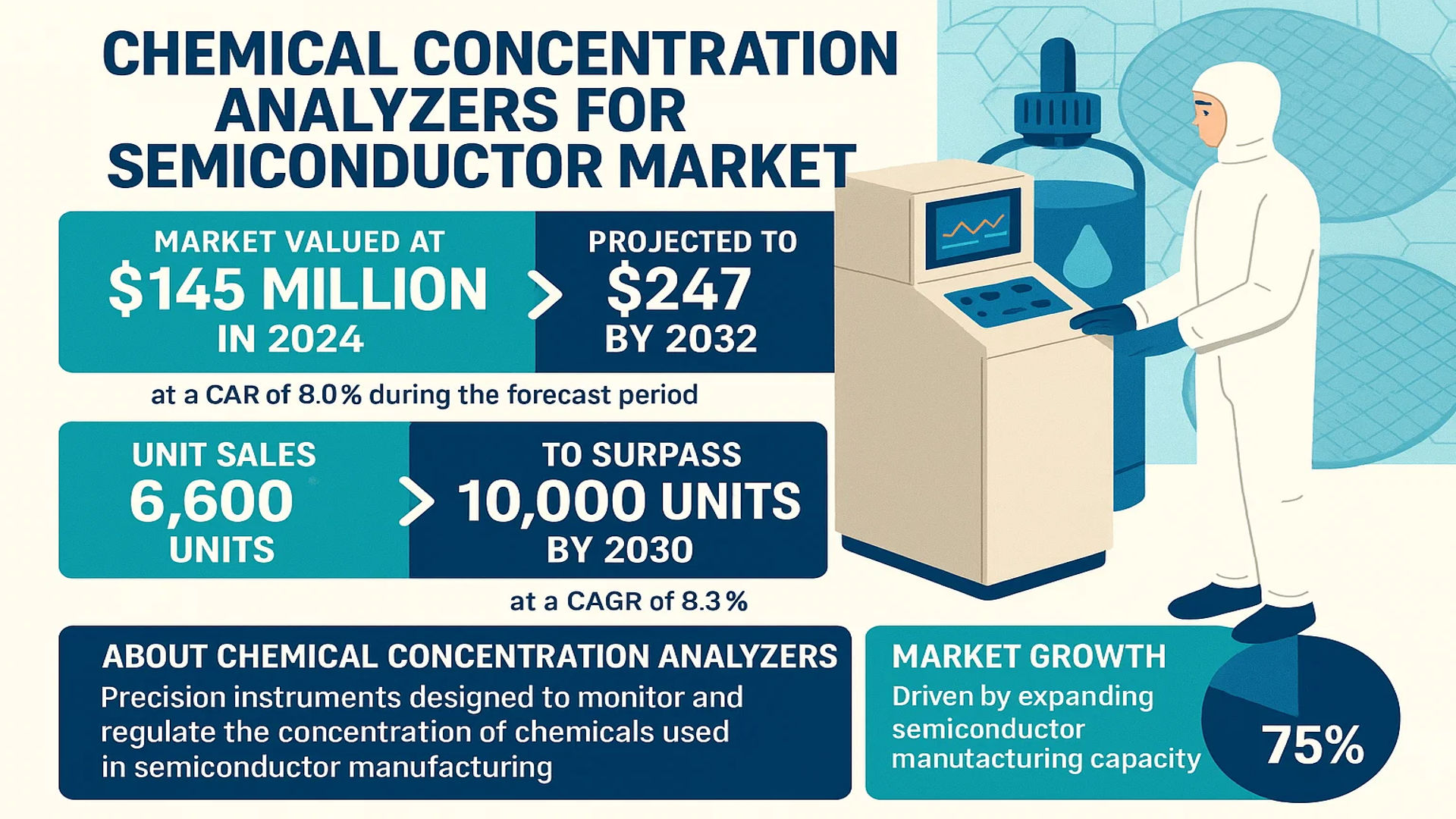

The global Chemical Concentration Analyzers for Semiconductor Market was valued at 145 million in 2024 and is projected to reach US$ 247 million by 2032, at a CAGR of 8.0% during the forecast period. Unit sales in this market reached 6,600 units in 2024, with projections indicating they will surpass 10,000 units by 2030 at a CAGR of 8.3%.

Chemical concentration analyzers for semiconductors are precision instruments designed to monitor and regulate the concentration of chemicals used in semiconductor manufacturing processes. These systems are critical for maintaining process consistency in key fabrication steps including wafer cleaning, etching, and deposition. Real-time concentration monitoring ensures optimal chemical performance, directly impacting product yield and quality in semiconductor production.

Market growth is primarily driven by expanding semiconductor manufacturing capacity globally, particularly in Asia-Pacific countries which accounted for 75% of 2024 revenues. The increasing complexity of semiconductor processes, coupled with stricter quality control requirements, has elevated demand for advanced analytical solutions. Leading manufacturers including HORIBA, Entegris, and KURABO INDUSTRIES dominate the market, collectively holding over 90% market share through their technologically advanced product portfolios.

MARKET DYNAMICS

MARKET DRIVERS

Surging Semiconductor Industry Demand to Accelerate Adoption

The semiconductor industry’s unprecedented growth, valued at over $620 billion in 2024, creates significant demand for precise chemical monitoring solutions. With logic chips and memory segments expanding by 21% and 61% respectively this year, manufacturing processes require tighter control than ever before. Chemical concentration analyzers have become indispensable for maintaining exact chemical proportions in etching and cleaning baths where nanometer-level precision directly impacts chip yields. The transition to 3nm and 2nm process nodes has increased sensitivity to chemical variations by approximately 40% compared to previous generations, making real-time concentration monitoring a production necessity rather than optional quality control.

Automation and Industry 4.0 Integration Driving Market Expansion

Smart factory initiatives in semiconductor fabrication plants are accelerating adoption rates for inline analyzers. Over 80% of analyzer sales in 2024 involve systems with industrial IoT connectivity, enabling predictive maintenance and autonomous process adjustments. Major foundries now mandate real-time data integration from chemical monitoring equipment into their Manufacturing Execution Systems (MES). This trend aligns with broader industry movements, as semiconductor facilities invest approximately 20% more annually in digital transformation compared to other high-tech manufacturing sectors. The ability of modern analyzers to provide instantaneous concentration feedback helps eliminate costly wafer losses that previously accounted for nearly 5% of production value.

Additionally, regulatory pressures are contributing to market growth:

➤ The semiconductor industry faces increasingly stringent environmental regulations regarding chemical usage and waste management, making accurate concentration monitoring both an operational and compliance requirement.

This dual pressure of technological necessity and regulatory demand creates a strong growth trajectory for advanced analyzer solutions through the forecast period.

MARKET RESTRAINTS

High Equipment Costs and ROI Concerns Limit Small-Scale Adoption

While essential for leading-edge fabs, chemical concentration analyzers present significant capital expenditure barriers. Advanced inline systems typically range between $50,000-$150,000 per unit, creating steep adoption curves for smaller manufacturers. Many facilities operating older process nodes (28nm and above) continue to rely on manual sampling methods, where labor costs remain below the break-even point for automation. The specialized nature of analyzer maintenance further complicates total cost of ownership calculations, as service contracts often add 15-20% annually to operational budgets.

Technical Implementation Challenges in Brownfield Facilities

Retrofitting existing fabrication lines presents multiple technical hurdles for analyzer integration. Older facilities frequently lack the digital infrastructure and physical space required for seamless implementation of modern monitoring systems. The industry estimates that nearly 40% of semiconductor plants built before 2010 require substantial modifications to support advanced chemical monitoring solutions. These retrofit projects often involve extended downtimes that production-conscious operators aim to minimize, creating friction in technology adoption timelines.

MARKET CHALLENGES

Measurement Accuracy in Next-Generation Process Chemicals

Emerging semiconductor chemistries present novel measurement challenges for analyzer manufacturers. The adoption of complex formulations for advanced nodes, including metal-organic compounds and low-concentration additives, exceeds the detection limits of many existing analyzer technologies. Modern etching solutions may contain active chemical components at concentrations below 0.1%, while remaining sensitive to fluctuations as small as 0.001%. This places extreme demands on sensor precision and calibration stability. Analyzer validation for new chemical formulations typically requires 6-12 months of rigorous testing before achieving production-grade reliability.

Additional Implementation Challenges

Material Compatibility Issues

Aggressive semiconductor processing chemicals accelerate corrosion in sensor components, reducing maintenance intervals and increasing total cost of ownership. Analyzer manufacturers must continuously develop new material solutions to keep pace with chemical innovation.

Data Integration Complexity

The lack of standardized communication protocols across different semiconductor equipment manufacturers creates integration bottlenecks. Custom interface development for each fab’s MES system accounts for approximately 30% of analyzer implementation costs.

MARKET OPPORTUNITIES

AI-Enhanced Predictive Analytics Creating New Value Propositions

Integration of machine learning algorithms transforms chemical concentration analyzers from monitoring devices to predictive process optimization tools. Advanced systems now correlate historical concentration data with wafer yield metrics to recommend optimal bath replacement schedules and process adjustments. Early adopters report chemical consumption reductions exceeding 15% through AI-driven optimization while maintaining equivalent quality standards. This technological evolution opens new business models where analyzer value extends beyond measurement to include tangible cost savings and sustainability benefits.

Geographic Expansion into Emerging Semiconductor Hubs

Government initiatives in multiple countries to build domestic semiconductor capabilities create substantial growth potential. Current projections indicate that capacity outside traditional hubs (USA, Taiwan, South Korea) will grow at nearly twice the industry average through 2030. These new facilities prioritize advanced process control from inception, presenting opportunities to establish analyzer technologies as foundational elements rather than retrofit solutions. Localization of service networks and technical support will be critical factors in capturing these emerging opportunities while maintaining required reliability standards.

CHEMICAL CONCENTRATION ANALYZERS FOR SEMICONDUCTOR MARKET TRENDS

Rising Demand for High-Performance Chips Fuels Market Expansion

The global semiconductor industry is experiencing unprecedented growth, primarily driven by the surge in demand for AI, HPC, and advanced consumer electronics. This growth necessitates precise manufacturing processes, where Chemical Concentration Analyzers for Semiconductors play a crucial role in maintaining process integrity. These analyzers ensure the accurate monitoring and control of chemical solutions used in etching, cleaning, and deposition – processes that define semiconductor performance. With the semiconductor market projected to reach $1 trillion by 2030, manufacturers are increasingly adopting advanced concentration analyzers to optimize yield and minimize defects, further propelling market demand.

Other Trends

Automation and Industry 4.0 Integration

As semiconductor fabs transition toward smart manufacturing, the demand for online concentration analyzers with real-time monitoring capabilities is surging. These systems automatically adjust chemical concentrations, reducing manual intervention and human errors. Currently, online analyzers dominate over 80% of the market, proving essential for maintaining strict process tolerances. The integration of IoT and AI into these systems allows predictive maintenance and dynamic process adjustments, significantly improving operational efficiency in high-volume production environments.

Geographic Shifts in Semiconductor Manufacturing

While Japan remains the production hub for concentration analyzers (contributing over 80% of global output), consumption is heavily concentrated in Asia-Pacific, accounting for 75% of revenue share. China’s rapid semiconductor capacity expansion is particularly noteworthy, representing 27% of regional demand in 2024. Meanwhile, the United States and Europe are witnessing renewed investments in domestic semiconductor production, which will likely create additional demand for precision chemical monitoring solutions in these regions over the coming decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Capabilities Amid Surging Semiconductor Demand

The global chemical concentration analyzers market for semiconductors demonstrates a highly concentrated structure, with Japanese manufacturers maintaining technological dominance. HORIBA emerges as the undisputed leader, capturing approximately 32% market share in 2024 through its proprietary laser-based measurement technologies. Their leadership stems from decades of specialization in analytical instrumentation and strategic partnerships with major foundries.

KURABO INDUSTRIES and Fuji Ultrasonic Engineering collectively hold about 45% market share, leveraging Japan’s advanced materials science ecosystem. These companies benefit from proximity to major semiconductor fabrication plants in Asia, enabling rapid product iteration cycles. Their ultrasonic measurement technologies have become industry standards for wet chemical process monitoring.

Meanwhile, Western players like Entegris and ABB are gaining traction through integrated solution offerings. Entegris particularly strengthens its position by combining concentration analysis with its semiconductor-grade chemical delivery systems, creating complete process control ecosystems. The company’s 2023 acquisition of a German sensor technology firm significantly enhanced its real-time monitoring capabilities.

Emerging competitors face substantial barriers to entry due to the need for semiconductor-grade reliability certifications and the industry’s preference for proven solutions. However, technology transitions toward advanced nodes below 5nm are creating opportunities for innovators capable of addressing new measurement challenges in extreme manufacturing environments.

List of Key Chemical Concentration Analyzer Companies

- HORIBA, Ltd. (Japan)

- Entegris, Inc. (U.S.)

- KURABO INDUSTRIES LTD. (Japan)

- ABB Ltd. (Switzerland)

- CI Semi (CI Systems) (Israel)

- Fuji Ultrasonic Engineering Co., Ltd. (Japan)

- SensoTech GmbH (Germany)

- PIMACS Pte. Ltd. (Singapore)

- Rhosonics BV (Netherlands)

Segment Analysis:

By Type

Contactless Type Segment Dominates Due to Non-Invasive Measurement and High Precision

The market is segmented based on type into:

- Contact Type

- Subtypes: Electrochemical, Conductivity-based, and others

- Contactless Type

- Subtypes: Ultrasonic, Optical, and others

By Application

Semiconductor Cleaning Segment Leads Due to Critical Need for Process Control

The market is segmented based on application into:

- Semiconductor Cleaning

- Subtypes: SC1 cleaning, SC2 cleaning, and others

- Semiconductor Etching

- Subtypes: Wet etching, Dry etching

- Others

By Technology

Ultrasonic Technology Gains Traction for Real-Time Concentration Monitoring

The market is segmented based on technology into:

- Ultrasonic

- Optical

- Electrochemical

- Others

By End User

Foundries Account for Majority Adoption Due to High Volume Production

The market is segmented based on end user into:

- Semiconductor Foundries

- IDMs (Integrated Device Manufacturers)

- Research Institutes

Regional Analysis: Chemical Concentration Analyzers for Semiconductor Market

Asia-Pacific

The Asia-Pacific region dominates the global market for Chemical Concentration Analyzers for Semiconductors, accounting for approximately 75% of global revenue share in 2024. This dominance is driven by massive semiconductor manufacturing hubs in countries like China, Japan, South Korea, and Taiwan. China alone represents 27% of regional demand, fueled by aggressive expansions in wafer fabrication plants and government initiatives like the “Made in China 2025” policy. While Japan remains a key production center with players like HORIBA and Fuji Ultrasonic Engineering, the region’s growth is increasingly propelled by emerging semiconductor ecosystems in Southeast Asia. The shift toward advanced nodes (below 10nm) and the booming AI chip demand are accelerating adoption of high-precision online analyzers across Asia-Pacific foundries.

North America

North America’s market is characterized by cutting-edge R&D and stringent quality requirements from leading semiconductor firms like Intel and Micron. The U.S. accounts for over 80% of regional demand, with the CHIPS Act’s $52 billion investment in domestic semiconductor production creating new opportunities for analyzer suppliers. While the region imports most equipment from Japan, local players like Entegris are strengthening their positions through advanced filtration-integrated monitoring solutions. The focus on compound semiconductors (GaN, SiC) and NASA/defense applications drives demand for specialized analyzers capable of handling exotic chemistries beyond traditional wet processes.

Europe

Europe maintains a technology leadership position in specialty semiconductor applications, particularly automotive and industrial IoT chips. German automotive semiconductor giants like Infineon and NXP are driving 15-20% annual growth in analyzer demand for cleaning/etching processes. The region benefits from strong collaborations between equipment makers (e.g., ABB, SensoTech) and research institutions under EU Horizon programs. However, the lack of leading-edge foundries limits market volume compared to Asia, pushing European manufacturers toward high-margin, customized solutions for MEMS and power devices where precision outweighs cost considerations.

South America

The South American market remains in nascent stages but shows potential with local assembly operations by major OEMs in Brazil and Mexico. While the region accounts for less than 3% of global demand, increasing investments in automotive electronics (particularly in Argentina’s lithium battery supply chain) are creating niche opportunities. Market growth is constrained by reliance on imported equipment and limited local semiconductor manufacturing infrastructure, though the trend toward nearshoring could stimulate future demand as global supply chains diversify.

Middle East & Africa

This emerging market is witnessing strategic investments in semiconductor back-end operations, particularly in Israel’s thriving fabless ecosystem and the UAE’s high-tech zones. Israel’s analyzer demand grew 12% YoY in 2024, driven by its strong position in imaging sensors and communication chips. While the region lacks front-end wafer fabs, its growing role in semiconductor packaging and testing creates opportunities for concentration monitoring in related chemical processes. Long-term growth potential exists through sovereign wealth fund investments in local semiconductor initiatives, though limited indigenous manufacturing currently caps market size.

Report Scope

This market research report provides a comprehensive analysis of the global Chemical Concentration Analyzers for Semiconductor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 145 million in 2024 and is projected to reach USD 247 million by 2032, growing at a CAGR of 8.0%.

- Segmentation Analysis: Detailed breakdown by product type (Contact Type, Contactless Type), application (Semiconductor Cleaning, Semiconductor Etching, Others), and end-user industry to identify high-growth segments and investment opportunities. In 2024, online-type analyzers dominated with over 80% market share.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific accounted for 75% of global revenue in 2024, with China, Japan, Taiwan, and South Korea as key contributors.

- Competitive Landscape: Profiles of leading market participants including HORIBA, Entegris, ABB, KURABO INDUSTRIES, and CI Semi (CI Systems), covering their product offerings, R&D focus, and recent developments. The top 5 players held over 90% market share in 2024.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of Industry 4.0 solutions, and evolving semiconductor fabrication standards. The semiconductor cleaning application segment held nearly 60% market share in 2024.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as AI chip demand and semiconductor industry expansion, along with challenges like supply chain constraints and technical barriers.

- Stakeholder Analysis: Insights for semiconductor equipment manufacturers, chemical suppliers, foundries, investors, and policymakers regarding strategic opportunities in this specialized market.

Primary and secondary research methods are employed, including interviews with industry experts, data from semiconductor associations, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Chemical Concentration Analyzers for Semiconductor Market?

-> Chemical Concentration Analyzers for Semiconductor Market was valued at 145 million in 2024 and is projected to reach US$ 247 million by 2032, at a CAGR of 8.0% during the forecast period.

Which key companies operate in this market?

-> Key players include HORIBA, Entegris, ABB, KURABO INDUSTRIES, CI Semi (CI Systems), Fuji Ultrasonic Engineering, and SensoTech, among others.

What are the key growth drivers?

-> Key growth drivers include rising semiconductor production, AI chip demand, and increasing need for precision in semiconductor manufacturing processes.

Which region dominates the market?

-> Asia-Pacific dominates with 75% revenue share, driven by semiconductor manufacturing hubs in China, Japan, Taiwan, and South Korea.

What are the emerging trends?

-> Emerging trends include real-time monitoring solutions, Industry 4.0 integration, and advanced chemical analysis technologies for next-generation semiconductor fabrication.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...