MARKET INSIGHTS

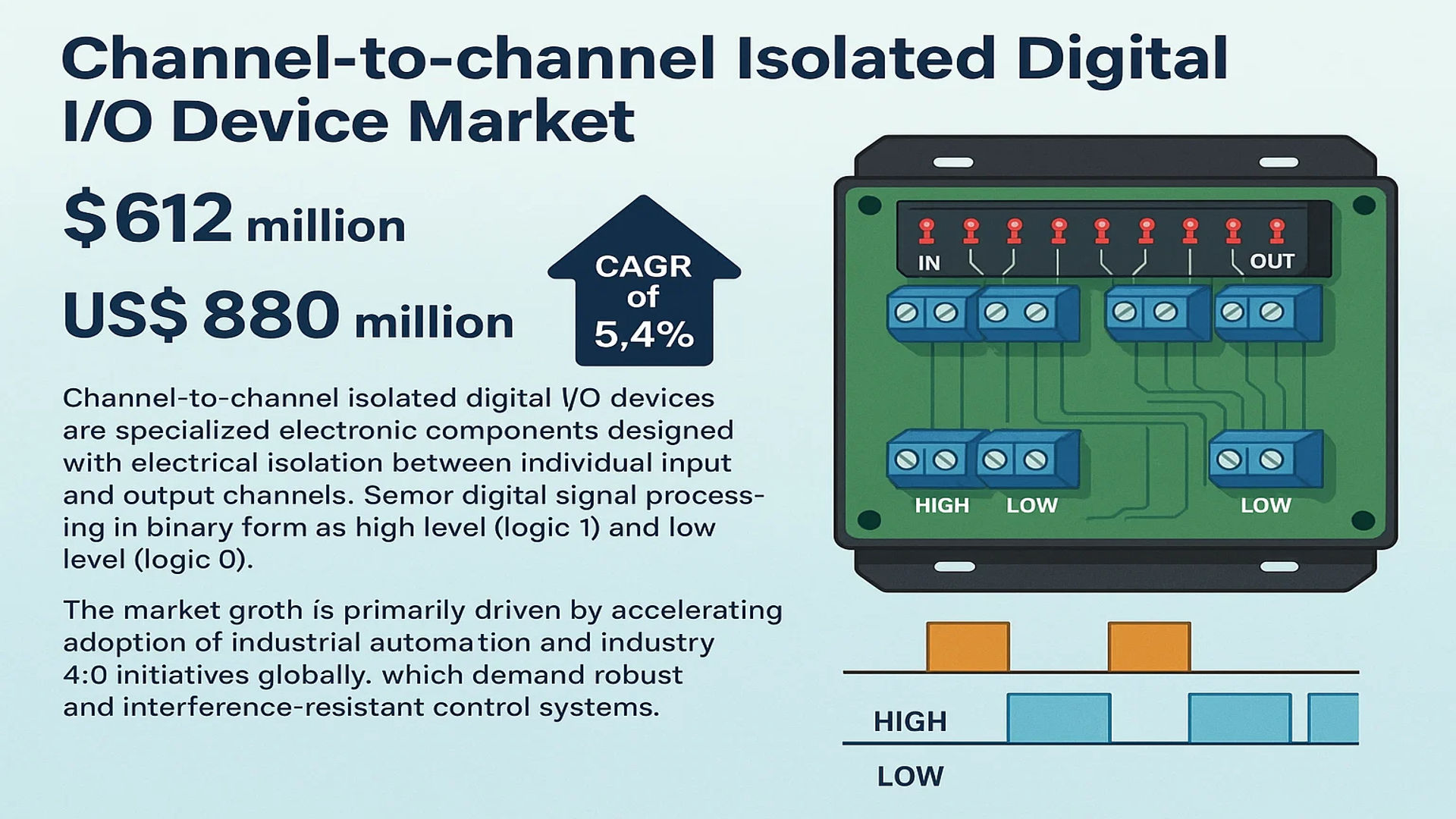

The global Channel-to-channel Isolated Digital I/O Device Market was valued at 612 million in 2024 and is projected to reach US$ 880 million by 2032, at a CAGR of 5.4% during the forecast period.

Channel-to-channel isolated digital I/O devices are specialized electronic components designed with electrical isolation between individual input and output channels. This isolation is a critical safety and performance feature, preventing signal interference, noise transmission, and potential electrical hazards to ensure each channel operates independently. These devices process digital signals, represented in binary form as high level (logic 1) and low level (logic 0), and are fundamental to applications requiring high reliability and noise immunity.

The market growth is primarily driven by the accelerating adoption of industrial automation and Industry 4.0 initiatives globally, which demand robust and interference-resistant control systems. Furthermore, the expansion of test and measurement equipment in R&D and the increasing complexity of medical and aerospace electronics are significant contributors. The optical coupling isolation segment is anticipated to be a major growth driver. Key market players, including NI, Keysight Technologies, and Advantech, continue to innovate, with recent developments focusing on higher channel density and improved isolation voltages to meet evolving industry standards.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation to Propel Market Growth

The global industrial automation sector is experiencing robust growth, driven by the increasing adoption of Industry 4.0 technologies and smart manufacturing practices. Channel-to-channel isolated digital I/O devices are critical components in automation systems, providing essential electrical isolation to prevent signal interference, enhance safety, and ensure operational reliability in harsh industrial environments. The market for industrial automation is projected to grow significantly, with investments in automation technologies exceeding $400 billion annually. These devices are widely used in programmable logic controllers (PLCs), distributed control systems (DCS), and human-machine interfaces (HMIs) to manage digital signals accurately. The demand for higher efficiency, reduced downtime, and improved productivity in manufacturing processes is accelerating the integration of isolated digital I/O solutions. For instance, the automotive and electronics industries rely heavily on these devices for precision control and data acquisition, contributing to market expansion.

Rising Demand in Test and Measurement Applications to Boost Adoption

Test and measurement applications represent a major growth area for channel-to-channel isolated digital I/O devices, particularly in sectors such as telecommunications, electronics, and aerospace. These devices ensure signal integrity and accuracy in high-noise environments, which is crucial for reliable data acquisition and control systems. The global test and measurement equipment market is valued at over $30 billion, with a compound annual growth rate of approximately 5.5%. Isolated digital I/O devices are integral to automated test equipment (ATE), benchtop instruments, and data loggers, where they provide galvanic isolation to protect sensitive components from voltage spikes and ground loops. The proliferation of 5G infrastructure, IoT devices, and electric vehicles is further driving the need for advanced testing solutions, thereby increasing the demand for high-performance isolated I/O devices. Additionally, stringent regulatory standards for product quality and safety are encouraging manufacturers to adopt these isolation technologies.

Advancements in Medical Equipment to Fuel Market Growth

The medical equipment sector is increasingly utilizing channel-to-channel isolated digital I/O devices to enhance patient safety and device reliability. Medical devices such as patient monitors, diagnostic imaging systems, and therapeutic equipment require high levels of electrical isolation to prevent leakage currents and protect patients from electrical hazards. The global medical device market is expanding rapidly, with revenues surpassing $500 billion, driven by an aging population and rising healthcare expenditures. Isolated digital I/O devices are essential in ensuring compliance with international safety standards, such as IEC 60601-1, which mandates stringent isolation requirements. For example, in MRI machines and ultrasound systems, these devices help maintain signal accuracy while isolating sensitive electronic components from high voltages. The ongoing innovation in portable and wireless medical devices is also creating new opportunities for compact and efficient isolation solutions.

Moreover, the increasing focus on telehealth and remote patient monitoring is expected to further drive the adoption of these devices in the healthcare sector.

➤ For instance, regulatory agencies worldwide are emphasizing the importance of electrical safety in medical devices, leading to greater integration of isolation technologies in new product designs.

Furthermore, the trend towards miniaturization and energy efficiency in electronic components is encouraging manufacturers to develop advanced isolated digital I/O devices with higher channel density and lower power consumption.

MARKET CHALLENGES

High Cost of Advanced Isolation Technologies to Impede Market Penetration

While channel-to-channel isolated digital I/O devices offer significant benefits, their high cost remains a substantial barrier to widespread adoption, especially in price-sensitive markets and small to medium-sized enterprises. Advanced isolation technologies, such as optical coupling and magnetic isolation, involve complex manufacturing processes and high-quality materials, leading to increased production expenses. The average cost of high-performance isolated digital I/O modules can be 30-50% higher than non-isolated alternatives, making them less accessible for budget-constrained applications. This cost factor is particularly challenging in emerging economies, where industries may prioritize affordability over advanced features. Additionally, the need for rigorous testing and certification to meet international safety standards adds to the overall cost, further limiting market growth in certain segments.

Other Challenges

Technical Complexity in Integration

Integrating channel-to-channel isolated digital I/O devices into existing systems can be technically challenging, requiring specialized knowledge and expertise. Design engineers must carefully consider factors such as isolation voltage, channel density, signal speed, and power consumption to ensure compatibility and optimal performance. The complexity increases in multi-channel applications where cross-talk and noise immunity are critical concerns. This technical barrier can slow down adoption rates, as companies may need to invest in additional training or hire skilled personnel, adding to the overall cost and time of implementation.

Supply Chain Disruptions

The global electronics supply chain has faced significant disruptions in recent years, affecting the availability of key components such as semiconductors and isolation materials. These disruptions can lead to extended lead times, increased prices, and production delays for isolated digital I/O devices. Industries reliant on just-in-time manufacturing, such as automotive and consumer electronics, are particularly vulnerable to these challenges, potentially hindering market growth and adoption rates.

MARKET RESTRAINTS

Limited Standardization and Compatibility Issues to Hinder Market Expansion

The lack of universal standards for channel-to-channel isolated digital I/O devices can create compatibility issues, restraining market growth. Different manufacturers often use proprietary designs and communication protocols, making it difficult to integrate devices from multiple vendors into a single system. This fragmentation can lead to increased complexity, higher costs, and longer development cycles for end-users. Industries such as industrial automation and test and measurement require seamless interoperability between devices to ensure system reliability and efficiency. Without widely adopted standards, companies may hesitate to invest in these technologies, particularly in multi-vendor environments. Furthermore, the rapid pace of technological innovation means that existing devices may become obsolete quickly, adding to the challenges of long-term system planning and investment.

Additionally, the varying isolation requirements across different applications and regions complicate the design and certification processes. For example, medical devices must comply with stringent safety standards, while industrial equipment may have different regulatory needs. This diversity in requirements can slow down product development and limit the ability of manufacturers to offer universal solutions.

Moreover, the need for continuous firmware updates and software support to maintain compatibility with evolving systems can place a burden on both manufacturers and end-users, potentially deterring adoption in cost-sensitive markets.

MARKET OPPORTUNITIES

Growth in Renewable Energy and Electric Vehicles to Create New Avenues for Market Expansion

The renewable energy and electric vehicle (EV) sectors are emerging as significant growth opportunities for channel-to-channel isolated digital I/O devices. In renewable energy systems, such as solar inverters and wind turbine controllers, these devices are essential for managing power conversion, monitoring system performance, and ensuring safety through electrical isolation. The global renewable energy market is projected to grow at a compound annual growth rate of over 8%, with investments reaching $2 trillion annually by 2030. Similarly, the electric vehicle market is expanding rapidly, with sales expected to exceed 30 million units per year by the end of the decade. Isolated digital I/O devices play a critical role in EV charging infrastructure, battery management systems, and onboard electronics, where they provide reliable signal isolation and noise immunity. The increasing emphasis on energy efficiency and carbon reduction is driving innovation in these sectors, creating demand for advanced isolation technologies.

Additionally, government initiatives and subsidies promoting clean energy and transportation are accelerating the adoption of these technologies. For example, many countries are investing in smart grid infrastructure and fast-charging networks for electric vehicles, which require robust isolated I/O solutions for safe and efficient operation.

Furthermore, advancements in wide-bandgap semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), are enabling higher efficiency and power density in energy systems, which in turn drives the need for compatible isolated digital I/O devices capable of operating at higher voltages and temperatures.

CHANNEL-TO-CHANNEL ISOLATED DIGITAL I/O DEVICE MARKET TRENDS

Industry 4.0 and Smart Manufacturing to Emerge as a Trend in the Market

The global push towards Industry 4.0 and smart manufacturing is significantly accelerating the adoption of channel-to-channel isolated digital I/O devices. These components are fundamental to modern automation systems, providing the necessary electrical isolation to ensure data integrity and operational safety in harsh industrial environments. With manufacturing facilities increasingly integrating IoT sensors, robotics, and complex control systems, the demand for reliable signal interfacing has surged. The market is responding with devices offering higher channel densities, faster data rates exceeding 100 Mbps, and enhanced noise immunity. This trend is particularly strong in the automotive and electronics manufacturing sectors, where production line uptime and precision are paramount. Furthermore, the rise of predictive maintenance strategies, which rely on continuous data acquisition from equipment, is creating sustained demand for these robust I/O solutions.

Other Trends

Advancements in Isolation Technology

Continuous innovation in isolation technologies is a primary driver for market evolution and performance enhancement. While optical coupling remains a dominant method, accounting for a significant portion of the market, newer technologies like magnetic and capacitive coupling are gaining traction. These advanced methods offer superior performance in terms of speed, power consumption, and longevity. Magnetic coupling isolation, for instance, provides robust noise immunity and high common-mode transient immunity, making it ideal for motor control and power conversion applications. The development of integrated isolated digital I/O solutions that combine the isolator and the interface circuitry into a single package is also a key trend, reducing board space and simplifying system design for end-users.

Expansion in Test and Measurement and Medical Applications

The test and measurement sector, along with the medical equipment industry, represents a high-growth application area for these devices. In test and measurement, the need for accurate data acquisition from multiple points without cross-talk is critical. Isolated digital I/O devices are essential in automated test equipment (ATE) for semiconductor validation, board-level testing, and scientific instrumentation. In the medical field, patient safety regulations mandate high levels of electrical isolation in equipment. Devices used in patient monitoring systems, diagnostic imaging, and therapeutic equipment require reliable isolation to protect patients from electrical hazards. The increasing automation of laboratory processes and the development of more sophisticated diagnostic machines are further propelling the demand in these verticals.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on Technological Innovation and Strategic Expansion

The global channel-to-channel isolated digital I/O device market features a semi-consolidated competitive structure, with a mix of established multinational corporations and specialized regional players competing for market share. This landscape is characterized by intense competition driven by technological innovation, product reliability, and application-specific solutions. While the top five players collectively held a significant portion of the market revenue in 2024, numerous medium and small-sized companies continue to thrive by addressing niche applications and regional demands.

National Instruments (NI) emerges as a dominant force in this market, particularly within the test and measurement segment. Their position is strengthened by their comprehensive software-hardware ecosystem and strong brand recognition among engineering professionals. The company’s recent focus on Platform-Based Design and integration with industry-standard software environments has allowed them to maintain technological leadership. Meanwhile, Keysight Technologies and Analog Devices, Inc. have solidified their positions through extensive R&D investments in high-performance isolation technologies and signal integrity solutions. Both companies benefit from their broad product portfolios that cater to diverse industrial and laboratory applications.

The competitive dynamics are further influenced by regional specialists who have developed strong footholds in their respective markets. Advantech and ADLINK Technology have demonstrated remarkable growth in the Asian market, particularly in industrial automation applications, leveraging their cost-competitive solutions and extensive distribution networks. European players including Phoenix Contact and Weidmüller maintain strong positions in industrial control applications, where their expertise in ruggedized designs and industry certifications provides competitive advantages in demanding environments.

Recent competitive developments highlight strategic shifts toward integrated solutions and industry-specific offerings. Several leading players have expanded their portfolios through both organic development and strategic acquisitions, aiming to provide complete signal chain solutions rather than standalone I/O devices. This trend is particularly evident in the medical equipment and aerospace segments, where companies are developing application-certified products that reduce integration complexity for end-users. Furthermore, the increasing demand for higher channel density and lower power consumption has driven innovation cycles, with companies racing to introduce next-generation products that address these evolving requirements.

The competitive intensity is expected to increase during the forecast period as industrial automation continues to evolve toward Industry 4.0 standards and IIoT implementations. Companies are investing significantly in developing products with enhanced cybersecurity features, better diagnostic capabilities, and improved interoperability with cloud platforms. While technological innovation remains the primary competitive differentiator, factors such as global distribution networks, technical support capabilities, and brand reputation continue to play crucial roles in market positioning.

List of Key Channel-to-channel Isolated Digital I/O Device Companies Profiled

- National Instruments (NI) (U.S.)

- Keysight Technologies (U.S.)

- Agilent Technologies, Inc. (U.S.)

- ADLINK Technology Inc. (Taiwan)

- Advantech Co., Ltd. (Taiwan)

- Contec Co., Ltd. (Japan)

- Analog Devices, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Phoenix Contact GmbH & Co. KG (Germany)

- Weidmüller Interface GmbH & Co. KG (Germany)

- Beckhoff Automation GmbH & Co. KG (Germany)

- Rockwell Automation, Inc. (U.S.)

- Novosense Microelectronics (China)

Segment Analysis:

By Type

Optical Coupling Isolation Segment Dominates the Market Due to Superior Noise Immunity and High Reliability

The market is segmented based on type into:

- Optical Coupling Isolation

- Transformer Isolation

- Capacitive Coupling Isolation

- Magnetic Coupling Isolation

By Application

Industrial Automation Segment Leads Due to Critical Need for Signal Integrity in Harsh Environments

The market is segmented based on application into:

- Industrial Automation

- Test and Measurement

- Medical Equipment

- Aerospace

- Other

By End User

Manufacturing Sector Holds Largest Share Owing to Extensive Adoption in Process Control and Factory Automation

The market is segmented based on end user into:

- Manufacturing

- Healthcare

- Telecommunications

- Energy and Utilities

- Research and Development

By Channel Count

Medium-Density Channels (8-32) Represent Key Segment Balancing Performance and Cost Efficiency

The market is segmented based on channel count into:

- Low-Density (1-8 channels)

- Medium-Density (8-32 channels)

- High-Density (32+ channels)

Regional Analysis: Channel-to-channel Isolated Digital I/O Device Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global Channel-to-channel Isolated Digital I/O Device market, accounting for the largest market share by volume and value. This leadership is primarily fueled by China’s massive manufacturing and industrial automation sector, which consumes a significant volume of these components for factory automation, robotics, and process control systems. Japan and South Korea are also major contributors, driven by their advanced electronics and automotive industries that demand high-reliability isolation for test and measurement applications. While cost sensitivity remains a key purchasing factor, leading to strong demand for optical coupling isolation types, there is a growing, albeit gradual, shift towards more advanced isolation technologies like capacitive and magnetic coupling to support the region’s push into higher-value manufacturing and next-generation industrial IoT infrastructure.

North America

The North American market is characterized by high-value, technologically advanced demand, particularly from the United States. This region is a hub for innovation in sectors like aerospace, defense, and medical equipment, which require the highest levels of signal integrity, safety, and reliability. Stringent regulatory standards, such as those from the FDA for medical devices and FAA for aerospace, mandate the use of robust isolation solutions, driving adoption beyond basic optical isolation to include transformer and magnetic coupling technologies. Furthermore, significant investments in modernizing manufacturing through initiatives like Industry 4.0 and reshoring efforts are creating sustained demand for these devices to ensure system robustness and cybersecurity in smart factories.

Europe

Europe represents a mature and stable market for Channel-to-channel Isolated Digital I/O Devices, with demand being heavily influenced by strict EU-wide industrial safety and EMC (Electromagnetic Compatibility) directives. Germany, as the continent’s industrial powerhouse, is the largest consumer, utilizing these devices extensively in automotive manufacturing, mechanical engineering, and renewable energy systems. The market is defined by a strong preference for high-quality, reliable products from established European suppliers, with a significant focus on compliance and certification. The push towards industrial digitalization and green energy transitions, such as those outlined in the European Green Deal, is further propelling the need for isolated I/O in smart grid and automation applications, ensuring long-term market stability.

South America

The market in South America is emerging and is primarily driven by basic industrial automation and infrastructure development in countries like Brazil and Argentina. Economic volatility and currency fluctuations often constrain capital expenditure, leading to a price-sensitive market where cost-effective optical isolation solutions are predominantly sought after. While the mining, oil & gas, and food processing industries present opportunities for these devices to protect control systems, the adoption of more advanced isolation technologies is slow. Growth is further hindered by fragmented regulatory landscapes and a reliance on imported components, making the market susceptible to supply chain disruptions and limiting its overall expansion potential in the short to medium term.

Middle East & Africa

This region presents a nascent but growing market opportunity, largely centered around oil & gas, utility, and infrastructure projects in the Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE. The primary driver is the need for durable and reliable equipment that can withstand harsh environmental conditions in these sectors, creating demand for isolated digital I/O devices to ensure operational safety and prevent signal interference. However, the market’s development is uneven across the broader region, often hampered by limited local manufacturing capabilities, reliance on imports, and a general lag in adopting advanced industrial automation compared to other regions. While long-term potential exists with ongoing economic diversification plans, the current market volume remains relatively low.

Report Scope

This market research report provides a comprehensive analysis of the global Channel-to-channel Isolated Digital I/O Device market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Channel-to-channel Isolated Digital I/O Device Market?

-> Channel-to-channel Isolated Digital I/O Device Market was valued at 612 million in 2024 and is projected to reach US$ 880 million by 2032, at a CAGR of 5.4% during the forecast period.

Which key companies operate in Global Channel-to-channel Isolated Digital I/O Device Market?

-> Key players include NI, Keysight Technologies, Agilent, ADLINK, Advantech, Contec, Analog Devices, Infineon, Phoenix Contact, and Weidmüller, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for robust safety systems in critical applications, and advancements in semiconductor isolation technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by manufacturing expansion, while North America remains a dominant market due to high adoption in aerospace and defense sectors.

What are the emerging trends?

-> Emerging trends include integration with IIoT platforms, miniaturization of devices, and development of higher channel density modules with enhanced isolation capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...