Market Insights

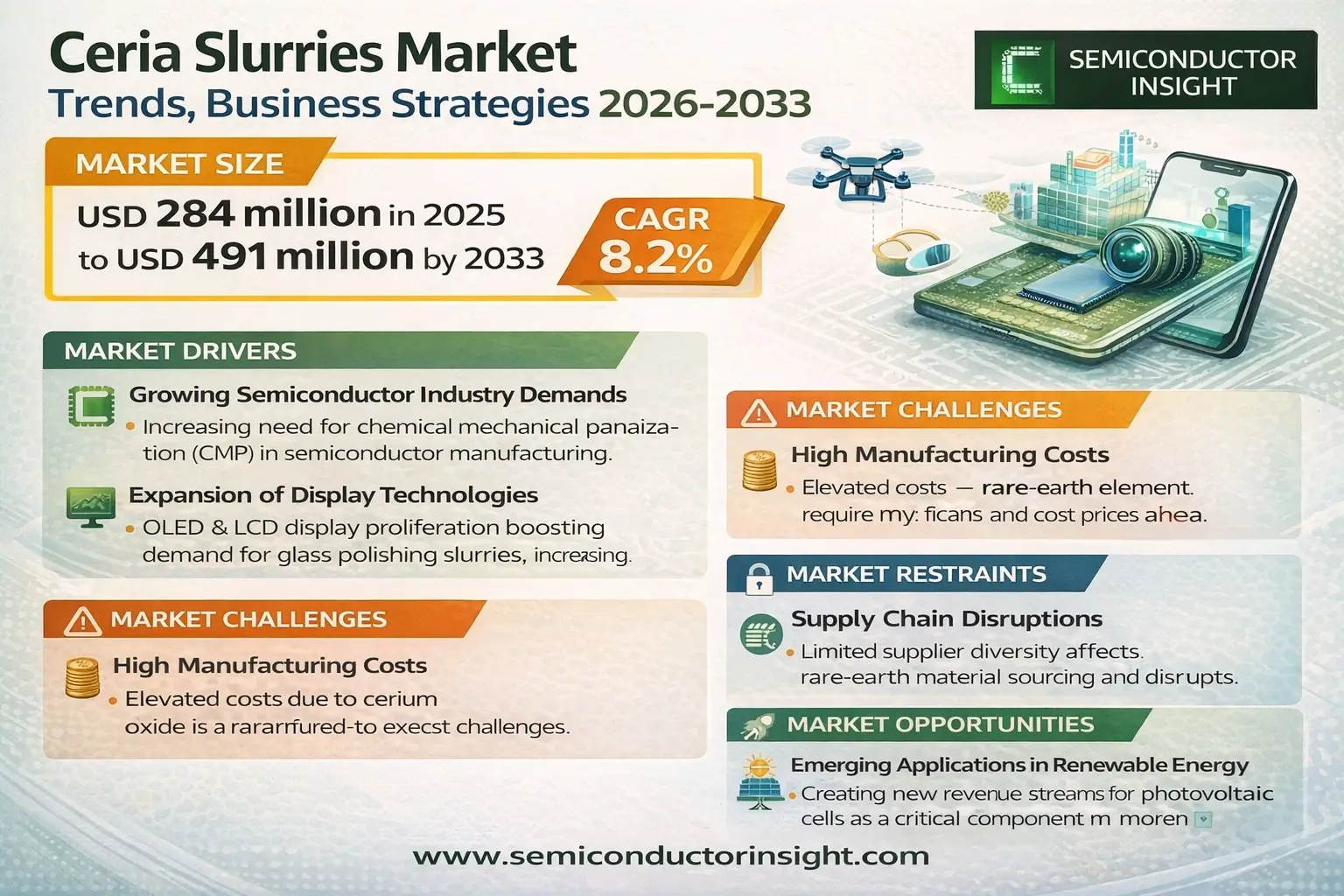

Global Ceria Slurries Market was valued at USD 284 million in 2024 and is projected to reach USD 491 million by 2032, at a CAGR of 8.2% during the forecast period. The growth is driven by increasing demand in semiconductor manufacturing, particularly for advanced integrated circuit (IC) fabrication processes.

Ceria slurries are critical materials used in chemical mechanical planarization (CMP), a precision polishing technique essential for semiconductor wafer production. These slurries consist of cerium oxide (CeO₂) particles suspended in a liquid medium, enabling high-performance surface planarization with minimal defects. The particle size distribution and chemical composition are optimized for specific applications, such as shallow trench isolation (STI) and interlayer dielectric (ILD) polishing.

The market expansion is fueled by rising semiconductor production, especially in Asia-Pacific regions like China and South Korea. In 2024, the top four global players Resonac, Merck KGaA, AGC, and KC Tech collectively held an 84% revenue share. Meanwhile, emerging Chinese manufacturers such as Hubei Dinglong and Konfoong Materials International are gaining traction due to localized supply chain advantages. Colloidal ceria slurries dominate the product segment with a 77.17% market share owing to their superior stability and polishing efficiency.

MARKET DRIVERS

Growing Semiconductor Industry Demands

Global Ceria Slurries Market is witnessing significant growth due to increasing demand from the semiconductor industry. Ceria slurries are essential for chemical mechanical planarization (CMP) processes, which are critical in semiconductor manufacturing. With the rising production of advanced chips and wafers, the need for high-quality Ceria Slurries is accelerating.

Expansion of Display Technologies

The proliferation of OLED and LCD displays in consumer electronics is driving the demand for Ceria Slurries, particularly for glass polishing applications. Manufacturers are investing heavily in R&D to produce more efficient slurries that enhance precision in display production.

Additionally, the rise of smart devices and IoT technologies has further amplified the need for ultra-precise polishing materials, positioning Ceria Slurries as a critical component in modern manufacturing.

MARKET CHALLENGES

High Manufacturing Costs

One of the primary challenges in the Ceria Slurries Market is the high cost of raw materials and production processes. Ceria (cerium oxide) is a rare-earth element, and its extraction and refinement require significant investment, leading to elevated product prices.

Other Challenges

Environmental Regulations

Strict environmental policies regarding the disposal and handling of Ceria Slurries pose compliance challenges for manufacturers, particularly in regions with stringent waste management laws.

MARKET RESTRAINTS

Supply Chain Disruptions

Ceria Slurries Market faces constraints due to geopolitical tensions and supply chain vulnerabilities affecting rare-earth material sourcing. Limited supplier diversity and transportation bottlenecks further exacerbate these challenges, impacting market stability.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy

The integration of Ceria Slurries in solar panel manufacturing presents a significant growth opportunity. As the renewable energy sector expands, the demand for high-performance polishing materials for photovoltaic cells is expected to rise, creating new revenue streams for Ceria Slurries producers.

Ceria Slurries Market Trends

Rapid Growth in Semiconductor Industry Driving Demand

Global Ceria Slurries Market was valued at USD 284 million in 2024 and is projected to reach USD 491 million by 2032, growing at a CAGR of 8.2%. This growth is primarily driven by the expanding semiconductor industry, which recorded USD 627.6 billion in sales in 2024, a 19.1% increase from 2023. As Ceria Slurries are critical for chemical mechanical planarization (CMP) processes in chip manufacturing, the booming semiconductor demand directly impacts slurry consumption.

Other Trends

Market Consolidation Among Key Players

The top four companies – Resonac, Merck KGaA, AGC, and KC Tech – collectively hold 84% of the Ceria Slurries Market revenue as of 2024. This concentration indicates high barriers to entry and strong technological expertise required in slurry production. Recent industry surveys show these players are actively investing in R&D to improve slurry formulations for advanced semiconductor nodes.

Chinese Market Emergence

Chinese manufacturers like Hubei Dinglong and Konfoong Materials are becoming increasingly competitive, signaling a potential shift in the market landscape. Local players currently focus on cost-competitive colloidal ceria slurries, which dominate 77.17% of the product segment. Industry analysts predict Chinese companies will capture greater market share in the next six years.

Application-Specific Demand Patterns

Over 95% of Ceria Slurries are used in Shallow Trench Isolation (STI) and Interlayer Dielectric (ILD) processes. With logic chips (sales of USD 212.6 billion in 2024) and memory chips (USD 165.1 billion) requiring different slurry specifications, manufacturers are developing specialized formulations. The DRAM segment’s 82.6% sales growth in 2024 indicates particular opportunities for Ceria Slurry optimization in memory production.

COMPETITIVE LANDSCAPEKey Industry Players

Ceria Slurries Market Dominated by Global Specialists with Emerging Chinese Challengers

Ceria Slurries Market exhibits a concentrated structure with Resonac, Merck KGaA, AGC, and KC Tech collectively commanding 84% revenue share in 2024. These established players dominate through advanced R&D capabilities and long-term semiconductor industry partnerships. Japanese and South Korean manufacturers maintain competitive advantages in colloidal slurry formulation, particularly for advanced node STI/ILD applications. The market’s high technical barriers create significant challenges for new entrants in meeting the stringent purity and particle size distribution requirements of leading foundries.

China’s rapid semiconductor expansion has spurred domestic slurry production, with firms like Anjimirco Shanghai and Hubei Dinglong gaining market share through government-supported initiatives. The competitive landscape is evolving with increasing M&A activity, as evidenced by Merck’s acquisition of Versum Materials. Regional dynamics show American and European suppliers focusing on premium-grade products while Asian manufacturers compete aggressively on both quality and pricing across the value chain.

List of Key Ceria Slurries Companies Profiled

- Resonac (formerly Hitachi Chemical)

- Merck KGaA

- AGC Inc.

- KC Tech

- Anjimirco Shanghai

- Soulbrain

- Dongjin Semichem

- Samsung SDI

- Saint-Gobain

- Ferro (UWiZ Technology)

- Hubei Dinglong

- Konfoong Materials International

- Zhuhai Cornerstone Technologies

- CHUANYAN

- Fujimi Incorporated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Colloidal Ceria Slurry dominates the market due to:

|

| By Application |

|

STI/ILD CMP accounts for overwhelming majority of demand because:

|

| By End User |

|

Semiconductor Foundries represent the largest consumer segment due to:

|

| By Manufacturing Process |

|

Front-end CMP processes dominate consumption patterns because:

|

| By Material Purity |

|

High Purity (4N+) grades show strongest growth owing to:

|

Regional Analysis: Ceria Slurries Market

Asia-Pacific (Leading Region)

Taiwan’s Semiconductor Stronghold

Taiwan’s semiconductor ecosystem drives premium Ceria Slurries demand with TSMC and other foundries requiring high-purity polishing solutions for advanced nodes below 7nm.

South Korea’s Memory Market

South Korean memory chip manufacturers utilize specialty Ceria formulations for 3D NAND flash production, creating consistent high-volume demand for advanced polishing materials.

China’s Expanding Production

China’s semiconductor self-sufficiency push significantly boosts domestic Ceria Slurries consumption, with new fabs requiring local supply chain solutions for polishing applications.

Japan’s Material Science Edge

Japanese chemical companies develop proprietary Ceria Slurry formulations with superior particle size control for advanced semiconductor and optical polishing applications.

North America

North America maintains significant Ceria Slurries demand through semiconductor research facilities and specialty IC manufacturers. The region’s focus on advanced packaging technologies creates opportunities for next-generation slurry formulations. Major semiconductor equipment companies collaborate with material suppliers to develop customized Ceria solutions for emerging applications in AI and high-performance computing chips. The U.S. government’s CHIPS Act investments are expected to strengthen domestic semiconductor production and associated material needs including polishing slurries.

Europe

Europe’s Ceria Slurries Market benefits from specialty semiconductor production and automotive electronics demand. Leading chemical companies focus on high-purity formulations for MEMS and power device manufacturing. The region’s strong automotive sector drives demand for polishing materials used in sensor and power electronics production. Collaborative R&D between academic institutions and material suppliers fosters innovation in environmentally friendly slurry technologies for semiconductor applications.

South America

South America’s emerging electronics manufacturing sector shows growing interest in Ceria Slurries, primarily for consumer electronics production. Brazil’s developing semiconductor packaging industry creates new demand channels for polishing materials. The region focuses on cost-effective slurry solutions for medium-grade semiconductor applications, with increasing imports from global suppliers.

Middle East & Africa

The Middle East demonstrates nascent potential in Ceria Slurries adoption through strategic technology investments. Growing semiconductor testing and packaging facilities in UAE and Saudi Arabia require polishing materials for specialized applications. Africa’s developing electronics repair sector shows preliminary demand for entry-level Ceria Slurries in component refurbishment processes.

Report Scope

This market research report provides a comprehensive analysis of the Ceria Slurries Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Ceria Slurries Market?

-> Ceria Slurries Market was valued at USD 284 million in 2024 and is projected to reach USD 491 million by 2032, at a CAGR of 8.2% during the forecast period.

What is the growth rate (CAGR) of the Ceria Slurries Market?

-> The market is expected to grow at a CAGR of 8.2% during the forecast period (2024-2032).

Which key companies operate in Ceria Slurries Market?

-> Key players include Resonac, Merck KGaA, AGC, KC Tech, Soulbrain, and Anjimirco Shanghai, with the top four companies holding approximately 84% market share in 2024.

What are the main product segments in this market?

-> In 2024, Colloidal Ceria Slurry held 77.17% market share, while Calcined Ceria Slurry accounted for 22.83%.

What are the primary applications of Ceria Slurries?

-> Currently, STI and ILD processes dominate the market with over 95% share of applications.

Which region has the most active Ceria Slurries Market?

-> The Chinese market is very active with new entrants like Hubei Dinglong, Konfoong Materials International, Zhuhai Cornerstone Technologies and CHUANYAN driving future growth.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...